Global Rice Snacks Market Size, Share Analysis Report By Product Type (Rice Cakes, Rice Crisps, Rice Crackers, and Others), By Flavor (Salty, Sweet, Spicy, and Others), By Packaging Type (Pouches, Bags, Boxes, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2034

- Published date: Mar 2026

- Report ID: 181584

- Number of Pages: 236

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

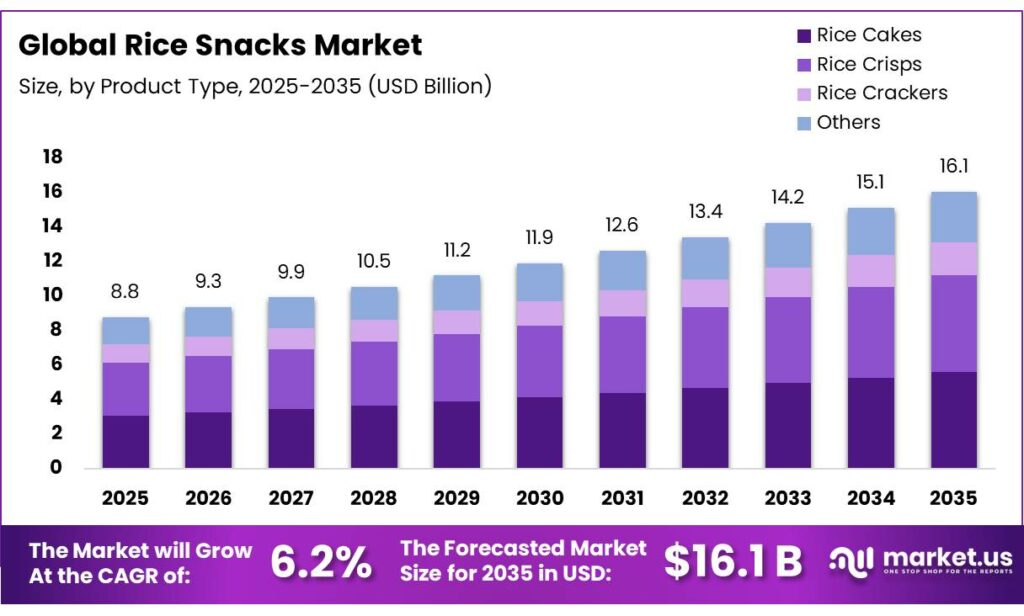

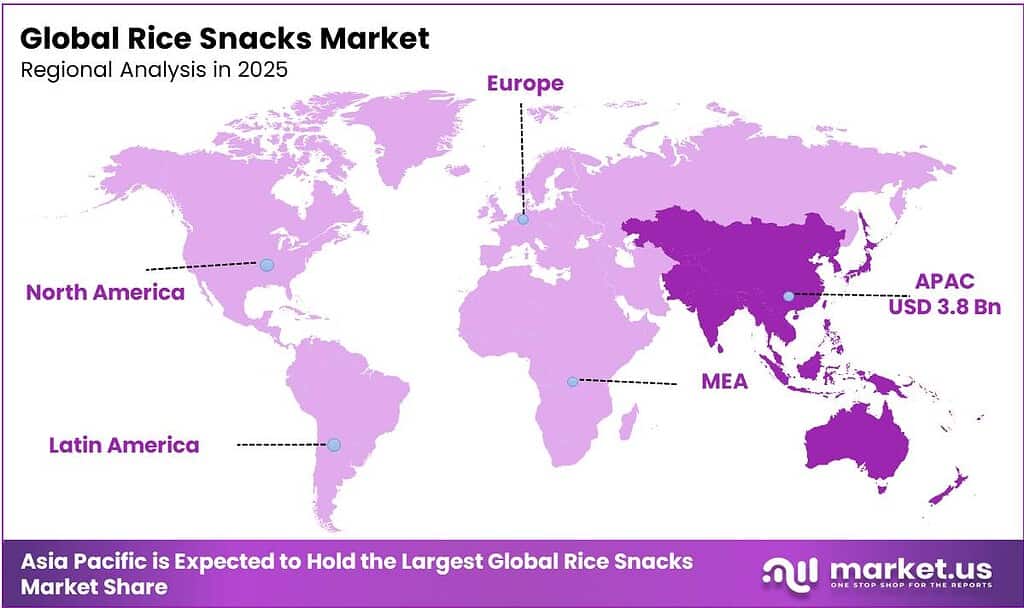

The Global Rice Snacks Market size is expected to be worth around USD 16.1 Billion by 2034, from USD 8.8 Billion in 2024, growing at a CAGR of 6.2% during the forecast period from 2025 to 2034. In 2024, Asia Pacific held a dominant market position, capturing more than a 43.7% share, holding USD 3.8 billion revenue.

Rice snacks are a broad category of light, often crispy foods made primarily from rice or rice flour. They range from airy, disk-shaped rice cakes to crunchy, seasoned rice crackers and bite-sized rice crisps. The rice snacks market is shaped by a combination of consumer trends, product innovation, and regional consumption patterns. Asia Pacific is the largest market due to high rice production, accounting for over 90% of global output, and deep cultural integration of rice in daily diets.

- According to the United States Department of Agriculture (USDA), the total global production of rice in the fiscal year 2025 was approximately 541.3 million metric tons.

Consumers increasingly favor rice cakes for their low-calorie, versatile, and minimally processed characteristics, and salty variants dominate as they enhance the neutral flavor of rice and align with savory snacking habits. In addition, manufacturers focus on flavor and form innovation, introducing puffed crisps, coated rice bites, and multigrain blends, as well as gluten-free, vegan, and health-oriented formulations.

Strategic emphasis on digital and direct-to-consumer channels, along with reliable sourcing and supply chain management, enables wider reach and operational efficiency. Pouch packaging is predominant due to its protective, moisture-resistant properties and convenience features. Distribution is concentrated in supermarkets and hypermarkets, leveraging broad visibility, shelf space, and inventory management advantages. Collectively, these factors position rice snacks as a versatile, accessible, and health-compatible segment within the broader snack market.

Key Takeaways

- The global rice snacks market was valued at US$8.8 billion in 2024.

- The global rice snacks market is projected to grow at a CAGR of 6.2% and is estimated to reach US$16.1 billion by 2034.

- On the basis of types of rice snacks, rice cakes dominated the market, constituting 34.8% of the total market share.

- Based on the packaging type, pouches dominated the rice snacks market, with a substantial market share of around 40.1%.

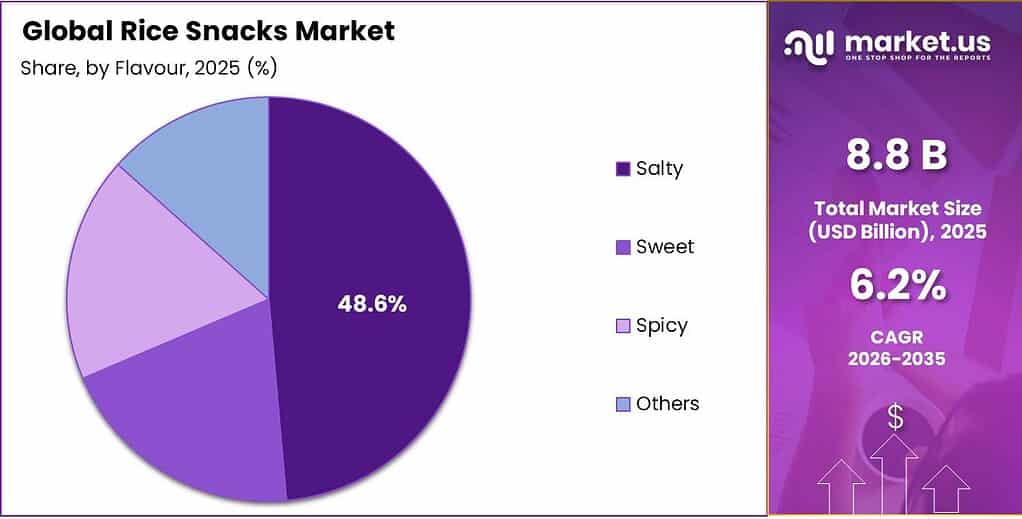

- Based on the flavor, the salty rice snacks led the market, comprising 48.6% of the total market.

- Among the distribution channels, supermarkets/hypermarkets held a major share in the rice snacks market, 51.9% of the market share.

- In 2024, the Asia Pacific was the most dominant region in the rice snacks market, accounting for 43.7% of the total global consumption.

Product Type Analysis

Rice Cakes are a Prominent Segment in the Rice Snacks Market.

The rice snacks market is segmented based on types of rice snacks into rice cakes, rice crisps, rice crackers, and others. The rice cakes led the rice snacks market, comprising 34.8% of the market share, due to their simpler composition, lower perceived caloric density, and versatility in consumption. Standard rice cakes are typically produced through puffing whole rice grains under heat and pressure, a process that often requires few additional ingredients such as oils or flavor coatings. This manufacturing method aligns with consumer preferences for minimally processed and ingredient-transparent foods.

Additionally, their neutral taste and firm, porous texture make them suitable as carriers for diverse toppings, including nut spreads, fruits, vegetables, or savory spreads, allowing them to function as snacks and light meal components. Similarly, rice cakes are commonly marketed in plain, unsalted, or lightly flavored forms, supporting dietary patterns that emphasize reduced sodium or simple formulations. These attributes differentiate them from rice crackers or crisps, which frequently involve frying, seasoning blends, or higher fat content, thereby positioning rice cakes as a comparatively candid snack option.

Flavor Analysis

Salty Rice Snacks Dominated the Market.

On the basis of flavor, the rice snacks market is segmented into salty, sweet, spicy, and others. The salty rice snacks dominated the market, comprising 48.6% of the market share, as salt enhances flavor perception and complements the neutral taste of rice, making the product broadly acceptable across diverse consumer groups. Rice-based snack bases such as puffed rice, rice crackers, or rice crisps typically have mild intrinsic flavor with salt and light savory seasonings that improve palatability without requiring complex formulations.

In addition, salty profiles align closely with traditional savory snack consumption patterns, where products such as crackers or chips are commonly eaten as accompaniments to beverages or light meals. Compared with sweet or strongly spicy variants, lightly salted versions are generally perceived as more versatile and less polarizing, enabling wider consumption across age groups and meal occasions. This sensory compatibility and formulation simplicity contribute to the widespread preference for salty rice snack variants.

Packaging Type Analysis

Rice Snack Products Are Mostly Sold in Pouches.

Based on the packaging type, the rice snacks market is divided into pouches, bags, boxes, and others. The pouches dominated the rice snacks market, with a notable market share of 40.1%, as this packaging format provides efficient protection, flexibility, and cost-effective distribution for lightweight and fragile products. Many rice snacks, such as puffed rice crisps, rice crackers, and coated rice bites, have low density and brittle textures, making them susceptible to breakage during transport. Flexible pouches made from multilayer films can absorb minor impacts and reduce product damage compared with rigid containers.

Similarly, pouches offer effective barrier properties against moisture and oxygen, as rice-based snacks readily lose crispness when exposed to humidity. Heat-sealed pouch structures help maintain product texture and shelf stability. In addition, pouches require less material and storage space during shipping and retail display, allowing manufacturers to transport larger volumes relative to weight. Features such as resealable zippers and tear notches further support convenience and portion control, reinforcing the widespread use of pouch packaging for rice snack products.

Distribution Channel Analysis

Supermarkets/Hypermarkets Held a Major Share of the Rice Snacks Market.

Among the distribution channels, 51.9% of the total global consumption of rice snack products is sold through supermarkets/hypermarkets, as these channels provide broad product visibility, high shelf space, and efficient bulk distribution, which suit packaged snack products with relatively low unit weight and high turnover. Supermarkets offer structured category placement, allowing rice snacks to be displayed alongside other snack foods, facilitating comparison and impulse purchases.

Similarly, these formats support inventory management and replenishment efficiency, enabling manufacturers to deliver large quantities in a single shipment while maintaining consistent stock levels. While convenience stores offer limited space, and online channels require additional logistics for fragile, low-density products, supermarkets and hypermarkets provide an ideal balance between consumer access, product presentation, and supply chain efficiency. Additionally, the ability to bundle or cross-promote rice snacks with complementary items, such as beverages or packaged foods, further reinforces supermarket and hypermarket dominance in distribution.

Key Market Segments

By Product Type

- Rice Cakes

- Rice Crisps

- Rice Crackers

- Others

By Flavor

- Salty

- Sweet

- Spicy

- Others

By Packaging Type

- Pouches

- Bags

- Boxes

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Others

Drivers

Rise of Gluten-Free and Vegan Diets Drives the Rice Snacks Market.

The rise of gluten-free and vegan diets has structurally expanded demand for rice-based snack formulations, as rice is inherently gluten-free and plant-derived. Additionally, rice acts as a hypoallergenic substitute for wheat and a neutral, dairy-free base. The U.S. Food and Drug Administration estimates that about 3 million individuals in the United States have celiac disease, a condition triggered by gluten ingestion.

To standardize food labeling for such consumers, the agency mandates that foods labeled gluten-free contain less than 20 parts per million (ppm) of gluten. Rice and rice-derived ingredients qualify naturally under this regulatory definition, making them widely usable in gluten-free snack formulations. While celiac disease affects roughly 1% of the population, broader adoption is fueled by consumer preference for “free-from” products and plant-based alternatives.

Additionally, the high prevalence of allergens in many plant-based foods positions rice as a critical, low-allergen ingredient for clean-label snacking. Similarly, dietary shifts reinforce this positioning. A survey by the Vegan Society reported that 3% of the population in Great Britain, about 2 million individuals, identify as vegan or plant-based, while 10% are reducing or eliminating animal products. These patterns influence snack design as rice-based products can simultaneously meet gluten-free labeling requirements and vegan dietary restrictions. Consequently, rice crackers, puffed rice snacks, and rice cakes function as compatible platforms for manufacturers targeting consumers seeking grain-based, gluten-free, and plant-derived snack options under established regulatory and dietary frameworks.

Restraints

Competition from Other Snack Categories Might Pose a Challenge to the Rice Snacks Market.

The rice snacks market faces substantial competition from established and emerging categories within the broader savory snack industry. While rice-based formats are expanding, they operate within a highly saturated landscape dominated by high-volume substitutes. For instance, traditional salty snacks, led by potato and tortilla chips, maintain a significant market lead.

The expansion of rice-based snacks is constrained by intensified demand for widely consumed snack formats such as chips, confectionery, and bakery products. In addition, these foods contribute substantial energy intake per consumer, 347 kcal for sweet bakery products and 215 kcal for savory snacks when consumed, indicating strong consumer penetration across multiple competing categories.

Moreover, snacking itself is frequent and diversified. The survey-based consumption data indicate that 78% of consumers snack on two or more products on any given day, enabling multiple product categories to compete for the same eating occasions. The high consumption frequencies and the broad presence of bakery, confectionery, nut-based, and chip products create substitution pressure that limits category-specific expansion opportunities for rice-based snack products.

Opportunities

Increased Utilization in Digital and Direct-to-Consumer (DTC) Channels Creates Opportunities in the Rice Snacks Market.

The integration of digital and direct-to-consumer (DTC) channels presents a critical structural opportunity for the rice snacks market, driven by shifting consumer procurement behaviors and regulatory adjustments for online food retail. E-commerce has emerged as a high-growth frontier for the food and beverage sector. Food purchasing has increasingly migrated to online platforms.

According to the USDA FAS report 2025, food and beverage categories saw online growth rates of 15.8% in major digital markets such as China. Domestically, the USDA Farm Computer Usage report 2025 indicates that 29% of farms use the internet specifically for marketing activities, an increase of 6% since 2023, facilitating a more direct farm-to-shelf digital pipeline for specialized producers. Similarly, the U.S. Census Bureau reported that retail e-commerce accounted for 16.4 % of total U.S. retail sales in Q3 2025.

Digital grocery adoption further expands the addressable channel for packaged snack categories. As rice snacks are shelf-stable packaged foods with relatively low storage constraints, they are compatible with e-commerce logistics, subscription models, and brand-managed DTC storefronts. The increasing digitalization of grocery purchasing provides a scalable channel for rice snack producers to reach consumers beyond conventional retail distribution networks.

Trends

Innovation in Flavor and Form of Rice Snacks.

Innovation in flavor profiles and physical forms serves as a primary structural driver in the rice snacks market, transitioning the category from traditional staples to diverse “better-for-you” alternatives. This evolution is characterized by the integration of global culinary influences and advanced processing techniques.

Manufacturers are increasingly incorporating complex, cross-cultural seasonings to differentiate products. There is a shift toward global flavors, including sriracha, wasabi, and sweet chili, to appeal to non-traditional markets. The rice crackers, such as senbei and arare, maintain high penetration due to constant flavor iterations, with seasonal and regional variations accounting for a significant portion of new product launches.

Similarly, the Japanese snack kaki-no-tane, consisting of soy-flavored rice crisps paired with peanuts, is marketed in multiple variants, including wasabi and pepper flavors, illustrating the integration of strong savory seasonings into rice-based snack bases. In addition, rice snacks now appear in multiple structural forms, including crackers, puffed crisps, cakes, and mixed snack assortments, broadening consumption occasions and textures.

For instance, Korean shrimp crackers made primarily from rice are produced in different product sizes and flavor variants such as spicy and sweet-and-sour formulations, illustrating adaptation through seasoning and format variation. In addition, contemporary rice snacks incorporate both sweet (caramel, chocolate, cinnamon) and savory (cheese, chili, herb) profiles, as well as coated or filled versions, indicating the shift from plain rice bases toward hybrid snack formats that combine grain textures with confectionery or savory flavor systems.

Geopolitical Impact Analysis

Increased Rice Prices Affecting Rice Snacks Market Amid Geopolitical Tensions.

The geopolitical tensions and trade policy responses in major rice-exporting countries have affected the supply environment for rice-based food products, including rice snacks. Rice is a globally traded staple, and policy shifts by key exporters influence raw-material availability and price stability. India alone accounts for over 40-45% of global rice exports, supplying rice to around 140 countries, which indicates that policy interventions in this market have global supply implications.

In July 2023, India imposed a ban on non-basmati white rice exports, which represented about 25% of its total rice exports and roughly 10% of global rice trade. This policy reduced international supply and contributed to price increases in several exporting countries, with benchmark rice prices rising 14% in Thailand and 22% in Vietnam during the period of restrictions. Such price volatility affects food manufacturers that rely on rice as a primary input for products such as crackers, puffed rice snacks, and rice cakes.

Geopolitical tensions and trade disruptions further compound supply risks. For instance, conflicts affecting shipping routes in the Middle East have raised concerns about logistics through the Strait of Hormuz, a critical maritime corridor for commodity trade. Additionally, export restrictions and licensing regimes across several producing countries, including India, Russia, and Vietnam, have been periodically implemented to safeguard domestic food security. These developments demonstrate that geopolitical instability and policy responses can influence rice availability, procurement costs, and supply chain reliability for rice-based snack manufacturers.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Rice Snacks Market.

In 2024, the Asia Pacific dominated the global rice snacks market, holding about 43.7% of the total global consumption. The region represents the largest regional base for rice-derived food products, including rice snacks, primarily due to the concentration of rice production and consumption in the region. According to the Food and Agriculture Organization (FAO), the Asia Pacific accounts for a significant amount of the global paddy rice output, indicating a strong raw-material base for rice-based food manufacturing. The estimates show that around 90% of global rice production occurs in Asia, with China and India together accounting for roughly 55% of world output.

The production concentrations enable extensive domestic processing and product diversification, including rice crackers, puffed rice snacks, and rice cakes. Furthermore, high per-capita rice consumption across East and Southeast Asia supports widespread product familiarity and demand for rice-based snack formats such as Japanese senbei and Korean rice crackers. The combination of dominant agricultural production, extensive cultivation area, and deep cultural integration of rice in daily diets positions the Asia Pacific as the principal market for rice-based snack products.

Market % of Global Production Total Production (2025/2026, Metric Tons) India 28% 152 Million China 27% 146.33 Million Bangladesh 7% 37.65 Million Indonesia 6% 33.6 Million Vietnam 5% 26 Million Thailand 4% 20.4 Million Philippines 2% 12.3 Million Burma 2% 12 Million Pakistan 2% 9.4 Million Cambodia 2% 8.2 Million Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of rice snacks focus on several strategic activities, such as product innovation, involving the development of new flavors, textures, and formats, such as puffed crisps, coated rice crackers, and multigrain blends, to address evolving consumer preferences. In addition, companies emphasize health-oriented formulations, including gluten-free, vegan, and reduced-sodium variants, aligning with regulatory labeling frameworks and dietary trends.

Another key strategy is packaging and portion innovation, such as single-serve packs and resealable formats that support on-the-go consumption and longer shelf stability. Manufacturers increasingly utilize digital and direct-to-consumer channels, including brand-managed online stores and e-commerce marketplaces, to expand distribution beyond traditional retail. In addition, firms invest in supply chain integration and sourcing reliability, particularly securing rice inputs and improving processing technologies to maintain consistent quality and production efficiency across diverse markets.

The Major Players in The Industry

- PepsiCo Inc.

- General Mills Inc.

- Element Snacks Inc.

- Nestlé S.A. (Osem)

- Lundberg Family Farms

- Kameda Seika Co. Ltd

- Hunter Foods LLC

- DeZhou Harvest Foods Co. Ltd

- Bourbon Corporation

- SanoRice Holding B.V.

- Want Want Holdings Ltd

- Calbee Inc.

- Lotte Corporation

- Lotus Foods, Inc.

- Blue Diamond Growers

- Tastemorr Snacks

- Umeya Co., Ltd

- Ricegrowers Ltd (SunRice)

- Riso Gallo

- Sanritsu Seika Co. Ltd

- Other Key Players

Key Development

- In March 2026, Quaker (PepsiCo Inc.) expanded its better-for-you portfolio by introducing a higher-protein option in their rice crisps line.

- In February 2023, Element Snacks, a leading U.S. brand known for its chocolate-topped rice cakes, announced the launch of its Sea Salt Caramel Crispy Rice Minis.

Report Scope

Report Features Description Market Value (2024) US$8.8 Bn Forecast Revenue (2034) US$16.1 Bn CAGR (2025-2034) 6.2% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Rice Cakes, Rice Crisps, Rice Crackers, and Others), By Flavor (Salty, Sweet, Spicy, and Others), By Packaging Type (Pouches, Bags, Boxes, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape PepsiCo Inc., General Mills Inc., Element Snacks Inc., Nestlé S.A. (Osem), Lundberg Family Farms, Kameda Seika Co. Ltd., Hunter Foods LLC, DeZhou Harvest Foods Co. Ltd., Bourbon Corporation, SanoRice Holding B.V., Want Want Holdings Ltd., Calbee Inc., Lotte Corporation, Lotus Foods, Inc., Blue Diamond Growers, Tastemorr Snacks, Umeya Co., Ltd., Ricegrowers Ltd (SunRice), Riso Gallo, Sanritsu Seika Co. Ltd., and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- PepsiCo Inc.

- General Mills Inc.

- Element Snacks Inc.

- Nestlé S.A. (Osem)

- Lundberg Family Farms

- Kameda Seika Co. Ltd

- Hunter Foods LLC

- DeZhou Harvest Foods Co. Ltd

- Bourbon Corporation

- SanoRice Holding B.V.

- Want Want Holdings Ltd

- Calbee Inc.

- Lotte Corporation

- Lotus Foods, Inc.

- Blue Diamond Growers

- Tastemorr Snacks

- Umeya Co., Ltd

- Ricegrowers Ltd (SunRice)

- Riso Gallo

- Sanritsu Seika Co. Ltd

- Other Key Players

Our Clients

- 181584

- Mar 2026