Global OCI Registry Security Market By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small And Medium Enterprises, Large Enterprises), By End-User (BFSI, Healthcare, IT And Telecommunications, Retail, Government, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 179458

- Number of Pages: 378

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component

- By Deployment Mode

- By Organization Size

- By End User

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

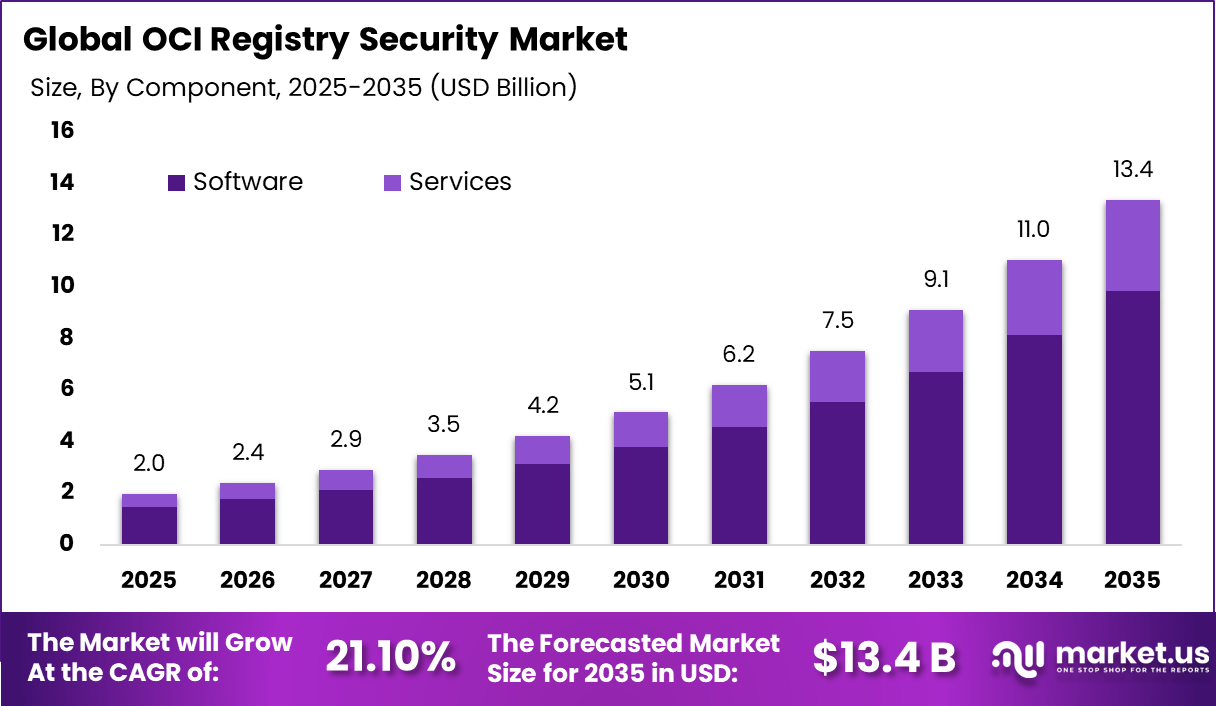

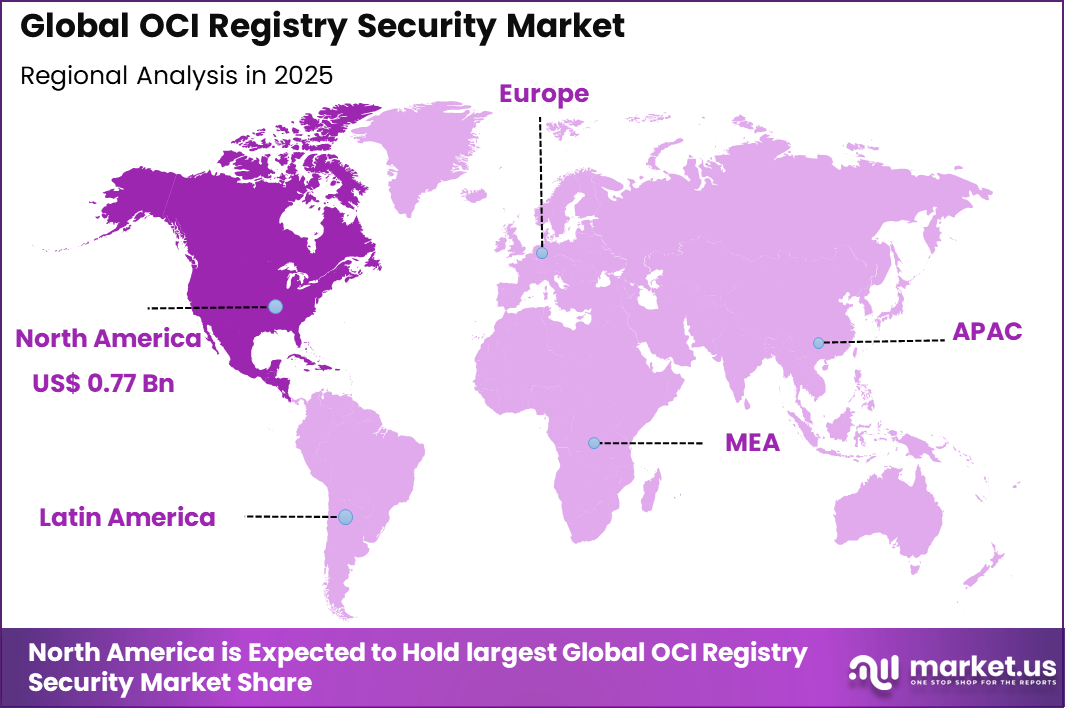

The Global OCI Registry Security Market generated USD 2 billion in 2025 and is predicted to register growth from USD 2.4 billion in 2026 to about USD 13.4 billion by 2035, recording a CAGR of 21.10% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 39.5% share, holding USD 0.77 Billion revenue.

The OCI Registry Security Market refers to the range of tools, practices, and services designed to protect container images, artifacts, and metadata stored in OCI compatible registries. Open Container Initiative (OCI) standards define how container images and software artifacts are packaged and shared across development pipelines. As organizations adopt containers extensively, ensuring the integrity, authenticity, and confidentiality of these assets becomes a priority.

Registry security addresses risks such as vulnerable images, unauthorized access, and supply chain threats that can affect deployment environments. One major driver of the OCI Registry Security Market is the widespread adoption of container based architectures. Containers have become a standard for building and deploying applications because of their portability and efficiency. More than 70% of organizations report using containers in at least some production workloads.

Top Market Takeaways

- By Component, software dominates with 73.6% share, delivering vulnerability scanners, image signing, and runtime policy enforcement for container registries hosting mission-critical workloads.

- By Deployment Mode, on-premises captures 62.5%, ensuring data sovereignty, air-gapped scanning, and integration with private OCI-compatible repositories like Harbor or JFrog Artifactory.

- By Organization Size, large enterprises hold 70.4%, managing enterprise-scale registry fleets with RBAC, secrets rotation, and SBOM generation across hybrid cloud environments.

- By End-User, BFSI leads at 45.8%, securing containerized trading platforms, core banking apps, and compliance workloads against supply chain attacks and zero-day exploits.

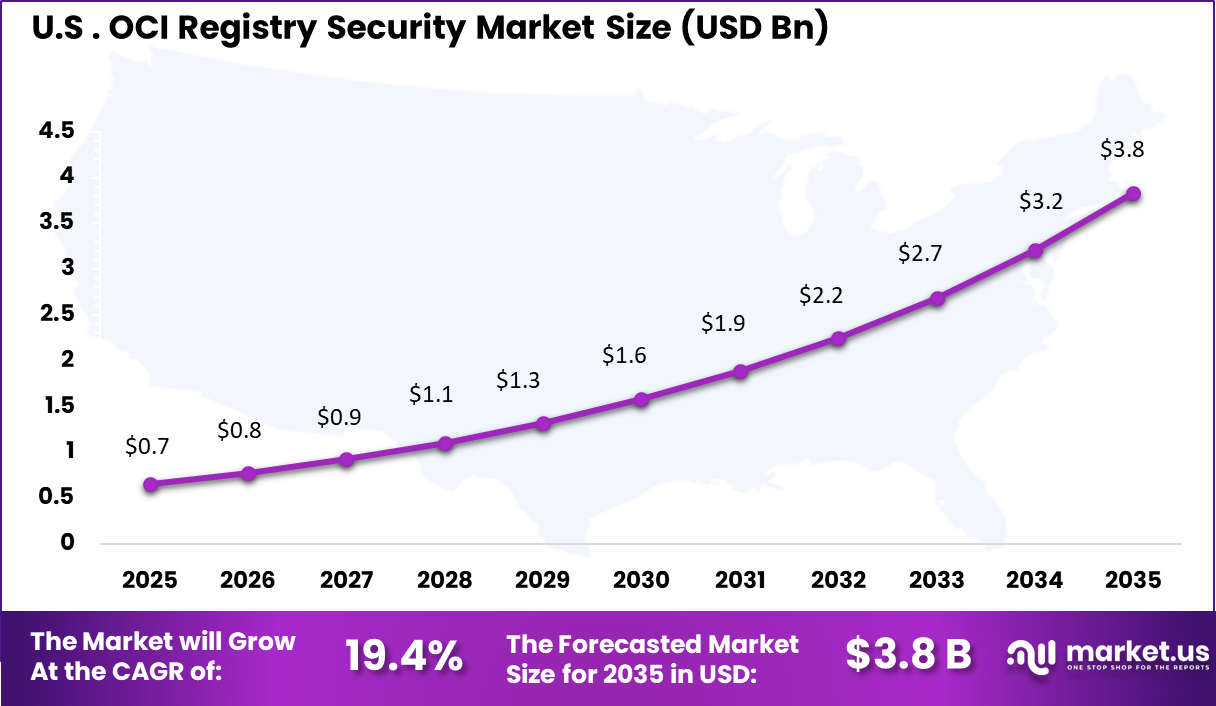

- Regionally, North America commands 39.5% global share, with the U.S. market at USD 0.65 billion and a CAGR of 19.4%, fueled by SEC regulations and Kubernetes adoption in financial services.

Drivers Impact Analysis

Key Drivers Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Strategic Importance Rising Adoption of Containers and Kubernetes +4.2% North America, Europe Short to Long Term Expands need for secure image registries Growing Focus on Software Supply Chain Security +3.8% Global Medium to Long Term Strengthens compliance and integrity controls Increase in DevSecOps Implementation +3.1% North America, APAC Medium Term Integrates security within CI/CD pipelines Regulatory Requirements for Application Security +2.4% North America, Europe Medium Term Drives mandatory vulnerability scanning Expansion of Multi-Cloud Environments +2.0% Global Long Term Requires centralized registry protection Restraints Impact Analysis

Key Restraints Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Market Constraint Level Complexity of Securing Dynamic Container Environments -2.5% Global Medium Term Requires specialized expertise Shortage of Cloud Security Professionals -2.1% Global Medium Term Slows optimized deployment High Integration Costs with Legacy Systems -1.7% Europe, APAC Short to Medium Term Budget limitations in traditional enterprises Tool Fragmentation Across DevOps Ecosystems -1.3% Global Medium Term Creates operational inefficiencies By Component

Software accounts for 73.6% of total adoption in the OCI Registry Security Market. This dominance reflects strong reliance on security platforms that scan, monitor, and protect container images stored in registries. Organizations prioritize software tools to detect vulnerabilities before deployment.

The preference for software solutions is also driven by the need for automated compliance checks. Continuous image scanning reduces the risk of introducing insecure code into production environments. This supports proactive threat management.

Software platforms further enable integration with DevOps pipelines. Security checks are embedded into development workflows to improve efficiency. These capabilities sustain the leadership of software within the component segment.

By Deployment Mode

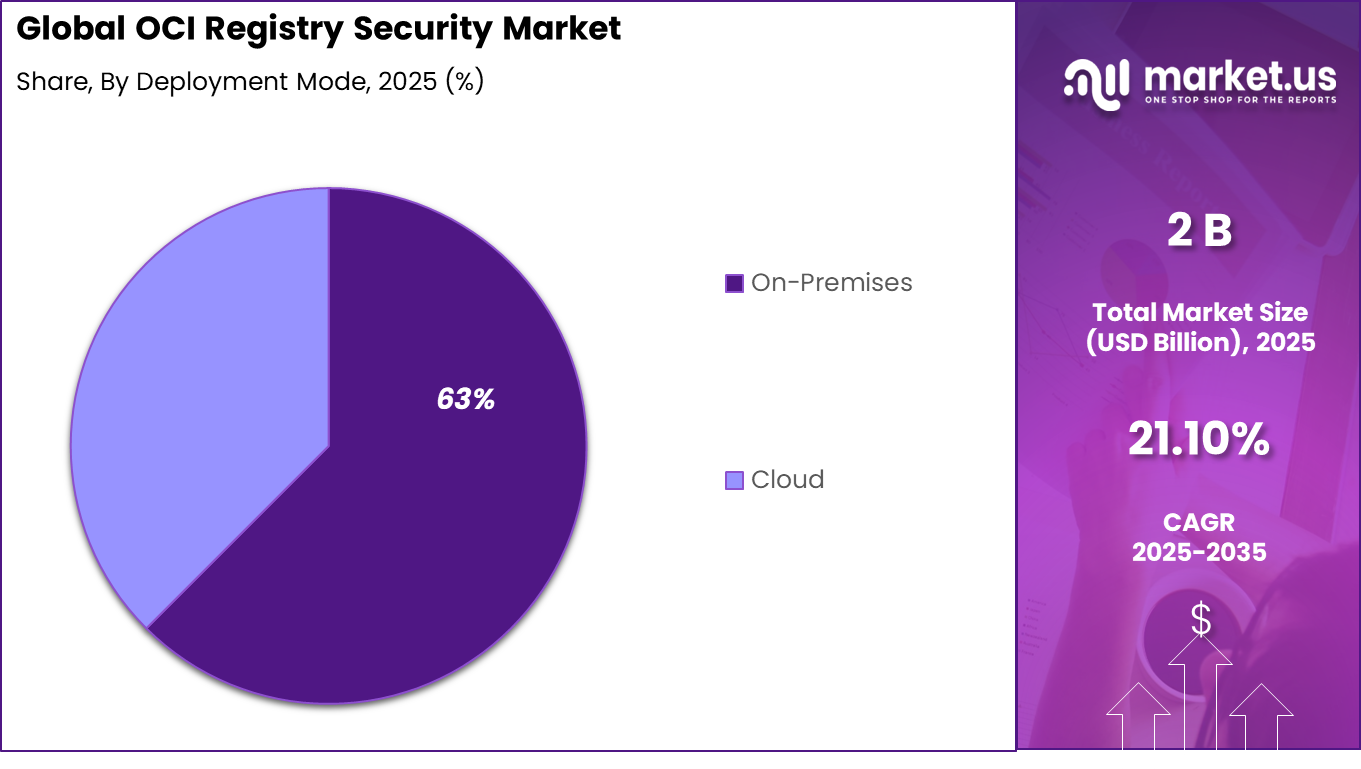

On premises deployment represents 63% of total adoption. This dominance reflects the need for direct control over sensitive container images and registry data. Organizations managing critical workloads prefer localized security infrastructure.

On premises systems also support strict internal governance policies. Data sovereignty and regulatory compliance requirements influence deployment decisions. This is particularly relevant for highly regulated industries.

Performance predictability is another factor supporting on premises deployment. Dedicated infrastructure ensures stable scanning and monitoring capabilities. These advantages reinforce its leading position in the deployment segment.

By Organization Size

Large enterprises account for 70.4% of total market demand by organization size. These organizations manage complex cloud native environments with extensive container usage. Registry security becomes critical as container volumes increase. The scale of enterprise operations increases exposure to security threats. Vulnerable container images can lead to operational disruption.

Advanced registry security platforms help mitigate this risk. Large enterprises also invest in structured security governance frameworks. Container security is integrated into broader cybersecurity strategies. This sustains strong adoption among large organizations.

By End User

The banking, financial services, and insurance sector accounts for 45.8% of total end user demand. This sector operates under strict regulatory oversight and requires high levels of system integrity. Secure container environments are essential for digital service delivery.

BFSI institutions prioritize vulnerability management and secure deployment pipelines. OCI registry security tools help maintain compliance and protect sensitive financial data. This drives consistent adoption within the sector.

The increasing digitization of financial services further amplifies the need for secure cloud native applications. Container based deployments are expanding. These dynamics maintain the BFSI sector’s leading share.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Venture Capital Very High High North America, Israel Strong interest in container security startups Private Equity High Medium North America, Europe Attractive recurring SaaS revenue models Strategic Cloud Providers Medium to High Low to Medium Global Focus on expanding cloud security portfolios Government & Sovereign Funds Medium Low North America National cybersecurity infrastructure priority Institutional Investors Medium Medium Developed Markets Long-term cloud infrastructure allocation Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Adoption Momentum AI-based Vulnerability Scanning +3.6% North America, Europe Short to Long Term Enhances real-time threat detection Image Signing and Integrity Verification Tools +2.9% Global Medium Term Strengthens supply chain validation Zero Trust Workload Security Models +2.5% North America Medium to Long Term Protects container runtime environments Automated Policy Enforcement in CI/CD +2.1% Global Medium Term Improves development lifecycle security Cloud-native Security Platforms +1.8% APAC, North America Long Term Enables scalable registry monitoring Emerging Trends

In the OCI Registry Security market, a clear trend is the adoption of automated scanning that checks container images as they are stored and retrieved. Organisations are increasingly building security checks into the registry itself so that vulnerabilities, misconfigurations, or policy violations are identified before images are used in production.

This helps teams act early and reduces uncertainty about what is being deployed. Another pattern emerging is the inclusion of simple, prioritised findings that help developers and operations staff understand which issues need attention first and why. This makes the security process feel more supportive and less like an obstacle.

Growth Factors

A key growth driver in this market is the rising reliance on containerised applications and micro services in everyday software delivery. As more teams package functions and services into images, the registry becomes a central point where security can be enforced consistently. Protecting this repository of assets helps ensure that only safe, compliant images make it into development pipelines and live environments.

Another important factor is the need to reduce friction between security and development teams. Developers value clear guidance that helps them fix issues quickly, and security teams need assurance that risks are managed without slowing delivery. Practices that make registry security transparent and actionable support both goals and encourage broader adoption within organisations.

Key Market Segments

By Component

- Software

- Services

By Deployment Mode

- On-Premises

- Cloud

By Organization Size

- Small And Medium Enterprises

- Large Enterprises

By End-User

- BFSI

- Healthcare

- IT And Telecommunications

- Retail

- Government

- Others

Regional Analysis

North America accounts for 39.5% of the OCI registry security market, supported by strong adoption of containerized applications and cloud-native development practices. Enterprises in the region are increasingly securing Open Container Initiative registries to prevent unauthorized image access, malware injection, and supply chain vulnerabilities. Demand is driven by rapid DevOps expansion, growing use of microservices architectures, and stricter governance requirements for software integrity across production environments.

The United States market is valued at USD 0.65 Bn and is expanding at a CAGR of 19.4%, reflecting accelerated deployment of container security frameworks. Adoption is influenced by increasing cybersecurity risks within CI/CD pipelines and rising need for automated vulnerability scanning and image validation. Growth is further supported by integration of registry security tools with cloud platforms and security operations workflows, enhancing software supply chain protection and regulatory compliance.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

Aqua Security and Sysdig maintain strong positions in OCI registry security through advanced image scanning and runtime protection capabilities. Palo Alto Networks with Prisma Cloud, supported by Twistlock integration, delivers unified container and registry security across hybrid and multi cloud environments. JFrog and Anchore strengthen software supply chain security by embedding vulnerability assessments into CI pipelines.

Snyk and Sonatype focus on developer centric security by identifying open source risks early in the build cycle, with strong emphasis on automation and policy based validation. Trend Micro and Qualys extend cloud workload protection into container registries through centralized risk management dashboards and continuous monitoring tools.

Red Hat with Quay and Harbor, as a CNCF backed project, support secure image storage and controlled distribution across Kubernetes clusters. Tenable and Rapid7 integrate registry vulnerability insights into broader exposure management frameworks. This strategy enables prioritized remediation and strengthens governance across complex hybrid infrastructures.

Microsoft with Azure Container Registry Security, Google with Artifact Registry Security, and Amazon Web Services with ECR Security embed registry protection directly within their cloud platforms. Docker enhances trusted image distribution through signing and built in scanning features. Black Duck under Synopsys and Checkmarx expand coverage through software composition analysis and code level risk detection.

Top Key Players in the Market

- Aqua Security

- Sysdig

- Palo Alto Networks (Prisma Cloud)

- JFrog

- Anchore

- Snyk

- Trend Micro

- Qualys

- Red Hat (Quay)

- Harbor (CNCF Project)

- Sonatype

- Tenable

- Rapid7

- Microsoft (Azure Container Registry Security)

- Google (Artifact Registry Security)

- Amazon Web Services (ECR Security)

- Twistlock (Acquired By Palo Alto Networks)

- Docker

- Black Duck (Synopsys)

- Checkmarx

- Others

Future Outlook

The future outlook for the OCI Registry Security Market is positive as organizations increasingly adopt containerized and cloud-native applications. Demand for OCI (Open Container Initiative) registry security solutions is expected to grow because these tools help protect container images from vulnerabilities and unauthorized access.

Adoption of automated scanning, real-time threat detection, and policy enforcement will improve security and compliance across development pipelines. Growth can be attributed to rising use of containers, stricter application security requirements, and the need for safer software deployment practices. Overall, the market is expected to expand as businesses prioritize secure and reliable container operations.

Recent Developments

- February 2025 – Sysdig launched Secure 4.0, adding AI-driven threat hunting tailored for container images in AWS ECR and Google Artifact Registry, which is a game-changer for multi-cloud setups.

- September 2025 – JFrog announced Artifactory 8.5 with built-in Snyk-powered security for Quay and Harbor users, streamlining compliance for DevOps pipelines in regulated industries.

Report Scope

Report Features Description Market Value (2025) USD 2 Billion Forecast Revenue (2035) USD 13.4 Billion CAGR(2025-2035) 21.10% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small And Medium Enterprises, Large Enterprises), By End-User (BFSI, Healthcare, IT And Telecommunications, Retail, Government, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Aqua Security, Sysdig, Palo Alto Networks (Prisma Cloud), JFrog, Anchore, Snyk, Trend Micro, Qualys, Red Hat (Quay), Harbor (CNCF Project), Sonatype, Tenable, Rapid7, Microsoft (Azure Container Registry Security), Google (Artifact Registry Security), Amazon Web Services (ECR Security), Twistlock (Acquired By Palo Alto Networks), Docker, Black Duck (Synopsys), Checkmarx, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  OCI Registry Security MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

OCI Registry Security MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Aqua Security

- Sysdig

- Palo Alto Networks (Prisma Cloud)

- JFrog

- Anchore

- Snyk

- Trend Micro

- Qualys

- Red Hat (Quay)

- Harbor (CNCF Project)

- Sonatype

- Tenable

- Rapid7

- Microsoft (Azure Container Registry Security)

- Google (Artifact Registry Security)

- Amazon Web Services (ECR Security)

- Twistlock (Acquired By Palo Alto Networks)

- Docker

- Black Duck (Synopsys)

- Checkmarx

- Others

Our Clients

- 179458

- Feb. 2026