Global Phosphate Chemical Reagents Market Size, Share, And Enhanced Productivity By Type (Ammonium Phosphate, Calcium Phosphate, Sodium Phosphate, Potassium Phosphate, Others), By Formulation Type (Phosphoric Acid, Phosphate Salts, Phosphate Esters and Organic Phosphates), By Application (Agriculture, Water Treatment, Food and Beverage, Pharmaceuticals, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178066

- Number of Pages: 366

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

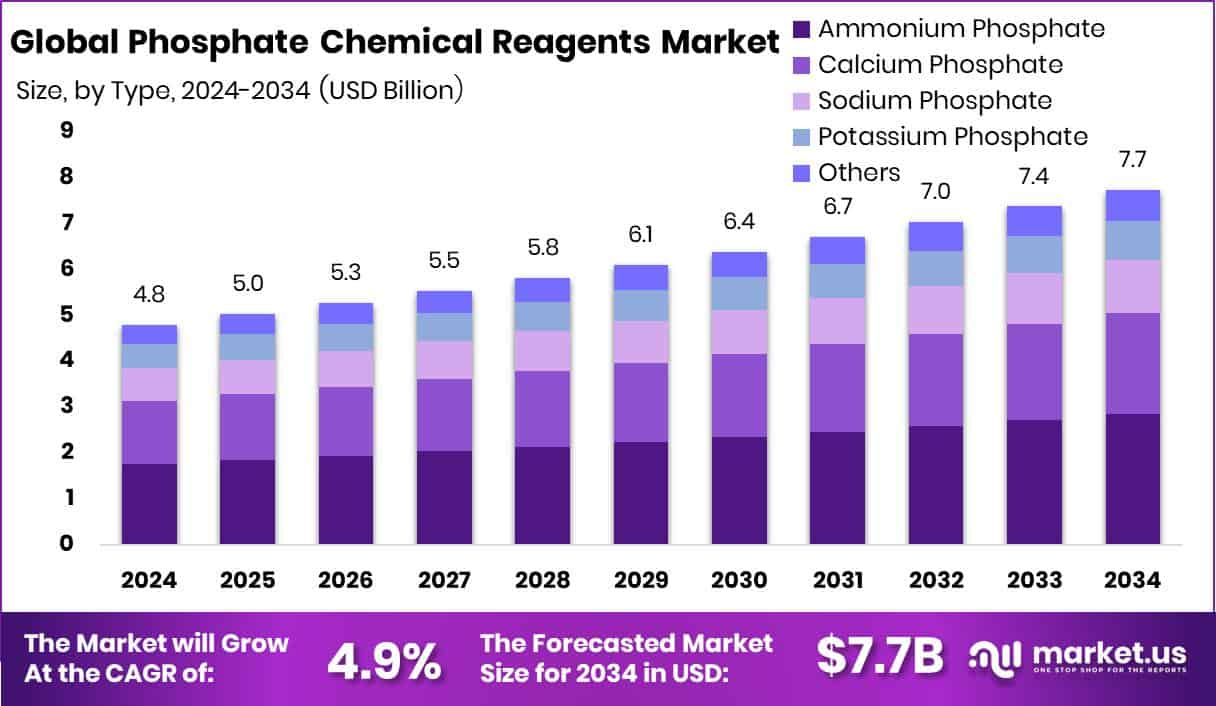

The Global Phosphate Chemical Reagents Market is expected to be worth around USD 7.7 billion by 2034, up from USD 4.8 billion in 2024, and is projected to grow at a CAGR of 4.9% from 2025 to 2034. Strong industrial and agricultural demand supported the Asia Pacific 42.9% growth.

Phosphate chemical reagents are chemical compounds derived from phosphoric acid and phosphate minerals, widely used in industrial, agricultural, laboratory, and food-related processes. These reagents include ammonium phosphate, calcium phosphate, sodium phosphate, potassium phosphate, and other specialized phosphate compounds. They are valued for their buffering capacity, nutrient properties, and reactivity in chemical formulations. In practical use, phosphate reagents support soil fertility, water purification, food preservation, and pharmaceutical formulations, making them essential across multiple sectors.

The Phosphate Chemical Reagents Market refers to the global trade and production ecosystem covering these compounds by type, formulation, and application. By formulation, phosphoric acid, phosphate salts, and phosphate esters serve as core intermediates across agriculture, water treatment, food and beverage, and pharmaceutical uses. Market growth is influenced by agricultural expansion and sustainability programs. Verdant Minerals securing key leases for its $700m Ammaroo Phosphate Project and China’s KMCJNC advancing a USD265 million phosphate chemical project in Egypt reflect upstream supply strengthening. Additionally, MNB is moving closer to production with $14M from a development bank signals investment momentum in phosphate processing.

Demand growth is strongly linked to agriculture and environmental management. Energy Department announcements of $25 million to extract critical minerals from wastewater, alongside ARPA-E awarding $2.7 million to Northwestern engineers for microbial wastewater resource recovery, highlight innovation in phosphorus recovery. UConn Engineering receiving $3M in federal wastewater research funding further underlines resource optimization trends. Meanwhile, agri-input investments such as Talus Renewables securing $22m for green ammonia and German funding of €30m for OCP Group’s green ammonia scheme demonstrate integration between phosphate nutrients and sustainable fertilizer production.

Opportunities are emerging through circular economy models and green chemistry integration. Wastewater mineral extraction initiatives create secondary phosphate sources, reducing reliance on virgin mining. Large-scale development financing, including MNB’s $14M support and Egypt’s USD265 million project expansion, indicates confidence in long-term supply security. As regulatory focus shifts toward sustainability, phosphate reagents are positioned to benefit from cleaner production pathways and improved nutrient recovery systems across agriculture and water infrastructure.

Key Takeaways

- The Global Phosphate Chemical Reagents Market is expected to be worth around USD 7.7 billion by 2034, up from USD 4.8 billion in 2024, and is projected to grow at a CAGR of 4.9% from 2025 to 2034.

- Ammonium Phosphate dominates the Phosphate Chemical Reagents Market with a significant 36.8% share.

- Phosphoric Acid leads the Phosphate Chemical Reagents Market formulation segment, accounting for 48.2%.

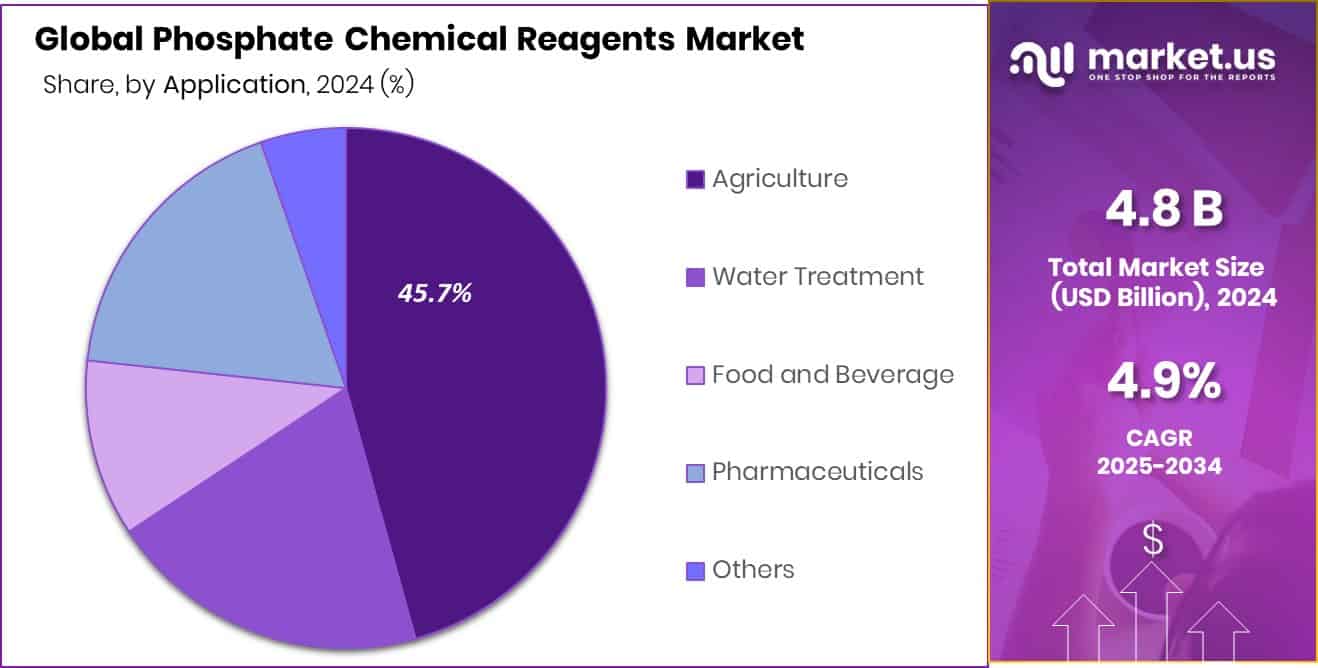

- Agriculture application commands 45.7% share in the Phosphate Chemical Reagents Market globally.

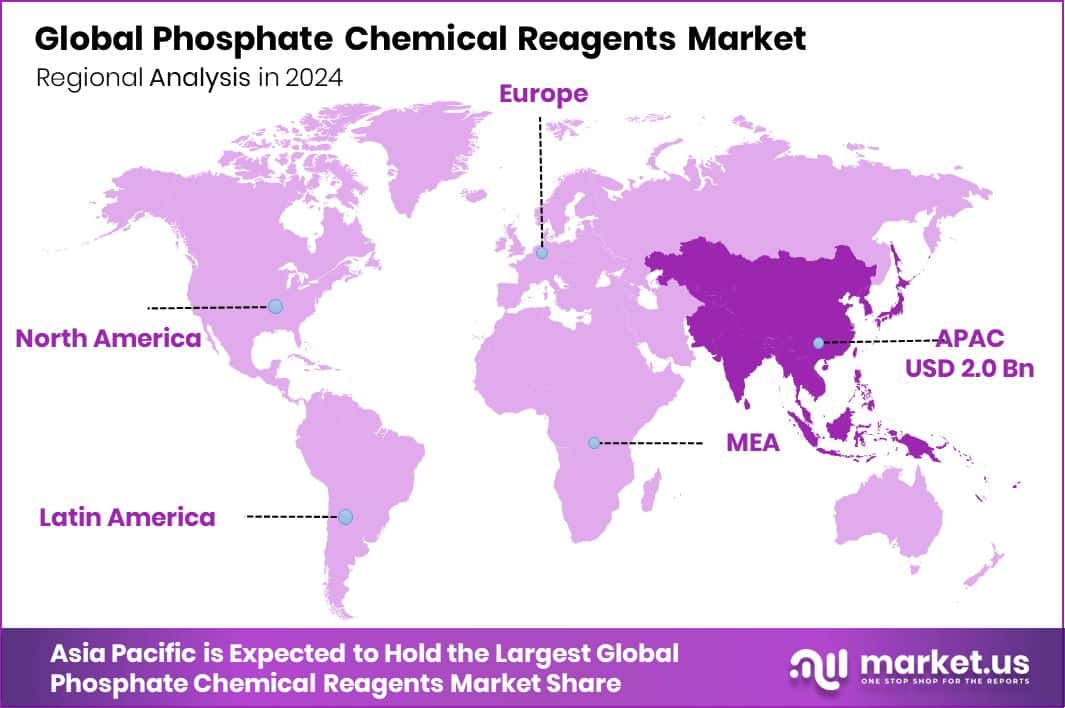

- Asia Pacific market valuation reached USD 2.0 Bn in 2024.

By Type Analysis

Ammonium Phosphate dominates Phosphate Chemical Reagents Market with 36.8% share.

In 2024, the Phosphate Chemical Reagents Market showed strong momentum under the Ammonium Phosphate segment, which accounted for 36.8% of the overall market share. This dominance reflects the compound’s broad utility across fertilizers, flame retardants, food processing additives, and water treatment formulations. Ammonium phosphate reagents are widely preferred due to their high solubility, stable composition, and efficient phosphorus delivery properties.

Industrial users value their consistent performance in laboratory and production-scale chemical reactions. Growing agricultural intensification, combined with expanding industrial manufacturing in emerging economies, has further strengthened demand. Manufacturers are also optimizing production efficiency to manage raw material costs while ensuring supply stability. The segment’s substantial share highlights its critical role in both commercial-scale production and specialty chemical applications worldwide.

By Formulation Type Analysis

Phosphoric Acid leads the formulation segment in Phosphate Chemical Reagents Market.

In 2024, the Phosphate Chemical Reagents Market by formulation type was led by Phosphoric Acid, capturing 48.2% of the total revenue share. Phosphoric acid remains a foundational intermediate in the production of various phosphate-based compounds, including salts and specialty reagents. Its versatility across fertilizer production, food-grade applications, metal surface treatment, and water purification processes has supported its leading position. Industrial operators rely on phosphoric acid for its consistent reactivity and adaptability in formulation development.

Demand growth has also been supported by infrastructure expansion and the increased need for corrosion control chemicals. With ongoing advancements in purification technologies and efficiency improvements in wet-process production, phosphoric acid continues to maintain its competitive edge as the most widely used formulation base in the global market.

By Application Analysis

Agriculture application accounts for 45.7% in the Phosphate Chemical Reagents Market.

In 2024, Agriculture emerged as the leading application segment in the Phosphate Chemical Reagents Market, holding 45.7% of the total market share. Rising global food demand, shrinking arable land per capita, and the push for higher crop yields have significantly increased the use of phosphate-based reagents in fertilizers and soil treatment solutions. Farmers depend on phosphate inputs to enhance root development, improve nutrient absorption, and strengthen crop resilience.

Government-backed agricultural productivity programs in developing economies have further accelerated consumption. In addition, the adoption of precision farming techniques is encouraging more targeted nutrient management, supporting steady demand growth. The strong share of agriculture underscores the essential role phosphate chemical reagents play in sustaining global food security and improving overall farm output efficiency.

Key Market Segments

By Type

- Ammonium Phosphate

- Calcium Phosphate

- Sodium Phosphate

- Potassium Phosphate

- Others

By Formulation Type

- Phosphoric Acid

- Phosphate Salts

- Phosphate Esters and Organic Phosphates

By Application

- Agriculture

- Water Treatment

- Food and Beverage

- Pharmaceuticals

- Others

Driving Factors

Rising global agricultural fertilizer consumption

Rising global agricultural fertilizer consumption continues to be a primary driver of the Phosphate Chemical Reagents Market. Growing food demand, soil nutrient depletion, and the need to enhance crop productivity are increasing reliance on phosphate-based fertilizers and associated reagents. Countries investing in agricultural modernization are strengthening nutrient management practices, which directly support demand for ammonium and other phosphate compounds.

At the same time, environmental research is reinforcing the importance of nutrient recovery and efficient phosphate utilization. UConn Engineering being selected to receive $3M in federal funding for wastewater research reflects ba roader institutional focus on phosphorus management and water sustainability. Such research initiatives indirectly support reagent demand by advancing treatment technologies that rely on phosphate chemistry in agricultural runoff control and nutrient recycling systems.

Restraining Factors

Volatile phosphate rock price fluctuations

Volatile phosphate rock price fluctuations remain a significant restraint for the Phosphate Chemical Reagents Market. Since phosphate rock is the core raw material for producing phosphoric acid and related salts, pricing instability can directly impact production costs and margins. Supply chain disruptions, geopolitical developments, and resource concentration contribute to price unpredictability. Additionally, alternative extraction and waste-to-value technologies are gradually influencing traditional mining economics.

Rainbow Rare Earths targeting 75% EBITDA margins with waste-to-value technology, supported by a $50M commitment from the US government, highlights increasing interest in alternative resource models. While such innovation strengthens long-term sustainability, it may pressure conventional phosphate producers by shifting cost structures and competitive dynamics within the broader mineral extraction landscape.

Growth Opportunity

Phosphorus recovery from industrial wastewater

Phosphorus recovery from industrial wastewater represents a promising growth opportunity in the Phosphate Chemical Reagents Market. Industries are increasingly adopting circular economy principles, focusing on nutrient recycling rather than disposal. Wastewater treatment plants are becoming resource recovery hubs, extracting usable phosphate compounds for reuse in agriculture and industrial processes. This transition supports both environmental protection and long-term raw material security.

International collaborations further reinforce this direction. Oman and China setting up a $200m clean energy fund reflects growing cross-border investment in sustainable resource and energy solutions, indirectly supporting the cleaner production of chemical inputs. Such funding initiatives encourage innovation in recovery technologies and green processing methods, creating new pathways for phosphate reagent demand beyond traditional mining-based supply chains.

Latest Trends

Green ammonia integrated phosphate production

Green ammonia integrated phosphate production is emerging as a notable trend shaping the Phosphate Chemical Reagents Market. As fertilizer manufacturing seeks to reduce carbon intensity, producers are aligning phosphate processing with low-emission ammonia production systems. This integration improves energy efficiency and supports sustainable agriculture goals. Financial performance in the sector also indicates resilience and operational strength.

Chemical group Duc Giang posting $201 million profit in nine months signals stable demand and improved production efficiencies within phosphate-linked chemical operations. Companies are increasingly investing in cleaner technologies, optimized processing routes, and value-added downstream applications. These developments reflect a broader shift toward environmentally responsible manufacturing while maintaining profitability and supporting long-term market stability.

Regional Analysis

Asia Pacific dominated Phosphate Chemical Reagents Market with 42.9% share.

The Phosphate Chemical Reagents Market demonstrates varied regional performance across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, reflecting differences in industrial maturity and agricultural intensity. Asia Pacific emerged as the dominating region, accounting for 42.9% of the global market and reaching a valuation of USD 2.0 Bn. The region’s leadership is supported by its large-scale agricultural production, expanding chemical manufacturing base, and strong demand for phosphate derivatives across fertilizers and industrial processing.

North America maintains a stable position driven by established agrochemical consumption and consistent industrial reagent usage. Europe shows steady demand supported by regulated agricultural practices and advanced chemical processing standards.

Meanwhile, the Middle East & Africa region benefits from fertilizer consumption linked to improving crop productivity, while Latin America demonstrates sustained uptake due to its strong agricultural export base. Overall, Asia Pacific’s 42.9% share and USD 2.0 Bn valuation clearly position it as the leading regional contributor to market revenue.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, AAT Bioquest, Inc. continues to position itself as a specialized provider of advanced assay reagents and biochemical solutions, including phosphate-related chemical reagents used in life science research. From an analyst’s perspective, the company benefits from its focused portfolio tailored to laboratories, research institutions, and biotechnology companies. Its strength lies in product customization, consistent quality standards, and the ability to serve niche experimental applications where precision is critical. By emphasizing research-driven innovation and technical support, AAT Bioquest sustains a competitive edge in specialty reagent supply. Its role in the global Phosphate Chemical Reagents Market remains closely tied to high-value research applications rather than bulk industrial volumes.

Biosystems S.A. operates with a strong presence in diagnostic reagents and analytical solutions, where phosphate-based chemicals are commonly integrated into testing kits and laboratory formulations. The company’s structured manufacturing capabilities and emphasis on standardized diagnostic performance provide stability within regulated markets. Analysts observe that Biosystems S.A. leverages its expertise in clinical and laboratory chemistry to maintain steady demand for phosphate reagents used in biochemical testing environments. Its growth outlook is supported by ongoing demand for laboratory automation and reliable reagent formulations, strengthening its positioning in application-specific phosphate chemical segments.

Cayman Chemical maintains a recognized footprint in the supply of biochemical research reagents, including phosphate compounds used in molecular biology and pharmaceutical research. The company is known for its catalog depth and commitment to supplying high-purity chemicals for experimental and analytical use. From a market standpoint, Cayman Chemical benefits from strong relationships with academic and pharmaceutical research communities. Its phosphate chemical offerings are primarily aligned with research-scale applications, where quality, traceability, and technical documentation are essential. This focused operational model allows Cayman Chemical to sustain relevance within specialized segments of the global Phosphate Chemical Reagents Market in 2024.

Top Key Players in the Market

- AAT Bioquest, Inc.

- Biosystems S.A.

- Cayman Chemical

- Geno Technology Inc.

- HiMedia Laboratories

- Honeywell International Inc.

- ICL

- KYORITSU CHEMICAL CHECK Lab. Corp

- Tintometer GmbH

Recent Developments

- In July 2025, HiMedia Laboratories received validation from the Indian Council of Medical Research – National Institute of Virology (ICMR-NIV) for their Hi-PCR® Monkeypox Virus Multiplex Probe PCR Kit. This recognises the company’s advanced reagent development and quality standards in molecular diagnostics.

- In 2024, AAT Bioquest published its AssayWise Letters, Vol. 13(1) newsletter, highlighting advances such as efficient nucleic acid labeling with Helixyte™ iFluor® dyes—a development useful in research applications.

Report Scope

Report Features Description Market Value (2024) USD 4.8 Billion Forecast Revenue (2034) USD 7.7 Billion CAGR (2025-2034) 4.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Ammonium Phosphate, Calcium Phosphate, Sodium Phosphate, Potassium Phosphate, Others), By Formulation Type (Phosphoric Acid, Phosphate Salts, Phosphate Esters and Organic Phosphates), By Application (Agriculture, Water Treatment, Food and Beverage, Pharmaceuticals, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape AAT Bioquest, Inc., Biosystems S.A., Cayman Chemical, Geno Technology Inc., HiMedia Laboratories, Honeywell International Inc., ICL, KYORITSU CHEMICAL CHECK Lab. Corp, Tintometer GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Phosphate Chemical Reagents MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Phosphate Chemical Reagents MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- AAT Bioquest, Inc.

- Biosystems S.A.

- Cayman Chemical

- Geno Technology Inc.

- HiMedia Laboratories

- Honeywell International Inc.

- ICL

- KYORITSU CHEMICAL CHECK Lab. Corp

- Tintometer GmbH

Our Clients

- 178066

- February 2026