Global Multi-Cloud Data Management Market Size, Share and Analysis Report By Component (Software/Solutions, Services), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Application (Data Integration and Migration, Backup and Recovery, Security and Compliance, Disaster Recovery, Data Governance, Data Orchestration, Others), By End-User Industry (Banking, Financial Services, and Insurance, Healthcare, IT and Telecommunications, Retail and E-commerce, Manufacturing, Government, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178108

- Number of Pages: 285

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key Insights

- By Component

- By Deployment Mode

- By Organization Size

- By Application

- By End-User Industry

- Regional Overview

- Emerging Trend Analysis

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Market Segments

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

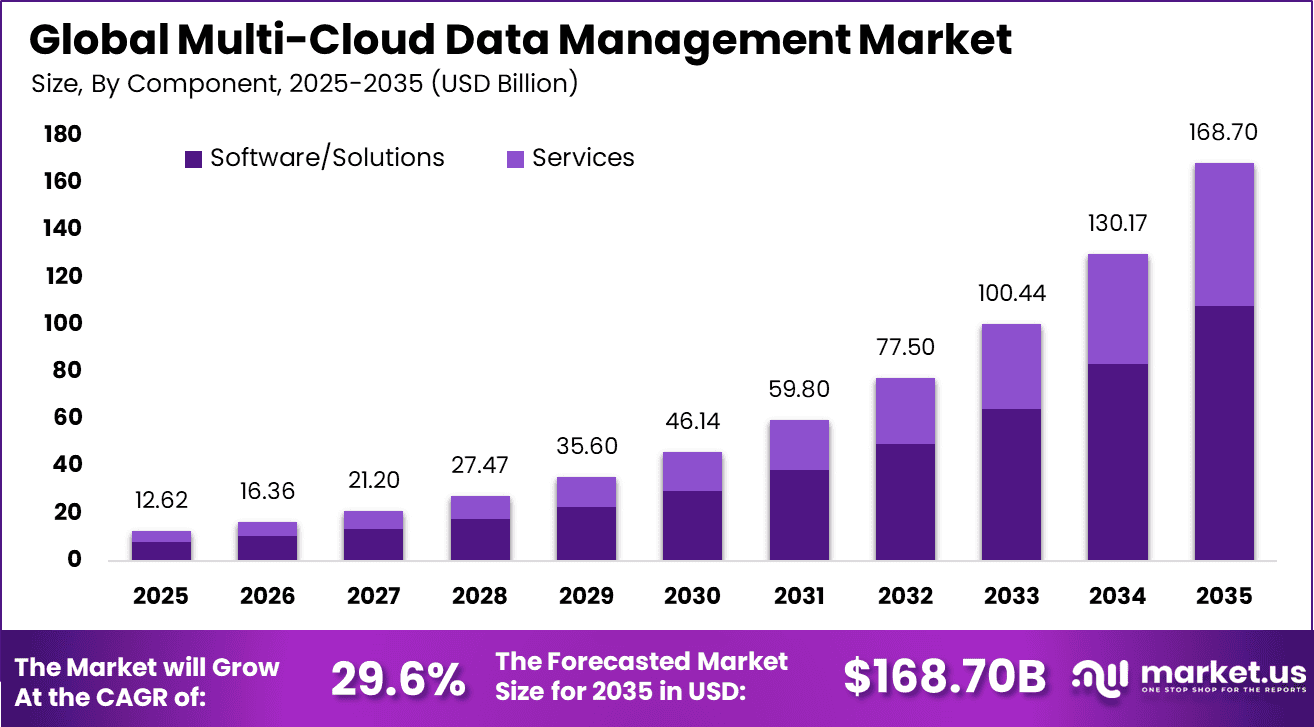

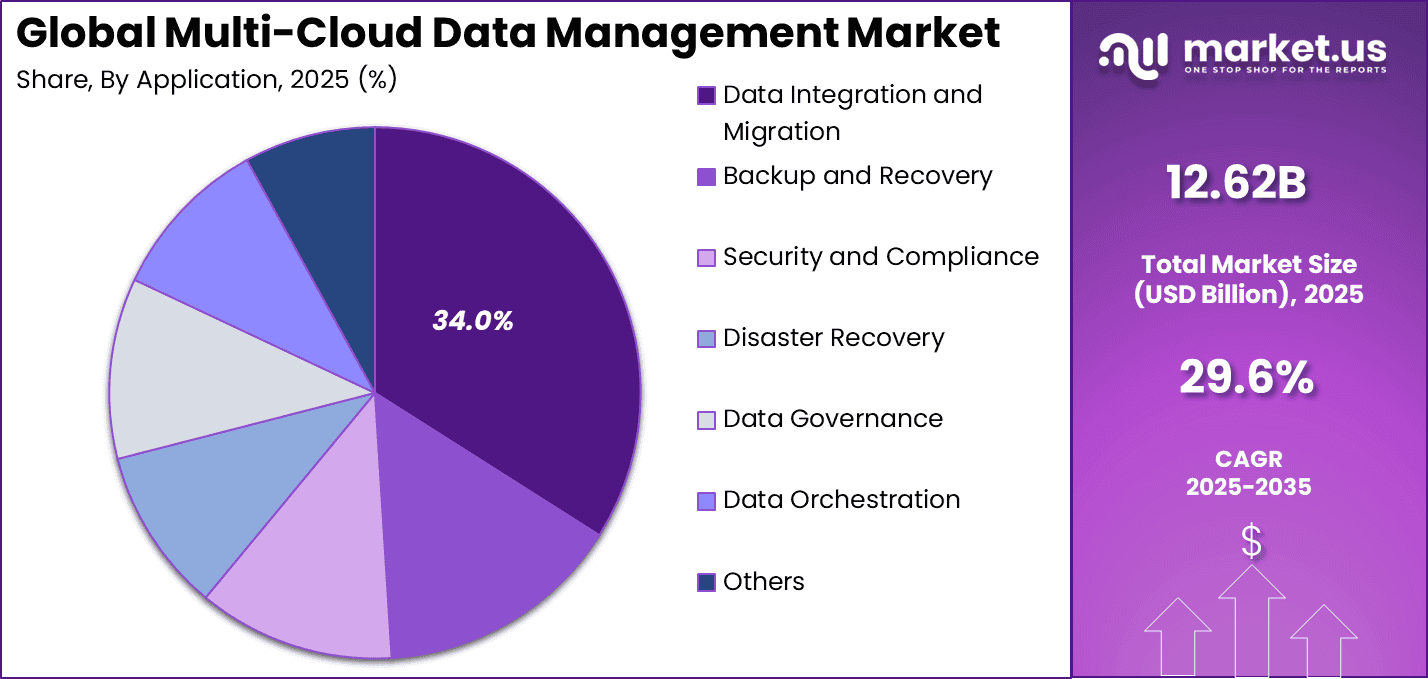

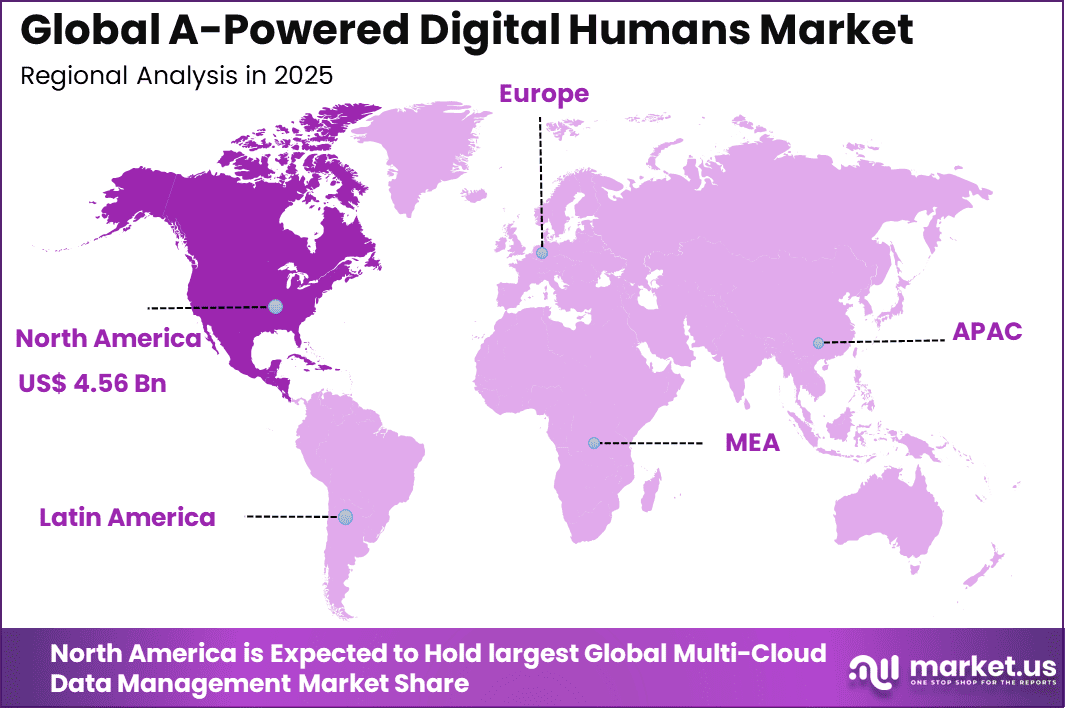

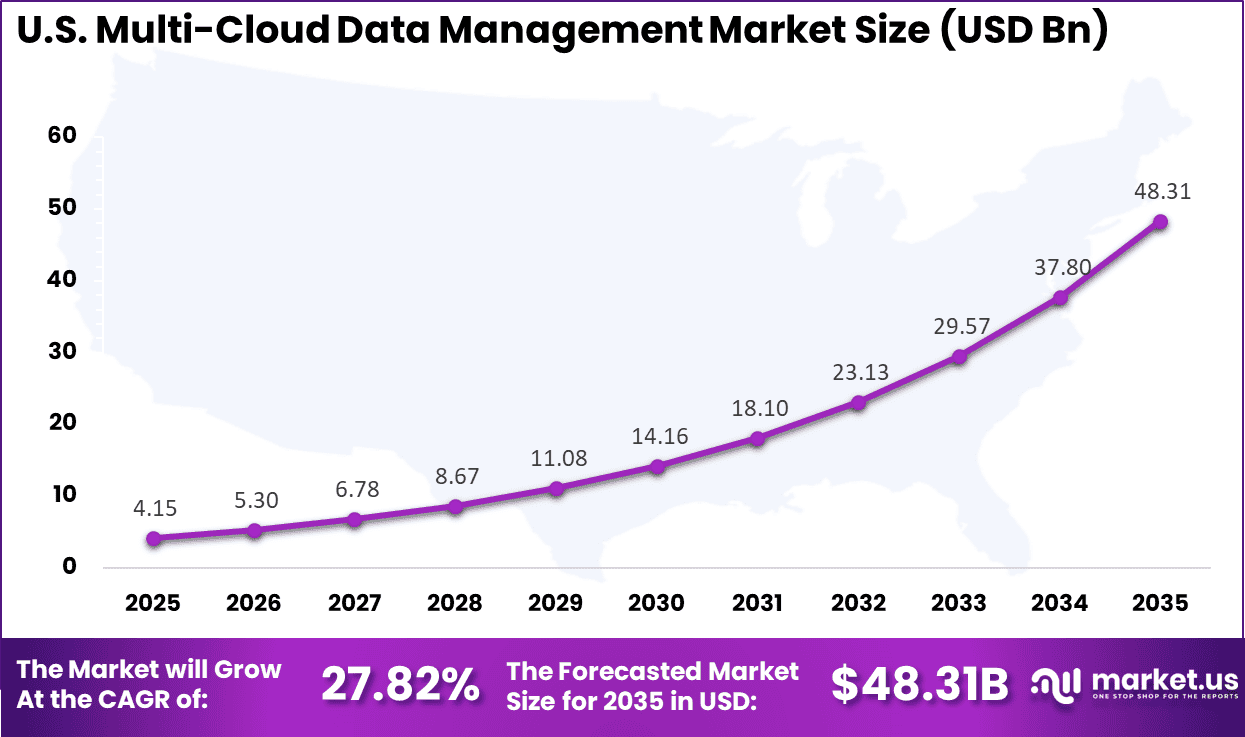

The Global Multi-Cloud Data Management Market size is expected to be worth around USD 168.70 billion by 2035, from USD 12.62 billion in 2025, growing at a CAGR of 29.6% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 36.15% share, holding USD 4.56 billion in revenue.

The multi-cloud data management market refers to the set of technologies and practices used to govern, store, and move data across more than one cloud environment. It has emerged in response to enterprise strategies that distribute workloads among cloud service providers to reduce risk and improve flexibility. This market encompasses tools that ensure consistent data access, security, and compliance across disparate cloud platforms.

Reliable data management is essential for organizations that depend on data availability and performance to support operations. Enterprises are increasingly adopting multi-cloud strategies to avoid vendor lock-in and to optimize cost and performance. These approaches require coherent data management frameworks to prevent fragmentation and data silos. The market includes solutions for data integration, replication, cataloging, and governance to maintain data integrity.

The scope of this market spans public, private, and hybrid cloud environments where data mobility and interoperability are critical. Organizations seek to harmonize data policies across platforms to reduce risk and ensure regulatory adherence. Multi-cloud data management supports analytics and operational workloads with consistent governance practices. The market is shaped by enterprise needs for unified visibility and control over distributed data assets.

One key factor driving the multi-cloud data management market is the rapid growth in enterprise data volumes. Organizations generate and capture data at unprecedented rates, creating complexity in how data is stored and accessed across multiple cloud platforms. Effective management ensures that data remains consistent and reliable regardless of its location. Without proper controls, data fragmentation can lead to inefficiencies and operational risk.

Demand for multi-cloud data management solutions is gaining momentum among large enterprises and growing midsize firms. Organizations that rely on advanced analytics, artificial intelligence, and digital services require dependable data management to fuel decision making. These solutions help reduce operational risk while improving data accessibility and quality. Ensuring that data flows seamlessly across platforms is increasingly viewed as a competitive necessity.

For instance, in November 2025, SAP announced SAP-owned datacenters for Business Technology Platform starting mid-2025, expanding a multi-cloud foundation alongside hyperscalers. This hybrid strategy helps SAP clients standardize services while maintaining flexibility across clouds.

Key Takeaway

- The Software and Solutions segment accounted for 64.0% of the total market share. Growth has been supported by increasing demand for centralized control platforms, orchestration tools, and cross-cloud analytics capabilities.

- Hybrid Cloud led with 48.0% share, reflecting enterprise preference for combining public and private environments to ensure flexibility, compliance control, and optimized workload distribution.

- Large Enterprises captured 71.0% of total demand. Higher data volumes, regulatory obligations, and multi-region operations have driven greater adoption among large-scale organizations.

- Data Integration and Migration represented 34.0% of the market. The need to transfer, synchronize, and consolidate data across multiple cloud platforms remains a core operational requirement.

- Banking, Financial Services, and Insurance accounted for 32.0% of overall market revenue. Strong regulatory compliance mandates, cybersecurity requirements, and digital banking expansion have accelerated adoption within this sector.

- North America held 36.15% of the global market share, supported by mature cloud ecosystems and strong enterprise cloud investments.

- The United States market reached USD 4.15 Billion, expanding at a CAGR of 27.82%, driven by rapid digital transformation, fintech innovation, and large-scale cloud migration initiatives.

Key Insights

- Multi-cloud and hybrid cloud adoption has reached between 89% and 98% of organizations globally, indicating that distributed cloud strategies are now standard practice.

- Around 76% of enterprises operate with at least two cloud providers, while 69% use three or more, reflecting growing infrastructure diversification.

- Nearly 31% of enterprises rely on four or more cloud providers, which increases architectural complexity and governance requirements.

- Hybrid cloud models are used by approximately 80% of organizations, combining public and private cloud environments to balance scalability and control.

- By 2024, enterprises planned to allocate nearly 80% of total IT budgets to cloud-related expenditures, underscoring the strategic priority of cloud infrastructure.

- Avoidance of vendor lock-in remains the primary driver, contributing an estimated +8.5% incremental growth impact on multi-cloud adoption.

- Disaster recovery strategies contribute approximately +6.2% to growth, as organizations prioritize business continuity and resilience.

- Data residency and regulatory compliance requirements continue to accelerate multi-cloud deployment, particularly in highly regulated sectors.

- Approximately 32% of enterprise cloud budgets are lost due to overprovisioned or idle resources, highlighting inefficiencies in cost governance.

- About 80% of organizations report visibility gaps across their cloud environments, limiting real-time operational insight.

- Nearly 63% of IT leaders manually correlate data from five or more management tools, increasing operational burden and slowing incident response.

- Cloud misconfigurations account for 62% of security incidents, demonstrating weaknesses in configuration management and policy enforcement.

- In broader cloud environments, misconfigurations contribute to as much as 99% of security failures, particularly in complex multi-cloud architectures.

- The average cost of a data breach reached USD 4.88 million in 2024, reinforcing the financial risk associated with inadequate cloud governance and monitoring.

By Component

Software and solutions account for 64.0% of the multi-cloud data management market. This dominance reflects the growing need for centralized platforms that can manage, orchestrate, and secure data across multiple cloud environments. As enterprises increasingly adopt more than one cloud provider, the complexity of data movement, synchronization, and governance has increased significantly.

Software tools provide unified dashboards, automation capabilities, and policy enforcement mechanisms. These features enable organizations to maintain visibility and control over distributed data assets. Multi-cloud software platforms also support workload portability and seamless data replication between environments.

This reduces vendor dependency and enhances operational flexibility. Advanced solutions incorporate encryption, access management, and compliance tracking to address regulatory requirements. Automation within these tools minimizes manual intervention and reduces operational risk. As a result, software solutions remain the core revenue contributor within this segment.

For Instance, in October 2025, IBM Corporation teamed up with Google Cloud to advance multi-cloud software for transformations. The partnership focuses on secure data tools and migrations, helping enterprises unify workloads with strong analytics software. It highlights software’s role in making multi-cloud reliable for daily operations.

By Deployment Mode

Hybrid cloud deployment holds 48.0% of the market share, indicating strong enterprise preference for combining private and public cloud environments. Organizations adopt hybrid strategies to balance scalability with data control and security. Sensitive workloads are often retained in private infrastructure, while scalable analytics and applications are deployed in public clouds.

Multi-cloud data management solutions ensure consistent data governance across these environments. This integration helps maintain performance and compliance standards. Hybrid models also provide business continuity and disaster recovery advantages.

Data can be replicated across private and public systems to ensure availability during outages. Enterprises benefit from flexible workload distribution based on cost and performance requirements. Monitoring and orchestration tools play a key role in maintaining synchronization between cloud environments. This balanced approach explains the strong position of hybrid deployment within the market.

For instance, in September 2024, Microsoft Corporation expanded Oracle Database@Azure in more regions. Running OCI directly in Azure data centers supports hybrid cloud data management, linking enterprise databases seamlessly. Users gain low-latency access, ideal for hybrid strategies balancing security and agility.

By Organization Size

Large enterprises represent 71.0% of total adoption in the multi-cloud data management market. These organizations operate across multiple regions and business units, generating large volumes of operational and customer data. Managing data across various cloud platforms requires structured governance and standardized processes. Multi-cloud management platforms provide centralized oversight and policy enforcement. This ensures data consistency and regulatory alignment across global operations.

Enterprises also prioritize performance optimization and cost efficiency across cloud providers. Multi-cloud strategies allow them to allocate workloads based on pricing structures and service capabilities. Advanced analytics, artificial intelligence, and real-time processing further increase the need for integrated data management. Automated orchestration reduces operational complexity and enhances decision support systems. The scale and technical maturity of large enterprises contribute to their dominant share.

For Instance, in February 2026, Dell Technologies Inc. advanced hybrid solutions for enterprises through partnerships. Their tools integrate with multi-cloud for large ops, focusing on resilient data handling. It aids big companies in optimizing costs and performance in complex environments.

By Application

Data integration and migration account for 34.0% of total market share. As organizations modernize legacy systems, seamless data transfer between on-premises infrastructure and multiple clouds becomes essential. Integration tools ensure that data remains consistent and synchronized across platforms. This supports unified analytics, reporting accuracy, and operational continuity. Effective migration reduces downtime and prevents data loss during system transitions.

Enterprises also rely on integration tools to connect diverse applications and databases across environments. Automated pipelines streamline real-time data movement and reduce manual workload. These capabilities are critical when consolidating data for analytics or regulatory reporting. Migration strategies are often aligned with digital transformation initiatives and cloud modernization plans. The increasing pace of infrastructure upgrades supports steady demand within this segment.

For Instance, in October 2025, SAP SE deepened ties with IBM for cloud migrations, including data integration. Leveraging IBM Power for RISE with SAP, it speeds S/4HANA shifts with seamless data flows. This eases integration across hybrid clouds for enterprises updating systems.

By End-User Industry

The Banking, Financial Services, and Insurance sector holds 32.0% of the multi-cloud data management market. Financial institutions manage complex data ecosystems that include transaction records, risk assessments, compliance reports, and customer information. Multi-cloud strategies enable these organizations to distribute workloads while maintaining high security standards.

Data management platforms ensure encryption, access control, and audit traceability. This supports compliance with strict financial regulations. Financial institutions also require real-time analytics for fraud detection, credit risk modeling, and customer engagement. Multi-cloud management ensures seamless data availability across analytics platforms.

Redundancy across cloud providers enhances resilience and minimizes service disruption risks. Structured governance frameworks help maintain transparency and regulatory alignment. These operational requirements explain the strong adoption within this industry segment.

For Instance, in November 2025, Amazon Web Services Inc. boosted multi-cloud for BFSI with secure data tools. New features aid banks in compliant integrations across clouds, enhancing fraud detection. It supports financial firms scaling data ops while meeting regs.

Regional Overview

North America accounts for 36.15% of the global multi-cloud data management market. The region demonstrates advanced cloud adoption and strong enterprise digital transformation initiatives. Organizations prioritize workload flexibility, cybersecurity, and compliance readiness. Multi-cloud strategies are increasingly integrated into long-term IT modernization plans. This drives sustained demand for centralized data orchestration platforms.

For instance, in December 2025, AWS and Google Cloud launched a jointly engineered multi-cloud networking solution using AWS Interconnect-multicloud and Google Cross-Cloud Interconnect, enabling private high-speed connectivity between VPCs. This collaboration simplifies data transfer and operations across clouds, showcasing North American hyperscalers’ dominance in multi-cloud infrastructure.

The United States remains the primary growth engine within the region, supported by a market value of USD 4.15 Bn and a CAGR of 27.82%. Enterprises in the US are accelerating cloud migration across financial services, healthcare, retail, and technology sectors. Investment in data governance and hybrid infrastructure continues to expand. Strong innovation capacity and regulatory oversight further reinforce market growth. North America is expected to remain a leading region for multi-cloud data management adoption.

For instance, in January 2026, Google Cloud introduced fully-managed Model Context Protocol (MCP) servers and expanded MCP support for Google Services, including BigQuery, Maps, Compute Engine, and GKE, enabling seamless multi-cloud data access and AI agent integration. This innovation provides enterprise-ready governance and security, reinforcing U.S. leadership in multi-cloud data management.

Emerging Trend Analysis

One emerging trend in multi-cloud data management is the increasing adoption of unified orchestration and automation frameworks that simplify the coordination of data workflows across heterogeneous cloud environments. Organizations are advancing from siloed cloud operations toward integrated platforms that automate provisioning, governance, and optimization processes at scale. This shift is enabling more consistent management of data lifecycles, reducing manual tasks, and improving the reliability of distributed cloud operations.

In parallel, intelligent analytics and artificial intelligence are being embedded into management solutions to predict performance bottlenecks, identify compliance deviations, and support data governance decisions. These capabilities provide dynamic insights that help ensure data reliability and security in complex multi-cloud infrastructures. The incorporation of predictive analytics is also supporting enhanced cost optimization by forecasting usage patterns and suggesting resource adjustments.

Driver Analysis

A significant driver of multi-cloud data management adoption is the pursuit of operational flexibility and avoidance of dependency on a single cloud service provider. Many organizations are strategically deploying workloads across multiple cloud environments to optimize performance, leverage best-of-breed services, and reduce vendor lock-in risks.

This approach enables enterprises to align workload placement with performance requirements and organizational policies while maintaining negotiation leverage with providers. Such flexibility supports broader digital transformation efforts, making multi-cloud data management solutions a core component of enterprise IT strategy.

Furthermore, the need for governance, policy enforcement, and automation across distributed systems is driving investment in advanced data management platforms. As enterprises expand their cloud footprints, maintaining consistent controls for data quality, security, and compliance across environments becomes increasingly important. Effective management tools help enforce standardized policies, reduce operational risk, and streamline compliance with internal and external standards.

Restraint Analysis

One notable restraint in the multi-cloud data management landscape is the technical complexity inherent in integrating and synchronizing diverse cloud platforms. Managing data across multiple service environments involves coordinating different APIs, data formats, identity frameworks, and management interfaces, which can create operational friction. This complexity can lead to extended deployment timelines and increased reliance on specialized technical expertise, which may be scarce in some organizations.

The need to bridge disparate systems also increases the risk of configuration errors, complicating efforts to maintain consistent data integrity and governance. Another restraint arises from the challenges associated with achieving compliance and data sovereignty across geographically distributed cloud deployments. Different regions enforce varying regulatory requirements for data storage, processing, and transfer, and ensuring adherence to these regulations across multiple cloud environments can be difficult.

Opportunity Analysis

A significant opportunity within the multi-cloud data management market lies in developing solutions that enhance data governance, compliance, and risk management. As regulatory requirements become more stringent across global jurisdictions, organizations will seek tools that simplify compliance reporting and policy enforcement across diverse cloud environments.

Platforms that provide end-to-end governance capabilities with centralized visibility can reduce risk and administrative burden while supporting audit readiness. This presents an opportunity for vendors to differentiate offerings with robust governance and policy automation features. Additionally, there is expanding opportunity in delivering analytics-driven optimization and cost management features that help organizations balance performance with expenditure.

Multi-cloud deployments can generate unpredictable cost patterns due to varying pricing models and data transfer charges across providers. Solutions that provide real-time cost insights, predictive budgeting, and optimization recommendations can help enterprises control expenses while maintaining service performance. These value-added capabilities can drive greater adoption among organizations focused on financial efficiency.

Challenge Analysis

A primary challenge in multi-cloud data management is ensuring consistent security and access control across all cloud environments. Differences in security models, identity management systems, and access policies among cloud providers can complicate the creation of a unified security posture. Organizations must implement strong identity and access management frameworks that seamlessly operate across environments while mitigating risks such as unauthorized access and data breaches.

Failure to address these challenges effectively can expose sensitive data and undermine stakeholder trust. Another ongoing challenge is managing the costs associated with multi-cloud operations. While multi-cloud strategies can offer cost advantages through optimized resource allocation, they can also lead to unpredictable and rising expenses if not managed strategically.

Data transfer fees, storage costs, and resource usage across providers can accumulate quickly without effective monitoring and control mechanisms. Organizations must balance performance requirements with budget constraints, ensuring that cost management practices are embedded within their multi-cloud data management strategies.

Key Market Segments

By Component

- Software/Solutions

- Services

By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Application

- Data Integration and Migration

- Backup and Recovery

- Security and Compliance

- Disaster Recovery

- Data Governance

- Data Orchestration

- Others

By End-User Industry

- Banking, Financial Services, and Insurance

- Healthcare

- IT and Telecommunications

- Retail and E-commerce

- Manufacturing

- Government

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Global cloud hyperscalers such as Google LLC, Microsoft Corporation, and Amazon Web Services Inc. lead the multi-cloud data management market. Their platforms provide unified storage, analytics, and governance tools across distributed environments. Alibaba Cloud strengthens adoption in Asia-Pacific markets. These providers benefit from scalable infrastructure and integrated AI services. Demand is driven by enterprise strategies that reduce vendor lock-in and improve workload portability.

Enterprise software and infrastructure vendors such as International Business Machines Corporation, Oracle Corporation, SAP SE, Dell Technologies Inc., Hewlett Packard Enterprise Company, and Cisco Systems Inc. provide hybrid and multi-cloud orchestration capabilities. These vendors emphasize interoperability, data protection, and compliance. Adoption is strong among regulated industries managing complex data environments.

Data platform and backup specialists such as Snowflake Inc., NetApp Inc., Teradata Corporation, Commvault Systems Inc., and Hitachi Vantara Corporation enhance cross-cloud data mobility and resilience. These players support advanced analytics, disaster recovery, and governance frameworks. Other vendors expand regional presence and innovation, supporting sustained growth in multi-cloud data management solutions.

Top Key Players in the Market

- Google LLC

- Microsoft Corporation

- Amazon Web Services Inc.

- International Business Machines Corporation

- Oracle Corporation

- SAP SE

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Cisco Systems Inc.

- Snowflake Inc.

- NetApp Inc.

- Teradata Corporation

- Commvault Systems Inc.

- Hitachi Vantara Corporation

- Alibaba Cloud

- Others

Recent Developments

- In January 2026, Cisco advanced cloud solutions simplified multi-cloud management with unified dashboards and security. Cisco’s networking edge continues powering seamless data movement across diverse cloud setups.

- In December 2025, Microsoft Azure bolstered Azure Arc for seamless hybrid/multi-cloud management, extending consistent data governance to AWS and GCP resources. It’s a smart move that cements Microsoft’s dominance in unified multi-cloud data strategies for global enterprises.

- In November 2025, HPE unveiled Unified Cloud Management services for hybrid multi-cloud with AI optimization across infrastructure domains. Practical tools like concept-to-operation support make HPE a go-to for simplifying complex multi-cloud environments.

Report Scope

Report Features Description Market Value (2025) USD 12.6 Bn Forecast Revenue (2035) USD 168.7 Bn CAGR(2026-2035) 29.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software/Solutions, Services), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Application (Data Integration and Migration, Backup and Recovery, Security and Compliance, Disaster Recovery, Data Governance, Data Orchestration, Others), By End-User Industry (Banking, Financial Services, and Insurance, Healthcare, IT and Telecommunications, Retail and E-commerce, Manufacturing, Government, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Google LLC, Microsoft Corporation, Amazon Web Services Inc., International Business Machines Corporation, Oracle Corporation, SAP SE, Dell Technologies Inc., Hewlett Packard Enterprise Company, Cisco Systems Inc., Snowflake Inc., NetApp Inc., Teradata Corporation, Commvault Systems Inc., Hitachi Vantara Corporation, Alibaba Cloud, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Multi-Cloud Data Management MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Multi-Cloud Data Management MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Google LLC

- Microsoft Corporation

- Amazon Web Services Inc.

- International Business Machines Corporation

- Oracle Corporation

- SAP SE

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Cisco Systems Inc.

- Snowflake Inc.

- NetApp Inc.

- Teradata Corporation

- Commvault Systems Inc.

- Hitachi Vantara Corporation

- Alibaba Cloud

- Others

Our Clients

- 178108

- Feb. 2026