Quick Navigation

Report Overview

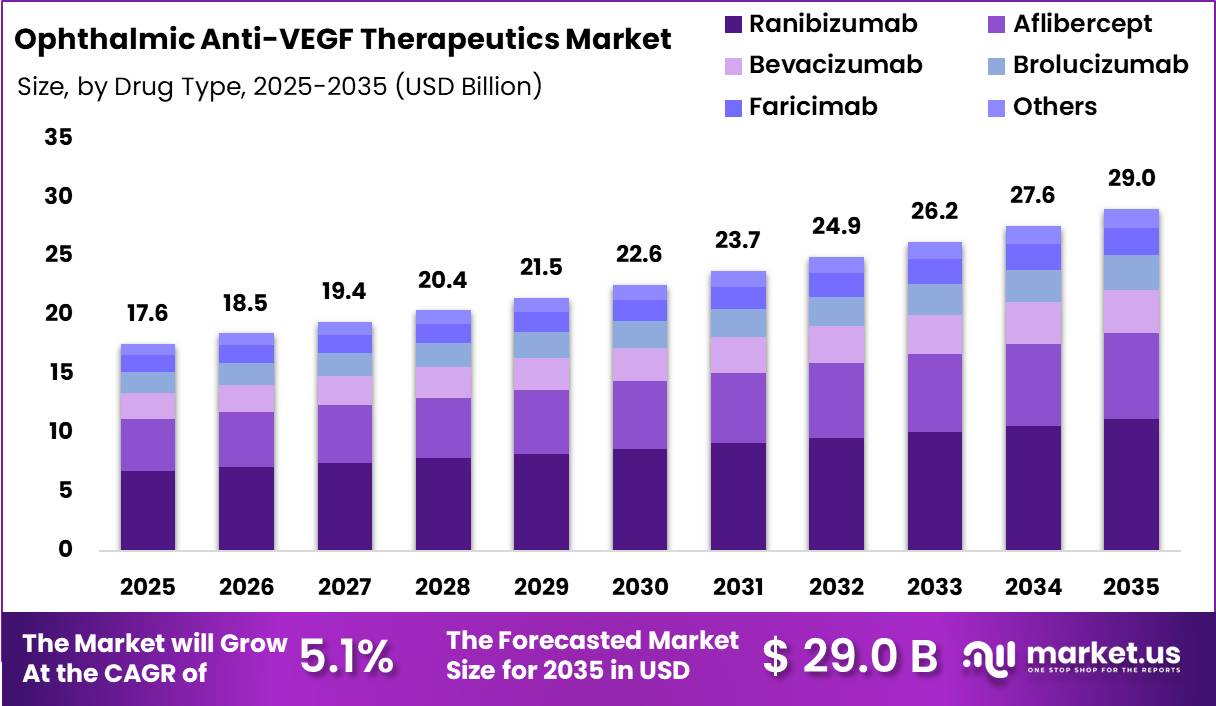

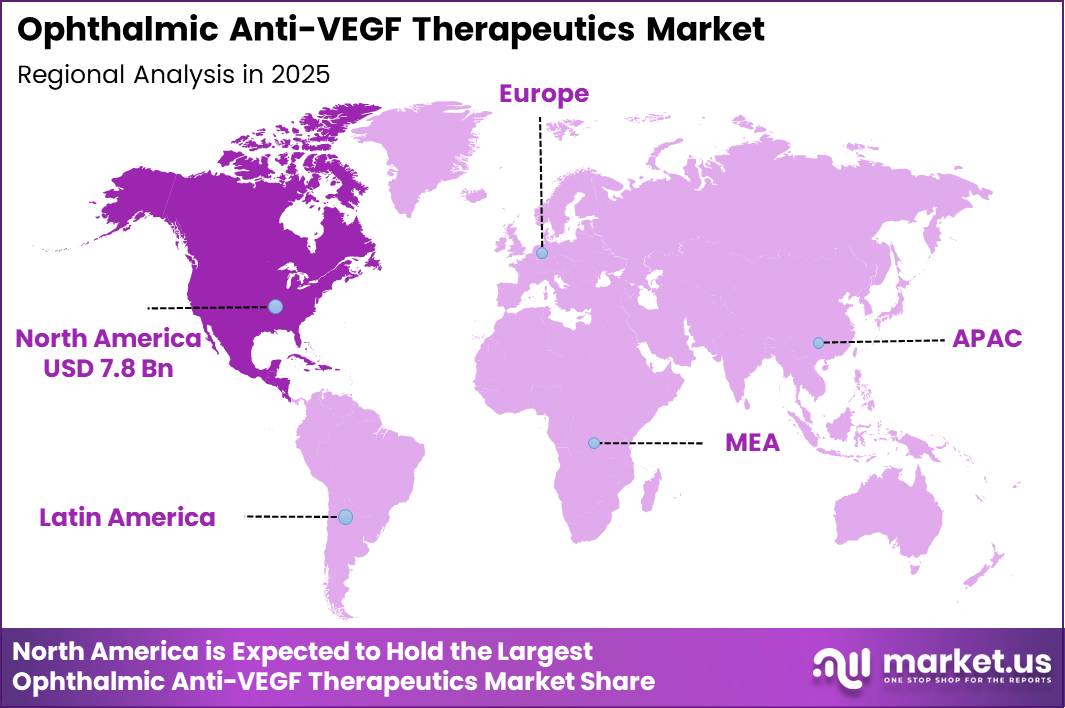

Global Ophthalmic Anti-VEGF Therapeutics Market size is expected to be worth around US$ 29.0 Billion by 2035 from US$ 17.6 Billion in 2025, growing at a CAGR of 5.1% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 44.5% share with a revenue of US$ 7.8 Billion.

The ophthalmic anti-VEGF therapeutics market represents a critical segment of the global ophthalmology industry, driven by the increasing prevalence of retinal vascular disorders and the growing need for effective vision-preserving treatments.

Anti-VEGF (vascular endothelial growth factor) therapies are designed to inhibit abnormal blood vessel growth and vascular leakage in the retina, making them the standard of care for conditions such as age-related macular degeneration (AMD), diabetic macular edema (DME), diabetic retinopathy (DR), and retinal vein occlusion (RVO). These diseases are among the leading causes of vision impairment and blindness worldwide, creating sustained demand for anti-VEGF therapies across developed and emerging healthcare markets.

The rising global burden of diabetes and age-related eye disorders is a major factor supporting market expansion. According to the International Diabetes Federation (IDF), approximately 589 million adults aged 20–79 years were living with diabetes worldwide in 2024, and this number is projected to reach 853 million by 2050. Diabetes significantly increases the risk of diabetic retinopathy and diabetic macular edema, both of which frequently require long-term anti-VEGF treatment.

In addition, the World Health Organization (WHO) estimates that at least 2.2 billion people globally experience near or distance vision impairment. Among vision-threatening conditions, age-related macular degeneration affects approximately 8 million people worldwide, while diabetic retinopathy accounts for nearly 3.9 million cases of vision impairment or blindness. Population aging and longer life expectancy are expected to further increase the incidence of these retinal diseases.

Market growth is also supported by continuous innovation in ophthalmic biologics, including long-acting anti-VEGF formulations, higher-dose therapies, and novel dual-target mechanisms designed to improve efficacy and reduce treatment frequency.

Ongoing investments in ophthalmology research, expanding access to specialized retinal care centers, and improving reimbursement frameworks are strengthening treatment adoption globally. As healthcare systems increasingly prioritize the prevention of vision loss and blindness, anti-VEGF therapeutics are expected to remain a cornerstone of retinal disease management, supporting long-term market growth and therapeutic advancement.

Key Takeaways

- Market Size: Global Ophthalmic Anti-VEGF Therapeutics Market size is expected to be worth around US$ 29.0 Billion by 2035 from US$ 17.6 Billion in 2025.

- Market Share: growing at a CAGR of 5.1% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Ranibizumab dominated the market with a 38.5% share in 2025.

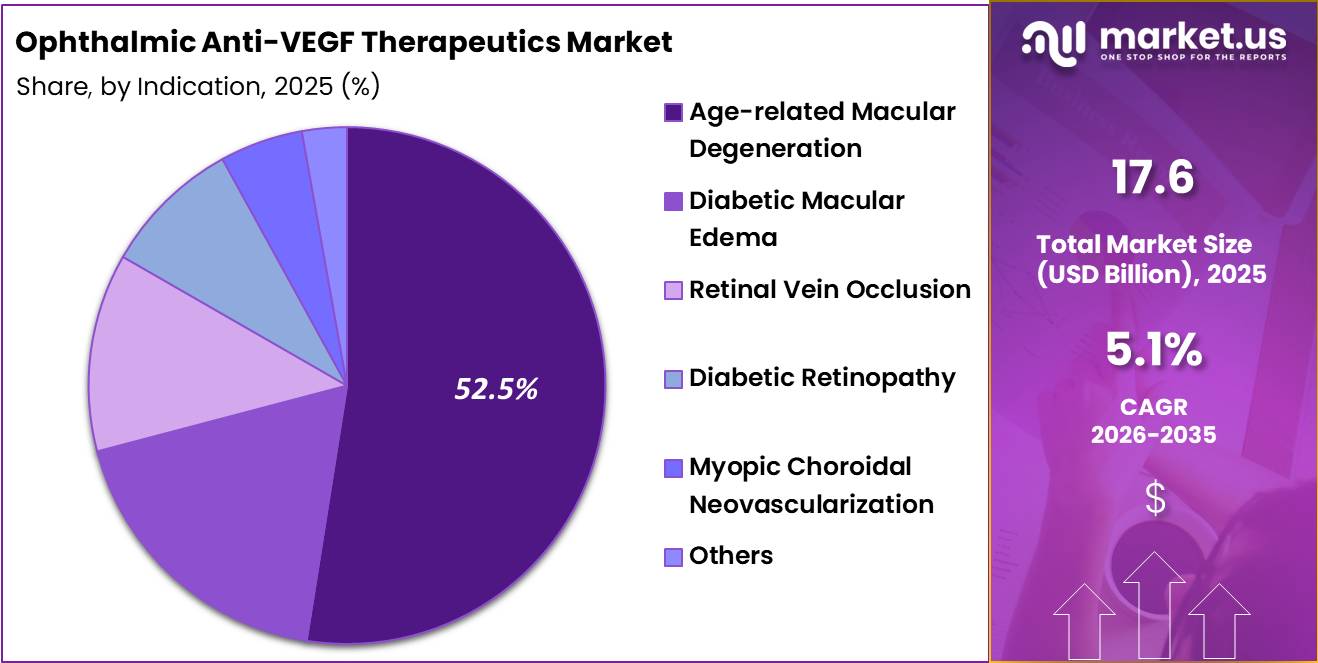

- Indication Analysis: Age-related Macular Degeneration accounted for the largest market share of 52.5% in 2025.

- End User Analysis: Hospitals held the dominant market share of 48.5% in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 44.5% share with a revenue of US$ 7.8 Billion.

Drug Type Analysis

The drug type segment of the Ophthalmic Anti-VEGF Therapeutics Market is categorized into Ranibizumab, Aflibercept, Bevacizumab, Brolucizumab, Faricimab, and Others. Ranibizumab dominated the market with a 38.5% share in 2025, primarily due to its long-established clinical efficacy, extensive regulatory approvals, and widespread adoption in the treatment of retinal vascular diseases. Its proven safety profile and strong physician confidence have supported sustained demand across major healthcare markets.

Aflibercept represents a significant segment owing to its high binding affinity for VEGF and longer dosing intervals, which reduce treatment burden for patients. Bevacizumab continues to maintain substantial utilization, particularly in cost-sensitive markets, due to its affordability and comparable clinical outcomes in several ophthalmic indications. Brolucizumab has gained attention for its ability to provide extended durability and improved retinal fluid control in selected patients.

Faricimab, a newer dual-pathway inhibitor targeting both VEGF-A and Angiopoietin-2, is witnessing rapid adoption because of its enhanced efficacy and longer treatment intervals. The Others category includes emerging anti-VEGF therapies and biosimilars that are expected to strengthen market competition and expand treatment accessibility during the forecast period.

Indication Analysis

Based on indication, the Ophthalmic Anti-VEGF Therapeutics Market is segmented into Age-related Macular Degeneration (AMD), Diabetic Macular Edema (DME), Retinal Vein Occlusion (RVO), Diabetic Retinopathy (DR), Myopic Choroidal Neovascularization (mCNV), and Others. Age-related Macular Degeneration accounted for the largest market share of 52.5% in 2025, driven by the increasing prevalence of the aging population and the high incidence of neovascular AMD worldwide. Anti-VEGF therapies remain the standard of care for preserving vision and preventing disease progression in AMD patients.

Diabetic Macular Edema represents the second-largest segment, supported by the growing global burden of diabetes and rising awareness regarding early retinal disease management. Retinal Vein Occlusion continues to generate notable demand for anti-VEGF treatments due to their effectiveness in reducing macular edema and improving visual outcomes.

Diabetic Retinopathy is experiencing increasing treatment adoption as screening programs and diagnosis rates improve globally. Myopic Choroidal Neovascularization contributes a smaller but steadily expanding share, particularly in regions with high myopia prevalence. The Others segment includes less common retinal disorders requiring VEGF inhibition, contributing to market diversification and supporting the continued expansion of ophthalmic therapeutic applications.

End User Analysis

Based on end user, the Ophthalmic Anti-VEGF Therapeutics Market is segmented into Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers, and Others. Hospitals held the dominant market share of 48.5% in 2025, owing to their advanced ophthalmic infrastructure, availability of specialized retinal surgeons, and capacity to manage complex retinal disorders. Hospitals also benefit from integrated diagnostic and treatment facilities, making them the preferred setting for anti-VEGF administration and follow-up care.

Ophthalmic Clinics represent a significant market segment, supported by increasing patient preference for specialized eye care centers that offer focused expertise, shorter waiting times, and personalized treatment services. The growing number of dedicated retinal clinics across developed and emerging markets continues to strengthen segment growth. Ambulatory Surgical Centers (ASCs) are gaining traction due to their cost-effective treatment models, operational efficiency, and ability to perform ophthalmic procedures in outpatient settings.

Rising healthcare expenditure optimization initiatives are further supporting ASC adoption. The Others segment includes academic medical centers, research institutions, and community healthcare facilities involved in retinal disease management. Continued expansion of ophthalmic care networks and increasing access to specialized retinal treatments are expected to drive growth across all end-user categories throughout the forecast period.

Key Market Segments

By Drug Type

- Ranibizumab

- Aflibercept

- Bevacizumab

- Brolucizumab

- Faricimab

- Others

By Indication

- Age-related Macular Degeneration

- Diabetic Macular Edema

- Retinal Vein Occlusion

- Diabetic Retinopathy

- Myopic Choroidal Neovascularization

- Others

By End User

- Hospitals

- Ophthalmic Clinics

- Ambulatory Surgical Centers

- Others

Driving Factors

Rising Burden of Retinal Diseases and Vision Impairment

The increasing prevalence of retinal disorders such as age-related macular degeneration (AMD), diabetic retinopathy (DR), diabetic macular edema (DME), and retinal vein occlusion is a major driver for the ophthalmic anti-VEGF therapeutics market. Anti-VEGF therapies are considered the standard treatment for several retinal vascular diseases because they inhibit vascular endothelial growth factor (VEGF), a protein responsible for abnormal blood vessel growth and leakage in the retina.

According to the World Health Organization (WHO), at least 2.2 billion people worldwide live with near or distance vision impairment, and approximately 1 billion cases could have been prevented or remain untreated. WHO estimates indicate that around 8 million people are affected by age-related macular degeneration and 3.9 million people suffer from diabetic retinopathy-related vision impairment globally.

Furthermore, the growing prevalence of diabetes is increasing the incidence of DME and DR, creating substantial demand for anti-VEGF injections. The National Eye Institute (NEI) states that anti-VEGF therapies are widely used for wet AMD, diabetic retinopathy, and diabetic macular edema and often require repeated dosing to preserve vision. Aging populations and rising diabetes prevalence are therefore significantly expanding the patient pool requiring anti-VEGF treatment.

Trending Factors

Development of Longer-Acting and Reduced-Frequency Anti-VEGF Therapies

A significant trend in the ophthalmic anti-VEGF therapeutics market is the development of long-acting formulations designed to reduce treatment burden and improve patient adherence. Conventional anti-VEGF agents often require monthly or bimonthly intravitreal injections, creating challenges related to patient compliance, healthcare resource utilization, and treatment costs.

According to the National Eye Institute, many patients initially receive anti-VEGF injections once every month before transitioning to less frequent treatment schedules depending on disease progression. This frequent administration has encouraged pharmaceutical innovation toward therapies capable of maintaining efficacy with extended dosing intervals. New-generation anti-VEGF drugs and delivery systems are being developed to sustain therapeutic activity for longer durations, thereby reducing the number of annual injections.

The trend is particularly important because most patients affected by wet AMD and diabetic retinal diseases are over 50 years of age, a population that may face mobility and access challenges. The World Health Organization also highlights that population aging is increasing the number of individuals susceptible to retinal diseases. Consequently, healthcare providers and regulatory authorities are increasingly supporting treatment approaches that maintain visual outcomes while minimizing clinic visits and injection frequency.

Restraining Factors

High Treatment Burden and Long-Term Therapy Requirements

Despite strong clinical efficacy, the ophthalmic anti-VEGF therapeutics market faces constraints associated with long-term treatment requirements and patient adherence challenges. Anti-VEGF therapies generally require repeated intravitreal injections administered by trained ophthalmologists, often extending over several years.

According to the National Eye Institute, patients commonly begin treatment with monthly injections and may continue receiving therapy at regular intervals to maintain disease control and prevent vision deterioration. This treatment burden can result in missed appointments, inconsistent therapy, and suboptimal clinical outcomes.

Additionally, repeated clinical visits increase healthcare system pressure, particularly in regions with limited ophthalmology infrastructure. The World Health Organization reports that vision impairment disproportionately affects low- and middle-income regions, where access to specialized eye care services remains constrained. WHO further notes that approximately 1 billion cases of vision impairment globally remain unaddressed, reflecting significant gaps in access to diagnosis and treatment.

The need for ongoing monitoring, imaging assessments, and recurrent injections can create financial and logistical barriers for both patients and healthcare providers. These factors may limit treatment uptake, especially among elderly populations and patients residing in rural or underserved areas, thereby restraining broader market expansion despite the proven effectiveness of anti-VEGF therapies.

Opportunity

Expanding Access to Eye Care in Emerging and Underserved Regions

A substantial opportunity for the ophthalmic anti-VEGF therapeutics market lies in improving access to retinal disease diagnosis and treatment across emerging economies and underserved healthcare systems.

WHO data further indicate that the prevalence of distance vision impairment in low- and middle-income regions is approximately four times higher than in high-income regions. As governments and public health agencies strengthen eye care infrastructure and integrate ophthalmology services into national healthcare programs, the diagnosis rates of retinal diseases are expected to increase significantly.

The WHO’s Integrated People-Centred Eye Care initiatives and global vision programs are promoting earlier detection and management of conditions such as diabetic retinopathy and age-related macular degeneration. Furthermore, the rising global diabetic population is expected to increase screening programs for retinal complications, creating additional demand for anti-VEGF treatments.

Expanded insurance coverage, teleophthalmology services, and investment in specialized retinal care centers can improve treatment accessibility. With millions of untreated patients and increasing awareness regarding preventable blindness, emerging markets present considerable growth potential for anti-VEGF manufacturers seeking to expand their patient reach and improve visual health outcomes worldwide.

Regional Analysis

North America dominated the ophthalmic anti-VEGF therapeutics market in 2025, accounting for over 44.5% of the global market and generating revenue of US$ 7.8 billion. The region’s leadership can be attributed to the high prevalence of retinal disorders such as age-related macular degeneration (AMD), diabetic retinopathy (DR), and diabetic macular edema (DME), coupled with advanced healthcare infrastructure and strong access to innovative biologic therapies.

The presence of leading biotechnology and pharmaceutical companies, favorable reimbursement policies, and widespread adoption of anti-VEGF treatments further support market growth across the United States and Canada.

Europe represented the second-largest regional market, driven by increasing geriatric populations, rising diabetes prevalence, and well-established ophthalmology care networks. Countries such as Germany, the United Kingdom, France, Italy, and Spain continue to witness growing demand for retinal disease management and advanced intravitreal therapies.

The Asia-Pacific region is expected to register the fastest growth during the forecast period. Expanding healthcare investments, improving access to specialized eye care services, increasing awareness of vision-threatening diseases, and a rapidly growing diabetic population are contributing to market expansion across China, Japan, India, South Korea, and Australia.

Latin America, the Middle East, and Africa are emerging markets with significant long-term potential. Improvements in healthcare infrastructure, growing screening programs for retinal diseases, and increasing availability of ophthalmic biologics are expected to enhance treatment adoption across these regions. However, limited access to specialized ophthalmologists and reimbursement challenges continue to influence market penetration in several developing countries.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The ophthalmic anti-VEGF therapeutics market is characterized by the presence of several leading pharmaceutical and biotechnology companies focused on developing innovative treatments for retinal disorders. F. Hoffmann-La Roche Ltd. maintains a strong market position through its widely adopted anti-VEGF therapies and extensive global distribution network. Regeneron Pharmaceuticals, Inc. is a major competitor, supported by strong clinical outcomes and continued investments in product lifecycle expansion.

Novartis AG has strengthened its presence through strategic collaborations and commercialization initiatives targeting retinal diseases. Bayer AG remains an important participant through marketing partnerships and broad geographic reach. Emerging companies are increasingly focusing on next-generation anti-VEGF agents with improved durability, reduced injection frequency, and enhanced patient outcomes.

Market participants are actively investing in clinical trials, research and development, and strategic alliances to expand their product portfolios. Competitive intensity is expected to increase as biosimilars enter the market and novel therapies gain regulatory approvals, fostering innovation and market growth.

Market Key Players

- Novartis AG

- Regeneron Pharmaceuticals Inc.

- Bayer AG

- Roche Holding AG

- Amgen Inc.

- Viatris Inc.

- Samsung Bioepis Co., Ltd.

- Biogen Inc.

- Apellis Pharmaceuticals Inc.

- Kodiak Sciences Inc.

- Ophthotech Corporation

- Alimera Sciences Inc.

- Graybug Vision Inc.

- Outlook Therapeutics Inc.

- Oxurion NV

- Others

Recent Developments

- Roche (April, 2026): Roche announced that it will present extensive new real-world and clinical data on its ophthalmology portfolio, including Vabysmo and the port-delivery Susvimo platform, at ARVO 2026, underscoring continued lifecycle management and evidence-generation around its anti-VEGF franchise.

- Samsung Bioepis Co., Ltd.(January, 2026): Samsung Bioepis confirmed that commercialization of BYOOVIZ (ranibizumab-nuna) in a new pre-filled syringe presentation would start in January 2026, enhancing injector convenience and supporting broader ophthalmology adoption of its Lucentis biosimilar.

- Regeneron Pharmaceuticals Inc.(February, 2026): Market commentary highlighted that Eylea HD (aflibercept 8 mg) US sales grew 36% year-on-year to about 1.6 billion dollars in 2025, indicating rapid uptake of the high-dose formulation and confirming Regeneron’s strategic shift toward extended-interval dosing amid rising biosimilar pressure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 17.6 Billion |

| Forecast Revenue (2035) | US$ 29.0 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Ranibizumab, Aflibercept, Bevacizumab, Brolucizumab, Faricimab, Others) By Indication (Age-related Macular Degeneration, Diabetic Macular Edema, Retinal Vein Occlusion, Diabetic Retinopathy, Myopic Choroidal Neovascularization, Others) By End User (Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Novartis AG, Regeneron Pharmaceuticals Inc., Bayer AG, Roche Holding AG, Amgen Inc., Viatris Inc., Samsung Bioepis Co., Ltd., Biogen Inc., Apellis Pharmaceuticals Inc., Kodiak Sciences Inc., Ophthotech Corporation, Alimera Sciences Inc., Graybug Vision Inc., Outlook Therapeutics Inc., Oxurion NV, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |