Quick Navigation

Report Overview

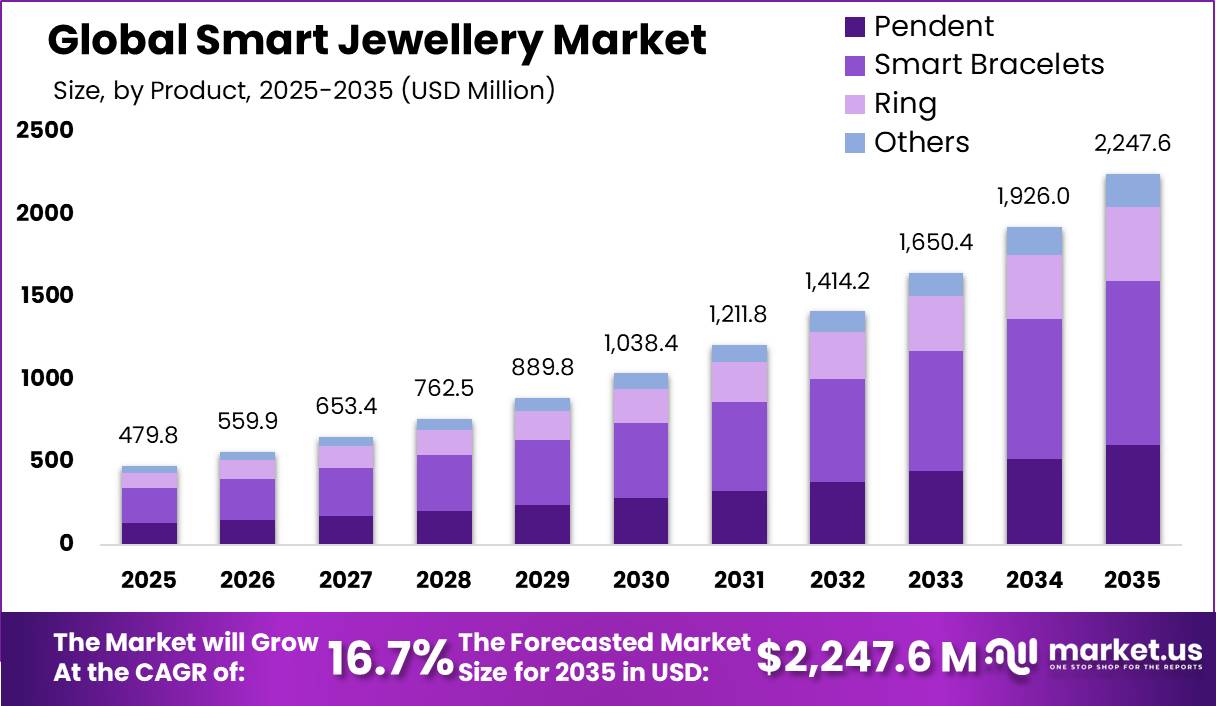

Global Smart Jewellery Market size is expected to be worth around USD 2,247.60 Million by 2035 from USD 479.7 Million in 2025, growing at a CAGR of 16.70% during the forecast period 2026 to 2035. Smart jewelry blends fashion design with embedded sensors for everyday wearability. This format appeals to consumers who want health insights without a traditional smartwatch.

This reflects a product category structured across product type, age group, operating system, and application. Pendants, bracelets, and rings carry sensors for heart rate, activity, and sleep tracking. Devices run on Android or iOS platforms and serve pediatric, adult, and geriatric users. This structure lets manufacturers target distinct buyer needs across fashion and clinical wellness segments.

Key Takeaways

- The global market reached USD 479.7 Million in 2025 and is projected to reach USD 2,247.60 Million by 2035.

- The market is set to expand at a CAGR of 16.70% between 2026 and 2035.

- Smart Bracelets led the product segment with a 44.20% share in 2025.

- The Adult age group held the largest share at 68.80% in 2025.

- Android based devices dominated the operating system segment with 69.10% share.

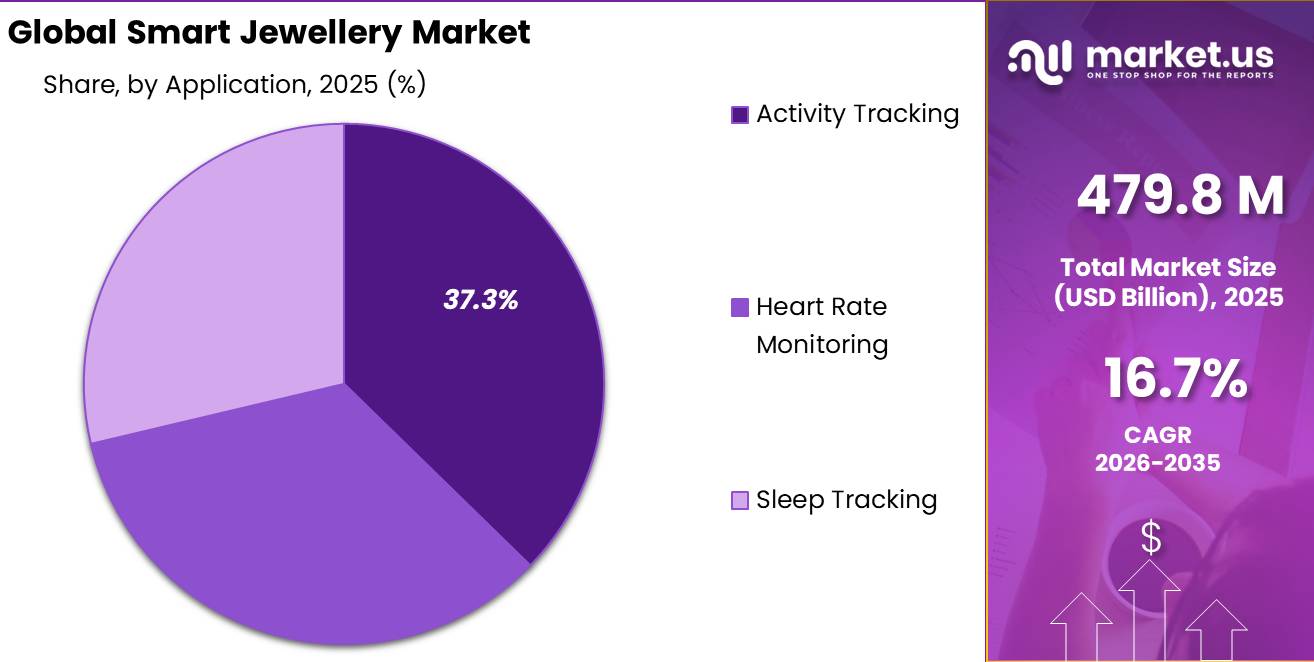

- Activity Tracking led application use cases with a 37.30% share.

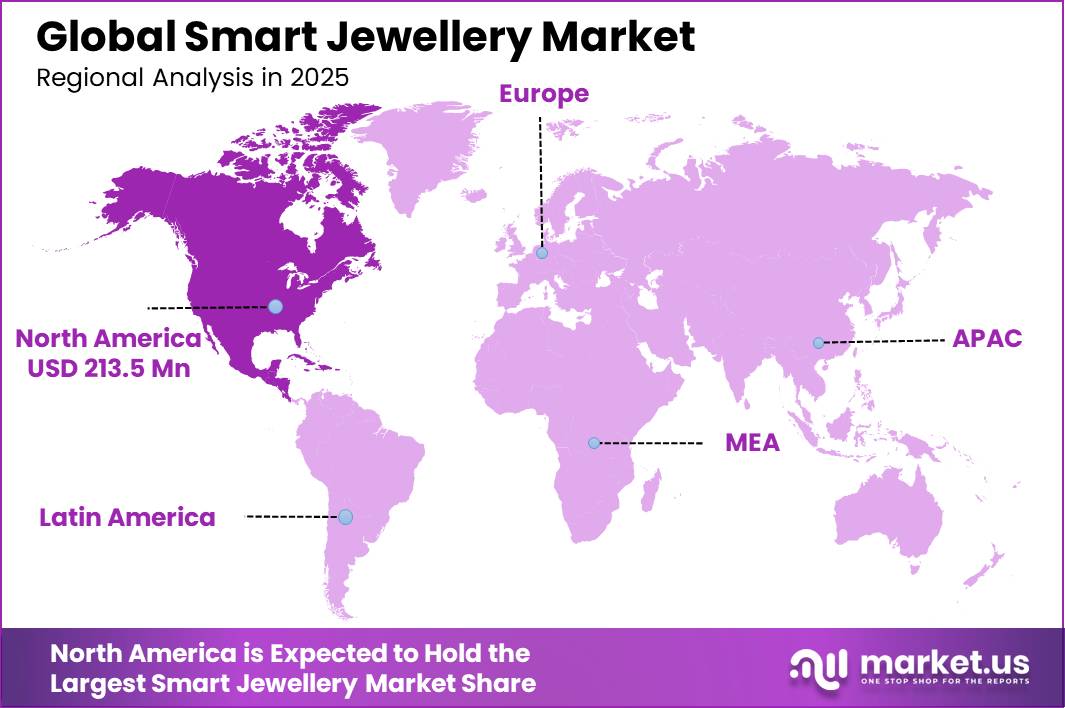

- North America led the global market with a 44.50% share, valued at USD 213.511 Million in 2025.

However, adoption signals point to strong consumer pull. As reported by ŌURA, Oura Ring sales surpassed 5.5 million units globally by September 2025. This pace of unit sales shows smart rings moving from niche gadgets to mainstream wearables.

Therefore, the market is set to grow nearly 4.7 times in value between 2025 and 2035. This pace signals strong investor interest in wearable health jewelry over the next decade. Companies that scale production early stand to capture outsized share before competition intensifies across regions.

Product Analysis

Smart Bracelets dominates with 44.20% due to versatile fitness tracking and broad appeal.

Pendants carry sensors within a necklace format that conceals health tracking inside familiar jewelry. This share of 27.00% reflects buyer preference for subtle wearables over visible bands. Consequently, pendant makers focus on sensor placement near the chest for accurate heart rate capture.

In 2025, Smart Bracelets held a dominant market position in the By Product segment of Smart Jewellery Market, with a 44.20% share. Bracelets combine continuous fitness tracking with all-day wearability across age groups. This broad utility helps brands reach both casual fitness buyers and dedicated health trackers seeking constant monitoring.

Rings capture 20.00% share as a compact format suited to discreet biometric tracking. As reported by Ultrahuman, the January 2025 Rare collection introduced 18K gold and platinum rings at CES 2025. This signals a shift toward luxury materials that position rings as both jewelry and clinical-grade health tools.

Age Group Analysis

Adult dominates with 68.80% due to high disposable income and fitness focus.

Pediatric users account for 20.00% share, largely through parental purchases for activity and safety tracking. Parents favor lightweight designs that monitor location and basic vitals without overwhelming young wearers. This positions pediatric smart jewelry as a safety-first category rather than a fitness-first one.

In 2025, Adult held a dominant market position in the By Age Group segment of Smart Jewellery Market, with a 68.80% share. Adults drive purchases through gym memberships, sleep tracking interest, and disposable income for premium devices. This concentration signals that marketing budgets should prioritize adult fitness and wellness channels over other age groups.

Geriatric users hold 11.20% share, centered on fall detection and remote health monitoring needs. Older adults adopt jewelry formats over smartwatches for comfort and lower visibility of medical tracking. Therefore, this segment favors devices built around safety alerts rather than fitness metrics.

Operating System Analysis

Android dominates with 69.10% due to broader global device compatibility.

In 2025, Android held a dominant market position in the By Operating System segment of Smart Jewellery Market, with a 69.10% share. Android’s wide device base across price tiers gives smart jewelry brands a larger compatible audience. This reach lets manufacturers prioritize Android integration before building parallel iOS features.

iOS devices hold 30.90% share, concentrated among premium buyers in North America and parts of Europe. iOS users typically pay more for app ecosystems and tighter health data integration. This signals an opportunity for premium tier smart jewelry pricing within the iOS user base.

Application Analysis

Activity Tracking dominates with 37.30% due to broad daily fitness use cases.

In 2025, Activity Tracking held a dominant market position in the By Application segment of Smart Jewellery Market, with a 37.30% share. Daily step counts and movement data give users immediate, easy to understand feedback. This simplicity keeps activity tracking as the entry level feature that draws first time wearable buyers.

Heart Rate Monitoring holds 34.00% share as a core health metric across fitness and clinical use cases. Continuous heart rate data supports both workout optimization and early warning for irregular patterns. Consequently, this application anchors premium pricing for devices with higher sensor accuracy.

Sleep Tracking accounts for 28.70% share, reflecting rising consumer interest in recovery and rest quality. Nighttime wear suits ring and pendant formats better than bulkier wrist devices. This favors compact form factors as sleep tracking demand grows alongside daytime activity features.

Key Market Segments

By Product

- Pendant

- Smart Bracelets

- Ring

- Others

By Age Group

- Pediatric

- Adult

- Geriatric

By Operating System

- Android

- iOS

By Application

- Activity Tracking

- Heart Rate Monitoring

- Sleep Tracking

Drivers

Regulatory clarity is reshaping the smart jewelry market in 2026. The FDA’s January 2026 update to its General Wellness and Clinical Decision Support Software guidance lets manufacturers offer metrics like SpO2, blood pressure, and HRV without full medical device approval, provided they avoid diagnostic claims. This lowers entry barriers and speeds up wearable clearances industry wide.

Companies pursuing FDA Class II 510(k) clearance gain access to insurance reimbursement and prescription based markets. In Europe, CE-MDR compliance supports premium pricing through stronger consumer trust. Therefore, the FTC’s extended Health Breach Notification Rule makes data privacy compliance a competitive advantage rather than just a legal obligation.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health & Biometric Monitoring Demand: Rising consumer adoption of continuous health tracking (heart rate, SpO₂, HRV, sleep, stress) embedded in discreet jewelry form factors | +3.8% | North America core; EU secondary; APAC corridors (China, South Korea, Japan) | Short term (≤ 2 years) |

| Miniaturized Sensor & Edge AI Integration: Advances in MEMS sensors, multi-wavelength PPG, and on-device AI enabling medical-grade data accuracy without cloud dependency | +2.9% | North America, EU, South Korea, Taiwan (supply chain); APAC demand corridors | Medium term (2–4 years) |

| Women’s Personal Safety Ecosystem: Growing demand for discreet SOS/GPS wearables among urban female consumers, amplified by government-backed safety mandates and app integrations | +2.1% | South Asia (India primary); North America; Southeast Asia spill-over; EU secondary | Short to Medium term |

| APAC Premiumization & Middle-Class Affluence: Rapid income growth in Tier-1/2 cities driving demand for hybrid luxury-tech wearables; China CAGR of 20.4%, India fastest-growing APAC sub-market | +2.6% | APAC corridors (China, India, South Korea, Japan); South America spill-over | Medium term (2–4 years) |

| Regulatory Clarity & FDA/CE-MDR Pathways: January 2026 FDA wellness guidance update and 2021–2025 surge in 510(k) clearances (183% increase, 2021–2023) opening insurance reimbursement and prescription markets | +1.8% | North America; EU (CE-MDR); emerging in APAC post-harmonization | Medium to Long term |

| Sustainability-Led Design & ESG Consumer Shift: Demand for recycled metals, lab-grown gemstones, and blockchain-traced supply chains; sustainable jewelry market at ~USD 75.55 billion in 2026 | +1.4% | EU primary (regulatory pressure); North America; APAC Gen-Z and millennial cohorts | Long term (≥ 4 years) |

Restraints

Precious metal costs are squeezing smart jewelry manufacturers in 2026. Gold prices rose about 65% in 2025 while silver surged nearly 150%, pushing up production costs for ring and bracelet components. Since metals make up 35 to 55% of manufacturing costs, this surge drives major bill of materials inflation.

Higher material costs threaten premium device demand as retail prices climb, while budget manufacturers struggle to hold affordable price points. As a result, many companies are testing thinner metal designs and alternative alloys, trading some durability and perceived luxury for cost control.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precious Metal Cost Inflation (Gold/Silver Surge) | -2.8% | Global core; APAC & Middle East most exposed | Short term (≤ 2 years) |

| Data Privacy & Regulatory Compliance Burden (GDPR, EU AI Act, DPDP) | -2.2% | EU primary; North America secondary; India & APAC emerging | Medium term (2–4 years) |

| Battery Life & Miniaturization Technical Ceiling | -1.9% | Global; North America & Western Europe premium segment | Medium term (2–4 years) |

| US-China Trade Tariff Pressures & Supply Chain Disruption | -2.5% | North America core; APAC corridors; EU re-routing | Short term (≤ 2 years) |

| Semiconductor Component Shortage & Long Lead Times | -1.5% | Global; APAC manufacturing corridors, Taiwan–China nodes | Medium term (2–4 years) |

| High ASP & Mass-Market Adoption Barrier | -1.7% | Emerging markets (India, SE Asia, LatAm); price-sensitive EU tiers | Long term (≥ 4 years) |

Challenges

Cross-platform fragmentation challenges smart jewelry makers as devices must support Bluetooth Low Energy, NFC, and low-power Wi-Fi while integrating with iOS, Android, payment systems, and access-control networks. This lack of a unified standard consumes an estimated 20 to 35% of software engineering resources that could otherwise fund new features.

Regional NFC variation adds localization costs and certification delays when entering new markets. Closed ecosystem restrictions limit functionality for many users, forcing brands to run separate hardware and software builds. Until standards emerge, fragmentation will slow expansion and weaken subscription revenue retention.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Rare Earth & Critical Mineral Supply Disruption | -1.8% | Global; APAC manufacturing corridors, North America, EU sourcing hubs | Long term (≥ 4 years) |

| Semiconductor Miniaturization Yield Constraints | -1.5% | APAC fab clusters (Taiwan, South Korea, Japan); North America design centers | Long term (≥ 4 years) |

| Multi-Jurisdictional Biometric Data Compliance | -1.2% | EU regulatory hubs, North America state-level patchwork, APAC evolving regimes | Medium term (2–4 years) |

| Precious Metal Cost Inflation & BOM Volatility | -1.1% | Global; South Asia, Middle East, North America retail-tier markets | Medium term (2–4 years) |

| Cross-Platform IoT Ecosystem Fragmentation | -0.9% | North America, EU, East Asia smart device ecosystems | Medium term (2–4 years) |

| Dual-Competency Talent Deficit (Tech + Craft) | -0.8% | North America, EU, India innovation clusters | Long term (≥ 4 years) |

Opportunities

Pharmaceutical and clinical research represent a major opportunity as sponsors seek continuous, real world physiological data for trials. Smart rings have shown strong predictive results, including COVID-19 detection 2.75 days before symptoms with 82% sensitivity and bipolar episode detection 3 to 7 days early with 79% sensitivity.

Momentum built after the FDA’s December 2025 guidance accepted de-identified wearable data for regulatory decisions, lowering barriers to clinical trial use. However, no smart jewelry company has yet built GCP-compliant, HIPAA and GDPR ready infrastructure needed for formal research programs.

Companies investing in this infrastructure could lead the wearables for research field early. Pharmaceutical data licensing deals typically generate 70 to 85% gross margins, creating recurring revenue independent of hardware sales.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Digital Health & Insurance Premium Integration | +3.5% | North America, EU, India | Medium term (2–4 years) |

| Pharma & Clinical Trial Data Monetization | +2.8% | North America, EU | Long term (≥ 4 years) |

| Luxury Fashion House Co-Brand Licensing (Ultra-Premium Tier) | +2.2% | EU, North America, China | Medium term (2–4 years) |

| B2B Corporate Wellness & Enterprise Channel | +2.0% | North America, APAC | Short–Medium term (1–3 years) |

| APAC Emerging Market Mass Premiumization | +3.0% | India, SE Asia, South Korea | Medium–Long term (2–5 years) |

| Contactless Payment-Jewelry Convergence (Active NFC) | +2.5% | North America, EU, East Asia | Long term (≥ 4 years) |

Regional Analysis

North America Dominates the Smart Jewellery Market with a Market Share of 44.50%, Valued at USD 213.511 Million

North America leads the smart jewelry market through strong consumer spending on wearable health technology and dense retail distribution. As reported by Samsung, the 2025 Galaxy Ring delivers up to 7 days of battery life alongside built in health sensors. This battery performance supports daily wear without frequent charging, reinforcing regional demand for premium ring devices.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Keyplayer Analysis

Bellabeat focuses on female oriented wearable jewelry, combining fashion design with menstrual cycle and stress tracking features. This positioning carves a defensible niche separate from general fitness wearables. However, reliance on a narrow demographic limits Bellabeat’s addressable market compared to broader health tracking competitors entering the women’s wearable space.

Oura Health Oy. built category leadership in smart rings through clinical grade sensors and strong consumer trust. The Finland based company prioritizes continuous validation studies over rapid feature expansion. Therefore, Oura sustains premium pricing power while competitors race to match its sensor accuracy and proven research backed credibility in the wearable ring market.

Key Players

- Bellabeat

- Oura Health Oy.

- RINGLY

- Samsung

- Motiv, Inc.

- Ultrahuman

- Corsano Health

- Wellue

- Pebble

Recent Developments

- 2024 – Data from Rock Health shows 44% of US consumers owned wearable health tracking devices, including smartwatches and smart rings.

- October 2024 – A US consumer survey found that 63% of respondents were willing to pay subscription fees for ongoing analytics from personal health monitoring devices.

- June 2025 – Amazfit launched the Helio Strap, its first screen free wearable focused on fitness, recovery, and sleep tracking.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 479.7 Million |

| Forecast Revenue (2035) | USD 2,247.60 Million |

| CAGR (2026-2035) | 16.70% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Pendant, Smart Bracelets, Ring, Others), By Age Group (Pediatric, Adult, Geriatric), By Operating System (Android, iOS), By Application (Activity Tracking, Heart Rate Monitoring, Sleep Tracking) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Bellabeat, Oura Health Oy., RINGLY, Samsung, Motiv, Inc., Ultrahuman, Corsano Health, Wellue, Pebble |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |