Global Seed Drill And Broadcast Seeder Machinery Market Size, Share, And Industry Analysis Report By Equipment (Seed Drills, Broadcast Seeders), By Propulsion (Manual Hand Operated, Tractor Mounted, Self-Propelled), By Application (Cereals, Legumes, Oil Seeds, Grasses, Cover Crops), By End Use (Individual Farmers, Agricultural Contractors, Government Research Institutes), By Sales Channel (Online, Offline), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180881

- Number of Pages: 365

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

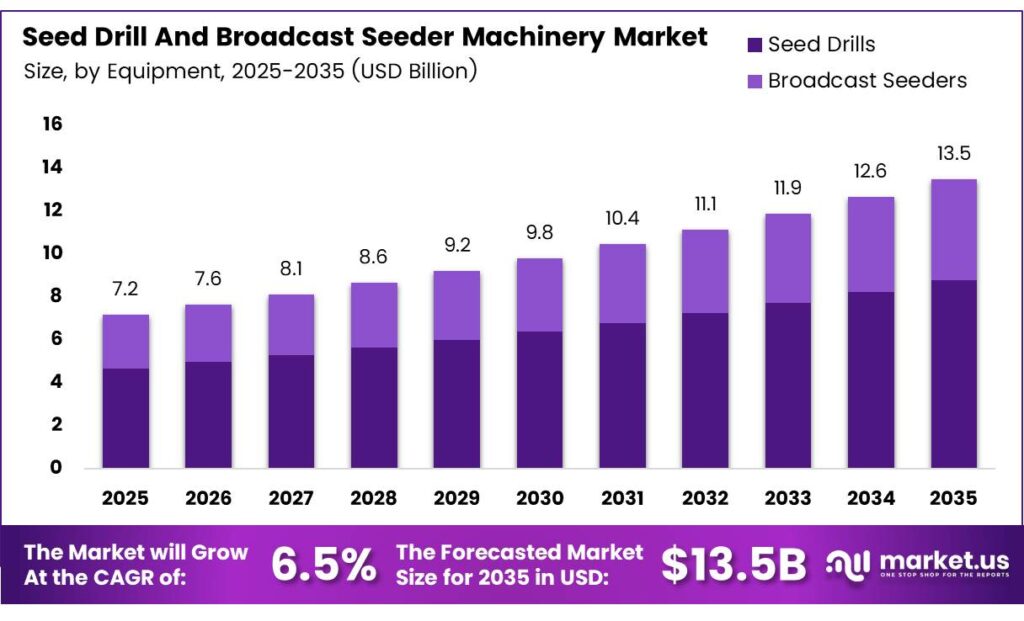

The Global Seed Drill and Broadcast Seeder Machinery Market size is expected to be worth around USD 13.5 billion by 2035 from USD 7.2 billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

The seed drill and broadcast seeder machinery market covers equipment used to plant seeds with precision and efficiency across crop fields. These machines range from manual hand-operated tools to advanced tractor-mounted and self-propelled systems. Farmers and agricultural contractors rely on this equipment to improve crop yields and reduce seed waste.

Seed drills place seeds at controlled depths and spacing in the soil, ensuring consistent germination. Broadcast seeders, however, distribute seeds across wider areas at a higher speed. Both equipment types serve distinct farming needs, from large-scale cereal production to cover crop establishment. Together, they form a critical backbone of modern planting operations.

- United States imports of seeders, planters, and transplanters reached $219,006.19 thousand in 2024 on 685,100 items, making the U.S. the world’s largest importer in this product code. This import volume reflects deep domestic demand and the scale of North American farming operations relying on advanced planting systems.

Government programs worldwide actively support farm mechanization through subsidies and incentive schemes. Nations across Asia, Africa, and Latin America allocate funding to help smallholder farmers access modern seeding equipment. This financial backing reduces adoption barriers and broadens the customer base for machinery manufacturers and distributors.

- Germany’s exports of seeders, planters, and transplanters under HS 843230 reached $550,041.81 thousand in 2024 on 10,627 items, making Germany the largest national exporter in this machinery line. This signals strong European manufacturing capacity and sustained global demand for precision seeding equipment.

Precision agriculture adoption accelerates demand for advanced seeding systems integrated with GPS and sensors. Farmers increasingly seek equipment that delivers variable-rate seeding and real-time soil feedback. This technology shift pushes manufacturers to develop smarter, data-driven planting machinery suited to modern farm management practices.

Key Takeaways

- The Global Seed Drill and Broadcast Seeder Machinery Market was valued at USD 7.2 billion in 2025 and is projected to reach USD 13.5 billion by 2035, growing at a CAGR of 6.5%.

- Seed Drills lead with a 69.7% market share in 2025.

- Tractor-Mounted segment holds a dominant 59.3% share.

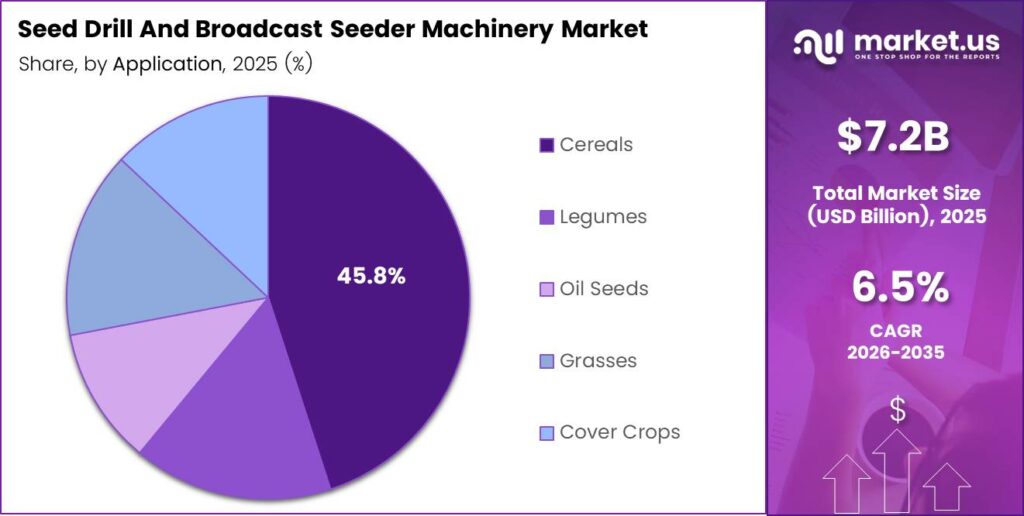

- Cereals represent the largest segment at 45.8%.

- Individual Farmers account for 59.1% of the market demand.

- Offline channels hold a commanding 78.9% share.

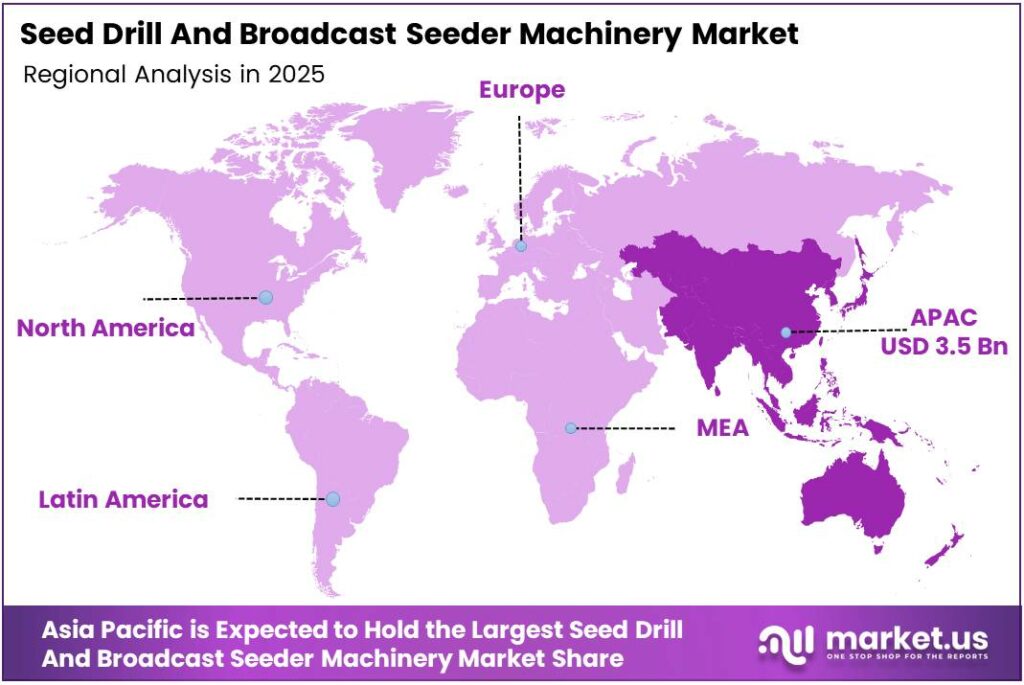

- Asia Pacific dominates the market with a 48.5% share, valued at approximately USD 3.5 billion.

Equipment Analysis

Seed Drills dominate with 69.7% due to precision planting needs across major crop types.

In 2025, Seed Drills held a dominant market position in the By Equipment segment of the Seed Drill and Broadcast Seeder Machinery Market, with a 69.7% share. Farmers prefer seed drills for their ability to place seeds at controlled depths and spacing. This precision reduces seed waste and improves germination rates. Moreover, seed drills support a wide range of sub-types, including single-disc, double-disc, air seed, and fertilizer seed configurations.

Broadcast Seeders represent the remaining equipment share and serve a distinct role in wide-area planting. These machines spread seeds rapidly across open fields, making them suitable for cover crops, grasses, and pasture establishment. Additionally, broadcast seeders include mounted, tow-behind, and self-propelled variants. This variety helps farmers choose equipment matching their land size and operational scale.

Propulsion Analysis

Tractor-Mounted segment dominates with 59.3%, driven by integration with existing farm power units.

In 2025, Tractor-Mounted systems held a dominant market position in the By Propulsion segment of the Seed Drill and Broadcast Seeder Machinery Market, with a 59.3% share. Farmers across mid-scale and large-scale operations prefer tractor-mounted seeders for their versatility. These systems leverage existing tractor power units, reducing the need for separate machinery investment. Consequently, adoption remains high in grain-producing regions across Asia, North America, and Europe.

Manual/Hand-operated equipment serves smallholder farmers in emerging economies where tractor access is limited. These low-cost tools enable subsistence and small commercial farmers to plant seeds efficiently without mechanized power. However, manual options face growing competition from subsidized tractor-mounted solutions. Self-Propelled seeders occupy a premium niche, offering autonomous operation for large commercial farms requiring high-speed planting over vast acreage.

Application Analysis

Cereals dominate with 45.8%, reflecting the scale of global grain cultivation requirements.

In 2025, Cereals held a dominant market position in the By Application segment of the Seed Drill and Broadcast Seeder Machinery Market, with a 45.8% share. Wheat, rice, maize, and barley cultivation drives consistent demand for precision seeding equipment. These crops require accurate row spacing and seed depth to maximize yields. Therefore, seed drill manufacturers prioritize cereal-compatible designs across their product portfolios.

Legumes represent a growing application segment as protein crop demand rises globally. Farmers expanding soybean and pulse cultivation increasingly adopt specialized legume drills for optimal seed placement. Oil Seeds such as canola and sunflower, add further demand for variable-rate seeding equipment. Additionally, Grasses and Cover Crops are emerging application areas tied to conservation agriculture and soil health programs, gaining traction worldwide.

End Use Analysis

Individual Farmers dominate with 59.1% as smallholder and mid-scale growers lead machinery purchases.

In 2025, Individual Farmers held a dominant market position in the By End Use segment of the Seed Drill and Broadcast Seeder Machinery Market, with a 59.1% share. Private farm operators represent the largest and most diverse buyer group for seeding equipment. Government subsidy programs and easy financing options make purchases accessible. Moreover, rising awareness of precision planting benefits encourages individual farmers to upgrade older equipment.

Agricultural Contractors form a commercially active buyer segment, investing in high-capacity seeding machinery to serve multiple farm clients. Their focus on operational efficiency drives demand for durable and high-output equipment. Government/Research Institutes procure seeding machinery for crop trials, demonstration farms, and rural development programs. Additionally, institutional procurement supports the diffusion of modern seeding practices across smallholder farming communities in developing nations.

Sales Channel Analysis

Offline channels dominate with 78.9%, as dealer networks and agri-retail stores remain the primary purchase route.

In 2025, Offline channels held a dominant market position in the By Sales Channel segment of the Seed Drill and Broadcast Seeder Machinery Market, with a 78.9% share. Farmers across all regions continue to prefer physical dealer networks, agri-stores, and manufacturer showrooms for seeding equipment purchases. These channels offer hands-on demonstrations, after-sales service, and financing support. Consequently, offline retail remains the dominant sales pathway for agricultural machinery worldwide.

Online sales channels are growing steadily as digital platforms and e-commerce portals expand their reach into rural markets. Equipment aggregators and manufacturer-owned websites enable farmers in remote regions to browse specifications and compare pricing. However, heavy machinery logistics and the need for after-purchase technical support continue to limit online channel penetration. Nevertheless, the online segment is expected to gain share steadily through the forecast period.

Key Market Segments

By Equipment

- Seed Drills

- Single-Disc

- Double-Disc

- Air Seed

- Fertilizer Seed

- Broadcast Seeders

- Mounted-Broadcast

- Tow-Behind

- Self-Propelled

By Propulsion

- Manual/Hand Operated

- Tractor-Mounted

- Self-Propelled

By Application

- Cereals

- Legumes

- Oil Seeds

- Grasses

- Cover Crops

By End Use

- Individual Farmers

- Agricultural Contractors

- Government/Research Institutes

By Sales Channel

- Online

- Offline

Emerging Trends

Modular Designs and Conservation Agriculture Reshape the Seeding Equipment Market

Manufacturers increasingly develop modular and interchangeable implement designs for multi-season utility. Farmers benefit from equipment that adapts across crop types without requiring full machine replacement. This flexibility reduces total ownership cost and appeals to operations managing diverse planting schedules. Additionally, modular designs extend product lifecycles and reduce post-harvest downtime for equipment vendors.

- No-till and conservation agriculture practices are driving strong demand for specialized seeding systems. China’s exports of seeders, planters, and transplanters reached $90,282.48 thousand in 2024 on 1,087,230 items, reflecting a high-volume, competitively priced segment feeding conservation-oriented markets globally. This export profile shows how lower-cost equipment from China supports smallholder no-till adoption in developing economies.

Telematics and fleet management software integration is transforming large-scale planting operations. Farm managers use real-time machine data to monitor field coverage, track fuel consumption, and schedule maintenance proactively. Furthermore, rising demand for lightweight, high-maneuverability drills is opening new commercial opportunities in orchard and vineyard cultivation, where conventional heavy drills struggle with terrain and row spacing requirements.

Drivers

Rising Global Food Demand and Farm Mechanization Incentives Drive Market Expansion

Escalating global food demand places direct pressure on agricultural productivity improvements. Governments and international agencies push for higher crop yields per hectare to feed growing populations. Consequently, farmers adopt advanced seeding machinery that ensures precise seed placement and reduces replanting needs. This productivity imperative consistently drives equipment procurement across all major agricultural economies.

- India imported $16,538.04 thousand of seeders, planters, and transplanters in 2024 on 236,933 items, while exports were only $4,887.42 thousand. This import gap signals strong domestic demand and limited local supply capacity, confirming that government mechanization subsidy programs are actively stimulating seeder adoption across Indian farming communities.

Acute labor scarcity in rural agricultural sectors accelerates mechanization adoption across all farm scales. Farmers facing seasonal labor shortages increasingly invest in self-propelled and tractor-mounted seeders to maintain planting timelines. Moreover, precision agriculture technologies integrating GPS and variable-rate controls make seeding equipment more productive per operator, strengthening the business case for machinery investment among mid-scale and large-scale farm operators.

Restraints

High Capital Costs and Fragmented Landholdings Constrain Market Penetration

High initial capital investment creates a significant adoption barrier for smallholder farmers in developing regions. Advanced seed drills and self-propelled seeders carry substantial purchase prices that exceed the financial capacity of most small-scale operators. Additionally, maintenance costs, spare parts availability, and skilled technician access compound the total cost of ownership for resource-limited farm operators.

- CNH North America agriculture sales reached $5,839 million in FY2024, down 18.4% from $7,157 million in FY2023, as tractor and combine demand weakened and dealers reduced inventories. This contraction reflects how affordability pressures and inventory corrections slow equipment replacement cycles, restraining near-term market volume even in developed agricultural markets.

Fragmented land holdings and complex topography in developing regions limit the operational efficiency of large seeding equipment. Smallholders cultivating irregularly shaped plots cannot fully utilize wide-span seed drills designed for open grain fields. Consequently, machinery manufacturers must develop smaller, more affordable models suited to fragmented farming landscapes, adding design and manufacturing complexity to product development roadmaps.

Growth Factors

IoT Integration and Sustainable Seeding Technologies Accelerate Market Expansion

IoT and AI integration enables real-time crop spacing and soil health monitoring during planting operations. Farmers using connected seeding equipment receive field-level data that helps them adjust seed rates and depths on the fly. This precision reduces input waste and improves crop establishment. Consequently, smart seeding systems command premium pricing and deliver measurable yield improvements that justify higher capital expenditure.

- Brazil exported $67,011.19 thousand of seeders, planters, and transplanters in 2024, while importing only $10,248.21 thousand, confirming that Brazil remained a net exporter in this farm machinery category. This trade position reflects Brazil’s growing manufacturing capability in multi-crop seeding equipment, which supports export-led growth as regional demand across Latin America rises.

Battery-electric and solar-powered seeding machinery development opens new commercial opportunities in off-grid farming regions. Custom hiring and rental service models further expand market reach among farmers who cannot afford outright equipment purchases. Moreover, innovation in multi-crop and variable-rate seeding technology enables farmers to manage diverse planting programs from a single machine platform, improving asset utilization and reducing the total fleet investment required.

Regional Analysis

Asia Pacific Dominates the Seed Drill and Broadcast Seeder Machinery Market with a Market Share of 48.5%, Valued at USD 3.5 Billion

Asia Pacific leads the global seed drill and broadcast seeder machinery market, holding a 48.5% share valued at approximately USD 3.5 billion. The region’s dominance reflects massive agricultural output across China, India, and Southeast Asia. Government mechanization subsidies and rural development programs actively support equipment adoption.

North America maintains strong market activity driven by large-scale grain and oilseed farming operations. Reflecting a robust air seeder manufacturing base. The United States simultaneously serves as the world’s largest importer of this machinery code, confirming deep domestic demand alongside active domestic production and cross-border trade flows within the region.

Latin America shows strong agricultural equipment demand, particularly in Brazil and Argentina. Expanding soybean and sugarcane cultivation drives consistent investment in seeding equipment. Moreover, favorable commodity prices improve farmers’ purchasing power, supporting machinery acquisition across the region.

The Middle East and Africa region represents an emerging market for seeding equipment, supported by food security programs and government agricultural investment. Countries across Sub-Saharan Africa adopt mechanized seeding solutions to improve smallholder productivity. However, infrastructure gaps and limited financing access slow adoption in rural areas.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Beri Udyog Pvt Ltd is an India-based agricultural machinery manufacturer with a strong presence in the domestic seeding equipment segment. The company produces a range of seed drills and broadcast seeders suited to Indian farming conditions, including small and fragmented landholding environments. Beri Udyog benefits from government mechanization subsidy programs that support equipment adoption among individual farmers across northern and central India.

Buhler Industries Inc. operates as a leading Canadian manufacturer of farm tillage, seeding, and material handling equipment. The company’s product portfolio spans air seeders, cultivators, and grain handling systems designed for large-scale North American prairie farming. Buhler’s engineering strength in high-capacity air seeding systems positions it competitively as precision agriculture integration and variable-rate technology adoption accelerate across Canadian and American grain belts.

CNH Industrial NV is a global agricultural and construction equipment manufacturer operating major brands serving farmers across all world regions. The company offers a comprehensive range of seeding and planting equipment integrated with precision farming platforms. CNH’s global distribution network and strong dealer infrastructure give it reach across developed and emerging agricultural markets, supporting both direct sales and after-sales service operations.

Deere and Co. stands as one of the world’s most recognized agricultural equipment manufacturers, with deep expertise in precision planting and seeding technology. Illustrating that North American agricultural machinery demand remains resilient despite broader market softness. Deere continues to invest in connected farming platforms that enhance seeder performance and data-driven field management.

Top Key Players in the Market

- Beri Udyog Pvt Ltd

- Buhler Industries Inc.

- CNH Industrial NV

- Deere and Co.

- DMW ENG

- Isher Engineering Works

- Kubota Corp.

- KUHN SAS

- Landpower Group Ltd.

- LEMKEN GmbH and Co. KG

- Mahindra and Mahindra Ltd.

- Preet Agro

- RG Steel Crafts

- Rostselmash

- Soil Master

- Stanhay

- Vaderstad Inc.

- Vishwakarma Agro Industries

- Yanmar Holdings Co. Ltd

Recent Developments

- In 2025, CNH’s Case IH brand had three agricultural technologies win AE50 awards for innovation from the American Society of Agricultural and Biological Engineers (ASABE). These innovations are directly relevant to seeding and planting. An intelligent system for the Tiger-Mate 255 field cultivator that monitors seedbed conditions in real-time and automatically adjusts tractor speed to ensure consistent soil preparation for planting.

- In 2025, despite a drop in first-quarter net income, Deere is optimistic that 2026 represents the bottom of the current market cycle. The company forecasts a recovery, particularly in its small ag and turf and construction segments. Deere acquired the intellectual property and related assets for tree planting equipment from Risutec Oy, a Finnish company.

Report Scope

Report Features Description Market Value (2025) USD 7.2 Billion Forecast Revenue (2035) USD 13.5 Billion CAGR (2026-2035) 6.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Equipment (Seed Drills (Single-Disc, Double-Disc, Air Seed, Fertilizer Seed), Broadcast Seeders (Mounted-Broadcast, Tow-Behind, Self-Propelled)), By Propulsion (Manual/Hand Operated, Tractor-Mounted, Self-Propelled), By Application (Cereals, Legumes, Oil Seeds, Grasses, Cover Crops), By End Use (Individual Farmers, Agricultural Contractors, Government/Research Institutes), By Sales Channel (Online, Offline) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Beri Udyog Pvt Ltd, Buhler Industries Inc., CNH Industrial NV, Deere and Co., DMW ENG, Isher Engineering Works, Kubota Corp., KUHN SAS, Landpower Group Ltd., LEMKEN GmbH and Co. KG, Mahindra and Mahindra Ltd., Preet Agro, RG Steel Crafts, Rostselmash, Soil Master, Stanhay, Vaderstad Inc., Vishwakarma Agro Industries, Yanmar Holdings Co. Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Seed Drill And Broadcast Seeder Machinery MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Seed Drill And Broadcast Seeder Machinery MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Beri Udyog Pvt Ltd

- Buhler Industries Inc.

- CNH Industrial NV

- Deere and Co.

- DMW ENG

- Isher Engineering Works

- Kubota Corp.

- KUHN SAS

- Landpower Group Ltd.

- LEMKEN GmbH and Co. KG

- Mahindra and Mahindra Ltd.

- Preet Agro

- RG Steel Crafts

- Rostselmash

- Soil Master

- Stanhay

- Vaderstad Inc.

- Vishwakarma Agro Industries

- Yanmar Holdings Co. Ltd

Our Clients

- 180881

- March 2026