Global Rice-Based Skincare Products Market Size, Share, Growth Analysis By Product Type (Moisturizers & Creams, Cleansers & Toners, Face Masks, Exfoliators & Scrubs, Sunscreens, Others), By End-User (Women, Men, Kids), By Distribution Channel (Offline, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182648

- Number of Pages: 277

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

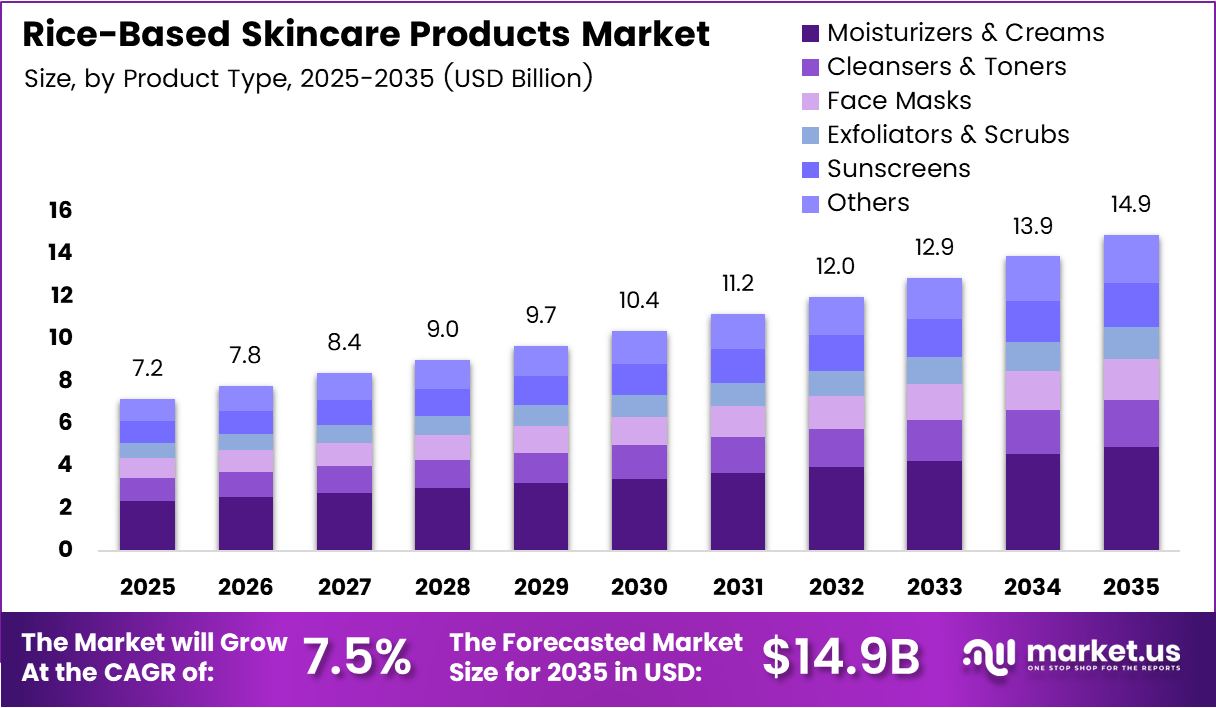

The Global Rice-Based Skincare Products Market size is expected to be worth around USD 14.9 Billion by 2035 from USD 7.2 Billion in 2025, growing at a CAGR of 7.5% during the forecast period 2026 to 2035.

Rice-based skincare uses bioactive compounds derived from rice bran, rice water, and fermented rice extracts to address skin hydration, brightening, and anti-aging concerns. These formulations rely on clinically studied ingredients such as ferulic acid, gamma oryzanol, and ceramides. Consumer preference has shifted toward ingredient-led skincare, placing rice extract at the center of premium product innovation.

The clean beauty movement has accelerated adoption of rice-infused formulations across moisturizers, cleansers, toners, and sunscreens. Brands position rice extract as a natural alternative to synthetic actives, appealing to ingredient-conscious buyers. This positioning allows manufacturers to command premium pricing while differentiating within crowded skincare aisles — a structural advantage that sustains margin growth across product categories.

North America holds the dominant regional position with a 32.60% market share, valued at USD 2.3 Billion. This leadership reflects strong consumer willingness to adopt Asian-inspired beauty rituals, backed by robust e-commerce and specialty retail infrastructure. The U.S. market’s maturity in functional skincare creates a high-conversion environment for rice-based product launches.

Women represent 71.3% of end-user demand, and offline distribution channels account for 67.4% of sales — confirming that this market still converts primarily through physical retail despite digital growth. Mamaearth’s launch of its Rice Facewash in May 2024 with a digital campaign featuring Palak Tiwari demonstrated how brand investments in rice-based lines are intensifying across emerging and developed markets.

According to Frontiers in Pharmacology, in vivo treatment with fermented rice bran extract increased skin moisture content and elastic coefficient by more than 10% compared to the untreated group. This clinical evidence directly strengthens purchase intent among informed consumers — it moves rice-based skincare from trend-led to science-backed, raising the bar for new market entrants and validating premium price positioning.

According to a double-blind, placebo-controlled clinical trial published in Cosmetics (MDPI), application of rice fermentation filtrate emulsion reduced transepidermal water loss by 25.05% after ten minutes. This result signals that rice-derived formulations deliver measurable efficacy at a speed that aligns with consumer expectations — a critical threshold for repeat purchase behavior and brand loyalty in the functional skincare segment.

Key Takeaways

- The Global Rice-Based Skincare Products Market was valued at USD 7.2 Billion in 2025 and is forecast to reach USD 14.9 Billion by 2035.

- The market advances at a CAGR of 7.5% during the forecast period 2026 to 2035.

- By Product Type, Moisturizers & Creams lead with a 31.2% share in 2025.

- By End-user, Women hold the dominant position at 71.3% of total market demand.

- By Distribution Channel, Offline channels account for 67.4% of total sales.

- North America dominates the regional landscape with a 32.60% share, valued at USD 2.3 Billion.

Product Type Analysis

Moisturizers & Creams dominate with 31.2% due to daily-use necessity and anti-aging positioning.

In 2025, Moisturizers & Creams held a dominant market position in the By Product Type segment of the Rice-Based Skincare Products Market, with a 31.2% share. Daily application frequency drives consistent repurchase rates, and rice extract’s documented ability to boost collagen and skin moisture content makes this format the most effective vehicle for communicating clinical benefits to consumers.

Cleansers & Toners serve as the entry point for consumers new to rice-based skincare, offering lower price thresholds and visible immediate results. This segment benefits directly from social media visibility around rice water rituals. In April 2025, I’m From launched the Black Rice Toner — a lightweight, oil-controlling formula targeting balanced hydration — signaling continued innovation pressure in this sub-segment.

Face Masks carry strong premiumization potential within the rice skincare category due to their positioning as treatment products rather than daily essentials. Consumers associate masks with intensive care, allowing brands to charge higher unit prices. However, lower purchase frequency compared to moisturizers limits the overall revenue ceiling for this format.

Exfoliators & Scrubs differentiate through the dual function of mechanical and biochemical exfoliation, leveraging rice bran particle texture alongside active compounds. This format appeals to consumers seeking visible skin renewal. The category’s growth depends on communicating ingredient science — particularly ferulic acid and gamma oryzanol — to justify premium positioning over commodity physical scrubs.

Sunscreens represent the highest-growth format opportunity within rice-based skincare, as brands combine UV protection with brightening and antioxidant claims from rice extract. Riceberry-derived formulations have demonstrated pH stability of 4.44 ± 0.03 with no delamination after five freeze-thaw cycles, validating commercial scalability. This stability data reduces formulation risk for manufacturers entering this sub-segment.

Others within the product type segment include serums, eye creams, and treatment essences — formats that serve advanced skincare consumers seeking targeted active delivery. These products carry the highest margin potential but require stronger clinical evidence to justify positioning. As bioactivity research on rice bran fermentation matures, serum formats will become the next battleground for premium differentiation.

End-User Analysis

Women dominate with 71.3% due to higher skincare engagement and multi-step regimen adoption.

In 2025, Women held a dominant market position in the By End-user segment of the Rice-Based Skincare Products Market, with a 71.3% share. Female consumers drive both volume and premiumization — they adopt multi-step routines that incorporate rice-based cleansers, toners, moisturizers, and masks simultaneously. This behavior multiplies per-consumer revenue and creates strong brand stickiness.

Men represent the fastest-expanding demand pool in rice-based skincare, fueled by shifting attitudes toward grooming and skin health among male consumers. The segment currently accounts for a minority share but offers disproportionate upside — brands that establish early credibility in male-targeted rice skincare will define category standards before competition intensifies.

Kids skincare represents a niche but high-trust segment, where parents actively seek gentle, natural-origin formulations. Rice extract’s mild bioactive profile and established safety data make it a credible ingredient choice for pediatric-positioned products. Brands entering this sub-segment benefit from low competitive intensity and strong parental loyalty once trust is established.

Distribution Channel Analysis

Offline dominates with 67.4% due to tactile trial preference and established retail networks.

In 2025, Offline channels held a dominant market position in the By Distribution Channel segment of the Rice-Based Skincare Products Market, with a 67.4% share. Consumers buying premium skincare prefer to evaluate texture, scent, and packaging before purchasing — a behavior that sustains physical retail dominance despite e-commerce expansion. Specialty beauty chains and department stores remain the primary conversion environment for rice-based premium lines.

Online distribution accelerates brand discovery and repeat purchase, particularly for digitally native rice-based brands. E-commerce platforms allow brands to educate consumers through content and reviews — critical for a category where ingredient credibility drives conversion. As clinical evidence for rice extract compounds accumulates, online channels become increasingly effective at converting ingredient-educated buyers at scale.

Key Market Segments

By Product Type

- Moisturizers & Creams

- Cleansers & Toners

- Face Masks

- Exfoliators & Scrubs

- Sunscreens

- Others

By End-User

- Women

- Men

- Kids

By Distribution Channel

- Offline

- Online

Drivers

Consumer Shift Toward Natural Ingredients and Clean Beauty Fuels Rice Skincare Adoption

Consumers increasingly reject synthetic actives in favor of plant-derived compounds with documented skin benefits. Rice extract — delivering ferulic acid, ceramides, and gamma oryzanol — meets this demand with a strong safety profile and cultural heritage. Brands that align formulations with clean beauty standards capture the premium end of this preference shift directly.

The clean beauty movement reshapes how brands formulate products, not just how they market them. Rice bran fermentation extracts gain credibility because they replace solvent-heavy processing with greener, resource-efficient methods. According to Frontiers in Pharmacology, fermented rice bran treatment increased skin collagen content by 10% compared to controls — evidence that elevates rice extract from cosmetic trend to clinically defensible ingredient.

Anti-aging benefit awareness among consumers creates sustained demand for functional botanicals. Rice extract compounds directly address collagen synthesis and moisture retention — two primary anti-aging concerns. In May 2024, Mamaearth’s launch of its Rice Facewash with a digital campaign emphasizing glass-skin benefits confirmed that brands are actively converting this ingredient awareness into commercial traction at scale.

Restraints

High Extraction Costs and Unresolved Efficacy Questions Limit Broader Market Penetration

Rice bran extract production requires multi-stage processing: ethanol extraction, controlled fermentation, heat inactivation, and freeze-drying. Each step adds cost and complexity that smaller brands cannot easily absorb. This process barrier concentrates production among well-capitalized manufacturers, limiting supply-side competition and keeping retail prices elevated for end consumers.

Limited peer-reviewed clinical validation for specific efficacy claims creates skepticism among dermatologists and retail buyers. Many rice-based products reference in vitro or animal model data rather than large-scale human trials. According to Frontiers in Pharmacology, elastin fiber content increased by approximately 2.03 ± 0.11-fold after 28 days of RBE treatment in mouse skin — meaningful data, but a mouse model, not a human clinical trial, which constrains the strength of label claims.

Regulatory scrutiny of cosmetic efficacy claims adds another layer of restraint. Brands making anti-aging or collagen-stimulating assertions must substantiate them within jurisdiction-specific frameworks. When available evidence stems primarily from preclinical studies, brands face either claim dilution — reducing marketing impact — or regulatory risk, both of which slow commercial expansion into conservative retail channels.

Growth Factors

Personalization, Male Grooming, and Sustainable Packaging Open New Revenue Streams

Personalized skincare represents the next evolution of the rice-based category. Brands that build customizable rice-infused formulations — adjusting active concentrations based on skin type, climate, or concern — can command subscription premiums and improve retention. This model shifts revenue from transactional to recurring, strengthening lifetime customer value for brands that invest early in personalization infrastructure.

The male grooming segment offers structural white space for rice-based skincare brands. Men’s skincare spending has accelerated globally, yet rice-positioned products remain overwhelmingly female-targeted. According to MDPI Cosmetics, solid-state fermentation of rice with Rhizopus oryzae increased ferulic acid concentration from 33 mg/g to 765 mg/g — a 23-fold increase. This potency data makes rice extract credible for high-performance male grooming lines seeking ingredient-led positioning.

Strategic partnerships between rice agricultural processors and cosmetic manufacturers reduce raw material costs while improving bioactive consistency. Sustainable packaging aligned with eco-conscious brand values strengthens retailer acceptance and consumer trust. Brands that combine ingredient innovation with supply chain integration and packaging sustainability create compounding advantages that are difficult for single-focus competitors to replicate.

Emerging Trends

Social Media, Western Adoption of Asian Rituals, and Vegan Certifications Reshape the Competitive Map

Social media platforms have transformed rice water cleansers and toners into mass-awareness products within months of launch. Consumer-generated content around rice water rituals reaches audiences that traditional advertising cannot replicate at equivalent cost. Brands that enable and amplify this content — through ambassador programs and education-first marketing — convert social interest into measurable sales velocity.

Western markets actively adopt traditional Asian beauty rituals incorporating rice, creating cross-regional demand that regional Asian brands are uniquely positioned to serve. Celebrity and influencer endorsements accelerate this adoption by providing cultural translation for unfamiliar consumers. According to research published in the Journal of Environmental and Public Health, Riceberry extract reduced melanin production by 20.60 ± 3.67% in B16F10 melanoma cells — brightening efficacy data that gives influencer content a credible scientific anchor.

Vegan and cruelty-free certifications have moved from differentiators to baseline requirements in premium skincare retail. Rice-based formulations align naturally with vegan positioning, as fermentation and plant extraction replace animal-derived actives. Brands that obtain recognized certifications early build retail access advantages — particularly in European markets where certification visibility directly influences purchase decisions on shelf.

Regional Analysis

North America Dominates the Rice-Based Skincare Products Market with a Market Share of 32.60%, Valued at USD 2.3 Billion

North America holds a 32.60% share valued at USD 2.3 Billion, driven by a mature premium skincare consumer base and deep penetration of Asian beauty trends through specialty retail and e-commerce. U.S. consumers demonstrate willingness to pay for ingredient-backed claims, making the market structurally receptive to rice extract’s documented bioactive benefits.

Europe Rice-Based Skincare Products Market Trends

Europe represents a disciplined and regulation-aware market, where clean beauty claims require substantiation to gain retail acceptance. Consumer preference for ethically sourced, sustainably processed botanicals aligns with rice bran fermentation’s green extraction credentials. Germany, France, and the UK function as the primary entry markets, with established natural beauty retail channels providing distribution reach for credible brands.

Asia Pacific Rice-Based Skincare Products Market Trends

Asia Pacific is the origin market for rice-based skincare and continues to set global product and formulation standards. South Korea, Japan, and China produce the majority of hero products that later achieve global distribution. Consumer sophistication in this region creates competitive intensity that drives continuous innovation — brands failing to match domestic formulation standards cannot sustain market share even in export markets.

Latin America Rice-Based Skincare Products Market Trends

Latin America presents an early-stage opportunity for rice-based skincare, where consumer awareness of rice extract benefits remains limited but is building through digital channels. Brazil and Mexico lead regional adoption, supported by young, digitally engaged consumer demographics. The region’s price sensitivity requires brands to calibrate entry-level product formats before introducing premium lines.

Middle East and Africa Rice-Based Skincare Products Market Trends

The Middle East and Africa market shows emerging interest in natural and botanical skincare, with Gulf Cooperation Council countries leading premiumization trends. High consumer spending capacity in GCC markets supports luxury and functional skincare positioning. However, limited local distribution infrastructure for niche botanical brands constrains penetration speed across the broader African region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Tatcha occupies the highest-margin position in the North American rice skincare market through its Japanese luxury brand architecture. Its Rice Wash, powered by fermented rice and the proprietary Hadasei-3 complex, anchors a product ecosystem that commands consistent premium pricing. In December 2024, Tatcha announced a partnership with Ulta Beauty to expand U.S. distribution across 1,400+ stores from January 2025 — a strategic move that converts brand equity into physical retail volume at scale.

The Face Shop leverages K-beauty’s mainstream credibility to distribute rice-based formulations across both specialty retail and mass-market channels. Its strategic advantage lies in price accessibility — delivering rice extract benefits at mid-market price points that expand the addressable consumer base beyond premium buyers. This positioning creates volume throughput that specialist luxury brands cannot replicate without brand dilution.

Skinfood builds its competitive identity on the food-to-skin ingredient narrative, making rice a hero ingredient across multiple formats including cleansers, masks, and moisturizers. This brand coherence reduces consumer education cost per new product launch. The brand’s concentrated focus on food-derived actives creates a defendable niche — a structure that insulates Skinfood from broader commodity competition within the botanical skincare category.

Innisfree differentiates through its sustainability and natural sourcing narrative, connecting rice-based formulations to Jeju Island’s agricultural heritage. This origin story builds consumer trust and justifies premium positioning without requiring heavy clinical evidence marketing. Innisfree’s vertically aligned sourcing model also reduces raw material cost volatility — a structural cost advantage as fermented rice extract procurement becomes more competitive globally.

Key Players

- Tatcha

- The Face Shop

- Skinfood

- Innisfree

- Shiseido

- JUARA Skincare

- MIRABELLE COSMETICS Pvt. Ltd

- GLAMVEDA

- Kose Corporation

- Etude House

- Beauty of Joseon

- TonyMoly

- Sulwhasoo

- Neogen Dermalogy

Recent Developments

- May 2024 — Mamaearth launched its Rice Facewash with a major digital campaign featuring Palak Tiwari, emphasizing traditional Korean rice water benefits for glass-skin results. The campaign directly targeted Indian urban consumers seeking natural-origin cleansing solutions positioned against imported K-beauty alternatives.

- April 2025 — I’m From launched the Black Rice Toner, a lightweight, oil-controlling formula designed for balanced hydration and glow. The product positioned itself as a next-generation rice toner, expanding the brand’s rice ingredient line to address combination and oily skin concerns within the cleansers and toners sub-segment.

- December 2024 — Tatcha announced a strategic partnership with Ulta Beauty to expand U.S. distribution of its Japanese rice-based skincare line across 1,400+ stores starting January 2025. The expansion includes the signature Rice Wash powered by fermented rice and Hadasei-3 complex, significantly broadening physical retail reach for the brand.

- July 2025 — Zen Dew, a new skincare brand founded by B-Glowing’s Lisa King, launched the Violet Aura 2% BHA Rice Toner featuring 73% Korean rice extract alongside niacinamide and salicylic acid. The formulation targets brightening and gentle exfoliation, combining high-concentration rice extract with pharmaceutical-grade actives in a single formula.

Report Scope

Report Features Description Market Value (2025) USD 7.2 Billion Forecast Revenue (2035) USD 14.9 Billion CAGR (2026-2035) 7.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Moisturizers & Creams, Cleansers & Toners, Face Masks, Exfoliators & Scrubs, Sunscreens, Others), By End-User (Women, Men, Kids), By Distribution Channel (Offline, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Tatcha, The Face Shop, Skinfood, Innisfree, Shiseido, JUARA Skincare, MIRABELLE COSMETICS Pvt. Ltd, GLAMVEDA, Kose Corporation, Etude House, Beauty of Joseon, TonyMoly, Sulwhasoo, Neogen Dermalogy Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Rice-Based Skincare Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Rice-Based Skincare Products MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Tatcha

- The Face Shop

- Skinfood

- Innisfree

- Shiseido

- JUARA Skincare

- MIRABELLE COSMETICS Pvt. Ltd

- GLAMVEDA

- Kose Corporation

- Etude House

- Beauty of Joseon

- TonyMoly

- Sulwhasoo

- Neogen Dermalogy

Our Clients

- 182648

- Mar 2026