Global Mobility Dataplace Market By Solution Type (Data Platforms, Analytics Tools, Mobility Management Systems, Others), By Application (Urban Mobility, Public Transportation, Fleet Management, Traffic Management, Others), By End-User (Government, Transportation Agencies, Mobility Service Providers, Enterprises, Others), By Deployment Mode (Cloud-Based, On-Premises), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Mar. 2026

- Report ID: 180073

- Number of Pages: 201

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Solution Type

- By Application

- By End User

- By Deployment Mode

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

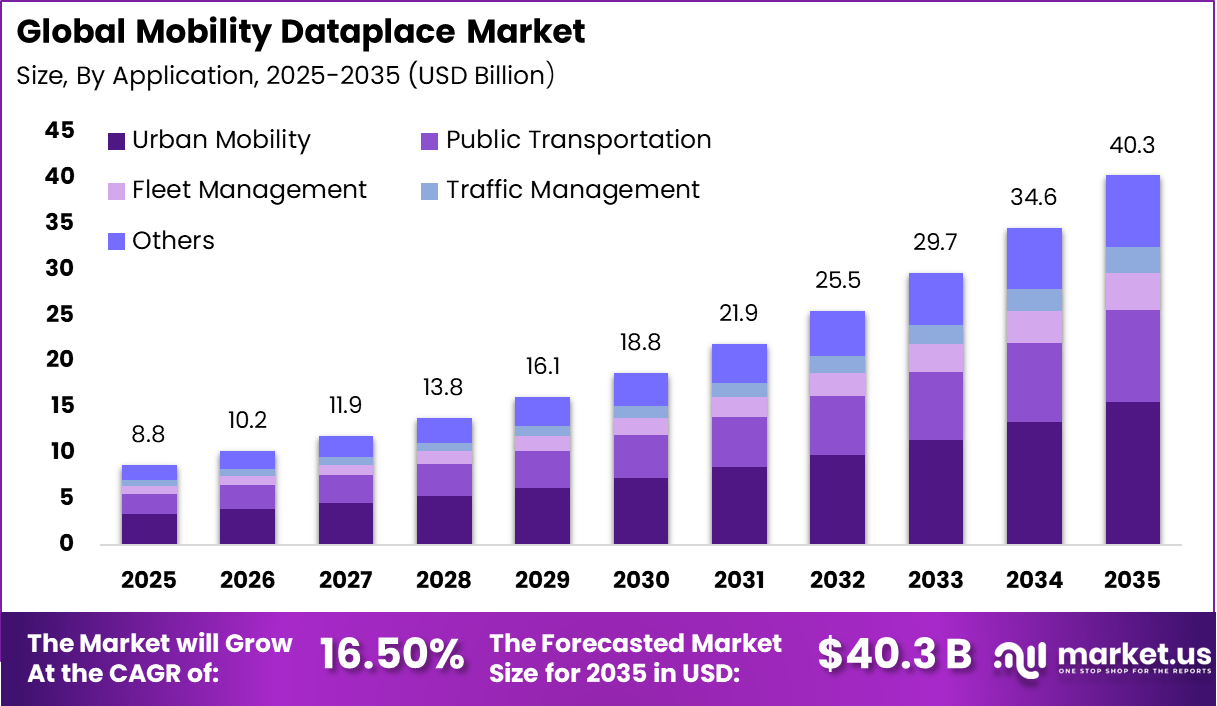

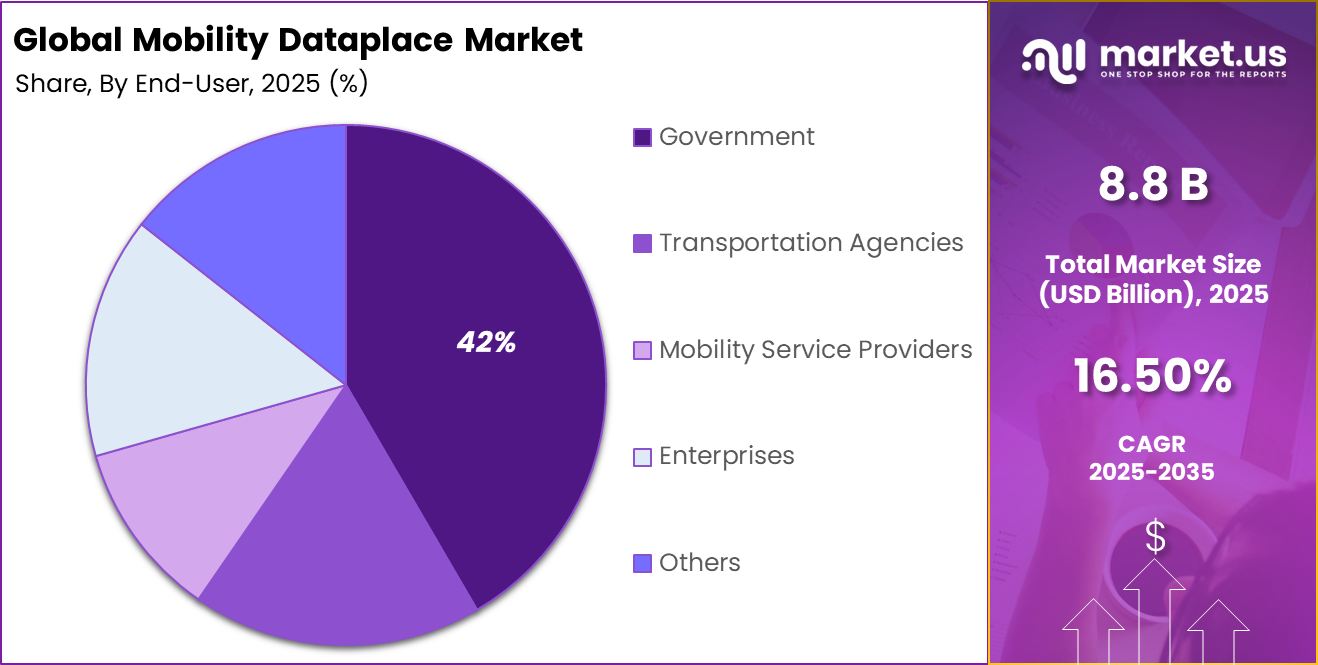

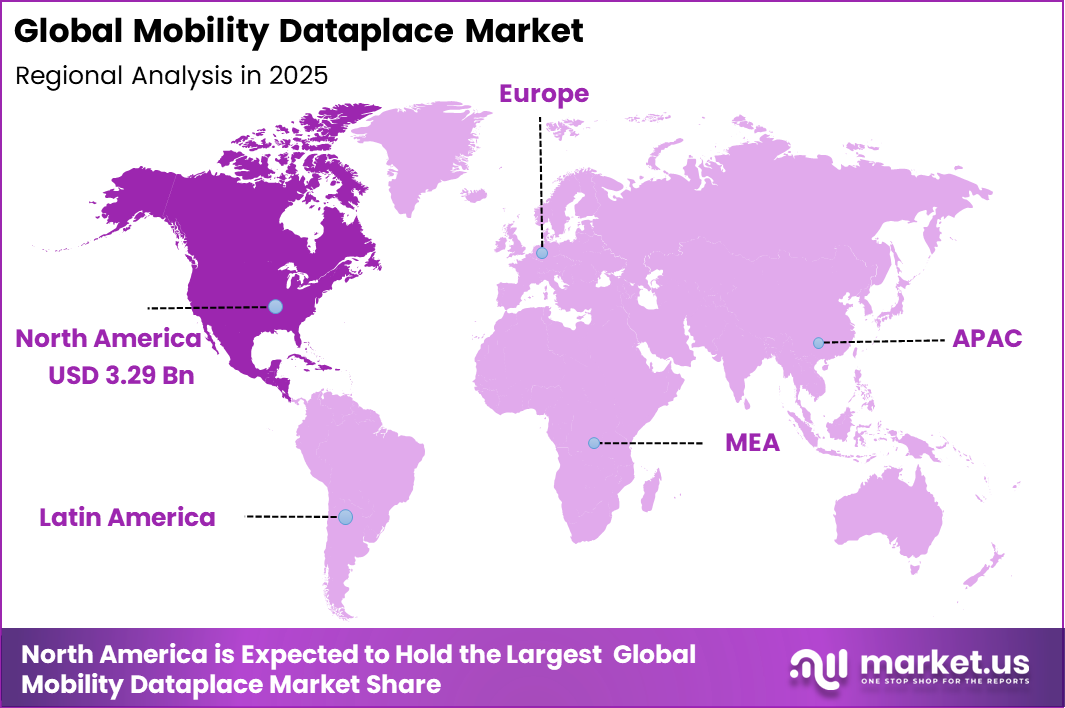

The Global Mobility Dataplace Market generated USD 8.8 billion in 2025 and is predicted to register growth from USD 10.2 billion in 2026 to about USD 40.3 billion by 2035, recording a CAGR of 16.50% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 37.7% share, holding USD 3.29 Billion revenue.

The Mobility Dataplace Market represents a rapidly expanding segment within the digital mobility ecosystem. Mobility dataplace platforms enable the collection, sharing, and monetization of transportation and mobility-related data generated by vehicles, infrastructure systems, mobile devices, and connected sensors. These platforms are increasingly used by governments, transportation agencies, and mobility service providers to improve traffic management, urban planning, and fleet optimization through data-driven insights.

Mobility dataplace platforms serve as intermediaries between data providers and data consumers. Transportation agencies, city planners, logistics companies, and ride-sharing operators use these platforms to access real-time mobility information. By combining datasets from different sources, these platforms support predictive analytics, route optimization, and infrastructure planning for modern transportation systems.

One major factor supporting market growth is the increasing deployment of connected vehicles and telematics technologies. Modern vehicles generate large volumes of data related to location, speed, driving behavior, and environmental conditions. Mobility dataplace platforms aggregate these datasets and convert them into actionable insights that improve traffic flow, vehicle safety, and transportation efficiency.

Demand for mobility dataplace platforms is rising due to the growing complexity of urban transportation networks. Cities are facing challenges related to traffic congestion, environmental sustainability, and population growth. Data-driven mobility systems allow urban planners to analyze traffic patterns and implement efficient transportation strategies.

The increasing adoption of Mobility-as-a-Service (MaaS) platforms is also strengthening demand for mobility data marketplaces. These platforms integrate different transportation services such as ride-sharing, public transit, and micro-mobility options into unified digital ecosystems. Mobility dataplace systems provide the underlying data infrastructure required to coordinate these services effectively.

Top Market Takeaways

- By Solution Type, data platforms dominate with 45.4% share, aggregating multi-modal transport telemetry, predictive traffic modeling, and real-time mobility analytics.

- By Application, urban mobility captures 38.6%, optimizing public transit, micromobility fleets, and congestion pricing through unified data lakes.

- By End-User, government holds 41.6%, powering city dashboards, MaaS orchestration, and policy-driven transport planning.

- By Deployment Mode, on-premises claims 54.7%, ensuring sovereign control over citizen mobility data and integration with legacy traffic systems.

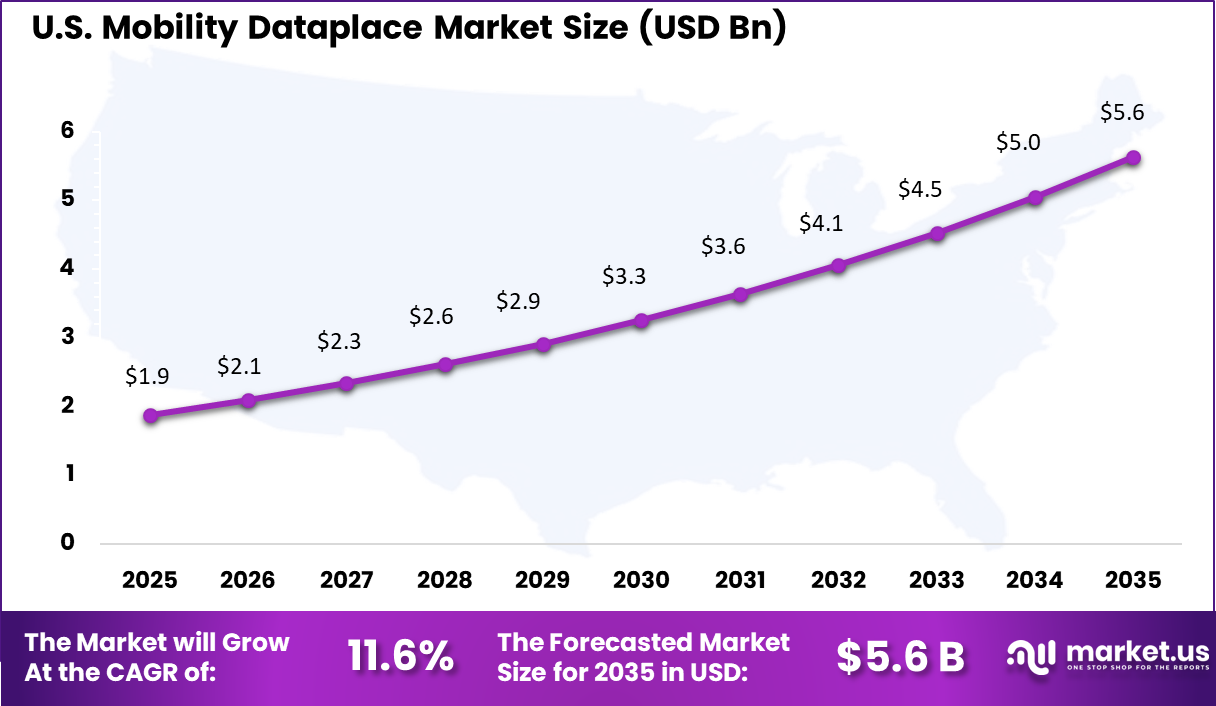

- Regionally, North America accounts for 37.7% global share, with the U.S. market valued at USD 1.88 billion and a CAGR of 11.6%, driven by federal smart infrastructure funding.

Drivers Impact Analysis

Key Drivers Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Strategic Importance Rapid Expansion of Connected and Autonomous Vehicles +3.6% North America, Europe Medium to Long Term Generates large volumes of mobility data Increasing Adoption of Smart City Transportation Systems +3.2% APAC, Europe Long Term Supports integrated urban mobility platforms Rising Demand for Real-time Traffic and Mobility Analytics +2.7% Global Medium Term Improves urban transport efficiency Growth in Mobility-as-a-Service Platforms +2.3% North America, APAC Medium to Long Term Encourages data sharing ecosystems Integration of Mobility Data with Urban Planning Systems +1.9% Europe, North America Long Term Enables predictive infrastructure planning Restraints Impact Analysis

Key Restraints Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Market Constraint Level Data Privacy and Security Concerns -2.3% Europe, North America Medium Term Limits unrestricted data sharing Fragmented Mobility Data Ecosystems -1.9% Global Medium Term Reduces interoperability between platforms High Infrastructure Deployment Costs -1.5% Emerging Markets Short to Medium Term Slows smart mobility adoption Lack of Standardized Data Governance Policies -1.2% Global Medium to Long Term Creates regulatory uncertainties By Solution Type

Data platforms account for 45.4% of the market, reflecting the importance of centralized systems that collect, manage, and distribute transportation related data. These platforms integrate information from traffic sensors, connected vehicles, public transit systems, and navigation services. By consolidating these datasets, mobility dataplaces enable better coordination among transportation stakeholders.

Organizations rely on these platforms to analyze traffic congestion, optimize route planning, and improve urban transportation efficiency. The ability to share standardized data across multiple systems helps city planners and service providers develop informed mobility strategies. As transportation networks become more connected, data platforms continue to form the foundation of mobility data exchange ecosystems.

By Application

Urban mobility represents 38.6% of market applications due to increasing demand for intelligent transportation systems within growing cities. Data driven mobility platforms help municipalities monitor traffic conditions, manage public transit operations, and improve road safety. These systems support efficient resource allocation by providing real time insights into transportation demand.

Urban mobility applications also enable the integration of shared mobility services such as ride sharing, bike sharing, and electric scooters. By analyzing mobility patterns, authorities can design more efficient transportation networks and reduce congestion levels. As cities pursue smart mobility initiatives, urban mobility applications remain a primary driver of dataplace adoption.

By End User

Government entities account for 41.6% of the market, reflecting their central role in managing public transportation infrastructure and traffic regulation systems. Municipal and national authorities use mobility dataplaces to collect and analyze transportation data from various sources. This data supports planning decisions related to road development, traffic control, and public transit optimization.

Public agencies also rely on these platforms to improve transparency and collaboration with private mobility service providers. Data sharing initiatives enable better coordination across transportation networks. As governments implement smart city programs, investment in mobility data platforms continues to increase.

By Deployment Mode

On premises deployment represents 54.7% of the market, indicating the importance of maintaining direct control over transportation data infrastructure. Mobility datasets often contain sensitive information related to infrastructure operations and public safety systems. Maintaining these systems within internal data centers helps governments and organizations enforce strict security policies.

On premises deployment also allows customized integration with existing traffic management systems and public infrastructure platforms. Many transportation authorities operate legacy systems that require secure internal connectivity. As data governance and security concerns remain significant, on premises deployment continues to play a dominant role.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Venture Capital High Medium to High North America, Europe Focus on mobility data startups and AI analytics Private Equity Medium to High Medium North America, Europe Attractive infrastructure and data platform investments Strategic Automotive and Mobility Firms High Medium Global Integration with connected vehicle ecosystems Institutional Investors Medium Medium Developed Markets Long-term smart infrastructure allocation Government-backed Infrastructure Funds Medium Low APAC, Middle East Smart city and transportation modernization Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Adoption Momentum AI-based Traffic and Mobility Analytics +3.4% North America, Europe Medium to Long Term Enables predictive traffic management Internet of Things Sensors in Transportation Networks +3.0% APAC, Europe Medium Term Expands real-time mobility data collection Cloud-based Mobility Data Platforms +2.4% Global Short to Medium Term Supports scalable data integration 5G-enabled Vehicle-to-Infrastructure Communication +2.0% North America, APAC Long Term Improves data transmission speed Digital Twin Simulation for Urban Mobility +1.6% Europe, North America Long Term Supports infrastructure planning Key Challenges

- Difficulty in integrating mobility data from multiple transportation sources

- Data privacy concerns when sharing location and travel information

- Lack of standardized data formats across mobility platforms

- High infrastructure cost for managing large real time mobility datasets

- Dependence on cooperation between public authorities and private mobility providers

Emerging Trends

In the Mobility Dataplace market, a major trend is the creation of shared digital platforms where transportation data from multiple sources can be collected, managed, and analysed in a unified environment. These platforms bring together data from vehicles, public transport systems, connected devices, and traffic infrastructure to provide a clearer picture of how people and goods move across cities.

This approach helps planners and service providers coordinate mobility services more effectively and improve transport efficiency. Another trend is the growing use of advanced analytics and artificial intelligence to interpret mobility patterns, allowing stakeholders to identify congestion points, optimise routes, and improve service planning.

Growth Factors

A key growth factor in this market is the increasing demand for connected and data driven mobility solutions as cities face rising traffic pressure and expanding urban populations. Governments and transportation agencies are turning to mobility data platforms to support smarter planning, reduce congestion, and improve safety across transport networks.

These platforms help integrate information from various mobility services and support coordinated decision making for public transport, traffic management, and fleet operations. Another important driver is the rapid development of digital infrastructure such as IoT sensors, GPS enabled devices, and connected vehicles, which generate large volumes of mobility data that can be analysed for operational insights and planning improvements.

Key Market Segments

By Solution Type

- Data Platforms

- Analytics Tools

- Mobility Management Systems

- Others

By Application

- Urban Mobility

- Public Transportation

- Fleet Management

- Traffic Management

- Others

By End-User

- Government

- Transportation Agencies

- Mobility Service Providers

- Enterprises

- Others

By Deployment Mode

- Cloud-Based

- On-Premises

Regional Analysis

North America accounts for 37.7% of the mobility dataplace market, supported by advanced transportation infrastructure and strong adoption of data-driven mobility planning. Public authorities, mobility service providers, and urban planners in the region are increasingly using mobility data platforms to analyze traffic flows, public transit usage, and multimodal transportation patterns. Demand is driven by the need to improve urban mobility efficiency, reduce congestion, and support data-informed transportation policies.

The U.S. market is valued at USD 1.88 Bn and is expanding at a CAGR of 11.6%, reflecting growing investment in smart mobility and digital transportation ecosystems. Adoption is influenced by increasing use of connected vehicle data, ride-sharing analytics, and real-time traffic monitoring systems. Growth is further supported by collaboration between government agencies and mobility technology providers to enhance transportation planning, infrastructure optimization, and sustainable urban mobility strategies.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The Mobility Dataplace market is led by global mapping, navigation, and transportation technology providers such as TomTom, HERE Technologies, INRIX, Google, Apple, Uber, Waze, Esri, Trimble, Siemens Mobility, Bosch Mobility Solutions, Cubic Transportation Systems, and Alstom. These companies compete on large scale mobility data collection, location intelligence, and integration with navigation and smart city systems. Their platforms are widely used by governments, mobility service providers, and urban planners that require accurate traffic insights, route optimization, and transportation network analytics.

Mobility analytics and transportation solution providers including Moovit, PTV Group, Transdev, Geotab, StreetLight Data, Otonomo, Iteris, and others compete through specialized mobility datasets and analytical tools. Competition in this segment is driven by real time traffic monitoring, vehicle data integration, and advanced urban mobility planning capabilities. These vendors are often selected by cities and transportation agencies that need reliable mobility insights to support infrastructure planning and traffic management.

Top Key Players in the Market

- TomTom

- HERE Technologies

- INRIX

- Apple

- Uber

- Moovit

- Siemens Mobility

- Bosch Mobility Solutions

- Trimble

- Esri

- PTV Group

- Cubic Transportation Systems

- Transdev

- Alstom

- Geotab

- Waze

- StreetLight Data

- Otonomo

- Iteris

- Others

Future Outlook

The future outlook for the Mobility Dataplace Market is positive as transportation systems increasingly depend on data sharing and analytics to improve mobility services. Mobility dataplaces enable organizations to exchange and analyze large volumes of mobility data from vehicles, public transport networks, and infrastructure systems. This supports better traffic planning, route optimization, and improved mobility services for cities and transportation providers.

Demand for these platforms is expected to grow as smart city projects, connected vehicles, and digital transportation networks expand worldwide. Adoption of real time data platforms, cloud technologies, and advanced analytics will further strengthen the role of mobility dataplaces in transportation planning. Growth can be attributed to rising urbanization, need for efficient traffic management, and increasing focus on intelligent mobility ecosystems.

Recent Developments

- In September 2025, TomTom partnered with iNavi Systems to embed its mapping and traffic data into mobility platforms for autonomous driving, boosting global reach.

- HERE Technologies enhanced its EV charging predictions using machine learning in early 2025, covering over 1.2 million connectors worldwide.

- Google teamed up with Bentley Systems in April 2025 to integrate AI-driven imagery for infrastructure management.

- INRIX focuses on traffic analytics and parking solutions drawn from millions of connected vehicles. They launched a predictive demand tool in November 2025, helping cities manage congestion during peak hours with 95% accuracy in forecasts. This positions them strongly for urban mobility contracts.

Report Scope

Report Features Description Market Value (2025) USD 8.8 Billion Forecast Revenue (2035) USD 40.3 Billion CAGR(2025-2035) 16.50% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Solution Type (Data Platforms, Analytics Tools, Mobility Management Systems, Others), By Application (Urban Mobility, Public Transportation, Fleet Management, Traffic Management, Others), By End-User (Government, Transportation Agencies, Mobility Service Providers, Enterprises, Others), By Deployment Mode (Cloud-Based, On-Premises) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape TomTom, HERE Technologies, INRIX, Google, Apple, Uber, Moovit, Siemens Mobility, Bosch Mobility Solutions, Trimble, Esri, PTV Group, Cubic Transportation Systems, Transdev, Alstom, Geotab, Waze, StreetLight Data, Otonomo, Iteris, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- TomTom

- HERE Technologies

- INRIX

- Apple

- Uber

- Moovit

- Siemens Mobility

- Bosch Mobility Solutions

- Trimble

- Esri

- PTV Group

- Cubic Transportation Systems

- Transdev

- Alstom

- Geotab

- Waze

- StreetLight Data

- Otonomo

- Iteris

- Others

Our Clients

- 180073

- Mar. 2026