Global Non-Slip Crawling Leggings Market Size, Share, Growth Analysis By Material (Cotton, Bamboo Fiber, Blended Fabrics, Others), By Age Group (Infants, Toddlers, Others), By Distribution Channel (Online Stores, Supermarkets/Hypermarkets, Specialty Stores, Others), By End-User (Unisex, Boys, Girls), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180401

- Number of Pages: 284

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

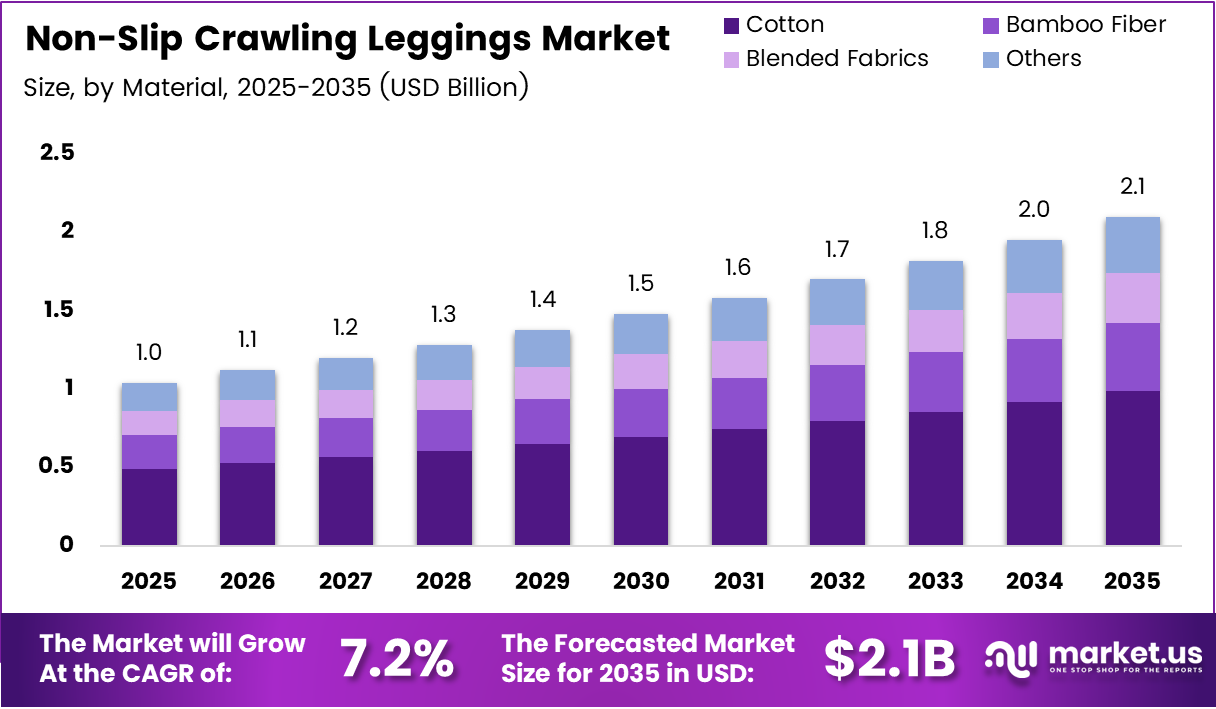

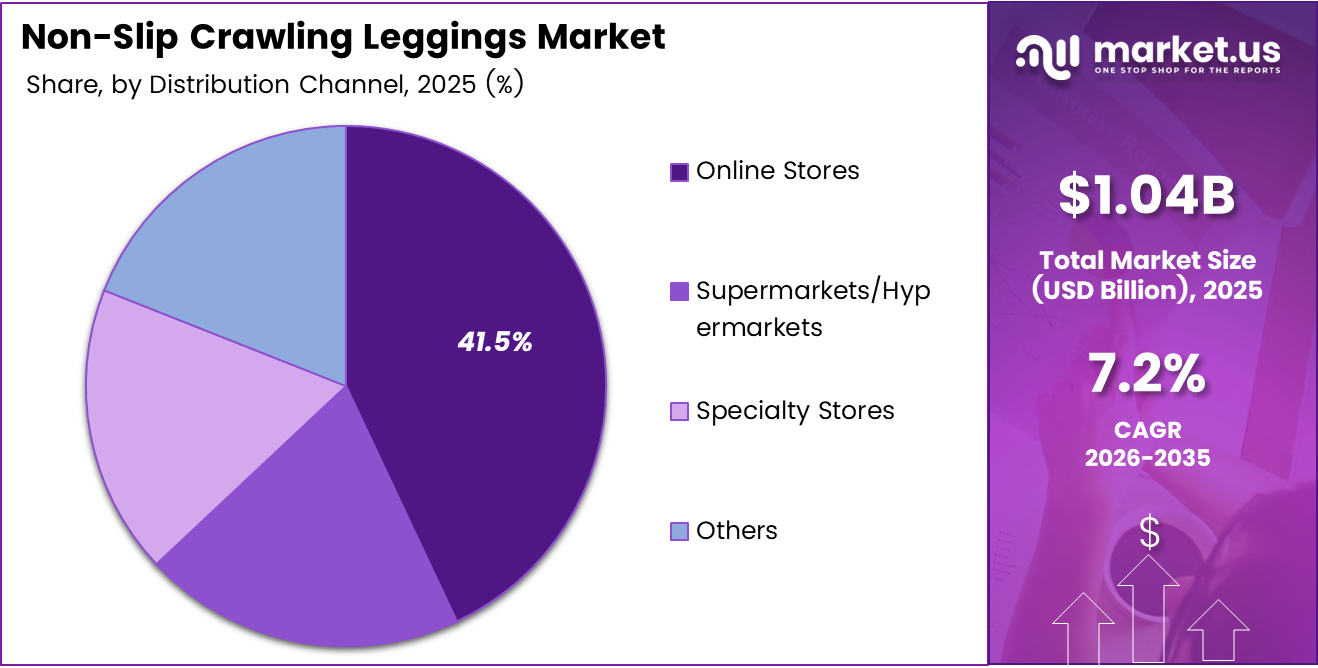

Global Non-Slip Crawling Leggings Market size is expected to be worth around USD 2.10 Billion by 2035 from USD 1.04 Billion in 2025, growing at a CAGR of 7.2% during the forecast period 2026 to 2035.

Non-slip crawling leggings are specialized infant apparel designed with grip technology — typically silicone-based knee and sole pads — that reduce slipping on smooth indoor surfaces. These garments serve a functional purpose beyond standard babywear, directly supporting infant mobility and reducing fall-related injuries during the crawling phase.

Parental awareness of early childhood motor development has reshaped how caregivers evaluate infant clothing. Buyers now prioritize garments that serve a developmental purpose, not merely a comfort or aesthetic one. This behavioral shift is translating into consistent purchase intent for safety-functional infant apparel categories, including anti-slip crawling leggings.

The market spans multiple material categories, including cotton, bamboo fiber, and blended fabrics, each targeting different buyer preferences around softness, sustainability, and durability. Cotton leads adoption due to its accessibility and widespread familiarity among parents. Meanwhile, bamboo fiber options are attracting eco-conscious buyers willing to pay a premium for skin-sensitive materials.

Online retail channels have become the primary access point for niche infant apparel brands. Parents researching developmental products turn to e-commerce platforms for variety, reviews, and convenience — conditions that strongly favor specialized brands that would otherwise struggle to reach buyers through traditional retail shelf space.

Government and pediatric advisory bodies across North America and Europe have reinforced the importance of supervised crawling environments for healthy infant motor development. This institutional emphasis adds credibility to product categories that support safer crawling — directly benefiting non-slip crawling leggings as a recommended companion product.

According to a longitudinal study published in PMC (PMC7443550), the mean age of crawling onset is approximately 272 days, with infants crawling for an average of 145 days before independent walking begins. This nearly five-month window of active crawling represents a defined and predictable usage period — giving brands a clear purchase-timing signal to target new parents at the right developmental milestone.

Key Takeaways

- The Global Non-Slip Crawling Leggings Market was valued at USD 1.04 Billion in 2025 and is forecast to reach USD 2.10 Billion by 2035.

- The market grows at a CAGR of 7.2% during the forecast period 2026 to 2035.

- By Material, Cotton leads with a 46.80% share due to widespread parental preference for soft, breathable infant fabric.

- By Age Group, Infants hold the dominant share at 52.70%, reflecting primary demand from parents of crawling-stage babies.

- By Distribution Channel, Online Stores account for 41.50% share, driven by parent research behavior and niche brand accessibility.

- By End-User, Unisex products dominate with a 52.30% share, reflecting practical purchasing preferences among caregivers.

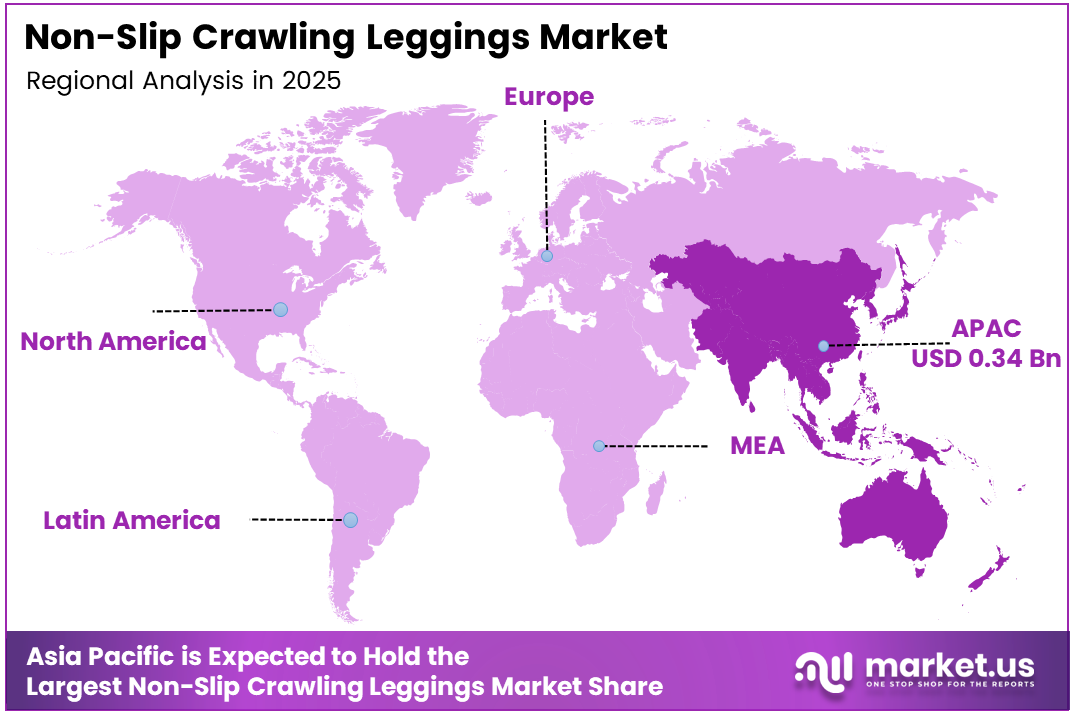

- Asia-Pacific leads regional markets with a 32.90% share, valued at USD 0.34 Billion.

Product Analysis

Cotton dominates with 46.80% due to trusted softness and broad parental familiarity.

In 2025, Cotton held a dominant market position in the By Material segment of the Non-Slip Crawling Leggings Market, with a 46.80% share. Cotton’s dominance reflects entrenched parental trust — caregivers default to cotton for infant skin contact because of its breathability, washability, and hypoallergenic properties. This familiarity lowers purchase hesitation and supports high repeat-buy rates.

Bamboo Fiber serves as the premium-tier alternative within the material segment. It targets eco-conscious and skin-sensitive infant care buyers who prioritize sustainable sourcing and thermoregulation. Bamboo fiber commands higher price points, making it a margin-rich opportunity for brands positioned in the natural or organic babywear space. However, its smaller buyer base limits mass-market scalability.

Blended Fabrics differentiate through performance-oriented construction. By combining cotton, spandex, or polyester blends, manufacturers achieve stretch, durability, and grip adhesion that pure cotton cannot match. These materials appeal to parents seeking functional performance over material purity, particularly for active crawlers on hard flooring surfaces where anti-slip technology must endure repeated use.

Others in the material category capture residual demand from specialty or emerging fabric technologies. These include modal, merino wool blends, or recycled fiber options entering the sustainable babywear space. Though small in volume, this segment signals early-stage innovation, particularly as sustainable manufacturing practices gain traction among infant apparel brands.

Age Group Analysis

Infants dominate with 52.70% due to peak crawling-stage demand and safety-focused parental buying.

In 2025, Infants held a dominant market position in the By Age Group segment of the Non-Slip Crawling Leggings Market, with a 52.70% share. Infant dominance is structurally logical — non-slip crawling leggings are designed specifically for the crawling developmental window, which occurs almost entirely within the infant age bracket. Parents purchase these products reactively, at the precise moment crawling begins.

Toddlers represent a secondary but meaningful segment within the age group category. As toddlers transition from crawling to early walking, parents continue purchasing grip-functional legwear for fall prevention on slippery surfaces. This use-case extension — from crawling support to walking stability — broadens the product’s relevance beyond its core infant application and supports longer purchase cycles per child.

Others in the age category include older children with specific developmental needs or physical therapy requirements. This sub-segment is niche but clinically relevant. Pediatric occupational therapists sometimes recommend grip-functional clothing for children with motor coordination challenges, creating a prescription-adjacent demand channel that operates outside standard retail purchasing behavior.

Distribution Channel Analysis

Online Stores dominate with 41.50% due to parental research behavior and niche brand access.

In 2025, Online Stores held a dominant market position in the By Distribution Channel segment of the Non-Slip Crawling Leggings Market, with a 41.50% share. Parents discovering developmental products typically research online before purchasing. E-commerce platforms allow specialized brands to reach buyers who would never encounter these products in physical retail, making online the natural primary channel for a niche, function-specific category.

Supermarkets and Hypermarkets carry the highest foot traffic but lower category specificity. These channels stock standard infant apparel, and non-slip crawling leggings compete for limited shelf space against conventional baby clothing. However, parent impulse purchases during broader baby shopping trips give this channel a complementary role — particularly for established brands with strong retail distribution agreements.

Specialty Stores serve an important trust-building function in this market. Baby boutiques and dedicated infant gear retailers attract high-intent parents who are actively seeking quality developmental products. These stores often carry premium and organic-certified lines, making them a disproportionately valuable channel for brands positioned above the mass-market tier.

Others within the distribution category include pharmacy chains, pediatric clinic gift shops, and direct-to-consumer brand websites. These channels operate at lower volume but often reach highly motivated buyers — parents who have received direct medical or developmental guidance and are seeking specific product solutions rather than browsing general infant apparel.

End-User Analysis

Unisex dominates with 52.30% due to practical parenting behavior and gifting convenience.

In 2025, Unisex held a dominant market position in the By End-User segment of the Non-Slip Crawling Leggings Market, with a 52.30% share. Unisex dominance reflects practical purchasing logic — parents and gift-buyers prefer gender-neutral products for their versatility across children and reuse potential. For a functional product category where safety performance matters more than aesthetics, unisex positioning removes a purchase barrier rather than limiting appeal.

Boys-specific non-slip crawling leggings occupy a secondary position, typically differentiated by color, print, or character-based designs. This sub-segment appeals to parents who prefer gender-coded apparel and are willing to pay for category-specific aesthetics alongside functional grip features. However, boys-specific SKUs require broader inventory management, which constrains smaller brand operators.

Girls-specific products follow a similar pattern, with differentiation through pastel tones, floral prints, and style-forward designs that combine safety function with fashion appeal. This segment benefits from the aesthetic-conscious gifting behavior common in infant apparel — grandparents and extended family members represent a significant buyer cohort for gender-coded infant clothing purchases.

Key Market Segments

By Material

- Cotton

- Bamboo Fiber

- Blended Fabrics

- Others

By Age Group

- Infants

- Toddlers

- Others

By Distribution Channel

- Online Stores

- Supermarkets/Hypermarkets

- Specialty Stores

- Others

By End-User

- Unisex

- Boys

- Girls

Drivers

Parental Safety Awareness and Grip Technology Adoption Drive Non-Slip Crawling Leggings Demand

Parents increasingly evaluate infant apparel by functional safety criteria, not just comfort or price. Rising awareness of injury risks on smooth indoor surfaces has pushed caregivers toward products that actively reduce slip-related falls. Non-slip crawling leggings address this need directly, moving them from a niche item into a considered safety purchase for first-time parents.

According to a population-based cohort study published in PMC (PMC8841506), the mean crawling onset occurs at 8.1 months across 8,395 children. This predictable developmental milestone gives brands a clear targeting window. Marketers and pediatric retailers who align messaging with this specific age threshold can intercept parents precisely when purchase motivation peaks — before crawling begins and slip risks become visible.

Premium babywear brands have recognized this demand signal and now offer specialized mobility-enhancing infant clothing lines. Expansion into grip-functional apparel by established childrenswear players validates the segment and accelerates mainstream adoption. Additionally, pediatric development awareness campaigns reinforce that movement-friendly clothing directly supports healthy motor progression, giving non-slip leggings a credibility advantage over generic infant legwear.

Restraints

Higher Product Costs and Limited Awareness in Price-Sensitive Markets Slow Category Penetration

Non-slip crawling leggings carry a price premium over conventional baby leggings due to grip technology application, specialized fabric selection, and safety certification requirements. In price-sensitive markets — particularly across Southeast Asia, Latin America, and emerging economies — this cost gap is significant enough to redirect purchasing toward standard infant legwear, limiting the addressable market for functional babywear brands.

Product awareness remains low in traditional infant clothing markets where parental purchasing decisions center on price and fabric softness rather than developmental function. Parents unfamiliar with the concept of grip-functional apparel have no purchase trigger — and without that awareness, even well-priced products face low conversion. This awareness gap is particularly acute in markets where pediatric developmental guidance is less accessible to average consumers.

The combination of cost barrier and awareness deficit creates a compound challenge. Brands must invest simultaneously in consumer education and price accessibility — a resource-intensive strategy that works against smaller operators. Consequently, market penetration in underdeveloped infant apparel regions will remain slower unless brands or distributors actively invest in awareness-building alongside competitive pricing strategies.

Growth Factors

Product Innovation, E-Commerce Access, and Pediatric Collaboration Expand the Non-Slip Crawling Leggings Market

Silicone grip pattern improvements, breathable organic fabric integration, and knee protection padding represent active product development directions that extend non-slip leggings beyond basic anti-slip function. Brands that combine multiple protection features in one garment — comfort, grip, and knee cushioning — command higher price points and reduce parental need to purchase separate protective accessories for crawling infants.

According to a study published on ScienceDaily, infants begin crawling at approximately 31 weeks (~7.7 months) on average. This early onset means parents must source non-slip crawling products before or during the early infant months — a timing that e-commerce channels serve effectively. Online platforms enable global access to niche infant mobility brands that traditional brick-and-mortar retail cannot accommodate, unlocking cross-border demand for specialized products.

Collaboration between pediatric development experts and babywear brands creates a clinically endorsed distribution pathway. When pediatricians or occupational therapists recommend grip-functional clothing as part of healthy motor development guidance, it generates pull-through demand that bypasses standard retail discovery. This professional endorsement channel is especially valuable in markets where parental purchasing decisions follow medical advice closely.

Emerging Trends

Sustainable Fabrics, Social Media Influence, and Aesthetic Design Reshape Infant Crawling Apparel Preferences

Organic cotton and skin-sensitive materials are displacing standard synthetic blends in infant crawling apparel as parents apply stricter ingredient standards to products in direct skin contact. Brands adopting certified organic cotton or bamboo fiber formulations are capturing a premium buyer segment that previously had limited product choices. This materials shift is also aligned with broader sustainable manufacturing adoption across the infant apparel sector.

According to a study from PMC (PMC8841506), each one-month delay in crawling onset increases the risk of motor impairment by approximately 5.3%. Social media parenting communities and influencer-driven content increasingly reference this type of developmental research when recommending safety-functional babywear. This amplification effect converts clinical data into purchase motivation, connecting pediatric research directly to consumer buying decisions through digital channels.

Stylish and aesthetic babywear designs that embed safety features are reshaping category expectations. Parents no longer accept a tradeoff between function and appearance — they expect non-slip leggings to look appealing in social media posts and family photos. This aesthetic-function convergence is driving product development toward fashion-forward grip apparel, allowing brands to compete on design differentiation rather than safety features alone.

Regional Analysis

Asia-Pacific Dominates the Non-Slip Crawling Leggings Market with a Market Share of 32.90%, Valued at USD 0.34 Billion

Asia-Pacific holds a 32.90% share of the global non-slip crawling leggings market, valued at USD 0.34 Billion. The region’s dominance reflects its large infant population base, a rising middle class with increasing per-infant spending, and the rapid expansion of e-commerce infrastructure that connects parents to functional babywear brands. China, India, and Japan contribute the largest share within the region.

North America Non-Slip Crawling Leggings Market Trends

North America represents a mature, high-spending infant apparel market where parental awareness of developmental products is well-established. Strong pediatric advisory networks and a well-developed e-commerce ecosystem accelerate category adoption. Premium product positioning finds receptive buyers here, and established childrenswear brands with grip-functional lines benefit from existing consumer trust and retail distribution depth.

Europe Non-Slip Crawling Leggings Market Trends

Europe’s market benefits from stringent children’s product safety regulations that validate the functional positioning of non-slip crawling leggings. Regulatory compliance requirements raise the entry bar for standard infant apparel producers, giving certified functional brands a structural advantage. Western European markets, particularly Germany and the UK, lead adoption, supported by parental preference for premium and sustainably produced infant apparel.

Latin America Non-Slip Crawling Leggings Market Trends

Latin America presents a developing demand profile constrained by price sensitivity and uneven awareness of developmental infant apparel. Brazil and Mexico represent the largest country-level opportunities, where urban middle-class parenting behaviors are increasingly aligning with North American and European trends. E-commerce penetration growth in these countries provides the access infrastructure needed to reach informed buyers beyond major retail centers.

Middle East and Africa Non-Slip Crawling Leggings Market Trends

The Middle East and Africa market remains at an early penetration stage for functional infant crawling apparel. GCC countries, particularly the UAE and Saudi Arabia, show the strongest near-term potential due to high per-capita infant spending and a growing premium retail environment. However, across broader Africa, limited distribution infrastructure and product awareness constrain category growth beyond urban centers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Carter’s Inc. holds one of the most defensible positions in infant apparel through its unmatched retail distribution across department stores, specialty retailers, and its own branded channels. Its scale allows it to introduce grip-functional product lines without the customer acquisition costs that smaller brands face. However, Carter’s broad positioning also means it competes on volume rather than developmental specialization — a gap that niche operators actively target.

Babysoy Inc. differentiates through its commitment to soy-based and organic fabrics, positioning itself at the intersection of skin-safety and environmental responsibility. In the non-slip crawling leggings segment, this materials-first approach resonates strongly with eco-conscious parents who apply the same ingredient scrutiny to baby clothing as to food. Its focused product philosophy allows premium pricing and strong retention among its buyer cohort.

Hanna Andersson builds its market position on Scandinavian-inspired quality, durability, and organic cotton certification. The brand targets higher-income parents who view infant apparel as an investment rather than a commodity. Its grip-functional offerings benefit from a loyal, brand-trusting customer base. Consequently, Hanna Andersson faces lower price sensitivity among its buyers compared to mass-market competitors, giving it structural margin protection.

Gerber Childrenswear LLC operates with the trust advantage of one of the most recognized names in infant care globally. Its extensive product range means grip-functional leggings can be cross-sold to parents already purchasing within the brand ecosystem. Gerber’s broad retail presence — spanning grocery, mass-market, and online channels — gives its non-slip crawling products scale accessibility that premium niche brands cannot replicate.

Key Players

- Carter’s Inc.

- Babysoy Inc.

- Hanna Andersson

- Gerber Childrenswear LLC

- Burt’s Bees Baby

- Zara Kids

- H&M Kids

- Nike Kids

- Adidas Kids

- Old Navy (Gap Inc.)

- Target Corporation (Cat & Jack)

- Mothercare plc

- Next plc

- The Children’s Place

- Gymboree

- Hudson Baby

- Luvable Friends

- JoJo Maman Bébé

- PatPat

- Other Key Players

Recent Developments

- September 2024 – Grip Baby launched a patent-pending crawling support onesie featuring strategically placed silicone grips designed to help infants gain traction on slippery indoor surfaces. This product introduction marks one of the first patent-level innovations specifically targeting the infant anti-slip mobility apparel segment.

Report Scope

Report Features Description Market Value (2025) USD 1.04 Billion Forecast Revenue (2035) USD 2.10 Billion CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Cotton, Bamboo Fiber, Blended Fabrics, Others), By Age Group (Infants, Toddlers, Others), By Distribution Channel (Online Stores, Supermarkets/Hypermarkets, Specialty Stores, Others), By End-User (Unisex, Boys, Girls) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Carter’s Inc., Babysoy Inc., Hanna Andersson, Gerber Childrenswear LLC, Burt’s Bees Baby, Zara Kids, H&M Kids, Nike Kids, Adidas Kids, Old Navy (Gap Inc.), Target Corporation (Cat & Jack), Mothercare plc, Next plc, The Children’s Place, Gymboree, Hudson Baby, Luvable Friends, JoJo Maman Bébé, PatPat, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Non-Slip Crawling Leggings MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Non-Slip Crawling Leggings MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Carter's Inc.

- Babysoy Inc.

- Hanna Andersson

- Gerber Childrenswear LLC

- Burt's Bees Baby

- Zara Kids

- H&M Kids

- Nike Kids

- Adidas Kids

- Old Navy (Gap Inc.)

- Target Corporation (Cat & Jack)

- Mothercare plc

- Next plc

- The Children's Place

- Gymboree

- Hudson Baby

- Luvable Friends

- JoJo Maman Bébé

- PatPat

- Other Key Players

Our Clients

- 180401

- Mar 2026