Quick Navigation

Report Overview

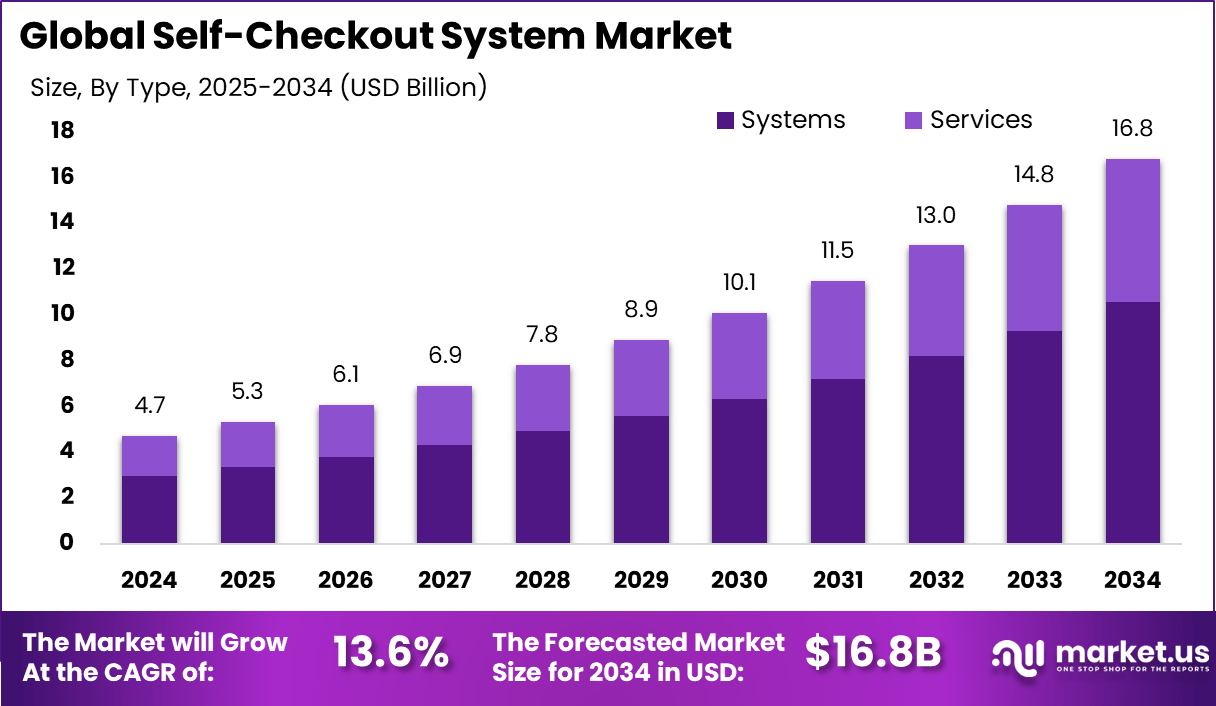

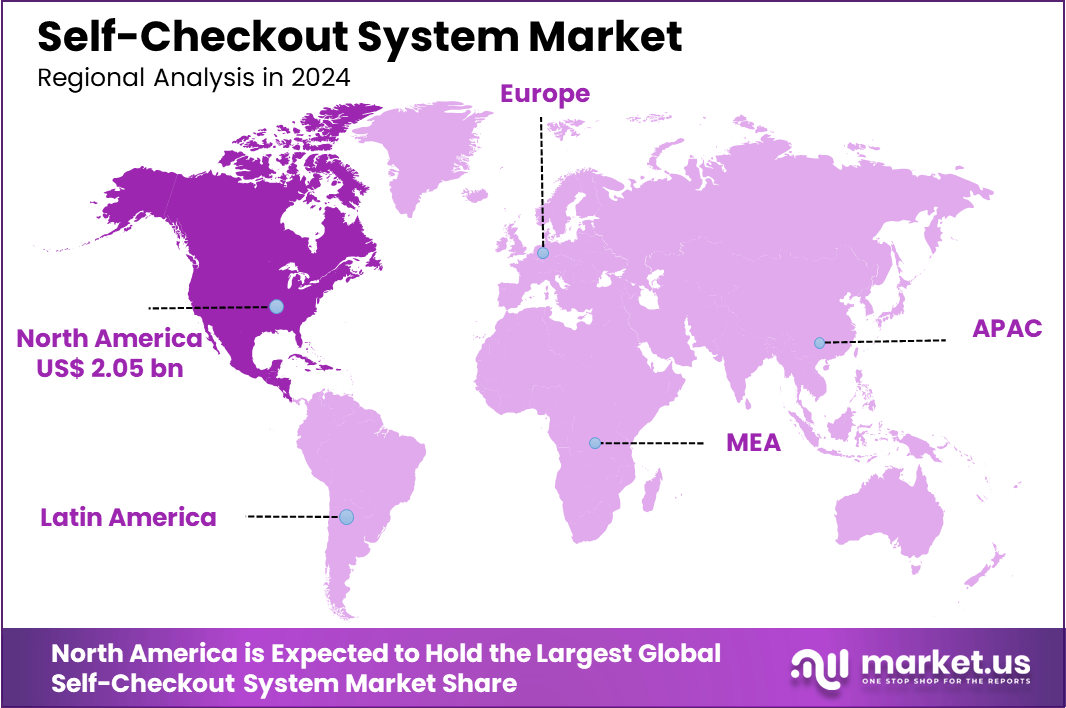

The Global Self-Checkout System Market size is expected to be worth around USD 16.8 Billion By 2034, from USD 4.7 billion in 2024, growing at a CAGR of 13.6% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 43.7% share, holding USD 2.04 Billion revenue.

A self-checkout system is an automated process that allows customers to handle their own purchase transactions without the need for cashier assistance. This technology comprises hardware and software components, including barcode scanners, touch screens, and payment terminals, enabling customers to scan, bag, and pay for their items autonomously.

The self-checkout system market is experiencing robust growth, driven by the increasing demand for faster checkout solutions and reduced labor costs in the retail sector. Retailers across the globe are adopting these systems to enhance customer experience and operational efficiency. The market is segmented based on the type of systems, including standalone units and wall-mounted units, and is further categorized by end-use sectors such as supermarkets, department stores, and convenience stores.

The primary driving factors of the self-checkout system market include the increasing labor costs and the retail industry’s emphasis on operational efficiency. Retailers are adopting these systems to reduce dependence on cashier manpower, thereby cutting costs and improving store operations.

Demand for self-checkout systems is primarily driven by the retail sector’s need to enhance efficiency and consumer satisfaction. The growing number of hypermarkets and supermarkets, especially in emerging economies, is substantially increasing the demand for these systems. Additionally, the post-pandemic shift towards contactless and hygienic transaction methods has accelerated the adoption of self-checkout solutions.

As per the latest insights from Market.us, The global self-service kiosk market is projected to grow from USD 23.9 billion in 2023 to USD 48.3 billion by 2033, registering a steady CAGR of 7.3% over the forecast period. This growth can be attributed to rising demand for contactless services, faster transaction experiences, and operational efficiency across sectors such as retail, healthcare, banking, and transportation.

Based on data from Capital One Shopping, self-checkout systems have become a dominant feature in the U.S. retail landscape, with 95.9% of consumers reporting they have used them. Nearly 40% of grocery store registers are now self-checkout kiosks, and 73% of shoppers say they prefer this method over traditional staffed lanes.

However, the data also uncovers significant challenges – particularly a rise in theft, which can be up to 65% higher compared to manned checkouts. Over 20 million Americans have admitted to stealing at self-checkout, and among the 15% who have done so intentionally, nearly half say they plan to do it again.

A report from Soocial highlights that 67% of shoppers choose self-checkout primarily for faster transactions. Additionally, 30.6% of users adjust their checkout method depending on product type and queue length. The popularity of self-checkout also aligns with broader digital convenience trends, following closely behind restaurant delivery (56%) and buy-online-pickup-in-store (50%) services.

The self-checkout system market presents strategic opportunities for stakeholders and new entrants through technological innovation and customization of offerings to meet diverse consumer needs. New entrants can gain a competitive edge by developing systems that are not only easy to use but also equipped with advanced security features and integration capabilities with existing retail management systems.

Key Takeaways

- The Self-Checkout System Market is projected to reach USD 16.8 billion by 2034, up from USD 4.7 billion in 2024. This growth is expected at a CAGR of 13.6% from 2025 to 2034.

- North America dominated the market in 2024, holding over 43.7% of the share with USD 2.04 billion in revenue.

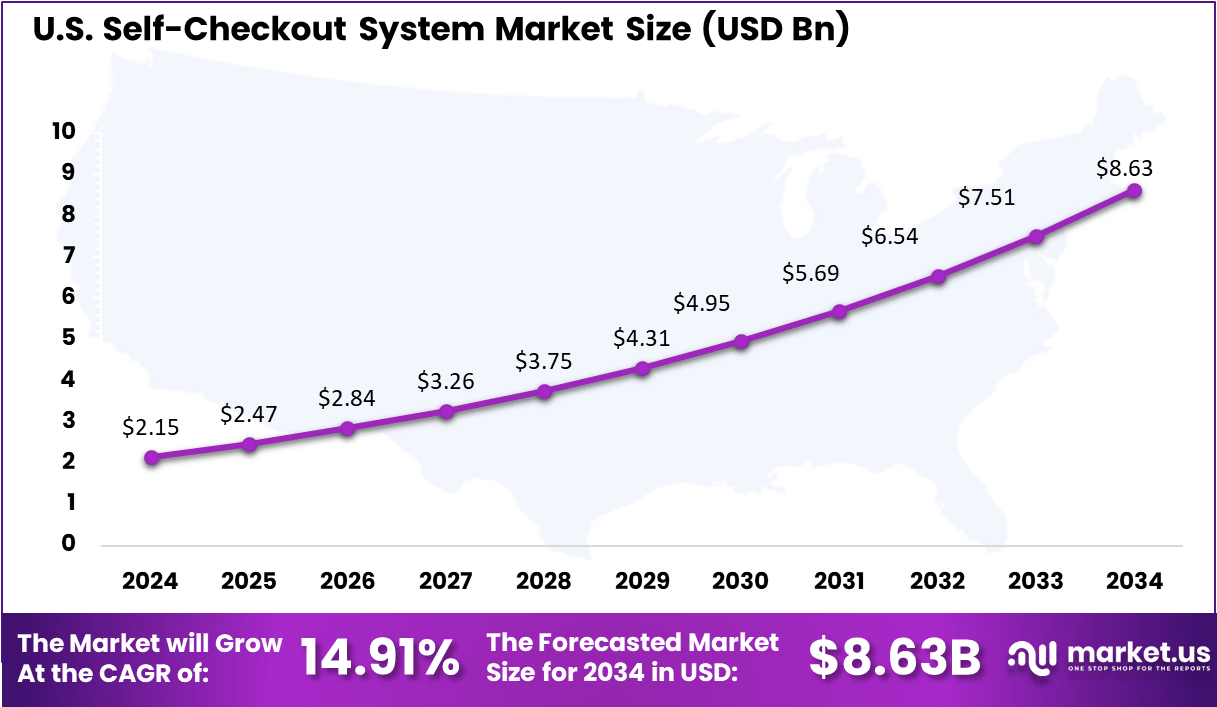

- The US market alone was valued at around USD 2.15 billion in 2024 and is forecasted to grow to approximately USD 8.63 billion by 2034, with a CAGR of 14.91%.

- The Systems segment led the market in 2024, capturing over 62.9% of the share.

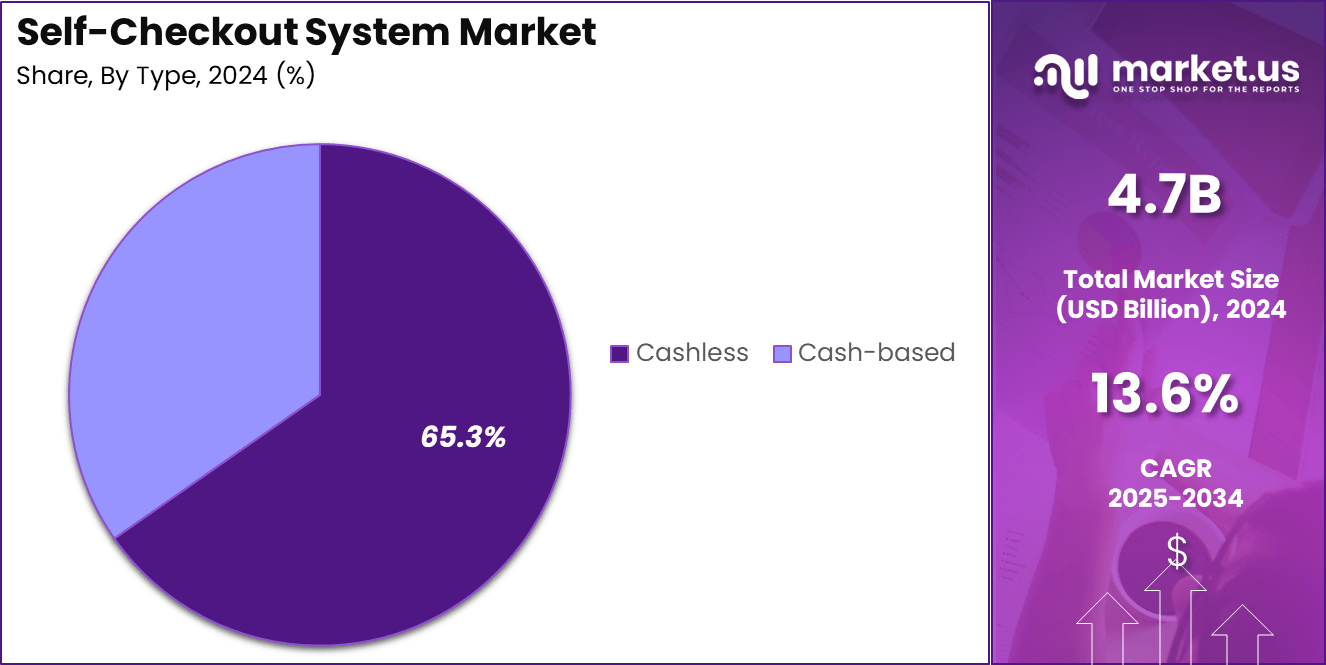

- The Cashless segment also held a strong position, accounting for more than 65% of the market share.

- Supermarkets and hypermarkets dominated the end-use segment in 2024, holding over 56.3% of the market share.

Analysts’ Viewpoint

From an investment perspective, the self-checkout system market is ripe with opportunities driven by continuous technological advancements and a favorable regulatory environment. Investors should focus on companies that are innovating in AI and machine learning to offer more intelligent and adaptable systems.

The regulatory landscape, generally supportive of automation technologies, also plays a crucial role in facilitating the widespread adoption of these systems. As retailers increasingly prioritize customer experience and operational efficiency, the market for self-checkout systems is expected to maintain its growth trajectory, making it an attractive sector for technological investments.

Impact of AI

Artificial intelligence (AI) has significantly transformed self-checkout systems in the retail sector. The following are five key impacts:

- Enhanced Theft Detection and Prevention: AI algorithms analyze customer behavior and transaction data in real-time to identify potential theft or fraud. For instance, AI can detect when an item is not scanned or when a barcode is manipulated, thereby alerting staff to intervene promptly. This proactive approach has led to a notable reduction in theft incidents.

- Improved Customer Experience: AI-powered self-checkout kiosks streamline the purchasing process by accurately identifying products and reducing errors. This efficiency minimizes wait times and enhances overall customer satisfaction. Retailers implementing such systems have observed increased customer preference for self-service options.

- Operational Efficiency and Cost Reduction: By automating routine tasks, AI enables retailers to reallocate staff to more strategic roles, thereby reducing labor costs. Additionally, AI-driven systems can operate continuously, allowing stores to extend operating hours without additional staffing expenses.

- Personalized Marketing and Promotions: AI systems analyze purchasing patterns to provide personalized promotions and product recommendations. This targeted approach not only enhances the shopping experience but also increases the likelihood of repeat purchases.

- Advanced Inventory Management: Real-time data collection by AI-powered self-checkout systems offers valuable insights into inventory levels and sales trends. This information assists retailers in optimizing stock replenishment, reducing overstock and stockouts, and improving supply chain efficiency.

The US Self-Checkout System Market is valued at approximately USD 2.15 Billion in 2024 and is predicted to increase from USD 2.47 Billion in 2025 to approximately USD 8.63 Billion by 2034, projected at a CAGR of 14.91% from 2025 to 2034.

The acceleration in self-checkout adoption is closely tied to broader trends in technological integration within the retail sector. U.S. consumers are increasingly seeking shopping experiences that offer convenience, speed, and minimal human contact, preferences that have been amplified by the health considerations of the COVID-19 pandemic.

Retailers are responding by implementing advanced self-checkout systems that cater to the growing demand for frictionless, fast service experiences. Technologies like mobile wallets and contactless payments facilitate these preferences and are being integrated into self-checkout solutions across the country.

In 2024, North America held a dominant market position in the self-checkout system sector, capturing more than a 43.7% share, amounting to USD 2.05 billion in revenue. This leadership can be attributed to several factors that uniquely position North America at the forefront of retail innovation and consumer technology adoption.

Firstly, the region has seen widespread digitalization across retail formats, from large supermarkets to compact convenience stores. Retailers in North America have been early adopters of self-checkout systems, driven by the dual objectives of enhancing customer experience and optimizing operational efficiency.

The integration of advanced technologies such as AI-powered product recognition and mobile payment systems has been particularly pronounced in the U.S. and Canada, where consumer preference for quick, seamless service encounters is high.

For instance, In February 2025, Kroger, in partnership with NCR Corporation, launched AI-powered self-checkout systems across select U.S. stores. These systems significantly improved product recognition accuracy and minimized scanning errors, while also enabling real-time security monitoring.

Moreover, the labor market dynamics in North America further accelerate the adoption of self-checkout systems. With rising minimum wage laws and the associated increase in labor costs, retailers are turning to automated systems to manage operational expenses effectively.

Self-checkout solutions offer a viable alternative to traditional cashier-staffed lanes, potentially reducing the number of staff required and reallocating labor to more critical areas of customer service and store management.

Component Analysis

In 2024, the Systems segment held a dominant market position within the self-checkout system market, capturing more than a 62.9% share. This substantial market share can be attributed to the increasing adoption of self-checkout solutions across various retail environments, including supermarkets, hypermarkets, and convenience stores.

Retailers are progressively recognizing the efficiency and enhanced customer experience offered by these systems, which has driven their widespread implementation. The leadership of the Systems segment is primarily due to the technological advancements in self-checkout systems, which include user-friendly interfaces, integrated theft prevention mechanisms, and the ability to accept multiple forms of payment.

These enhancements have not only streamlined the shopping experience but also reduced the time customers spend in checkout queues, thereby improving overall store throughput. Furthermore, self-checkout systems have been crucial in reducing labor costs for retailers by minimizing the need for traditional manned checkout stations.

Another factor contributing to the growth of the Systems segment is the customization and scalability of these technologies. Retailers can tailor self-checkout systems to meet the specific needs of their store layouts and customer preferences, making them a versatile solution across various store sizes and types. Moreover, the integration capabilities with other digital systems like inventory management and customer loyalty programs have further enhanced the value proposition of these systems.

As the retail industry continues to evolve with a strong focus on improving customer service and operational efficiency, the demand for self-checkout systems is expected to grow. The Systems segment, with its robust offerings that align with current retail trends, is poised to maintain its leading position in the market.

Type Analysis

In 2024, the Cashless segment held a dominant market position within the self-checkout system market, capturing more than a 65% share. This significant market share is largely driven by the growing consumer preference for quick and seamless transactions.

As digital payments continue to gain traction globally, more consumers are opting for cashless options due to their convenience and speed, which has directly influenced the proliferation of cashless self-checkout systems. The lead of the Cashless segment can also be attributed to the broad acceptance and integration of various digital payment methods, including credit cards, debit cards, and mobile payments.

These technologies enhance the shopping experience by offering higher security and reducing the physical interactions required during transactions, aligning with the increased consumer demand for safer and more hygienic payment methods, particularly in the context of ongoing health concerns.

Moreover, the adoption of cashless systems has been supported by advancements in payment technology and infrastructure. The integration of Near Field Communication (NFC) technology, QR codes, and mobile wallets has not only simplified the payment process but has also enabled retailers to manage transactions more efficiently and with reduced error rates.

Lastly, The Cashless segment is expected to continue leading the market, spurred by innovations in financial technology and an increasing shift towards digital economies around the world. Retailers are likely to continue investing in these systems to cater to the tech-savvy consumer base and to stay competitive in a market that increasingly values efficiency, security, and user-friendly shopping experiences.

Application Analysis

In 2024, the Supermarkets and Hypermarkets segment held a dominant market position within the self-checkout system market, capturing more than a 56.3% share. This leadership is underpinned by the large footfall and high transaction volumes characteristic of these retail environments, where the adoption of self-checkout systems significantly enhances operational efficiencies and customer satisfaction.

The scale of supermarkets and hypermarkets makes them ideal candidates for such technologies, which can handle a vast range of products and high customer throughput. The preference for self-checkout systems in supermarkets and hypermarkets is primarily driven by the need to reduce long queues and wait times, thereby improving the shopping experience for consumers.

These systems enable customers to scan, bag, and pay for their purchases without staff assistance, which not only speeds up the process but also allows stores to redeploy staff to other customer service roles, enhancing overall service quality. Moreover, self-checkout solutions in these settings are often integrated with loyalty programs and promotional offers, further incentivizing their use among shoppers.

Additionally, the continuous advancements in self-checkout technology, including the integration of AI and machine learning for better product recognition and error reduction, have made these systems more reliable and user-friendly. As supermarkets and hypermarkets continue to focus on technology-driven solutions to streamline operations and meet evolving consumer expectations, the adoption of self-checkout systems is expected to expand.

The ongoing trend towards automation in the retail sector, coupled with the growing consumer demand for convenience and quick service, suggests that the Supermarkets and Hypermarkets segment will maintain its lead in the self-checkout system market. As these systems become more sophisticated, incorporating features such as voice navigation and multilingual support, their appeal is likely to increase, securing their place as a fundamental component of modern retail operations.

Key Market Segments

By Component

- Systems

- Services

By Type

- Cash-based

- Cashless

By Application

- Supermarkets and Hypermarkets

- Department Stores

- Convenience Stores

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Labor Shortages and Consumer Expectations

The expansion of the self-checkout system market is significantly driven by labor shortages and evolving consumer expectations for convenience and speed during shopping. Countries like Canada and Thailand are facing labor shortages, prompting retailers to adopt self-checkout systems to streamline operations and reduce reliance on human cashiers.

Furthermore, consumers increasingly demand a variety of checkout options, including the quick and autonomous service provided by self-checkout systems, thus fostering market growth.

Restraint

Security Concerns and Consumer Resistance

Security concerns, especially related to theft and fraud, stand as a major restraint in the wider adoption of self-checkout systems. Despite advancements in technology, the fear of theft and the technical complexity of ensuring secure transactions remain significant hurdles.

Additionally, there is noticeable consumer resistance, particularly in regions like Germany, where traditional shopping practices are preferred, and the adoption of self-checkout technologies is slower. These factors together contribute to a cautious approach by both retailers and consumers towards fully embracing self-checkout technologies.

Opportunity

Advancements in Technology and Market Expansion

The self-checkout system market is ripe with opportunities, primarily due to technological advancements that enhance consumer and operational efficiencies. Innovations such as mobile payment integration, biometric authentication, and AI-powered analytics are making self-checkout systems more appealing and reliable.

North America continues to dominate the market, but significant growth opportunities are also emerging in the Asia-Pacific region, driven by urbanization, rising disposable incomes, and a shift towards digital and contactless payment methods. These technological and regional expansions are creating new avenues for market growth.

Challenge

Balancing Cost and Consumer Satisfaction

The primary challenge facing the rollout of self-checkout systems is balancing the initial high costs of implementation with the need to enhance consumer satisfaction. The cost of advanced technologies and integration can be substantial, and if not managed effectively, may not result in the desired return on investment.

Moreover, while self-checkout offers speed and convenience, it can also lead to consumer frustration due to technical issues like barcode reading errors or payment difficulties. Retailers must navigate these challenges carefully to ensure that the benefits of self-checkout systems outweigh the potential drawbacks.

Growth Factors

The self-checkout system market is witnessing substantial growth, primarily driven by technological advancements and changing consumer behaviors. Retailers are increasingly adopting these systems to cater to customer preferences for quick and autonomous shopping experiences, significantly driven by the convenience and speed offered by self-checkout options.

Technological innovations such as AI-powered product recognition, mobile payment integration, and touchless transactions are enhancing the efficiency and attractiveness of self-checkout solutions, further boosting their adoption across various retail formats including supermarkets, convenience stores, and pharmacies.

Moreover, the growth is bolstered by the strategic response of businesses to labor shortages, making these systems an attractive option to maintain customer service without the proportional increase in staff. This adoption is particularly pronounced in North America and Europe, where there is a strong push towards retail automation to improve operational efficiencies and customer service management.

Emerging Trends

Emerging trends in the self-checkout market reflect a significant shift towards integrating more advanced technologies and adapting to consumer expectations for a frictionless shopping experience. The integration of systems that support contactless payments, such as mobile wallets and contactless credit cards, is becoming standard, driven by a broader movement towards cashless transactions.

Additionally, the use of artificial intelligence to streamline the checkout process and minimize errors is on the rise, enhancing the overall consumer experience and operational throughput. In regions like Asia-Pacific, rapid urbanization and digital infrastructure improvements are propelling the adoption of self-checkout systems.

Business Benefits

Implementing self-checkout systems offers numerous business benefits, including enhanced customer satisfaction through reduced wait times and increased control over the shopping process. For retailers, these systems can lead to a reduction in labor costs and an ability to reallocate staff to more value-adding activities within the store, such as customer service or sales assistance.

Additionally, self-checkout systems can gather valuable data on purchasing behaviors and preferences, which can be used to tailor marketing strategies and improve inventory management.

Key Player Analysis

The following companies are recognized as leaders in the self-checkout systems market, holding the largest combined market share and shaping the direction of industry innovation: NCR Voyix Corporation, Diebold Nixdorf, Incorporated, and Toshiba Global Commerce Solutions.

These firms dominate through continuous investment in AI-driven features, contactless payment technologies, and customizable checkout solutions. Their strong presence and strategic partnerships with major retailers position them at the forefront of market development and digital transformation in retail environments.

Top Key Players in the Market

- Diebold Nixdorf, Incorporated

- ePOS HYBRID

- Fujitsu

- Gilbarco Veeder-Root Company.

- ITAB

- MetroClick

- NCR Corporation

- Pyramid Computer GMBH

- StrongPoint

- Toshiba Global Commerce Solutions

Recent Developments

- February 2025: NCR Corporation collaborated with Kroger to deploy AI-powered self-checkout systems across select U.S. stores. These systems enhance product recognition accuracy, reduce scanning errors, and provide real-time monitoring to improve security and operational efficiency.

- January 2024: Diebold Nixdorf introduced AI-enabled self-checkout technology that utilizes computer vision to recognize products without barcodes, verify ages for restricted purchases, and enhance loss prevention measures. This innovation aims to accelerate transactions, reduce errors, and bolster security in retail environments.

- In January 2024, ITAB secured a major contract with a prominent European grocery chain to supply 7,200 self-checkout systems across several countries. This large-scale deployment, already in progress and set for completion by February 2025, reflects ITAB’s growing influence in the global self-checkout market.

- April 2024: Fujitsu introduced a self-checkout system integrated with a mobile payment application, enabling customers to complete transactions seamlessly using their smartphones. This development caters to the growing demand for contactless payment options in retail settings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.7 Bn |

| Forecast Revenue (2034) | USD 16.8 Bn |

| CAGR (2025-2034) | 13.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Systems, Services), By Type (Cash Based, Cashless), By Application (Supermarkets & Hypermarkets, Convenience Stores) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Diebold Nixdorf, Incorporated, ePOS HYBRID, Fujitsu, Gilbarco Veeder-Root Company., ITAB, MetroClick, NCR Corporation, Pyramid Computer GMBH, StrongPoint, Toshiba Global Commerce Solutions |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |