Global Panthenol Market By Product (D-Panthenol and DL-Panthenol), By Form (Liquid and Powder), By Application (Cosmetics And Personal Care, Pharmaceuticals, Nutraceuticals & Food Supplements, Animal Nutrition, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 180327

- Number of Pages: 279

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

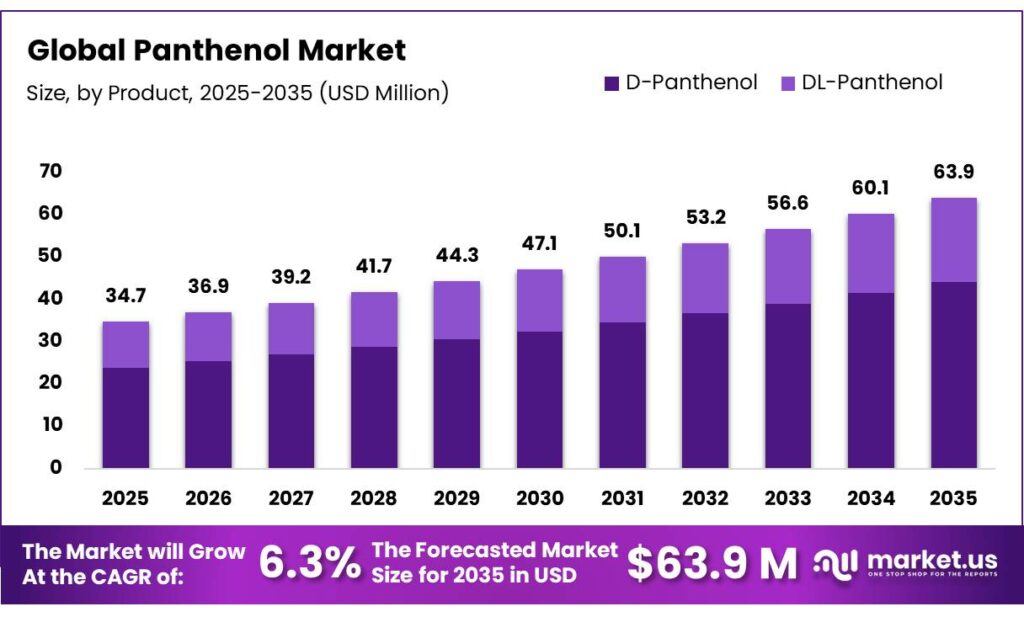

The Global Panthenol Market is expected to be worth around USD 63.9 Million by 2035, up from USD 34.7 Million in 2025, at a CAGR of 6.3% from 2026 to 2035. The Asia Pacific segment maintained 38.9%, supporting a Panthenol value of USD 89.6 Mn.

Panthenol, known as provitamin B5, is an alcohol analog of vitamin B5 derived from pantothenic acid. It appears as either a viscous, transparent oil (D-panthenol) or a white crystalline powder (DL-panthenol). The market is primarily driven by its widespread use in the cosmetics and personal care industries, where it is valued for its moisturizing, soothing, and skin barrier-enhancing properties.

The ingredient is predominantly used in skin and hair care products, such as shampoos, conditioners, lotions, and anti-aging formulations, due to its proven effectiveness and regulatory safety approval from authorities such as the U.S. FDA and European Medicines Agency (EMA). It is generally well-tolerated by all skin types, including sensitive skin and children’s skin. While uncommon, some individuals may experience an allergic reaction, such as contact dermatitis, which can cause redness or minor irritation.

While panthenol finds application in pharmaceuticals, nutraceuticals, and animal nutrition, its most significant demand comes from the personal care sector. The preference for liquid panthenol over powder forms, its superior bioavailability, and compatibility with various formulations further bolster its adoption. The Asia Pacific region remains the largest market, driven by increasing consumer demand for beauty and wellness products.

Key Takeaways:

- The global panthenol market was valued at USD 34.7 million in 2025.

- The global panthenol market is projected to grow at a CAGR of 7.0% and is estimated to reach USD 63.9 million by 2035.

- On the basis of product type, D-panthenol dominated the market, constituting 68.9% of the total market share.

- Based on the forms of the panthenol, liquid panthenol led the market, comprising 57.9% of the total market.

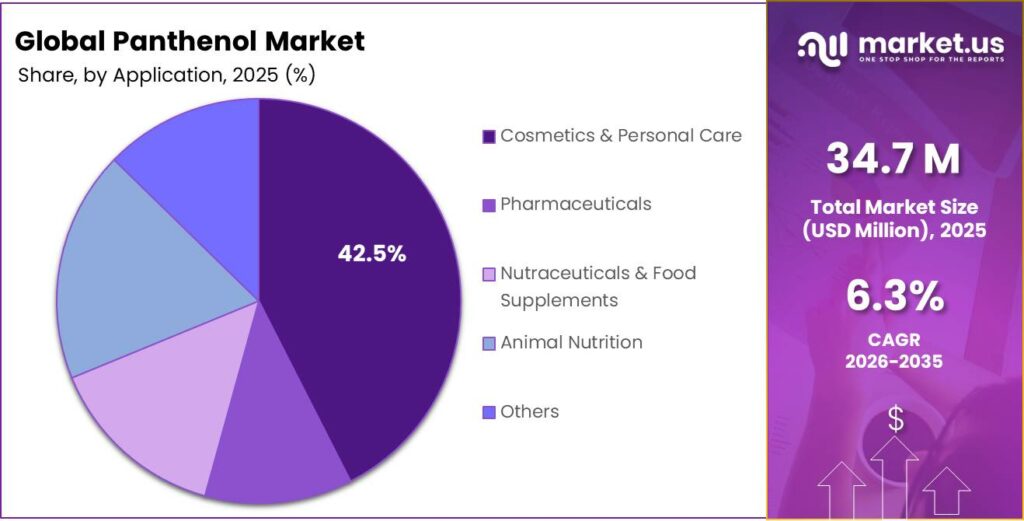

- Among the applications of the panthenol, the cosmetics & personal care industry is the most considerable end-use of the product, accounting for around 42.5% of the revenue.

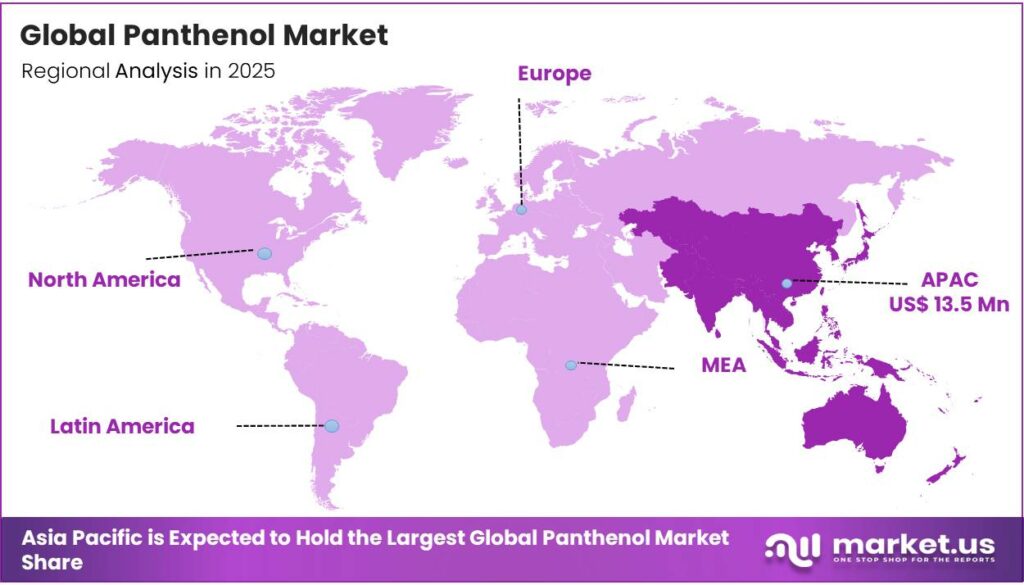

- In 2025, the Asia Pacific was the most dominant region in the panthenol market, accounting for 38.9% of the total global consumption.

Product Analysis

D-Panthenol is a Prominent Segment in the Market.

The market is segmented based on the product type into D-panthenol and DL-panthenol. The D-panthenol led the market, comprising 68.9% of the market share, primarily due to its superior stability and bioavailability. D-panthenol, the natural isomer, is more easily absorbed by the skin and hair, providing more effective hydration and nourishment. Its well-established efficacy in enhancing skin barrier function and promoting hair health makes it the preferred choice in cosmetic and personal care formulations.

In contrast, DL-panthenol, a synthetic mixture of both D- and L-isomers, is less commonly used as it is less bioavailable and can be less effective in achieving the desired cosmetic benefits. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) recognize D-panthenol as the standard for safe use, further driving its widespread adoption in skincare and haircare products.

Forms Analysis

Liquid Panthenol Dominated the Market.

On the basis of forms, the panthenol market is segmented into liquid and powder. The liquid panthenol dominated the market, comprising 57.9% of the market share, due to its easier incorporation and better formulation compatibility in cosmetic and personal care products. The liquid form dissolves quickly and uniformly in formulations, making it ideal for use in aqueous solutions such as lotions, creams, shampoos, and conditioners. This ease of blending enhances the stability and effectiveness of the final product.

In contrast, powder panthenol requires additional processing, such as dissolution in a solvent, which can complicate manufacturing. Additionally, liquid panthenol is more versatile in adjusting concentration levels, offering greater flexibility for manufacturers. Moreover, its ease of handling, combined with faster absorption by the skin and hair, further contributes to its popularity in both cosmetic and pharmaceutical applications.

Application Analysis

Panthenol is Mostly Utilized in Cosmetics & Personal Care Industry.

Among the applications of the panthenol, 42.5% of the total global consumption of panthenols is in the cosmetics & personal care industry, outperforming industries, such as pharmaceuticals, nutraceuticals & food supplements, animal nutrition, and others. Panthenol is used in the cosmetics and personal care industry due to its benefits for skin and hair health, which align with growing consumer demand for beauty and self-care products.

Additionally, its proven ability to hydrate, soothe, and promote healing makes it a key ingredient in moisturizers, shampoos, conditioners, and anti-aging formulations. While panthenol is used in pharmaceuticals, nutraceuticals, and animal nutrition, its application in these fields is less widespread, as its benefits are more pronounced in topical uses, and other ingredients often serve as more targeted solutions for those industries. The personal care sector’s broad consumer base and high product turnover drive the majority of panthenol’s demand.

Key Market Segments:

By Product

- D-Panthenol

- DL-Panthenol

By Form

- Liquid

- Powder

By Application

- Cosmetics & Personal Care

- Pharmaceuticals

- Nutraceuticals & Food Supplements

- Animal Nutrition

- Others

Drivers

Cosmetics & Personal Care Industry Demand Drives the Panthenol Market.

The cosmetics and personal care industry remains a primary driver for the panthenol market, underpinned by its functional role as a provitamin B5 humectant and emollient. According to research published in PMC, approximately 90% of individuals use some form of personal care product daily, creating a massive baseline for ingredient demand. It is significantly utilized in skin, hair, and nail care products.

Panthenol is favored for its moisturizing, healing, and anti-inflammatory properties, which contribute to its inclusion in formulations for products such as shampoos, conditioners, moisturizers, and wound healing ointments. The U.S. Food and Drug Administration (FDA) classifies it as a safe ingredient, promoting its continued use in personal care formulations.

Furthermore, the European Medicines Agency (EMA) acknowledges its efficacy in improving skin barrier function and its suitability for sensitive skin, further encouraging its adoption in skincare products. Panthenol’s popularity in the formulation of dermatological treatments and anti-aging products aligns with growing consumer interest in multifunctional, skin-beneficial ingredients.

Moreover, the industry is increasingly adopting hybrid beauty products that combine color cosmetics with skincare benefits, such as hydration and anti-aging. This expands panthenol’s utility beyond traditional lotions into products such as mascaras and foundations.

Restraints

Competition from Alternatives Might Hamper the Demand for the Panthenol.

The panthenol market faces increasing competition from functional alternatives, primarily driven by evolving consumer preferences for high-potency humectants and plant-derived ingredients. While panthenol remains a staple provitamin B5 source, specialized alternatives challenge its market share in targeted applications. Alternative ingredients such as sodium hyaluronate, hyaluronic acid, glycerin, and aloe vera offer similar moisturizing and skin-soothing benefits, which can reduce demand for panthenol in certain formulations.

According to National Institutes of Health (NIH) publications, hyaluronic acid can bind up to 1,000 times its weight in water, often positioning it as a premium hydration alternative to panthenol’s 1-5% standard formulations. Similarly, while panthenol offers unique wound-healing properties, ingredients such as niacinamide (Vitamin B3) provide overlapping benefits in barrier repair and anti-inflammation, leading to formulation substitutions in multi-functional serums.

Additionally, market trends show increased consumer preference for natural ingredients, which has prompted some manufacturers to explore plant-based alternatives, offering cleaner labels. This shift is underscored by government-regulated safety assessments, such as the Cosmetic Ingredient Review (CIR), monitoring a growing list of botanical alternatives such as squalane and glycerin, which often meet the demand for clean beauty, as 43% of consumers prefer natural skincare.

Moreover, in 2024, Codif TN, a French company, launched Pantodium Cica, an organic, fermented seaweed extract designed to act as a natural and organic alternative to synthetic D-Panthenol. Such regulatory and consumer-driven changes create a competitive environment that challenges the dominance of panthenol.

Opportunity

Application in Animal Nutrition Creates Opportunities in the Panthenol Market.

The application of panthenol (D-panthenol) in animal nutrition represents a significant market opportunity, primarily as a nutritional feed additive for a wide range of species in improving the health and growth of livestock. The European Food Safety Authority (EFSA) has recognized panthenol as a nutritional feed additive with beneficial effects on animal health, including enhancing skin and mucosal integrity in animals. The chemical promotes faster recovery from stress and injury in poultry and swine.

Additionally, panthenol has been used to improve the growth rate and feed efficiency in animals, particularly in monogastric species. Standard dietary recommendations for pantothenic acid range from 8-20 mg/kg for pigs, 10-15 mg/kg for poultry, 30-50 mg/kg for fish, and 8-14 mg/kg feed for pets. D-panthenol is considered a pro-vitamin essentially bioequivalent to pantothenic acid when administered via feed or drinking water, offering superior stability in acidic environments (pH 3 to 5).

Furthermore, clinical studies in geese demonstrate that optimal supplemental levels of 15.50 mg/kg significantly affect growth and slaughter performance, while higher concentrations correlate with significantly higher antioxidant capacity. As global demand for high-quality animal products grows, regulatory bodies’ increasing approval of panthenol as a feed ingredient indicates a significant opportunity for its expanded use in the sector.

Trends

Adoption in Nutraceuticals and Nutricosmetics.

The integration of panthenol into the nutraceutical and nutricosmetic sectors is driven by the beauty-from-within trend, where oral supplements are used to enhance skin, hair, and nail health. The panthenol serves as a bioavailable precursor to pantothenic acid, essential for fatty acid synthesis and tissue repair.

The U.S. Food and Drug Administration (FDA) has recognized panthenol as a safe ingredient in oral supplements, supporting its inclusion in functional foods and beverages aimed at improving skin elasticity, hydration, and overall health. Similarly, the European Commission’s Regulation on Food Additives (EC No 1333/2008) permits panthenol in various nutraceutical formulations, including those targeting skin aging and hair loss.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Severe Disruptions of the Supply Chains of Panthenol.

Geopolitical tensions exert a multifaceted impact on the panthenol market, primarily through supply chain disruptions and escalated production costs for chemical precursors. As an alcohol derivative of provitamin B5, panthenol production is highly dependent on global energy and petrochemical markets. The U.S.-China trade tensions have led to increased tariffs on chemical imports, including raw materials used in Panthenol production. This has raised costs for manufacturers in the U.S. and other affected regions, potentially influencing production and pricing decisions.

Similarly, the Russia-Ukraine conflict led to persistent inflationary pressure, with global inflation increasing by approximately 2% in 2022 and 1% in 2023. High energy prices in Europe have directly impacted the operational costs of panthenol synthesis, which is energy-intensive.

These geopolitical tensions create an uncertain operating environment, pressuring manufacturers to explore alternative sourcing strategies and increase resilience in their supply chains. The market trend is shifting toward near-shoring and strategic stockpiling as firms navigate these systemic uncertainties to ensure ingredient availability for the personal care and animal nutrition sectors.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Panthenol Market.

In 2025, the Asia Pacific dominated the global panthenol market, holding about 38.9% of the total global consumption, driven by the growing demand for personal care, cosmetics, and nutraceutical products. The region’s increasing middle-class population and rising disposable incomes have fueled the consumption of skin and hair care products containing panthenol. Additionally, panthenol’s popularity in Asia is particularly linked to its effectiveness in skincare products, with countries such as Japan, South Korea, and China leading in innovation.

Furthermore, public bodies such as the ASEAN Cosmetics Association have fostered standardization, promoting panthenol’s use across diverse product categories, further solidifying the Asia Pacific’s position as the dominant market for this ingredient. Furthermore, the region’s massive livestock sector, which requires substantial volumes of D-panthenol as a feed additive for growth optimization in swine and poultry, is a significant contributor.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of panthenol focus on several strategic activities, including continuous investment in research and development (R&D) to improve product formulations and address emerging consumer needs, such as clean label and sustainable ingredients. Companies prioritize regulatory compliance, ensuring their products meet safety standards set by bodies such as the European Medicines Agency (EMA) and the U.S. FDA, facilitating smoother market access.

Strengthening supply chain resilience is another focus, as manufacturers aim to mitigate raw material supply risks by diversifying sourcing and production locations. Additionally, strategic partnerships with key players in the cosmetics, pharmaceutical, and nutraceutical industries allow manufacturers to expand their distribution networks.

The Major Players in The Industry

- DSM-Firmenich

- Yifan Pharmaceutical Co., Ltd.

- Xinfa Pharmaceutical Co., Ltd

- Evonik Industries AG

- Croma-Pharma GmbH

- BASF SE

- TRI-K Industries, Inc.

- Jiangxi Tongde Chemical Technology Co., Ltd.

- RITA Corporation

- Ildong Pharmaceutical

- Other Key Players

Key Development

- In July 2023, Ildong Pharmaceutical announced the launch of panthenol care ointment, an over-the-counter medication with dexpanthenol, designed for the adjunctive treatment of dermatitis.

- In August 2025, Galderma, a leader in the dermatology sector, introduced the Cetaphil nourishing oil to foam cleanser, a formula crafted to provide deep cleansing while maintaining hydration and helping to protect the moisture barrier of sensitive skin.

Report Scope

Report Features Description Market Value (2025) US$34.7 Mn Forecast Revenue (2035) US$63.9 Mn CAGR (2025-2035) 6.3% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (D-Panthenol and DL-Panthenol), By Form (Liquid and Powder), By Application (Cosmetics & Personal Care, Pharmaceuticals, Nutraceuticals & Food Supplements, Animal Nutrition, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape DSM-Firmenich, Yifan Pharmaceutical Co., Ltd., Xinfa Pharmaceutical Co., Ltd., Evonik Industries AG, Croma-Pharma GmbH, BASF SE, TRI-K Industries, Inc., Jiangxi Tongde Chemical Technology Co., Ltd., RITA Corporation, Ildong Pharmaceutical, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- DSM-Firmenich

- Yifan Pharmaceutical Co., Ltd.

- Xinfa Pharmaceutical Co., Ltd

- Evonik Industries AG

- Croma-Pharma GmbH

- BASF SE

- TRI-K Industries, Inc.

- Jiangxi Tongde Chemical Technology Co., Ltd.

- RITA Corporation

- Ildong Pharmaceutical

- Other Key Players

Our Clients

- 180327

- Mar 2026