Quick Navigation

Report Overview

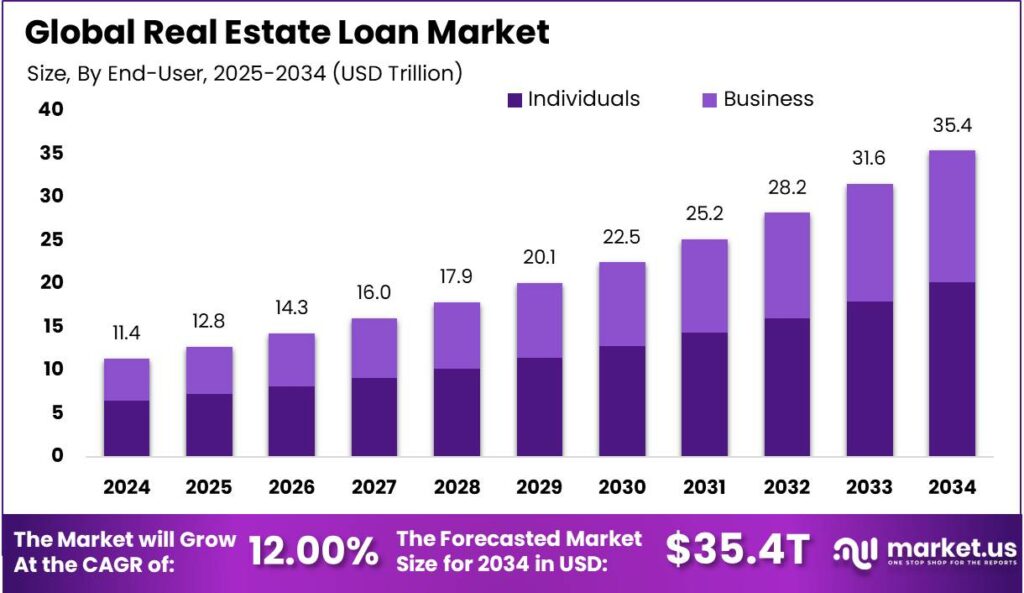

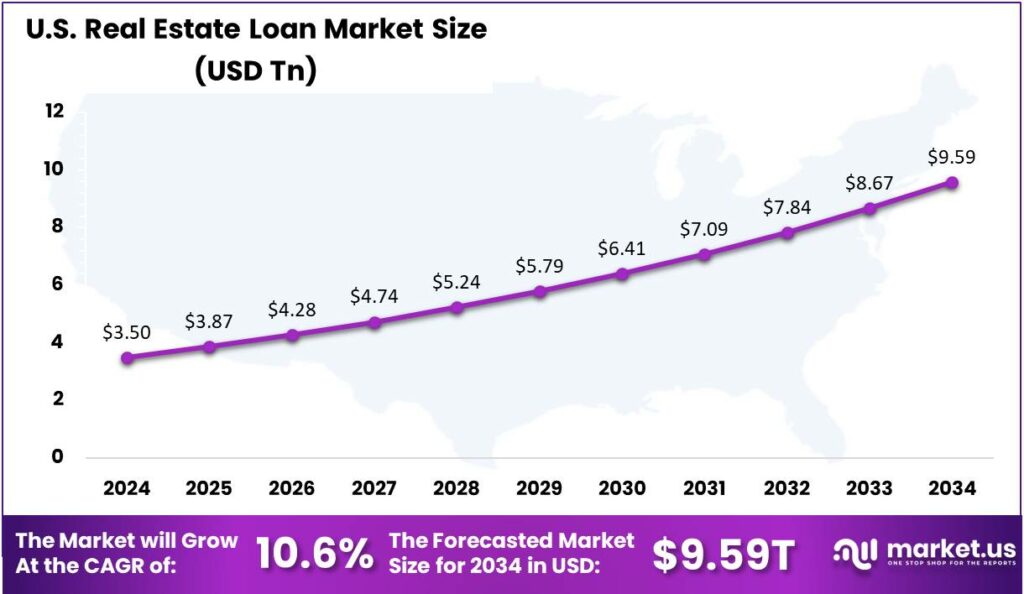

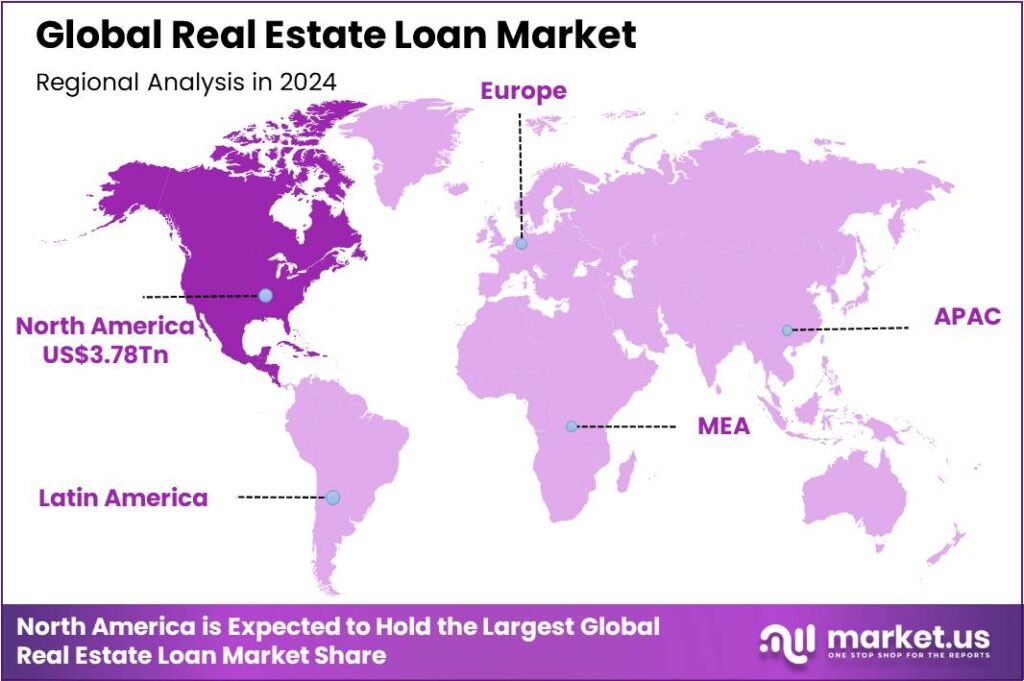

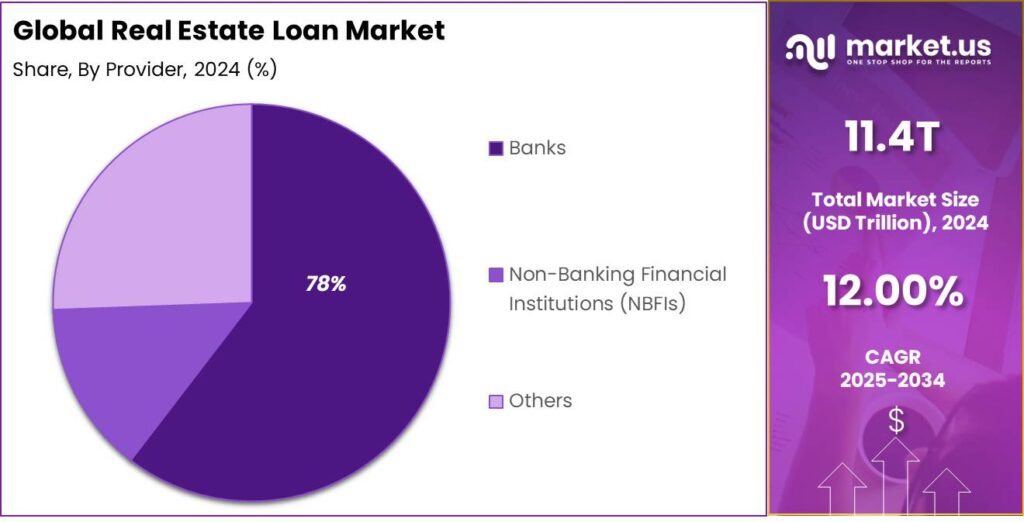

The Global Real Estate Loan Market size is expected to be worth around USD 35.4 Trillion By 2034, from USD 11.4 Trillion in 2024, growing at a CAGR of 12.00% during the forecast period from 2025 to 2034. In 2024, North America dominated the global real estate loan market, holding over 33.2% market share and generating USD 3.78 trillion in revenue. The U.S. market was valued at USD 3.5 trillion, with a projected CAGR of 10.6%.

The real estate loan market encompasses all lending activities related to property transactions. Several key factors are propelling the growth of the real estate loan market. Government policies, such as the Pradhan Mantri Awas Yojana (PMAY), aim to provide affordable housing, boosting demand for home loans. Technological advancements have streamlined loan processing, making it more accessible.

The demand for real estate loans in India is on the rise, particularly in metropolitan areas and emerging urban centers. This surge is attributed to increasing urbanization, rising disposable incomes, and the desire for homeownership. Moreover, the government’s focus on infrastructure development and smart cities has spurred real estate activities, further amplifying the need for financing options.

Technological innovations are transforming the real estate loan landscape. Digital platforms now offer end-to-end loan processing, from application to disbursement, reducing turnaround times. Artificial intelligence (AI) and machine learning algorithms assess creditworthiness more accurately, while blockchain ensures secure and transparent transactions. These technologies not only enhance efficiency but also improve customer experience .

The adoption of these technologies is driven by the need for faster processing, reduced operational costs, and enhanced customer satisfaction. Digital tools minimize paperwork, lower the risk of errors, and provide real-time updates to borrowers. For lenders, technology enables better risk assessment and portfolio management, leading to more informed lending decisions .

Investment opportunities in the real estate loan market are abundant. Investors can explore avenues like mortgage-backed securities, real estate investment trusts (REITs), and direct lending platforms. The sector’s growth potential, backed by strong demand and supportive policies, makes it an attractive option for both domestic and international investors seeking stable returns.

Businesses benefit from the real estate loan market through increased access to capital for expansion and development projects. For financial institutions, offering real estate loans diversifies their portfolio and generates steady income streams. Additionally, the integration of technology in loan processing enhances operational efficiency and customer engagement.

Key Takeaways

- The Global Real Estate Loan Market size is expected to be worth around USD 35.4 Trillion by 2034, growing from USD 11.4 Trillion in 2024, at a CAGR of 12.00% during the forecast period from 2025 to 2034.

- In 2024, the Banks segment held a dominant market position, capturing more than 78% share in the real estate loan market.

- In 2024, the Individuals segment dominated the market, holding over 57% of the global real estate loan market share.

- The Residential segment also held a dominant market position in 2024, accounting for over 61% of the total share in the global real estate loan market.

- North America was the dominant region in the global real estate loan market in 2024, capturing more than 33.2% of the total market share and generating a remarkable USD 3.78 trillion in revenue.

- The U.S. Real Estate Loan Market was valued at USD 3.5 trillion in 2024 and is projected to grow at a CAGR of 10.6%.

U.S. Market Influence

In 2024, the U.S. Real Estate Loan Market reached an impressive valuation of $3.5 trillion, reflecting its critical role in financing residential, commercial, and industrial property developments across the country. This enormous figure underscores the market’s deep integration within the broader financial ecosystem, as it supports everything from first-time home purchases to large-scale infrastructure projects.

The U.S. Real Estate Loan Market is currently expanding at a compound annual growth rate (CAGR) of 10.6%, which points to robust investor confidence and consistent demand from borrowers. This growth is fueled by a combination of factors, including low interest rates in previous years, urban expansion, demographic shifts, and technological innovation in mortgage processing and lending platforms.

The U.S. Real Estate Loan Market is set for continued growth amid stabilizing macroeconomic conditions and rising investor interest. Enhanced digitization, fintech partnerships, and tailored lending options are expanding credit access. Additionally, government initiatives supporting affordable housing and sustainability are fueling momentum in this trillion-dollar sector.

In 2024, North America held a dominant market position in the global Real Estate Loan Market, capturing more than 33.2% of the total share and generating a staggering USD 3.78 trillion in revenue. This commanding presence is largely driven by the strong economic foundation of the United States, which accounts for the lion’s share of the regional performance.

North America’s edge lies in broad credit access, a diverse financial ecosystem, and growing fintech integration in mortgages. Digital advances have streamlined loan processing and personalized lending. In the U.S. and Canada, strong job markets, urban growth in secondary cities, and suburban migration continue to drive mortgage demand.

Government policies strongly support North America’s real estate loan market. U.S. programs like FHA and VA loans aid first-time buyers, while tax incentives and Fed rate adjustments boost borrowing. Growing institutional investment in mortgage-backed securities adds liquidity. Combined with market transparency and legal stability, these factors keep the region globally competitive.

North America is poised to remain the global leader in real estate lending, supported by adaptive regulations, rising urban housing demand, and strong commercial financing. While APAC and Europe grow, North America’s scale, innovation, and policy backing keep it the market’s anchor.

Provider Analysis

In 2024, Banks segment held a dominant market position, capturing more than a 78% share in the real estate loan market. This dominance is largely attributed to their deep-rooted trust among borrowers, vast financial infrastructure, and regulatory credibility.

Banks also have a long-standing relationship with regulatory bodies, allowing them to seamlessly implement evolving compliance requirements like stress tests, risk assessments, and disclosure norms. This alignment with governance ensures smoother operations in the lending process and builds further consumer confidence.

Banks have strengthened their leadership by embracing digital lending, using AI underwriting, automated KYC, and mobile applications to speed up approvals. These tech advances have reshaped banks into agile, secure, and innovative lenders, with many partnering with PropTech firms for real-time loan tracking and property valuation.

Non-Banking Financial Institutions (NBFIs) are growing in niche and underserved segments, but banks hold a clear advantage in the mainstream market due to trust, regulatory backing, and widespread access. As property financing demand rises, especially in emerging economies, banks are set to maintain their lead, thanks to their scalability and strong compliance framework.

End-User Analysis

In 2024, the Individuals segment held a dominant market position, capturing more than a 57% share of the global real estate loan market. This dominance stems largely from the ongoing rise in homeownership aspirations among middle-income families, young professionals, and first-time buyers.

With increasing access to housing finance, especially in developing economies, individuals are finding it easier than ever to secure loans for buying residential properties. Supportive government schemes such as interest subsidies, tax incentives, and affordable housing programs have made real estate loans more accessible and attractive for this segment.

Another major factor contributing to the rise of the individuals segment is the growing financial inclusion brought about by digital banking. Mobile-first loan applications, simplified KYC procedures, and AI-backed credit assessments are enabling a broader range of people especially those from semi-urban and rural areas to participate in the housing finance ecosystem.

The cultural and emotional value of home ownership also plays a strong role in propelling the individuals segment forward. Owning property is often seen as a long-term investment and a mark of financial stability in many cultures. As real estate continues to be perceived as a safer, appreciating asset, more individuals are willing to commit to long-term loans.

Property Type Analysis

In 2024, the Residential segment held a dominant market position in the global Real Estate Loan Market, accounting for more than 61% of the total share. This dominance is primarily attributed to the consistently high demand for housing, particularly in urban and suburban areas where population density and affordability pressures remain strong.

Residential loans lead due to their high transaction volume and frequent refinancing activity. The shift to remote work has boosted demand for larger homes in suburban areas, driving up loan volumes and reinforcing the dominance of the residential segment in the real estate loan market.

Unlike commercial real estate, which is more cyclical and vulnerable to economic fluctuations, the residential sector provides greater stability for lenders, as housing demand remains consistent. Digital mortgage platforms and non-bank lenders have further improved access to housing credit, even in areas with limited traditional banking infrastructure, reducing risk for financial institutions.

The residential segment is set to maintain its dominance, driven by strong demographic demand, particularly in rapidly urbanizing developing markets. Rising incomes, greater financial literacy, and digital loan services, along with supportive government policies, will ensure residential real estate lending remains a leading force in the global market.

Key Market Segments

By Provider

- Banks

- Non-Banking Financial Institutions (NBFIs)

- Others

By End-User

- Business

- Individuals

By Property Type

- Residential

- Commercial

- Hotels

- Retail

- Industrial

- Office

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Aspirations and Urban Migration

The younger population in India views homeownership as a symbol of success, driving demand for real estate. Urban migration for better job opportunities, combined with cultural aspirations and financial support, has fueled the demand for housing. This trend is expected to continue as more people aim to settle in urban areas and achieve their homeownership dreams.

As cities grow and new urban areas develop, the need for residential spaces increases. This urban migration has spurred the creation of new housing projects in both major cities and emerging urban centers. Financial institutions are offering customized loan products for first-time homebuyers and those upgrading their homes.

Restraint

High Property Prices and Limited Affordability

Rising property prices in urban areas, driven by higher land, construction, and labor costs, have become a major barrier to homeownership. This price surge has outpaced income growth, making it difficult for many to afford homes in prime locations. Financial institutions offer various loan products, but high down payments and strict eligibility criteria limit access to housing finance for many buyers.

The combination of rising property prices and limited affordability has slowed the real estate market, with developers struggling to sell units and buyers delaying decisions in hopes of better prices or financial conditions. Overcoming this challenge requires joint efforts from both the government and the private sector to make housing more affordable and accessible.

Opportunity

Affordable Housing Initiatives

The government’s focus on affordable housing creates a major opportunity for the real estate loan sector. Through subsidies and incentives for buyers and developers, these initiatives make homeownership more accessible to lower and middle-income groups by reducing financial burdens, driving increased market participation.

Financial institutions are aligning their products to offer tailored loan options, supporting the growing affordable housing market. Public-private collaboration is expanding the market, especially in peripheral urban areas, addressing housing shortages and boosting regional economic activity. This focus on affordable housing presents both a social initiative and a strategic economic opportunity, driving growth in the real estate loan sector.

Challenge

Regulatory and Bureaucratic Hurdles

Despite progress in promoting housing, the real estate sector faces regulatory and bureaucratic challenges. Lengthy approval processes, varying regulations across states and municipalities, and a lack of transparency lead to project delays and increased costs, hindering timely execution.

Legal complexities around property titles, registration, and compliance deter potential buyers, impacting demand for real estate loans. While regulations like RERA aim for transparency, inconsistent implementation undermines confidence. Systemic reforms are needed to streamline processes, enhance transparency, and ensure consistent regulation, fostering growth in the real estate loan sector.

Emerging Trends

One notable trend is the adaptation of office spaces. With the rise of remote work, many traditional office buildings are being repurposed into residential units or data centers. This shift addresses the decreased demand for conventional office spaces and meets the growing need for housing and digital infrastructure.

Another emerging trend is the increased focus on multifamily housing and neighborhood retail sectors. These areas have shown resilience amidst economic fluctuations, attracting both lenders and investors. The consistent demand for housing and local retail ensures steady returns, making them appealing investment avenues.

Technological advancements are also reshaping the lending process. The integration of digital tools streamlines loan applications, approvals, and management, enhancing efficiency for both lenders and borrowers. This digital shift not only speeds up processes but also improves transparency and accessibility in real estate financing.

Business Benefits

Real estate loans offer businesses stability by allowing them to own their premises, providing control and permanence. Unlike renting, where lease terms can change, ownership removes the uncertainty of relocations or rent hikes, enabling long-term planning.

Real estate loans often come with fixed interest rates, leading to consistent monthly payments. This predictability aids in budgeting and financial planning, ensuring that housing costs remain stable over the loan term. In contrast, renting can expose businesses to fluctuating market rents, making long-term financial forecasting more challenging.

A business that owns its premises may be more attractive to potential buyers or investors. The property adds tangible value to the company, which can be a significant factor during valuation. Additionally, owning property provides flexibility in exit strategies.

Key Player Analysis

Key players in this market play a significant role in shaping trends, offering competitive rates, and providing various loan products to meet diverse borrower needs.

JPMorgan Chase & Co. is a leading player in the real estate loan market. JPMorgan, one of the largest global banks, offers a variety of real estate loan products, from residential mortgages to commercial property financing. With its strong financial position and global reach, it provides flexible terms and competitive rates to both homeowners and developers.

Bank of America Corporation is another major player in the real estate loan market. Known for its customer-centric approach, it offers various home loan products such as mortgages, home equity lines of credit, and refinancing options. Its ability to provide personalized services and competitive pricing makes it a popular choice among borrowers.

Citigroup Inc. is a key player in the real estate loan market, offering a broad range of mortgage and real estate lending services. Citigroup’s global network and diverse lending options allow it to meet the needs of a wide spectrum of borrowers, from first-time homebuyers to large commercial real estate investors.

Top Key Players in the Market

- JPMorgan Chase & Co.

- Bank of America Corporation

- Citigroup Inc.

- U.S. Bank

- The PNC Financial Services Group Inc.

- Fairway Independent Mortgage Corporation

- HomeBridge Financial Services

- Caliber Home Loans Inc.

- New American Funding LLC

- Navy Federal Credit Union

- loanDepot.com LLC

- Guild Mortgage Company

- Flagstar Bank N.A.

- Movement Mortgage

- Carrington Mortgage Services LLC

- Embrace Home Loans Inc.

- Northpointe Bank

- Sierra Pacific Mortgage Company Inc.

- PrimeLending

- Others

Top Opportunities for Players

- Surge in Refinancing Activity: With recent interest rate cuts, many homeowners are exploring refinancing options to secure better mortgage deals. This trend is leading to increased competition among lenders, prompting them to offer more attractive terms. For real estate loan providers, this environment offers a chance to expand their customer base by catering to borrowers seeking to optimize their loan conditions.

- Expansion of Private Credit Markets: Traditional banks are becoming more cautious in their lending practices, creating a space for private credit firms to step in. These firms are increasingly providing loans for real estate ventures, offering more flexible terms and faster approvals. This shift allows real estate loan players to diversify their funding sources and tap into new borrower segments.

- Emphasis on Sustainable and Green Financing: There’s a growing demand for environmentally friendly real estate projects. Lenders who offer green financing options can attract developers focused on sustainable construction. This not only meets the market’s evolving preferences but also aligns with global sustainability goals, positioning lenders as forward-thinking and socially responsible.

- Technological Advancements in Lending Processes: The adoption of digital tools is transforming the real estate loan industry. From online applications to automated underwriting, technology is enhancing efficiency and customer experience. Lenders embracing these innovations can process loans faster, reduce errors, and offer more personalized services, gaining a competitive edge in the market.

- Opportunities in Underserved Markets: Certain regions and demographics remain underbanked, presenting a significant opportunity for real estate loan providers. By developing tailored loan products and outreach strategies, lenders can tap into these markets, fostering financial inclusion and driving growth in areas previously overlooked.

Recent Developments

- In April 2025, Bank of America released its Specialty Asset Management Outlook, discussing trends in commercial real estate and other asset classes.

- In August 2024, HomeBridge enhanced its Access (Non-QM) program, increasing the maximum loan amount and adjusting loan-to-value ratios to better serve borrowers with non-traditional income sources.

- In June 2024, PrimeLending launched a new home equity loan product, offering homeowners the ability to convert home equity into cash.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 11.4 Trillion |

| Forecast Revenue (2034) | USD 35.4 Trillion |

| CAGR (2025-2034) | 12.00% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Provider (Banks, Non-Banking Financial Institutions (NBFIs), Others), By End-User (Business, Individuals), By Property Type (Residential, Commercial (Hotels, Retail, Industrial, Office, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | JPMorgan Chase & Co., Bank of America Corporation, Citigroup Inc., U.S. Bank, The PNC Financial Services Group Inc., Fairway Independent Mortgage Corporation, HomeBridge Financial Services, Caliber Home Loans Inc., New American Funding LLC, Navy Federal Credit Union, loanDepot.com LLC, Guild Mortgage Company, Flagstar Bank N.A., Movement Mortgage, Carrington Mortgage Services LLC, Embrace Home Loans Inc., Northpointe Bank, Sierra Pacific Mortgage Company Inc., PrimeLending, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |