Global Quartz Market Size, Share, Growth Analysis By Product Type (High-purity Quartz [Quartz Surface and Tile, Fused Quartz Crucible, Quartz Glass], Quartz Crystal, Silicon Metal), By End-user Industry (Building & Construction, Electronics & Semiconductor, Solar, Optical Fiber & Telecommunication, Automotive, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178748

- Number of Pages: 234

- Format:

-

keyboard_arrow_up

Quick Navigation

Market Overview

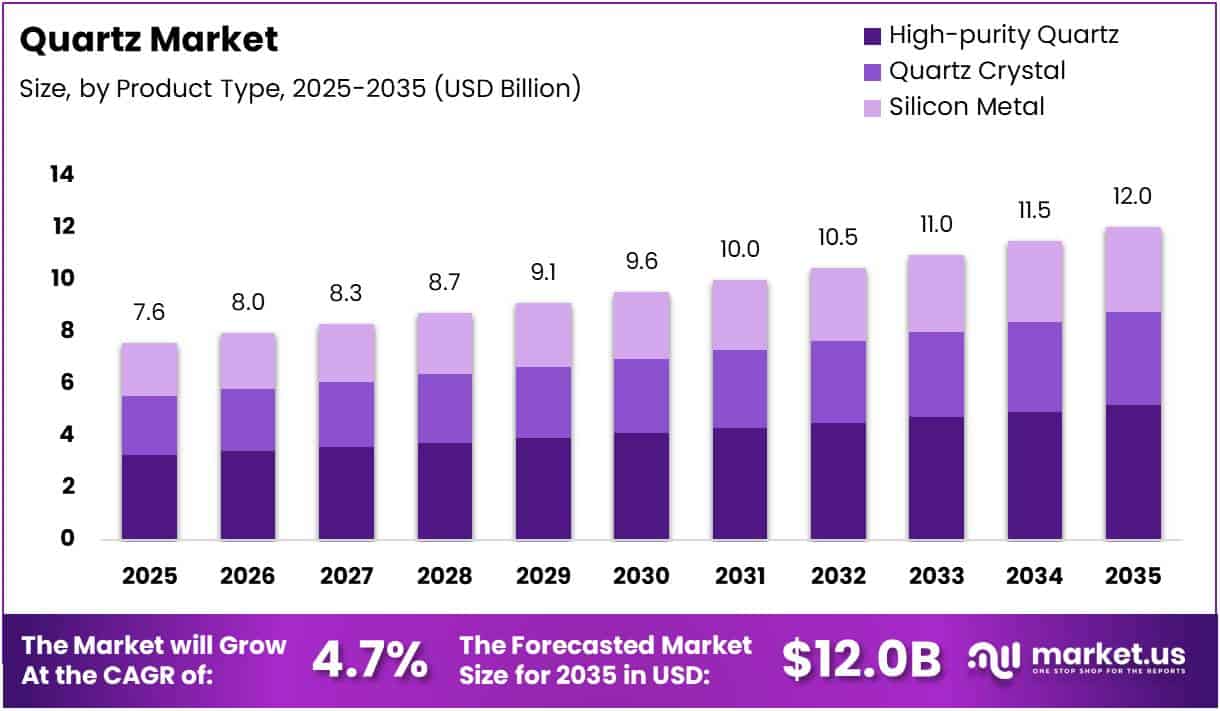

The Global Quartz Market size is expected to be worth around USD 12.0 Billion by 2035 from USD 7.6 Billion in 2025, growing at a CAGR of 4.7% during the forecast period 2026 to 2035.

Quartz is one of the most abundant and industrially significant minerals found in the Earth’s crust. It is valued for its exceptional hardness, chemical stability, and optical clarity. Moreover, high-purity quartz has become a critical raw material in advanced manufacturing, particularly for semiconductor-grade silicon wafer production and photovoltaic system components.

The quartz market encompasses a wide range of product types, including high-purity quartz, quartz surfaces and tiles, fused quartz crucibles, quartz glass, quartz crystals, and silicon metal. Each product category serves distinct industries. Consequently, the market benefits from diverse end-use demand that limits exposure to cyclical downturns in any single application sector.

Rapid growth in global semiconductor fabrication continues to fuel demand for high-purity quartz crucibles and precision components. Simultaneously, large-scale solar energy deployment worldwide has accelerated quartz-based material consumption. Additionally, construction sector expansion, especially across emerging economies, is sustaining strong demand for engineered quartz surfaces in both residential and commercial development projects.

Governments across major economies are actively investing in clean energy infrastructure and domestic semiconductor supply chains, creating favorable policy conditions for quartz producers. Evolving regulations around responsible mining are reshaping production strategies at the same time. Therefore, industry participants are prioritizing synthetic quartz development and sustainable extraction methods to align with environmental compliance requirements.

According to farmonaut.com, high-purity quartz used in photovoltaic silicon production contributes to 25–30% improved energy conversion efficiency in next-generation solar cells. This performance advantage underscores quartz’s growing strategic importance in the global clean energy transition. Moreover, according to IQD Frequency Products, quartz crystals maintain reliable performance when specified within a temperature range of -20 to 70 °C.

According to universalquartzz.com, quartz countertops have the potential to last between 20 to 60 years, reflecting the material’s exceptional durability and long service life. High-quality quartz countertops are composed of 90% or more quartz content. Consequently, architects and interior designers continue to specify quartz surfaces as a premium, low-maintenance choice in modern construction and renovation projects.

Key Takeaways

- The global Quartz Market is valued at USD 7.6 Billion in 2025 and is projected to reach USD 12.0 Billion by 2035.

- The market is growing at a CAGR of 4.7% during the forecast period 2026 to 2035.

- By Product Type, High-purity Quartz dominates the segment with a 43.1% market share in 2025.

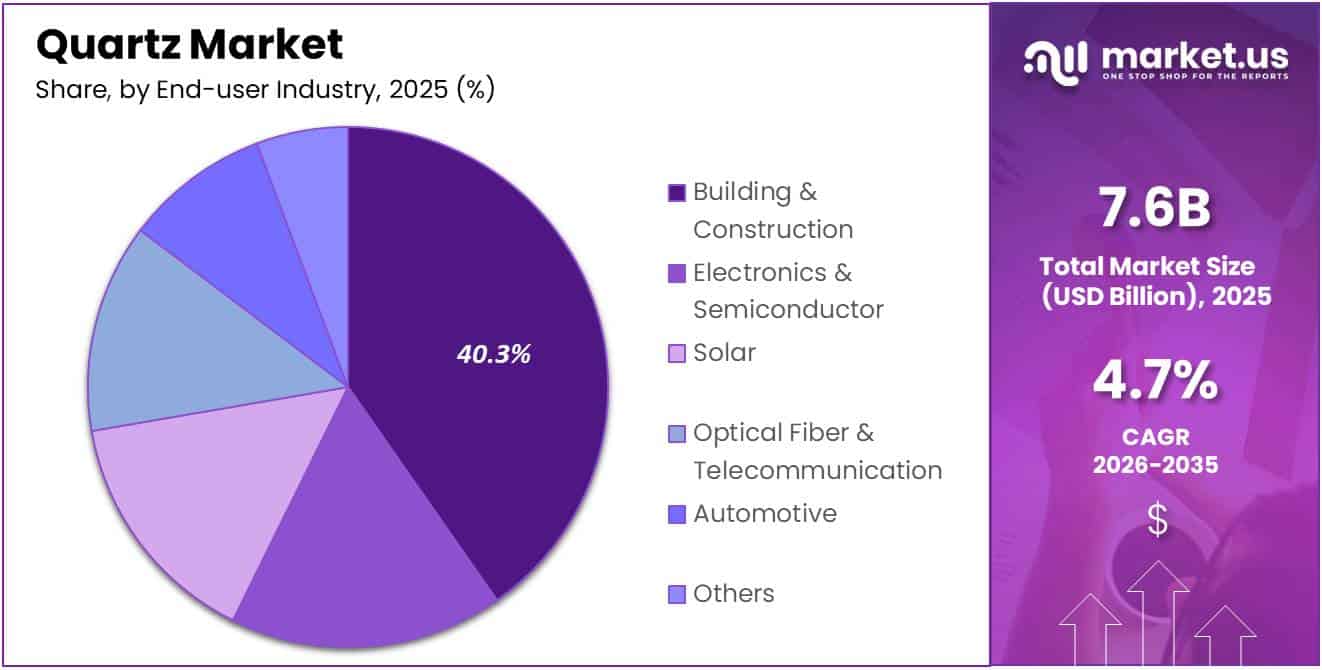

- By End-user Industry, Building & Construction holds the leading position with a 40.3% share in 2025.

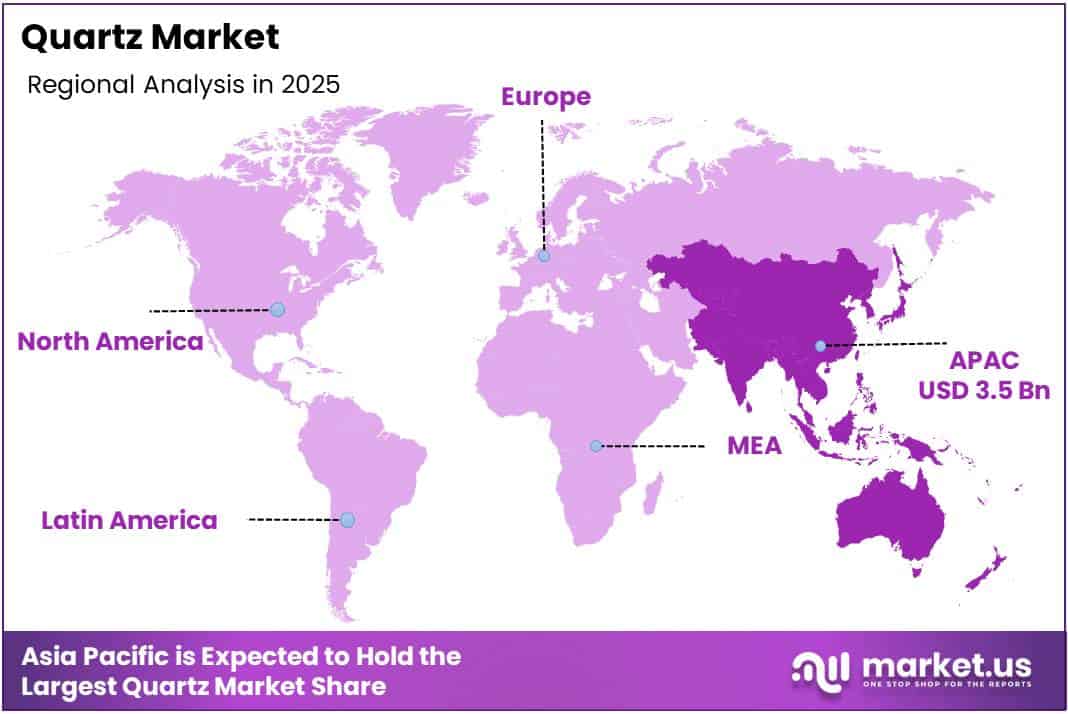

- Asia Pacific leads the global Quartz Market with a 45.5% regional share, valued at USD 3.5 Billion.

Product Type Analysis

High-purity Quartz dominates with 43.1% due to its critical role in semiconductor and solar manufacturing.

In 2025, High-purity Quartz held a dominant market position in the By Product Type segment of the Quartz Market, with a 43.1% share. Its dominance is driven by rising demand in semiconductor wafer production, photovoltaic silicon processing, and optical components. Moreover, its unmatched purity levels make it irreplaceable in high-technology industrial applications.

Quartz Crystal is widely used as a frequency control element in electronics, telecommunications, and timing devices. Its stability across defined temperature ranges ensures consistent performance in precision applications. Therefore, expanding consumer electronics production and growing deployment of wireless communication systems continue to support steady demand for quartz crystal components.

Silicon Metal, derived from quartz-based raw materials, is an important sub-segment serving chemical, aluminum, and semiconductor industries. It is also a key input in silicone compound production. Moreover, growing demand from electric vehicle battery systems and advanced electronics manufacturing is expected to support incremental volume growth in this sub-segment through the forecast period.

End-user Industry Analysis

Building & Construction dominates with 40.3% due to high demand for engineered quartz surfaces in residential and commercial projects.

In 2025, Building & Construction held a dominant market position in the By End-user Industry segment of the Quartz Market, with a 40.3% share. Urbanization, infrastructure investment, and consumer preference for durable premium surfaces continue to drive quartz surface demand. Moreover, engineered quartz tiles and countertops are increasingly specified in both new builds and renovation projects.

Electronics & Semiconductor represents a strategically important and fast-growing end-user segment for quartz, particularly for high-purity grades. Demand from chip fabricators and electronics manufacturers is expanding with each new semiconductor generation. Consequently, capacity investments in advanced node semiconductor plants globally are creating sustained long-term demand for high-specification quartz materials.

Solar is one of the most dynamic end-use segments, driven by rapid global expansion of photovoltaic energy capacity. Quartz crucibles and high-purity quartz are consumed intensively in polysilicon and wafer production. Additionally, government-backed clean energy mandates and declining solar installation costs are expected to accelerate quartz consumption in this segment through the forecast period.

Optical Fiber & Telecommunication relies on quartz glass as a primary material for manufacturing fiber optic cables and optical transmission components. Rising demand for high-speed broadband infrastructure globally is a key demand driver. Moreover, expansion of 5G networks and undersea cable deployments is increasing the consumption of high-purity quartz glass products worldwide.

Automotive is an emerging end-user segment for quartz, particularly in electronic control units, sensors, and timing devices embedded in modern vehicles. Growth in electric vehicle production is further expanding quartz-based component demand. Therefore, as vehicle electronics content increases, the automotive segment is expected to represent a progressively larger share of total quartz consumption.

Others include applications across medical devices, laboratory instruments, lighting, and industrial equipment. These segments collectively contribute stable incremental demand for specialty quartz products. Additionally, niche applications in aerospace, defense, and precision measurement systems further diversify the end-user base and support market resilience against demand fluctuations in any primary sector.

Key Market Segments

By Product Type

- High-purity Quartz

- Quartz Surface and Tile

- Fused Quartz Crucible

- Quartz Glass

- Quartz Crystal

- Silicon Metal

By End-user Industry

- Building & Construction

- Electronics & Semiconductor

- Solar

- Optical Fiber & Telecommunication

- Automotive

- Others

Drivers

Rising Industrial and Technological Demand Drives Sustained Growth in the Quartz Market

The semiconductor and electronics manufacturing sector is one of the most powerful demand drivers for high-purity quartz globally. Continuous expansion of chip fabrication facilities and advancement to smaller process nodes require increasingly pure quartz crucibles and components. Moreover, government investment in domestic semiconductor production across the US, Europe, and Asia is reinforcing this demand trajectory.

Expanding construction activity across both developed and emerging markets is significantly boosting consumption of engineered quartz surfaces and tiles. Rising urbanization and infrastructure development programs are increasing the installation of quartz countertops, flooring, and cladding. Additionally, the growing preference of consumers and architects for durable, low-maintenance premium surfaces continues to support steady volume growth in this segment.

The global expansion of photovoltaic solar panels installations is creating strong and sustained demand for quartz crucibles and high-purity quartz components used in silicon ingot and wafer production. Renewable energy targets set by governments worldwide are driving large-scale solar project development. Consequently, quartz producers supplying the solar value chain are well-positioned to benefit from this long-term structural growth driver.

Restraints

Regulatory Pressures and Material Substitution Pose Key Challenges to Quartz Market Expansion

Stringent environmental and mining regulations across major quartz-producing regions are limiting the pace of new extraction activity. Permitting requirements, land use restrictions, and environmental impact assessments are increasing both lead times and operational costs for producers. Moreover, tightening emission standards for mining and processing operations are adding compliance burdens that constrain capacity expansion plans in several markets.

The availability of alternative surface materials, including porcelain, ceramic tiles, marble composites, and advanced polymer-based products, presents a meaningful substitution risk for quartz in construction and interior design applications. These alternatives are often competitively priced and widely available. Therefore, quartz surface manufacturers must continue investing in design differentiation and performance improvements to maintain preference among architects and end consumers.

Supply chain concentration in high-purity quartz remains a structural vulnerability for the market. A limited number of geological deposits worldwide meet the stringent purity specifications required for semiconductor and solar applications. Consequently, end-users in critical manufacturing sectors face potential supply constraints during periods of high demand, which can lead to price volatility and procurement uncertainty across the value chain.

Growth Factors

Advanced Applications and Technology Investments Create Significant Growth Opportunities for the Quartz Market

Growing adoption of quartz glass in advanced optical and fiber communication systems represents a high-value growth avenue for the market. Deployment of 5G infrastructure, expansion of data center interconnects, and development of undersea cable networks are increasing consumption of specialty quartz optical components. Moreover, ongoing R&D into photonic systems is expected to open further application opportunities for high-performance quartz materials.

Emerging applications in electric vehicle battery manufacturing and power electronics represent a fast-growing opportunity for the quartz market. Quartz-derived silicon is a key input in silicon anode battery development and high-efficiency power semiconductor devices. Additionally, the global push for electrification in transportation and industrial systems is expected to drive significant incremental demand for quartz-based materials over the forecast period.

Technological advancements in synthetic quartz production are enabling more consistent purity levels and reducing dependence on natural deposit variability. Precision industrial uses in optics, sensors, and quantum computing require tightly controlled material specifications. Therefore, producers investing in synthetic and engineered quartz manufacturing capabilities are well-positioned to capture premium market segments that demand superior performance and supply reliability.

Emerging Trends

Sustainability, Premiumization, and Capacity Investment Define the Evolving Quartz Market Landscape

The quartz industry is witnessing a clear shift toward sustainable and low-emission mining and processing practices. Producers are adopting cleaner extraction technologies, reducing water usage, and minimizing land disturbance to meet regulatory expectations and corporate sustainability goals. Moreover, growing pressure from downstream buyers in electronics and solar sectors is accelerating the adoption of environmentally responsible supply chain standards across the industry.

Rising consumer preference for customized and premium quartz surface designs in residential and commercial interior spaces is reshaping product development strategies. Architects, designers, and homeowners are increasingly requesting unique color patterns, textures, and finishes. Consequently, quartz surface manufacturers are expanding their design portfolios and investing in advanced fabrication technologies to meet evolving aesthetic demand in the high-end construction segment.

Investment in high-purity quartz capacity expansion is accelerating, driven by rising demand from next-generation chip manufacturing and solar photovoltaic production. Leading mining and processing companies are developing new deposits and upgrading purification technologies. Additionally, strategic partnerships between quartz producers and semiconductor manufacturers are emerging to secure long-term supply of specification-grade materials critical to advanced electronics and clean energy value chains.

Regional Analysis

Asia Pacific Dominates the Quartz Market with a Market Share of 45.5%, Valued at USD 3.5 Billion

Asia Pacific leads the global Quartz Market, commanding a 45.5% share and a market valuation of USD 3.5 Billion in 2025. The region’s dominance is driven by its large-scale semiconductor fabrication, solar panel manufacturing, and construction industries. Moreover, countries such as China, Japan, South Korea, and India are significant consumers of both high-purity quartz and engineered quartz surfaces.

North America Quartz Market Trends

North America represents a mature and technologically advanced market for quartz, with strong demand from the semiconductor, electronics, and construction sectors. The United States is a key consumer of high-purity quartz for chip manufacturing and optical applications. Additionally, rising investment in domestic semiconductor production under federal industrial policy initiatives is expected to further support regional quartz demand over the forecast period.

Europe Quartz Market Trends

Europe maintains a stable and well-established quartz market, supported by its advanced industrial base in optics, precision engineering, and construction. Germany, France, and the United Kingdom are among the leading consumers in the region. Moreover, Europe’s push toward clean energy and semiconductor self-sufficiency through targeted industrial policies is creating incremental demand for high-specification quartz materials across multiple value chains.

Latin America Quartz Market Trends

Latin America represents a developing market for quartz, with Brazil and Mexico serving as primary consumption centers. Growth is mainly linked to construction sector expansion and increased infrastructure investment across the region. However, the market is also beginning to see broader adoption of quartz surfaces in commercial and residential projects, supporting gradual increases in regional demand over the coming years.

Middle East and Africa Quartz Market Trends

The Middle East and Africa region presents emerging growth opportunities in the quartz market, primarily driven by construction and urban development activity across Gulf Cooperation Council countries. Large-scale real estate, hospitality, and infrastructure projects are increasing consumption of quartz surfaces and tiles. Additionally, growing interest in solar energy deployment across the region may support longer-term demand for quartz components in photovoltaic applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AGC Inc. is a global leader in glass and advanced material solutions, with quartz glass products serving semiconductor, display, and optical fiber markets. The company leverages decades of material science expertise to develop high-purity quartz components for precision industrial applications. Moreover, its diversified product portfolio and strong R&D capabilities position it competitively across multiple high-growth segments of the quartz market.

Australian Silica Quartz Group Ltd is focused on the exploration and development of high-purity silica quartz resources, targeting supply to the rapidly growing semiconductor and solar industries. The company’s Australian deposits are recognized for their exceptional mineral quality and low contamination levels. Additionally, increasing global demand for specification-grade quartz raw materials presents significant long-term commercial opportunities for the company’s extraction and processing operations.

Dow is a global materials science company with a broad presence in silicon-based chemicals and specialty materials derived from quartz and silica feedstocks. Its silicone and silicon metal product lines serve end markets including construction, electronics, automotive, and energy. Consequently, Dow’s established manufacturing infrastructure and extensive customer relationships across industrial sectors make it a significant participant in the global quartz value chain.

Elkem ASA is a leading producer of silicon-based advanced materials, supplying silicon metal, silicones, and specialty compounds to global industrial markets. The company’s operations integrate quartz mining, smelting, and downstream material production. Furthermore, Elkem’s strategic investments in sustainable production technologies and growing exposure to electric vehicle and solar energy applications are expected to support its long-term competitive positioning within the evolving quartz and silicon materials market.

Key Players

- AGC Inc.

- Australian Silica Quartz Group Ltd

- Dow

- Elkem ASA

- Ferroglobe

- Imerys

- India Quartz

- Jiangsu Pacific Quartz Co., Ltd

- MACTUS

- NIHON DEMPA KOGYO CO., LTD.

- Nordic Mining ASA

- Saint-Gobain

- Sibelco

- SIMCOA

- The Quartz Corp

- Other Key Players

Recent Developments

- January 2025 – Heraeus announced the merger of Heraeus Conamic and Heraeus Comvance into a single new operating company, consolidating its high-performance quartz and advanced materials capabilities. This strategic integration is expected to streamline operations and strengthen the company’s ability to serve semiconductor and industrial customers with a unified product portfolio.

- July 2025 – Zhengfan Technology completed a strategic acquisition of Hanjing Semiconductor for 1.12 Billion Yuan, accelerating domestic production of core semiconductor materials including quartz-based components. This transaction reflects growing Chinese investment in vertically integrated semiconductor supply chains and positions Zhengfan Technology as a more significant player in the high-purity quartz and semiconductor materials market.

- November 2025 – Silicon Metals Corp. entered into a Share Purchase Agreement for the acquisition of the Crystal Hills Project, expanding its resource base in quartz and silicon metal raw materials. This move is aligned with increasing global demand for quartz-derived silicon in photovoltaic, semiconductor, and electric vehicle applications across major industrial markets.

Report Scope

Report Features Description Market Value (2025) USD 7.6 Billion Forecast Revenue (2035) USD 12.0 Billion CAGR (2026-2035) 4.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (High-purity Quartz, Quartz Surface and Tile, Fused Quartz Crucible, Quartz Glass, Quartz Crystal, Silicon Metal), By End-user Industry (Building & Construction, Electronics & Semiconductor, Solar, Optical Fiber & Telecommunication, Automotive, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape AGC Inc., Australian Silica Quartz Group Ltd, Dow, Elkem ASA, Ferroglobe, Imerys, India Quartz, Jiangsu Pacific Quartz Co., Ltd, MACTUS, NIHON DEMPA KOGYO CO., LTD., Nordic Mining ASA, Saint-Gobain, Sibelco, SIMCOA, The Quartz Corp Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- AGC Inc.

- Australian Silica Quartz Group Ltd

- Dow

- Elkem ASA

- Ferroglobe

- Imerys

- India Quartz

- Jiangsu Pacific Quartz Co., Ltd

- MACTUS

- NIHON DEMPA KOGYO CO., LTD.

- Nordic Mining ASA

- Saint-Gobain

- Sibelco

- SIMCOA

- The Quartz Corp

- Other Key Players

Our Clients

- 178748

- Feb 2026