Global Organic Baby Toiletries Market Size, Share, Growth Analysis By Product (Skin Care, Bathing Products, Diapers, Wipes, Hair Care, Others), By Formulation (Liquid, Cream, Gel), By End User (Infants, Toddlers), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180254

- Number of Pages: 284

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

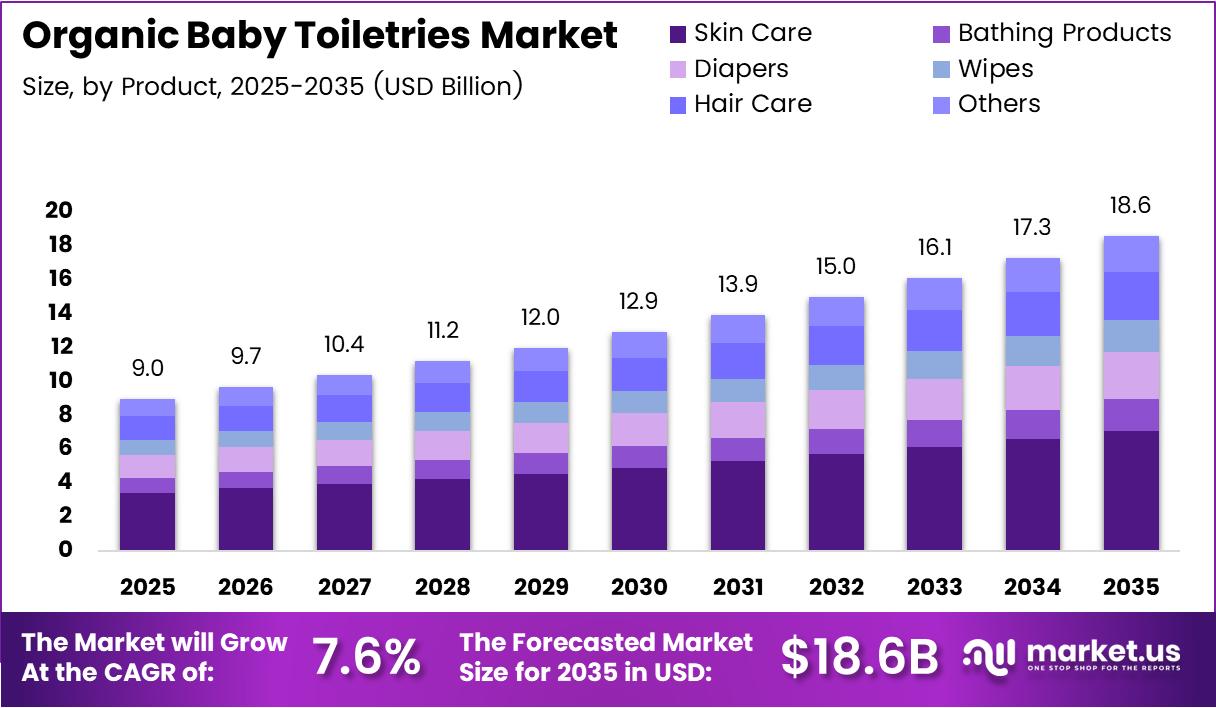

Global Organic Baby Toiletries Market size is expected to be worth around USD 18.6 Billion by 2035 from USD 9.0 Billion in 2025, growing at a CAGR of 7.6% during the forecast period 2026 to 2035.

The organic baby toiletries market covers plant-based and certified organic personal care products developed specifically for infants and toddlers. These include skin care formulations, bathing products, diapers, wipes, and hair care items. Manufacturers formulate these products without synthetic chemicals, parabens, or artificial fragrances. Consequently, they appeal directly to parents who prioritize skin safety and ingredient transparency.

Parental concern about toxic ingredient exposure has reshaped purchasing behavior across baby personal care. Health-conscious parents now actively seek dermatologically tested, hypoallergenic, and plant-based alternatives to conventional baby products. This shift is not trend-driven — it reflects a structural change in how families evaluate risk for infant skincare. Moreover, pediatrician endorsement of mild organic formulations has reinforced clinical credibility for this category.

Government and regulatory bodies across North America and Europe have tightened standards for cosmetic ingredients used in baby products. These regulations restrict synthetic preservatives and require fuller ingredient disclosure. As a result, brands formulating to organic certification standards gain a compliance advantage. This creates a higher barrier for conventional players trying to enter the certified organic segment without reformulation investment.

E-commerce and direct-to-consumer channels have accelerated access to premium organic baby toiletries beyond traditional retail. Parents research ingredients online before purchasing, giving transparent brands a discoverability advantage. Additionally, subscription-based purchasing models for diapers and wipes have improved repeat purchase rates for organic brands. This is reshaping distribution economics in favor of digitally-native organic baby care companies.

According to Indian Retailer, 61% of parents prefer baby products formulated with natural ingredients. This figure signals that natural-ingredient preference has crossed from niche to mainstream — meaning conventional brands that fail to reformulate now face direct shelf-share loss rather than a peripheral threat.

According to XJ Beauty research, around 60% of infants experience skin sensitivities during the first year of life. This clinical reality means the target consumer for organic baby toiletries is not defined by parental preference alone — it is defined by physiological need. That distinction gives organic formulations a defensible medical-use rationale that conventional products cannot easily replicate.

In 2025, Ceuticoz entered the baby care segment with Ceuticoz Baby, a dermatology-developed range aligning with the shift toward medicalized and natural baby toiletries. This type of entry by dermatology-positioned brands confirms that the organic baby toiletries market is attracting credibility-first competitors, raising the quality benchmark across the entire category.

Key Takeaways

- The Global Organic Baby Toiletries Market was valued at USD 9.0 Billion in 2025 and is forecast to reach USD 18.6 Billion by 2035.

- The market advances at a CAGR of 7.6% during the forecast period 2026 to 2035.

- By Product, Skin Care leads the market with a 38.2% share in 2025.

- By Formulation, Liquid formulations hold the dominant share of 51.5%.

- By End User, Infants represent the largest segment with a 63.7% share.

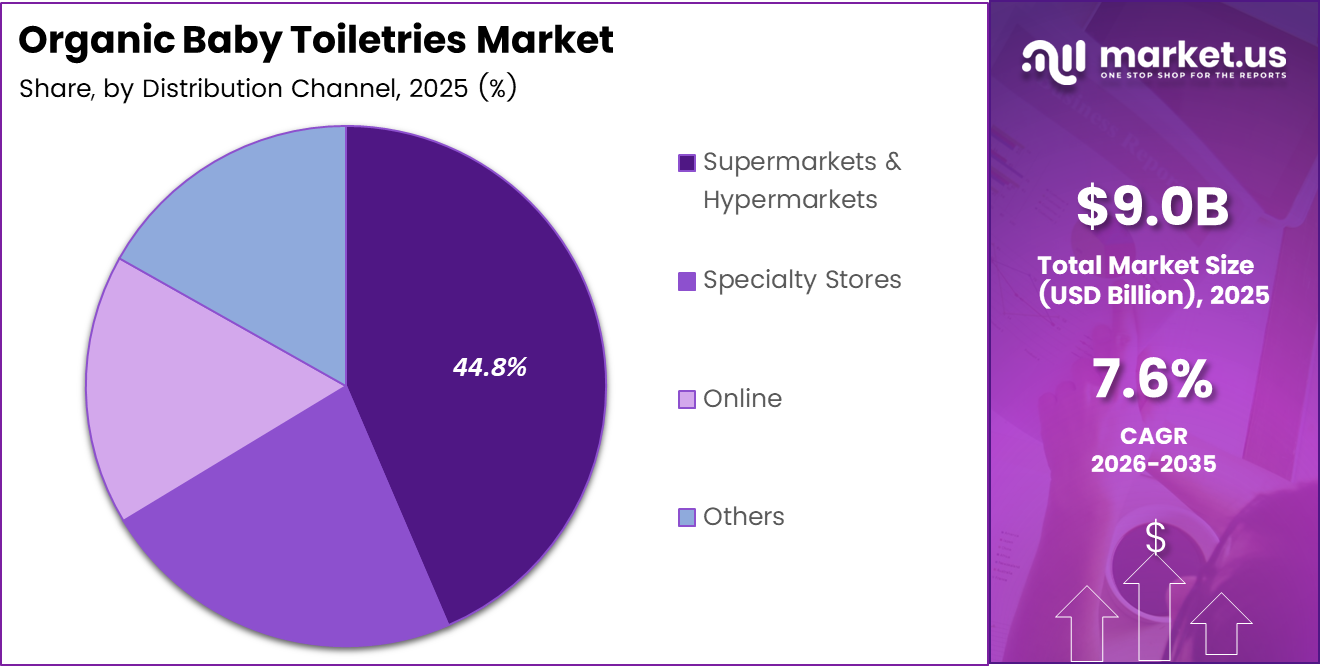

- By Distribution Channel, Supermarkets and Hypermarkets lead with a 44.8% share.

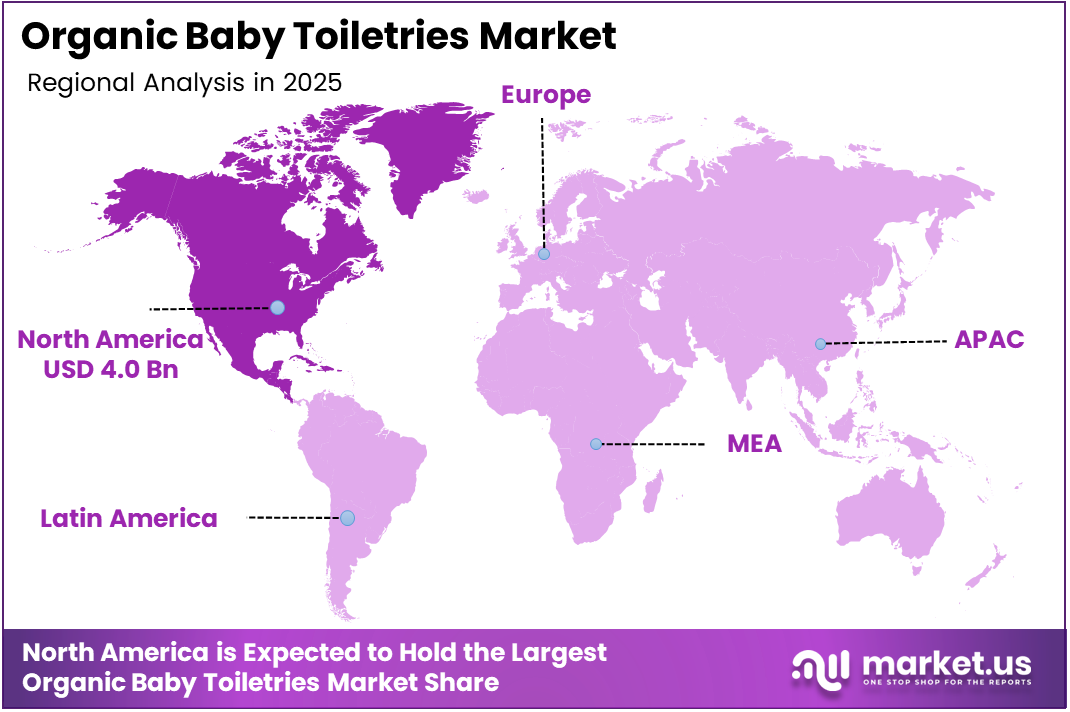

- North America dominates the global market with a 45.30% share, valued at USD 4.0 Billion in 2025.

Product Analysis

Skin Care dominates with 38.2% due to high infant skin sensitivity and clinical demand.

In 2025, Skin Care held a dominant market position in the By Product segment of the Organic Baby Toiletries Market, with a 38.2% share. According to Dandle•LION Medical, infant skin is around 20% thinner than adult skin, increasing permeability to topical ingredients. This biological vulnerability directly drives parental preference for certified organic skin care formulations and separates this sub-segment from all other product categories.

Bathing Products represent the highest-frequency daily-use category within organic baby toiletries. Parents apply wash and bath products at every bath, creating consistent repeat-purchase behavior. Moreover, bathing products serve as the entry point for organic baby care adoption — parents typically start with wash before transitioning to broader organic skincare regimens. This positions bathing products as a gateway segment for brand loyalty.

Diapers carry the highest volume-per-infant consumption of any single baby toiletry product. A single infant uses hundreds of diapers monthly, making this segment highly attractive for subscription and repeat-purchase models. However, organic diaper production involves stricter material sourcing requirements, which constrains supply scalability. Brands that solve the certified organic materials challenge in diapers hold a structural pricing advantage.

Wipes function as a multi-purpose hygiene product used far beyond diaper changes, including face cleaning and surface sanitization in infant environments. The convenience factor drives consistent demand across all retail formats. In February 2025, Fixderma launched the Hoopoe baby care line focusing on natural formulations, reflecting the broader industry movement to bridge mass-market accessibility with dermatological positioning in products like wipes.

Hair Care for infants occupies a specialized niche within organic baby toiletries, characterized by ultra-mild, tear-free formulations. Parental sensitivity to fragrance and sulfate content is highest in this sub-segment. Additionally, hair care products serve a secondary function as scalp treatments for common infant conditions such as cradle cap, giving organic formulations a functional-use advantage over conventional alternatives.

Others within the product category include organic baby sunscreens, oral care products, and specialty barrier creams. These are lower-volume but higher-margin items. Consequently, they attract premium positioning strategies from specialty organic brands targeting health-focused parents willing to pay for comprehensive organic baby care routines beyond core hygiene products.

Formulation Analysis

Liquid dominates with 51.5% due to easy application and parent-preferred rinse-off convenience.

In 2025, Liquid held a dominant market position in the By Formulation segment of the Organic Baby Toiletries Market, with a 51.5% share. Liquid formulations cover the highest-use baby product formats — washes, shampoos, and cleansers — where rinse-off convenience is critical. This dominance reflects that parents select organic baby toiletries primarily for daily hygiene routines where liquid formats are the practical standard.

Cream formulations serve the leave-on skincare segment, including moisturizers, diaper rash treatments, and protective barrier creams. These products carry higher per-unit margins than rinse-off liquids because ingredient concentration and skin-contact time are greater. Moreover, cream formulations are where dermatologist recommendations carry the most weight, making this sub-segment particularly responsive to clinical endorsement and certification labels.

Gel formulations occupy a smaller but growing position in organic baby toiletries, primarily in teething gels, hair styling products for toddlers, and specialty cleansers. The format appeals to parents seeking lightweight, non-greasy options. However, gel stability using only organic-certified preservatives presents a technical formulation challenge. Brands that resolve this stability constraint differentiate meaningfully in the premium organic gel segment.

End User Analysis

Infants dominate with 63.7% due to highest skincare vulnerability and first-purchase brand decisions.

In 2025, Infants held a dominant market position in the By End User segment of the Organic Baby Toiletries Market, with a 63.7% share. The infant segment drives organic purchase decisions most intensely because parents are forming brand habits during a period of maximum safety concern. First purchases made in the newborn stage are highly sticky — parents who adopt organic brands for infants rarely revert to conventional alternatives as children grow.

Toddlers represent a segment where organic baby toiletries usage continues but purchase urgency decreases relative to the infant stage. Parents remain loyal to organic brands established during infancy, though product needs shift toward items like organic toothpaste, detangling sprays, and sunscreens. Therefore, brands that successfully capture the infant stage inherit a natural toddler customer — making infant-stage acquisition the most commercially critical entry point in this market.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 44.8% due to high foot traffic and accessible shelf visibility.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Organic Baby Toiletries Market, with a 44.8% share. Large-format retail provides organic baby toiletry brands with simultaneous access to mainstream and health-conscious parent shoppers. Moreover, shelf placement next to conventional alternatives allows organic products to win at the point of decision, where ingredient comparisons occur in real time.

Specialty Stores serve the premium end of organic baby toiletries distribution, offering curated assortments with staff who can explain certification standards and ingredient differences. This channel commands higher average transaction values and attracts parents already committed to organic purchasing. Specialty retailers also provide emerging organic baby care brands a lower-volume but higher-credibility entry point before mainstream retail scale.

Online distribution has become structurally important for organic baby toiletries because parents research ingredients extensively before buying. Digital channels allow brands to communicate formulation stories, certifications, and clinical testing results that physical shelf labels cannot accommodate. Additionally, subscription models available through e-commerce platforms generate predictable revenue for high-repurchase products like diapers and wipes.

Others in distribution include pharmacies, baby specialty boutiques, pediatric clinics, and direct brand websites. Pharmacy placement carries clinical association that reinforces organic baby product credibility — parents who receive product recommendations from pediatricians often fulfill those purchases at pharmacy counters. This channel is smaller in volume but disproportionately influential in shaping trial and first adoption.

Key Market Segments

By Product

- Skin Care

- Bathing Products

- Diapers

- Wipes

- Hair Care

- Others

By Formulation

- Liquid

- Cream

- Gel

By End User

- Infants

- Toddlers

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Online

- Others

Drivers

Parental Awareness of Chemical Exposure and Clinical Evidence Drive Organic Baby Toiletry Adoption

Parents today make baby product purchasing decisions with far greater ingredient scrutiny than previous generations. According to XJ Beauty research, infants can absorb up to 60% more chemicals through their skin than adults. This physiological fact converts parental concern into a concrete purchasing criterion — making organic, low-toxin formulations the rational choice rather than simply the aspirational one.

Pediatrician and dermatologist recommendations have become the single most trusted purchase trigger in this market. When clinical professionals endorse mild, plant-based formulations for infant skin, parents act on that advice immediately. This professional validation narrows the decision process for first-time parents and accelerates trial of organic alternatives. Moreover, in December 2025, TAKE ME HOME launched its first natural and organic-leaning baby care line, reflecting how brand entrants are directly responding to this clinically-endorsed market pull.

According to PMC research, around 60% of cosmetics formulated for atopic dermatitis contain sensitizing substances capable of triggering allergic reactions. This finding exposes a critical gap in the conventional baby care market — even products marketed as sensitive-skin solutions carry allergy risk. Organic baby toiletries that minimize synthetic additives fill this gap, giving brands with clean-label credentials a defensible clinical positioning that conventional competitors cannot easily replicate.

Restraints

Premium Pricing and Raw Material Supply Constraints Limit Organic Baby Toiletry Market Penetration

Certified organic baby toiletries consistently retail at a significant premium over conventional alternatives. This price gap limits household adoption among cost-sensitive parents, particularly in middle- and lower-income demographics. Organic certification adds sourcing, testing, and compliance costs that manufacturers pass through to shelf price. Consequently, even parents who prefer organic formulations often default to conventional products at the point of purchase.

According to PMC research, 89% of products labeled “hypoallergenic” still contain potentially allergenic compounds. This finding reveals a consumer trust deficit that organic brands must actively overcome. Parents who have purchased “hypoallergenic” conventional products and experienced adverse reactions become skeptical of all label claims — including organic certifications. Rebuilding this trust requires clinical documentation and third-party verification that adds further cost to organic brand positioning.

Supply of certified organic raw materials for infant care formulations remains inconsistent globally. Seasonal agricultural variability, limited certified-organic supplier networks, and strict quality controls create bottlenecks for manufacturers scaling production. This supply fragility forces organic baby care brands to either over-source at higher cost or accept production gaps that damage retailer relationships. Until the certified organic ingredients supply chain matures, volume growth for this market remains structurally constrained.

Growth Factors

E-Commerce Expansion, Clinical Proof of Efficacy, and Emerging Urban Demand Open New Revenue Channels

E-commerce and direct-to-consumer platforms give organic baby toiletry brands direct access to health-conscious urban parents who research ingredients extensively before purchasing. This channel eliminates the shelf-space constraint that limits smaller organic brands in physical retail. Moreover, subscription models for diapers and wipes generate predictable recurring revenue — a structural advantage that conventional mass-market brands have not yet replicated effectively in the organic segment.

According to a clinical study published in PubMed, skin hydration in infants improved by 37% after one week of consistent use of natural baby skincare products. According to PMC, 90% of parents in the same study reported these products were mild and gentle. These clinical results transform organic baby toiletries from a preference-based purchase into an evidence-based medical recommendation — significantly expanding the addressable market beyond early adopters to mainstream healthcare-directed buyers.

In October 2024, Millennium Babycares raised USD 14.5 million in funding led by Bharat Value Fund, plus an additional INR 122 crore for product innovation and expansion in premium and natural baby care. This investment activity signals that institutional capital recognizes the urban emerging-market growth opportunity in organic baby toiletries. Urban middle-class households in India and other high-growth markets represent a structurally new demand base that established Western brands have not yet fully addressed.

Emerging Trends

Ingredient Transparency, Vegan Certifications, and Microbiome-Aware Formulations Define Next-Generation Organic Baby Care

Clean-label and full ingredient disclosure have shifted from a marketing differentiator to a baseline consumer expectation in baby toiletries. Parents now cross-reference ingredient lists against safety databases before purchasing. Brands that disclose every ingredient — including processing aids — build trust that opacity-first competitors cannot match. This transparency expectation is redefining what “organic” means to buyers beyond simple certification seals.

Vegan, cruelty-free, and USDA-certified organic credentials are increasingly bundled as a single positioning statement rather than separate claims. This bundling reflects parents’ desire for comprehensive ethical and health assurance from a single product. According to XJ Beauty research, organic farming methods reduce energy consumption by approximately 30–50% compared to conventional agriculture — giving sustainable-sourcing brands a compelling environmental story that resonates with eco-conscious millennial parents making purchasing decisions.

Microbiome-friendly and dermatologically-tested formulations represent the most technically advanced frontier in organic baby toiletries. Research increasingly links early microbiome disruption to long-term skin and immune health outcomes in infants. Brands that formulate with microbiome preservation in mind — using prebiotics and minimal-ingredient profiles — are positioning in front of a clinical trend that mainstream baby care has not yet addressed. Early movers in this space will define the premium tier of this market for the next decade.

Regional Analysis

North America Dominates the Organic Baby Toiletries Market with a Market Share of 45.30%, Valued at USD 4.0 Billion

North America leads with a 45.30% share, valued at USD 4.0 Billion in 2025. The region’s dominance reflects early regulatory mandates on cosmetic ingredient safety, a mature premium retail infrastructure, and high parental health literacy. U.S. consumers benefit from established organic certification frameworks and strong pediatric guidance culture, conditions that collectively sustain premium willingness-to-pay for certified organic baby toiletries.

Europe Organic Baby Toiletries Market Trends

Europe maintains a strong position in organic baby toiletries driven by stringent EU cosmetic regulations that restrict synthetic ingredient use more broadly than most global markets. German and French consumers demonstrate particularly high organic product adoption rates. Additionally, strong retail penetration of pharmacy chains and organic specialty stores across Western Europe gives certified organic baby care brands efficient distribution without reliance on mass-market channels.

Asia Pacific Organic Baby Toiletries Market Trends

Asia Pacific presents the fastest-expanding demand base for organic baby toiletries, anchored by urbanizing middle-class populations in China, India, and Southeast Asia. Rising awareness of infant skin sensitivity among educated urban parents — combined with rapid e-commerce penetration — is creating a new premium baby care consumer class. Moreover, domestic brand investment, as seen with Millennium Babycares in India, signals that local players are competing directly with Western imports.

Latin America Organic Baby Toiletries Market Trends

Latin America shows developing but accelerating interest in organic baby personal care, primarily in Brazil and Mexico where urban middle-class consumers increasingly align with global clean-label trends. Modern retail expansion and growing e-commerce infrastructure are improving access to certified organic baby products beyond major metropolitan areas. However, price sensitivity in broader consumer segments remains a structural constraint on mass adoption across the region.

Middle East and Africa Organic Baby Toiletries Market Trends

The Middle East and Africa market for organic baby toiletries is at an early stage of penetration, concentrated in GCC urban centers where premium imported baby care brands find receptive, high-income consumers. South Africa represents a secondary growth pocket with rising health-conscious parenting communities. Distribution infrastructure limitations and import cost premiums restrict market expansion beyond affluent urban segments across most of the broader MEA region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Earth Mama has built its competitive position on clinically-tested, midwife-recommended formulations — a trust signal that most organic baby care brands cannot credibly claim. By grounding its brand in maternal and neonatal clinical contexts, Earth Mama differentiates beyond ingredient lists into outcome-based credibility. This clinical positioning makes the brand particularly resilient to generic organic entrants competing primarily on price or packaging aesthetics.

California Baby occupies the premium tier of the organic baby toiletries market with a long-established track record in hypoallergenic and fragrance-free formulations. The brand’s strength lies in its early-mover advantage in eczema-prone and sensitive infant skin formulations — a category where parental switching costs are high once a trusted product is identified. This creates durable repeat purchase rates that newer organic entrants struggle to disrupt through promotional pricing alone.

Nature’s Baby Organics differentiates through a wide certified organic product range that spans hair care, skin care, and bathing — enabling parents to build a complete single-brand organic routine. This full-line strategy reduces parental decision fatigue and strengthens household penetration. Moreover, the brand’s consistent USDA-certified organic positioning across all SKUs provides regulatory-grade ingredient assurance that resonates strongly with health-literate consumers in North American and European markets.

The Honest Company, Inc. leverages its publicly-listed brand equity and broad mass-market retail presence to compete at the intersection of organic credentials and mainstream accessibility. Unlike specialty-only organic brands, The Honest Company’s Walmart and Target distribution gives it volume scale that pure specialty players cannot match. In April 2025, ITC acquired Mother Sparsh to build a comparable natural baby care portfolio in India — validating the commercial logic of combining brand credibility with mainstream retail reach.

Key players

- Earth Mama

- California Baby

- Nature’s Baby Organics

- The Honest Company, Inc.

- Green People

- Burt’s Bees Baby

- LittleTwig

- Erbaviva

- Babyganics

- Charlie Banana

Recent Developments

- November 2025 – Johnson’s Baby (Kenvue) upgraded its entire baby care range — including toiletries — with advanced skin-science formulas and more sustainable packaging, including bottles made from 50% recycled plastic. This move signals that legacy mass-market baby care brands are now directly competing with organic specialists on both formulation quality and sustainability credentials.

- 2025 – Ceuticoz entered the baby care market with Ceuticoz Baby, a dermatology-developed range covering wash, shampoo, and sunscreen. This launch aligns with the broader market shift toward medicalized and clinically-backed natural baby toiletry formulations that bridge the gap between pharmaceutical credibility and organic consumer preference.

- December 2025 – TAKE ME HOME, an Israeli textile brand, launched its first baby care product line at Super-Pharm stores, emphasizing natural ingredients, skin health, and environmental responsibility. The move demonstrates how brands from adjacent categories are recognizing and entering the organic baby care segment as parental demand for natural formulations continues to broaden beyond specialist channels.

Report Scope

Report Features Description Market Value (2025) USD 9.0 Billion Forecast Revenue (2035) USD 18.6 Billion CAGR (2026-2035) 7.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Skin Care, Bathing Products, Diapers, Wipes, Hair Care, Others), By Formulation (Liquid, Cream, Gel), By End User (Infants, Toddlers), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Earth Mama, California Baby, Nature’s Baby Organics, The Honest Company, Inc., Green People, Burt’s Bees Baby, LittleTwig, Erbaviva, Babyganics, Charlie Banana Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Organic Baby Toiletries MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Organic Baby Toiletries MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Earth Mama

- California Baby

- Nature's Baby Organics

- The Honest Company, Inc.

- Green People

- Burt's Bees Baby

- LittleTwig

- Erbaviva

- Babyganics

- Charlie Banana

Our Clients

- 180254

- Mar 2026