Global Orthopedic Splints Market By Product Type (Fibreglass splints, Plaster splints, Thermoplastic/composite splints, Splinting tools & accessories, Others) By Anatomical Location (Lower extremity, Upper extremity) By Type (Rigid/static splints, Dynamic/functional splints) By Application (Immobilization, Rehabilitation, Support, Prophylactic/preventive use) By End-User (Hospitals, Specialty Centers, Orthopedic clinics, Others) Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Nov 2025

- Report ID: 164569

- Number of Pages: 285

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

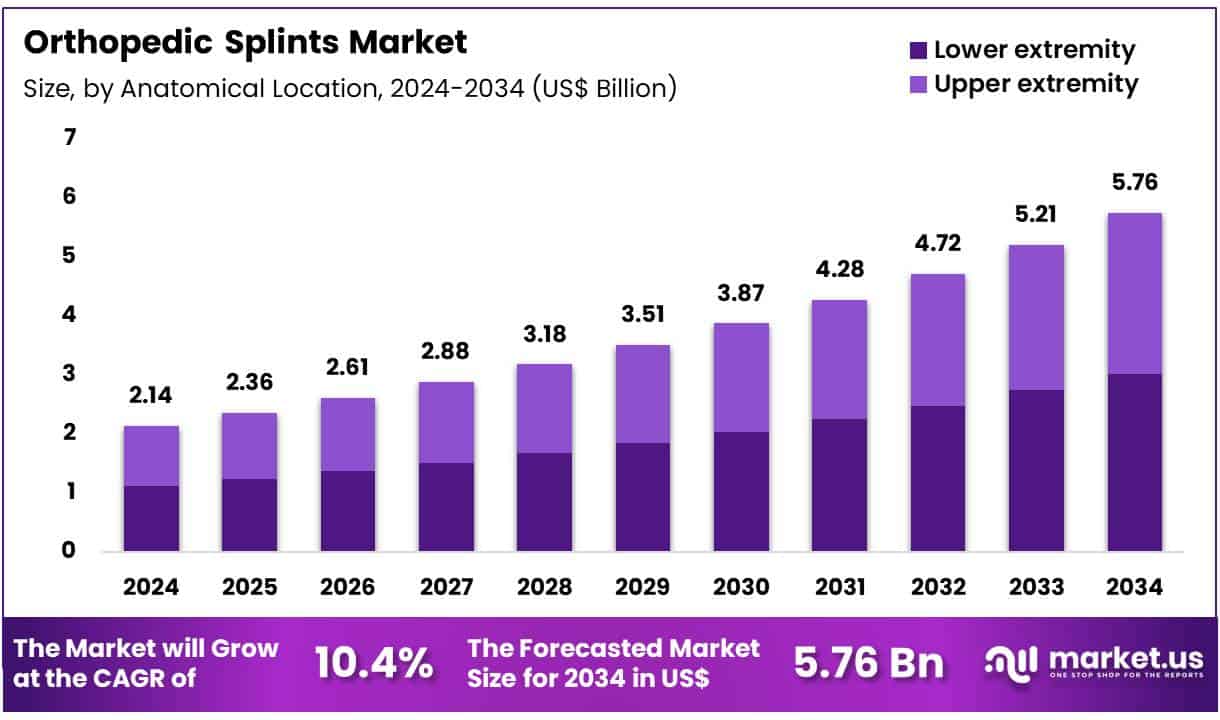

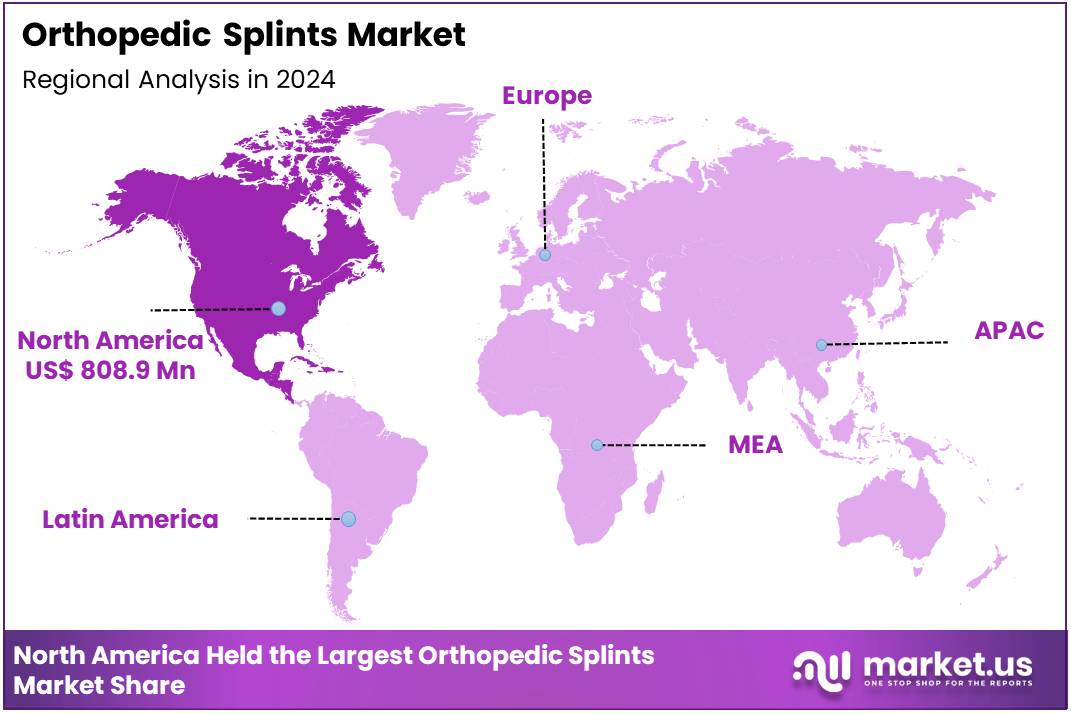

Global Orthopedic Splints Market size is expected to be worth around US$ 5.76 Billion by 2034 from US$ 2.14 Billion in 2024, growing at a CAGR of 10.4% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 37.8% share with a revenue of US$ 808.9 Million.

Growth in the orthopedic splints sector is being supported by the rising burden of musculoskeletal disorders worldwide. According to the World Health Organization, around 1.71 billion people are affected by musculoskeletal conditions. These conditions are a leading cause of disability and often limit mobility, which raises the day-to-day need for immobilization and support devices. As a result, consistent demand for orthopedic splints is being observed across acute care units, emergency departments, and outpatient rehabilitation centers.

The rise in osteoarthritis further strengthens market expansion. WHO data indicate that 528 million people were living with osteoarthritis in 2019. Many patients require rehabilitation to ease pain, improve movement, and protect joints. Orthopedic splints are widely used as part of conservative management, particularly for the knee, hand, and hip. Their use in routine rehabilitation pathways continues to reinforce product consumption in primary care and therapy settings.

Demographic trends add structural support. United Nations projections show that the global population aged 65 years and over will increase from 10 percent in 2022 to 16 percent by 2050. This age group experiences higher rates of fractures, osteoarthritis, and degenerative joint conditions. As these clinical issues grow, the volume of splint prescriptions is expected to increase steadily.

Rehabilitation needs are also expanding. WHO estimates that 2.4 billion people worldwide live with conditions that could benefit from rehabilitation. Musculoskeletal disorders represent the largest share of this need. Splints play a vital role by stabilizing joints and supporting safe movement during recovery. The scale-up of rehabilitation services thus contributes directly to rising splint usage.

Trauma and road injuries remain major contributors. WHO reports about 1.19 million deaths every year from road traffic crashes, along with tens of millions of non-fatal injuries that often require temporary immobilization. This situation maintains strong and recurring demand for splints in emergency and early postoperative care.

Global prioritization of assistive technology adds further momentum. WHO projects that up to 3.5 billion people may require assistive products by 2050. Orthoses and splints are included in this category, and expanded access policies are expected to strengthen procurement. Additionally, widespread osteoporosis and low bone mass in adults over 50 years increase fracture risk, reinforcing the clinical need for temporary splinting solutions.

Key Takeaways

- Market Size: Global Orthopedic Splints Market size is expected to be worth around US$ 5.76 Billion by 2034 from US$ 2.14 Billion in 2024.

- Market Growth: The market growing at a CAGR of 10.4% during the forecast period from 2025 to 2034.

- Product Type Analysis: Fibreglass splints are observed to dominate the market, accounting for an estimated 38.2% share in 2024.

- Anatomical Location Analysis: The lower extremity splints are estimated to hold a dominant share of 52.5% in 2024.

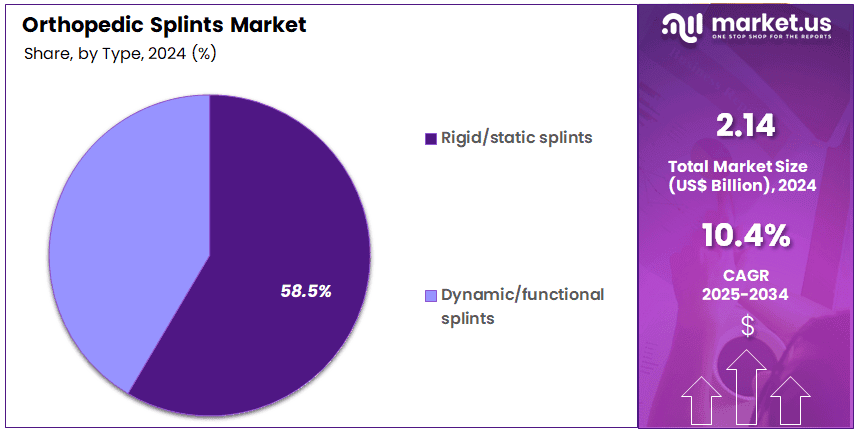

- Type Analysis: The dominance of rigid or static splints has been observed, with this segment estimated to account for 58.8% of the total market share in 2024.

- Application Analysis: The immobilization segment is estimated to dominate the market with 42.1% of the total share in 2024.

- End-Use Analysis: Hospitals accounted for 40.5% of the global market share in 2024.

- Regional Analysis: In 2024, North America led the market, achieving over 37.8% share with a revenue of US$ 808.9 Million.

Product Type Analysis

The orthopedic splints market has been segmented based on product type, and a perse portfolio of materials and accessories has been adopted to support various clinical requirements. Fibreglass splints are observed to dominate the market, accounting for an estimated 38.2% share in 2024. Their growth has been supported by characteristics such as lightweight structure, enhanced durability, and higher patient comfort.

Adoption has also been driven by improved radiolucency, which enables more accurate imaging during treatment follow-up. Plaster splints continue to hold a stable share, as their cost-effectiveness and molding flexibility remain valued in resource-limited settings. Thermoplastic and composite splints are being increasingly utilized due to their heat-activated customizability and reusability.

Splinting tools and accessories contribute to procedural efficiency and standardization in both emergency and orthopedic care environments. Other emerging splint types are gradually gaining attention as technological improvements support advanced immobilization and rehabilitation outcomes.

Anatomical Location Analysis

By anatomical application, and lower extremity splints are estimated to hold a dominant share of 52.5% in 2024. This segment includes hip, knee, ankle, and foot immobilization products, and its strong position has been supported by the high incidence of sports injuries, trauma cases, and age-related degenerative conditions affecting the lower limbs.

The demand for stable fixation and controlled movement has further contributed to the wider adoption of specialized splints in this category. Upper extremity splints, covering applications for the elbow, hand and wrist, shoulder, and neck, continue to represent a significant portion of total usage.

Their utilization has been influenced by occupational injuries, repetitive strain disorders, and post-operative rehabilitation needs. Although the upper extremity segment is expanding steadily, its growth pace remains comparatively moderate, while lower extremity splints retain their leading role due to higher clinical frequency and treatment complexity.

Type Analysis

By type segmented into rigid or static splints and dynamic or functional splints. The dominance of rigid or static splints has been observed, with this segment estimated to account for 58.8% of the total market share in 2024.

The strong position of this category can be attributed to its widespread use in fracture management, post-operative stabilization, and acute injury care, where immobilization is required to support bone healing and prevent further tissue damage. High utilization across hospitals and trauma centers has further reinforced its leading share.

Dynamic or functional splints represent the second major segment. Steady adoption has been supported by rising demand for controlled mobility solutions that facilitate rehabilitation while maintaining joint alignment. These splints are increasingly used in orthopedic therapy settings, especially for ligament injuries and post-surgical recovery, although their overall market share remains significantly lower compared with rigid or static splints.

Application Analysis

The orthopedic splints market has been segmented by application into immobilization, rehabilitation, support, and prophylactic or preventive use. The immobilization segment is estimated to dominate the market with 42.1% of the total share in 2024.

Its leading position has been supported by the extensive use of splints for stabilizing fractures, managing acute musculoskeletal injuries, and maintaining joint alignment during the early healing phase. High patient volume in emergency and trauma care settings has further contributed to the segment’s prominence.

The rehabilitation segment has been utilized primarily in post-operative recovery and therapeutic interventions, where controlled movement is required to restore function. Support applications have been adopted for routine orthopedic conditions, including sprains and joint instability, driving steady demand.

Prophylactic or preventive use has gained attention in sports medicine and occupational safety, as splints are increasingly employed to reduce injury risk. Although these categories show consistent growth, their shares remain lower than immobilization in 2024.

End-user Analysis

The end-user landscape of the orthopedic splints market is characterized by strong demand from institutional healthcare settings. Hospitals accounted for 40.5% of the global market share in 2024, and this dominance has been attributed to the high volume of trauma cases, orthopedic surgeries, and emergency care admissions managed in these facilities.

The availability of advanced treatment infrastructure and skilled orthopedic specialists has further supported the increased adoption of splinting solutions in hospital environments. Specialty centers represented a growing share of the market, driven by rising preferences for dedicated orthopedic and rehabilitation services.

Orthopedic clinics continued to contribute significantly due to the expansion of outpatient treatment and follow-up care. The “Others” category, which includes urgent care centers and long-term care facilities, showed steady uptake as awareness of fracture management solutions increased. Overall, sustained growth across all end-user segments is anticipated.

Key Market Segments

By Product Type

- Fibreglass splints

- Plaster splints

- Thermoplastic/composite splints

- Splinting tools & accessories

- Others

By Anatomical Location

- Lower extremity

- Hip

- Knee

- Ankle & Foot

- Upper extremity

- Elbow

- Hand & Wrist

- Shoulder

- Neck

By Type

- Rigid/static splints

- Dynamic/functional splints

By Application

- Immobilization

- Rehabilitation

- Support

- Prophylactic/preventive use

By End-User

- Hospitals

- Specialty Centers

- Orthopedic clinics

- Others

Driving Factors

The growth of the orthopedic splints market can be attributed to the rising global incidence of fractures and musculoskeletal disorders. According to the World Health Organization (WHO), musculoskeletal conditions affect over 1.7 billion people, while global fracture cases reached approximately 178 million in 2019. These conditions require immobilization and stabilization, which increases the adoption of splints in emergency and rehabilitative care.

The prevalence of osteoporosis, a major contributor to fragility fractures, is increasing with aging populations, as reported by the International Osteoporosis Foundation and the U.S. Centers for Disease Control and Prevention (CDC). As healthcare systems emphasize non-surgical and early-intervention orthopedic care, the demand for splints is expected to expand steadily.

Trending Factors

A key trend observed in the orthopedic splints market is the adoption of advanced, patient-centric materials and customized designs. Healthcare institutions are shifting from traditional plaster-based immobilization toward lightweight thermoplastics, breathable materials and adjustable support systems, which improve patient comfort and compliance. Research from the U.S. National Institutes of Health (NIH) highlights increased clinical interest in 3D-printed orthoses for personalized fitting and improved anatomical alignment.

The expansion of outpatient orthopedic services and the rise in sports-related injuries, as documented by CDC injury surveillance programs, further support the movement toward more ergonomic and reusable splinting solutions. These developments indicate a transition toward technology-enabled, efficient, and user-friendly immobilization devices.

Restraining Factors

Market expansion is constrained by several clinical and operational challenges. High-quality splints made from advanced composites or thermoplastic materials often involve elevated manufacturing and procurement costs, limiting access in resource-constrained healthcare systems.

In addition, guidelines from the U.S. Agency for Healthcare Research and Quality (AHRQ) outline risks associated with prolonged immobilization, such as pressure injuries, reduced circulation, and skin irritation, which may decrease clinician preference for certain splint types.

Limited reimbursement frameworks for orthopedic supports in some regions also restrain adoption, particularly where coverage is restricted to essential trauma care. Variability in training related to proper application and monitoring further affects consistent usage across facilities.

Opportunity

Significant opportunity exists in expanding access to orthopedic splints across developing regions with growing trauma burdens. The WHO estimates that road traffic injuries cause up to 50 million non-fatal injuries annually, creating substantial demand for rapid fracture stabilization.

Home-based rehabilitation and community-level orthopedic care represent emerging areas, supported by government initiatives promoting decentralized healthcare delivery. Advances in digital scanning, additive manufacturing and tele-rehabilitation present additional opportunity for personalized, quick-fit splints aligned with modern care pathways.

Geriatric populations, which experience higher rates of fall-related injuries according to CDC data, offer further potential for growth in preventive and post-injury support devices. These factors collectively indicate a favorable long-term market outlook.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 37.8% share and holds US$ 808.9 million market value for the year. Its leadership in the orthopedic splints market can be attributed to strong healthcare infrastructure. High adoption of advanced orthopedic care was also observed. The presence of a large patient base with trauma and musculoskeletal conditions supported the demand. Favorable reimbursement structures further accelerated product utilization.

Strong availability of specialized orthopedic services has been noted across the region. Diagnostic and treatment capabilities were expanded in hospitals and outpatient centers. These factors improved patient access to splints and immobilization devices.

The growth of the market in the United States was supported by higher injury incidence. Sports-related trauma and road accidents remained major contributors. Increased awareness of early fracture management also strengthened product penetration. Canada showed steady demand growth due to rising healthcare spending and improved clinical guidelines for fracture stabilization.

Technological improvements contributed to market expansion. Lightweight, durable, and customizable splint materials were adopted at a faster rate. This trend enhanced patient comfort and reduced treatment times. Clinical preference for noninvasive stabilization methods also encouraged wider use of splints.

Regulatory standards in North America provided consistent product quality. This created strong trust among healthcare professionals. Training programs for emergency responders and orthopedic teams raised treatment efficiency. These developments reinforced the region’s dominant market position.

Overall, steady investment in healthcare systems, strong clinical adoption, and a large patient pool ensured continued leadership of North America in the orthopedic splints market. The region is expected to maintain its strategic advantage due to ongoing innovation and high care accessibility.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

A competitive landscape overview of the orthopedic splints market indicates that leadership has been established by a group of multinational manufacturers with extensive product portfolios and strong distribution networks. Their market position has been supported by continuous investment in product innovation, lightweight materials, and patient-centric designs.

Expansion into emerging regions has been prioritized to capture rising trauma incidence and increasing healthcare expenditure. Mid-tier participants focus on cost-effective solutions and partnerships with regional hospitals to strengthen their presence. Specialized producers target niche segments such as pediatric and sports injury applications, contributing to market persification.

Strategic activities, including regulatory approvals and portfolio upgrades, have enhanced competitiveness. The overall environment remains moderately consolidated, with steady competition driven by quality standards, after-sales support, and technological improvements.

Market Key Players

- DeRoyal Industries

- Dynasplint Systems, Inc.

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Ottobock SE & Co. KGaA

- Essity AB

- Bauerfeind AG

- 3M

- Össur

- Breg, Inc.

- Medi GmbH & Co. KG

- Sam Medical

- Orthosys

- DJO Global, Inc.

- Tynor Orthotics Pvt. Ltd.

- Plasti Surge Industries Pvt. Ltd.

Recent Developments

- Dynasplint Systems, Inc. (June 2025): updated its dynamic splinting product line by releasing a refined low-load prolonged-duration stretching system for ankle and foot rehabilitation, enhancing home-therapy support.

- Stryker Corporation (July 2024): completed acquisition of Artelon Inc., a soft-tissue fixation specialist in foot & ankle/sports medicine, strengthening its extremities portfolio.

- Ottobock SE & Co. KGaA (September 2025): prepared listing on the Frankfurt stock exchange, raising ~€100 million in new capital as part of its global mobility-aid growth strategy.

- Össur (September 2025): acquired FIOR & GENTZ, a custom-orthosis planning and production provider, expanding its brace/orthosis manufacturing capabilities.

Report Scope

Report Features Description Market Value (2024) US$ 2.14 Billion Forecast Revenue (2034) US$ 5.76 Billion CAGR (2025-2034) 10.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Fibreglass splints, Plaster splints, Thermoplastic/composite splints, Splinting tools & accessories, Others) By Anatomical Location (Lower extremity, Upper extremity) By Type (Rigid/static splints, Dynamic/functional splints) By Application (Immobilization, Rehabilitation, Support, Prophylactic/preventive use) By End-User (Hospitals, Specialty Centers, Orthopedic clinics, Others) Regional Analysis North America-US, Canada, Mexico;Europe-Germany, UK, France, Italy, Russia, Spain, Rest of Europe;APAC-China, Japan, South Korea, India, Rest of Asia-Pacific;South America-Brazil, Argentina, Rest of South America;MEA-GCC, South Africa, Israel, Rest of MEA Competitive Landscape DeRoyal Industries, Dynasplint Systems, Inc., Zimmer Biomet Holdings, Inc., Stryker Corporation, Ottobock SE & Co. KGaA, Essity AB, Bauerfeind AG, 3M, Össur, Breg, Inc., Medi GmbH & Co. KG, Sam Medical, Orthosys, DJO Global, Inc., Tynor Orthotics Pvt. Ltd., Plasti Surge Industries Pvt. Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- DeRoyal Industries

- Dynasplint Systems, Inc.

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Ottobock SE & Co. KGaA

- Essity AB

- Bauerfeind AG

- 3M

- Össur

- Breg, Inc.

- Medi GmbH & Co. KG

- Sam Medical

- Orthosys

- DJO Global, Inc.

- Tynor Orthotics Pvt. Ltd.

- Plasti Surge Industries Pvt. Ltd.

Our Clients

- 164569

- Nov 2025