Quick Navigation

Report Overview

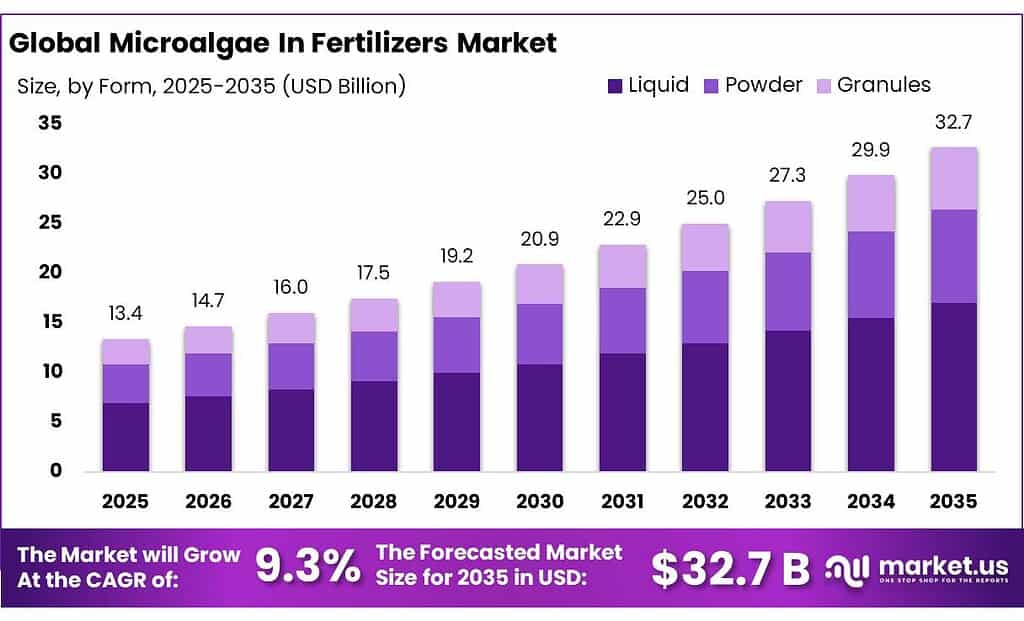

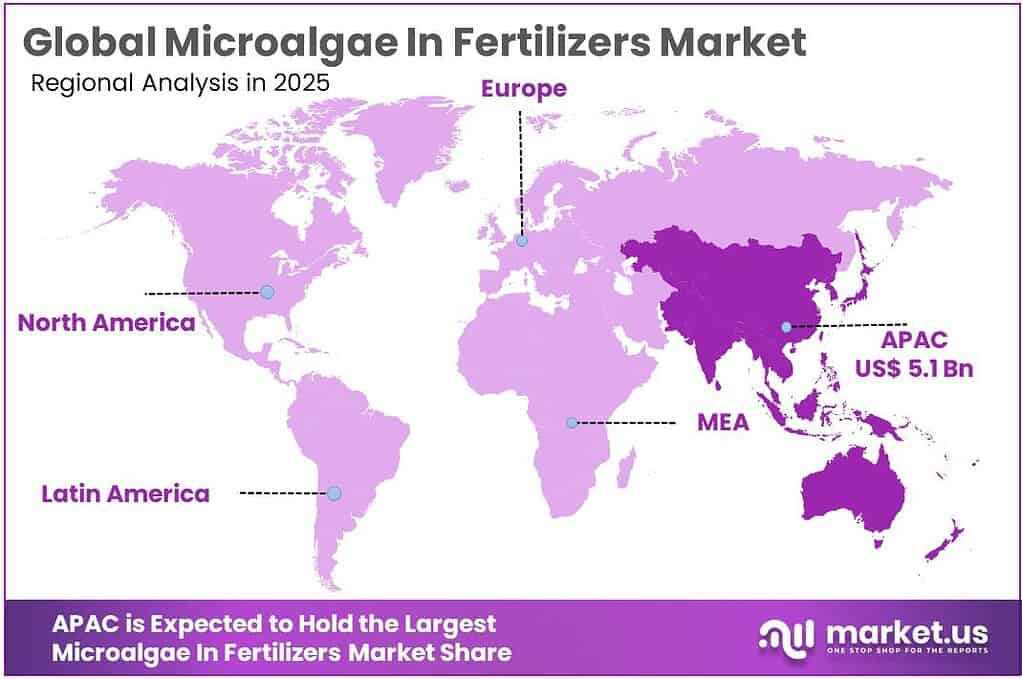

The Global Microalgae In Fertilizers Market size is expected to be worth around USD 32.7 Billion by 2035, from USD 13.4 Billion in 2025, growing at a CAGR of 9.3% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 38.5% share, holding USD 5.1 billion revenue.

Microalgae are microscopic photosynthetic organisms that are increasingly being explored for agricultural applications due to their rich nutrient composition and sustainability advantages. In fertilizer formulations, microalgae function as biofertilizers or biostimulants that enhance soil fertility, nutrient availability, and crop productivity.

- Additionally, some microalgae species can accumulate up to 65–70% protein content, highlighting their high nutrient density and biological productivity, which further supports their agricultural applications. Scientific estimates indicate that there may be 200,000–800,000 microalgae species globally, with around 50,000 already described, demonstrating a vast biological resource base for industrial applications in agriculture, food, and biotechnology sectors.

According to the Food and Agriculture Organization (FAO), global algae production increased dramatically from 0.56 million tonnes in 1950 to 35.82 million tonnes in 2019, demonstrating the rapid scaling of algaculture technologies. Additionally, global aquatic plant production increased from 13.5 million tonnes in 1995 to about 37.8 million tonnes in 2022, demonstrating strong growth in algae cultivation infrastructure worldwide.

In addition, FAO data indicate that algae cultivation represented around 30% of the approximately 120 million tonnes of global aquaculture production in 2019, highlighting the importance of algae-based biomass as a resource for multiple industrial applications including agriculture. While microalgae currently represent a smaller share of total algae biomass, commercial microalgae cultivation already produces approximately 60,000 tonnes per year globally, with production concentrated primarily in Asian countries such as China, Japan, and India.

Several structural drivers are accelerating the adoption of microalgae in fertilizers. Increasing global demand for sustainable farming inputs and the environmental concerns associated with chemical fertilizers are pushing agricultural systems toward biological alternatives. Microalgae-based biofertilizers can significantly improve crop productivity; experimental studies have shown yield increases of approximately 15.7% to 29.6% in certain fruit crops when microalgae fertilizers were applied, demonstrating their agronomic potential.

Government initiatives and research investments are also accelerating the development of the microalgae ecosystem. For example, collaborative initiatives such as the AlgaePARC research facility established by Wageningen University and supported by the Dutch Ministry of Agriculture were funded with approximately €2.25 million to advance pilot-scale algae production technologies and support commercialization of algae-based products across sectors including agriculture and bio-based materials.

Key Takeaways

- Microalgae In Fertilizers Market size is expected to be worth around USD 32.7 Billion by 2035, from USD 13.4 Billion in 2025, growing at a CAGR of 9.3%.

- Spirulina held a dominant market position, capturing more than a 29.3% share.

- Liquid held a dominant market position, capturing more than a 52.8% share in the microalgae fertilizers market.

- Field Crops held a dominant market position, capturing more than a 44.7% share.

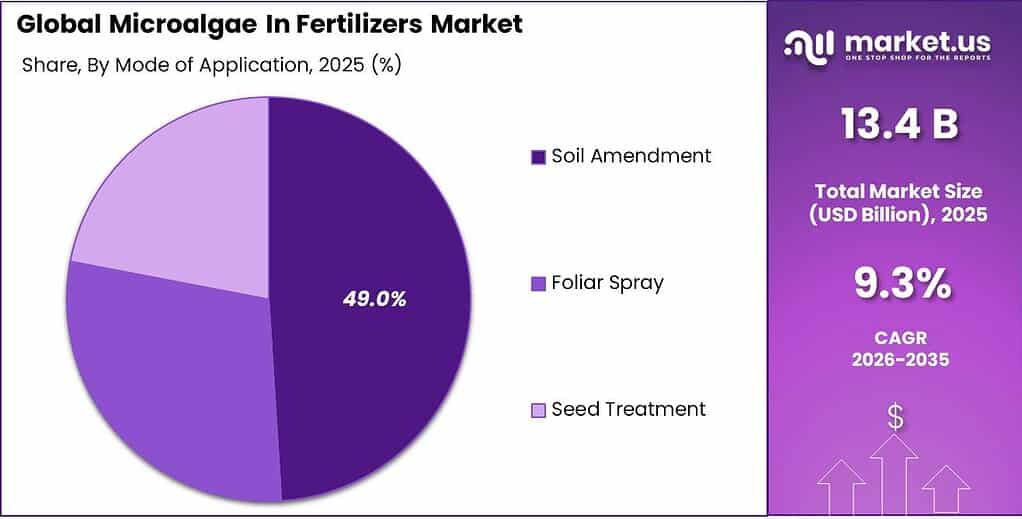

- Soil Amendment held a dominant market position, capturing more than a 49.6% share.

- Asia Pacific dominates the Microalgae in Fertilizers Market with 38.5% share, valued at around USD 5.1 Billion.

By Product Type Analysis

Spirulina dominates with 29.3% share due to its high nutrient content and wide agricultural applications

In 2024, Spirulina held a dominant market position, capturing more than a 29.3% share in the microalgae-based fertilizers market. This strong position can largely be attributed to Spirulina’s exceptional nutrient composition and its long history of commercial cultivation. Spirulina contains significant levels of nitrogen, amino acids, vitamins, and natural growth-promoting compounds that support plant development and soil health. Because of these properties, it has become one of the most widely used microalgae species in agricultural biostimulants and organic fertilizer formulations.

By Form Analysis

Liquid fertilizers lead with 52.8% share due to easy application and faster nutrient absorption

In 2024, Liquid held a dominant market position, capturing more than a 52.8% share in the microalgae fertilizers market. This strong presence is mainly linked to the ease of application and faster nutrient availability that liquid formulations offer. Liquid microalgae fertilizers are widely used by farmers because they can be easily applied through foliar spraying, drip irrigation systems, or fertigation methods. These application techniques allow nutrients and bioactive compounds from microalgae to reach plants more quickly compared to solid forms, helping improve plant growth and crop performance.

By Application Analysis

Field crops lead with 44.7% share as large-scale farming increases demand for natural fertilizers

In 2024, Field Crops held a dominant market position, capturing more than a 44.7% share in the microalgae fertilizers market. The strong presence of this segment is mainly driven by the extensive cultivation of staple crops such as wheat, rice, maize, and pulses across major agricultural regions. Farmers growing these crops are increasingly adopting biological fertilizers to maintain soil fertility and reduce dependence on chemical inputs.

By Mode of Application Analysis

Soil amendment leads with 49.6% share as farmers focus on improving soil health and fertility

In 2024, Soil Amendment held a dominant market position, capturing more than a 49.6% share in the microalgae fertilizers market. This leading position is mainly linked to the increasing need for improving soil quality in modern agriculture. Farmers are becoming more aware of the long-term effects of excessive chemical fertilizer use, which can reduce soil fertility over time. Microalgae-based fertilizers are widely used as soil amendments because they help restore soil nutrients, enhance microbial activity, and improve overall soil structure.

Key Market Segments

By Product Type

- Spirulina

- Chlorella

- Scenedesmus

- Nannochloropsis

- Porphyridium

- Others

By Form

- Liquid

- Powder

- Granules

By Application

- Field Crops

- Horticulture Crops

- Turf and Ornamentals

- Hydroponics

By Mode of Application

- Soil Amendment

- Foliar Spray

- Seed Treatment

Emerging Trends

Integration of Microalgae Cultivation with Wastewater Treatment and Circular Agriculture

One of the latest trends shaping the microalgae fertilizers sector is the integration of microalgae cultivation with wastewater treatment and circular bioeconomy systems. Researchers and agricultural industries are increasingly exploring ways to grow microalgae using agricultural or industrial wastewater instead of fresh water and synthetic nutrients. This approach helps convert waste nutrients into valuable biomass that can later be processed into biofertilizers and soil conditioners.

- According to data published by the Food and Agriculture Organization (FAO), worldwide algae production has increased dramatically over the past several decades. Production rose from about 0.56 million tonnes in 1950 to approximately 35.82 million tonnes by 2019, showing how quickly algae cultivation has expanded globally. This large increase in production capacity provides a strong base for developing new applications such as agricultural fertilizers. Much of this production is concentrated in Asia, where countries like China account for about 57% of global algae production, followed by Indonesia with around 27%, highlighting the strong industrial infrastructure already supporting algae cultivation.

Experimental studies have demonstrated measurable agricultural benefits; for example, the application of microalgae-based biofertilizers in fruit cultivation has been shown to increase crop yields by about 15.7% to 29.6% compared with conventional fertilization methods. These findings are encouraging farmers and agricultural researchers to experiment with microalgae fertilizers in different crop systems.

Drivers

Growing Demand for Sustainable and Eco-Friendly Fertilizers

One of the most important driving factors behind the growth of microalgae in fertilizers is the increasing global demand for sustainable and environmentally friendly agricultural inputs. Modern agriculture has relied heavily on chemical fertilizers for decades, but this dependence has raised concerns about soil degradation, nutrient runoff, and environmental pollution. As a result, farmers, researchers, and governments are now actively exploring biological alternatives that can maintain crop productivity while protecting soil health.

- According to the Food and Agriculture Organization (FAO), global algae production has increased dramatically over the last several decades. Production rose from about 0.56 million tonnes in 1950 to around 35.82 million tonnes by 2019, showing how rapidly the algae industry has expanded across aquaculture, food, and agricultural applications. FAO also reports that farmed algae contribute nearly 30% of global aquaculture production, totaling roughly 35.1 million tonnes, highlighting the scale of the sector and its potential to supply raw materials for agricultural inputs.

Another major factor driving the use of microalgae fertilizers is the biological diversity and untapped potential of algae species. Researchers estimate that there are around 72,500 known species of algae worldwide, but only a small portion of them are currently cultivated for commercial purposes. This enormous biodiversity offers a large opportunity for developing new agricultural products. Different microalgae species contain various nutrients, amino acids, proteins, and plant growth regulators that can benefit crops in different ways.

Government initiatives and sustainability policies are also playing a major role in encouraging the adoption of microalgae-based agricultural products. Many countries are promoting biological fertilizers as part of their strategies to reduce the environmental impact of conventional farming. For example, several global sustainability frameworks and agricultural development programs supported by organizations such as the FAO emphasize the importance of biological resources like algae for improving food security and supporting sustainable agricultural systems.

Restraints

High Production and Processing Costs Limiting Large-Scale Adoption

One of the most significant restraining factors for the growth of microalgae in fertilizers is the high cost associated with cultivating, harvesting, and processing microalgae biomass. While microalgae have strong potential as a sustainable agricultural input, producing them at a large commercial scale remains expensive compared with many conventional fertilizer alternatives. The cultivation process requires controlled environments, specialized equipment, and continuous monitoring of nutrients, light, and temperature conditions.

- A major challenge is the cost of producing microalgae biomass itself. Research studies show that the cost of microalgae biomass can vary widely depending on the production method and scale. In many industrial systems, biomass production costs can range from about 2.83 USD to 315 USD per kilogram, reflecting differences in cultivation technology, energy consumption, and harvesting methods. Such a wide cost range highlights the technological and economic challenges associated with large-scale production.

Another major expense occurs during harvesting and biomass recovery. Microalgae cells are extremely small and are suspended in water, which means they must be separated through processes such as centrifugation, filtration, or sedimentation. These processes require specialized equipment and energy, adding to production costs. Studies indicate that harvesting and biomass collection alone can account for around 30% of the total production cost in microalgae processing.

Infrastructure investment is also a barrier for companies entering the microalgae fertilizer sector. Building cultivation systems such as photobioreactors or large open-pond facilities requires considerable capital investment. For example, some prototype microalgae production units have required approximately €0.7 million in initial investment and about €0.5 million annually for operation and maintenance.

Production systems themselves also have technical limitations. According to data from the Food and Agriculture Organization, only large facilities capable of producing microalgae in mass quantities are able to achieve production costs below about USD 100 per kilogram of dry biomass, indicating that smaller facilities struggle to reach cost efficiency.

Opportunity

Expanding Global Organic Farming Creating Strong Opportunities for Microalgae Fertilizers

One of the biggest growth opportunities for microalgae fertilizers lies in the rapid expansion of organic and sustainable farming worldwide. Farmers are increasingly shifting toward natural agricultural inputs as they try to reduce dependence on synthetic fertilizers and maintain long-term soil health. Microalgae-based fertilizers fit well into this transition because they provide nutrients, natural growth stimulants, and organic matter without the environmental risks often linked to chemical fertilizers. These biological inputs can improve nutrient availability in soil and support plant growth while maintaining ecological balance in farming systems.

- According to data presented in The World of Organic Agriculture, organic farming is currently practiced in almost 190 countries, showing how widely sustainable agriculture has spread across the world. The same report states that nearly 99 million hectares of agricultural land were managed organically by at least 4.3 million farmers worldwide by 2023, reflecting a steady increase in organic farming activity.

The economic growth of the organic food sector further strengthens this opportunity. Global sales of organic food and beverages reached more than €136 billion in 2023, demonstrating strong consumer demand for sustainably produced food products. As consumer awareness about environmental sustainability and food quality continues to rise, farmers are under increasing pressure to adopt eco-friendly farming practices.

The continuous growth of sustainable agriculture worldwide suggests that demand for biological fertilizers will keep rising in the coming years. With millions of farmers already practicing organic farming and nearly 99 million hectares of land under organic management globally, the potential market for natural fertilizers like microalgae is significant.

Regional Insights

Asia Pacific dominates the Microalgae in Fertilizers Market with 38.5% share, valued at around USD 5.1 Billion

Asia Pacific represents the leading regional market for microalgae-based fertilizers, supported by the region’s strong agricultural base, expanding algae cultivation industry, and increasing shift toward sustainable farming practices. The region accounted for about 38.5% of the global market, reaching nearly USD 5.1 billion, making it the dominant regional contributor.

One of the biggest reasons for the region’s dominance is its well-established algae production infrastructure. According to data from the Food and Agriculture Organization (FAO), Asia is the global hub for algae cultivation. Nearly 97.38% of the world’s seaweed and algae production comes from Asian countries, highlighting the region’s strong supply base for algal biomass that can be used in agricultural inputs including fertilizers and biostimulants.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AlgaEnergy International Limited is a Spain-based biotechnology company focused on developing microalgae-based agricultural solutions such as biostimulants and biofertilizers. Founded in 2007, the company operates globally with research collaborations involving more than 120 institutions and partners. It has invested over €60 million in research and development projects related to microalgae technologies. The company employs around 150 employees and reported revenues of approximately USD 50 million in 2023, reflecting strong commercial expansion in agricultural biosolutions.

Algatech LTD, also known as AlgaTechnologies, is a microalgae biotechnology firm founded in 1998 and headquartered in Israel. The company focuses on cultivating high-value microalgae species for industrial applications including agriculture, cosmetics, and nutraceuticals. Algatech has raised approximately USD 50 million in funding to support its microalgae cultivation technologies and production facilities. It is known for producing natural astaxanthin and other algae-derived bioactive compounds used in agricultural and biological formulations.

DIC Corporation is a major Japanese chemical and biotechnology company founded in 1908 and headquartered in Tokyo. The company operates in multiple sectors including specialty chemicals, pigments, and microalgae-based ingredients. DIC has been actively involved in microalgae research and commercialization, particularly in spirulina and astaxanthin production. In 2023, the company reported revenues of approximately USD 8.3 billion, demonstrating its large global industrial presence.

Top Key Players Outlook

- AlgaEnergy International Limited

- Algatech LTD (Solabia Group)

- NeoEarth

- DIC Corporation (DIC Group)

- Kuehnle AgroSystems Inc.

- Seagrass Tech Private Limited

- Syngenta Group

- Kemin Industries, Inc.

- PhycoTerra (Heliae Agriculture LLC)

Recent Industry Developments

By 2024–2025, AlgaEnergy International Limited had expanded its agricultural biosolutions to more than 20 countries and reported an estimated annual revenue range between USD 50 million and USD 100 million, reflecting growing demand for sustainable agricultural inputs.

In FY2024, DIC Corporation reported consolidated net sales of ¥1,071.1 billion (around USD 6.9 billion), showing steady global operations across multiple industries including biotechnology and algae-based ingredients.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 13.4 Bn |

| Forecast Revenue (2035) | USD 32.7 Bn |

| CAGR (2026-2035) | 9.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Spirulina, Chlorella, Scenedesmus, Nannochloropsis, Porphyridium, Others), By Form (Liquid, Powder, Granules), By Application (Field Crops, Horticulture Crops, Turf and Ornamentals, Hydroponics, By Mode of Application (Soil Amendment, Foliar Spray, Seed Treatment) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AlgaEnergy International Limited, Algatech LTD (Solabia Group), NeoEarth, DIC Corporation (DIC Group), Kuehnle AgroSystems Inc., Seagrass Tech Private Limited, Syngenta Group, Kemin Industries, Inc., PhycoTerra (Heliae Agriculture LLC) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |