Quick Navigation

Report Overview

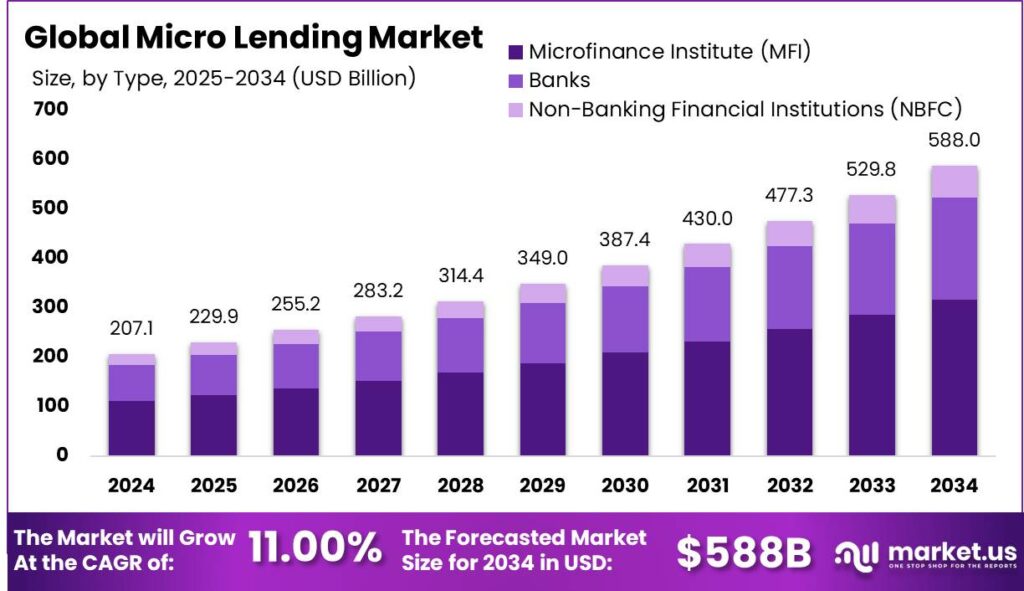

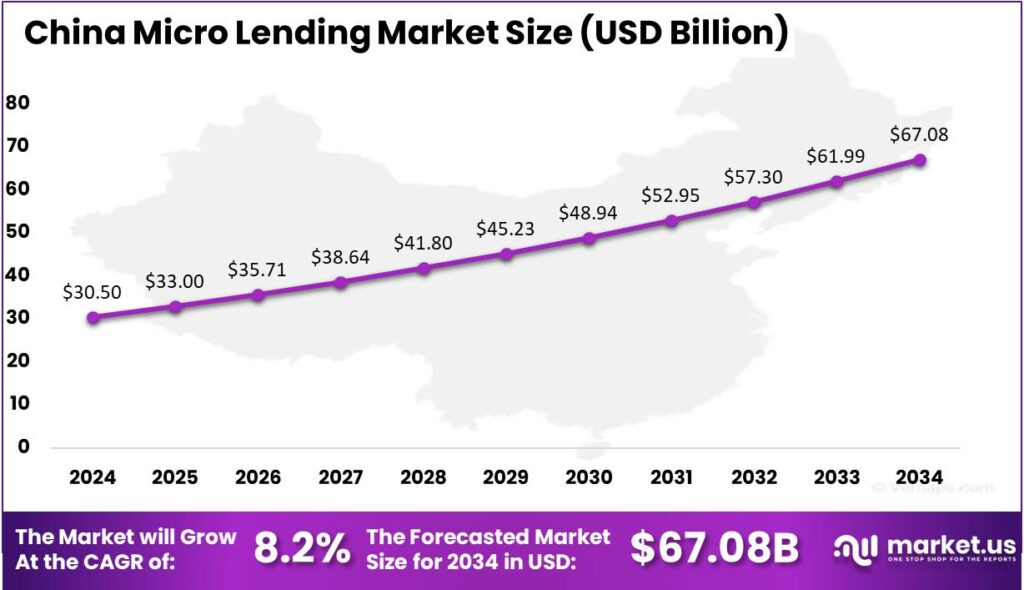

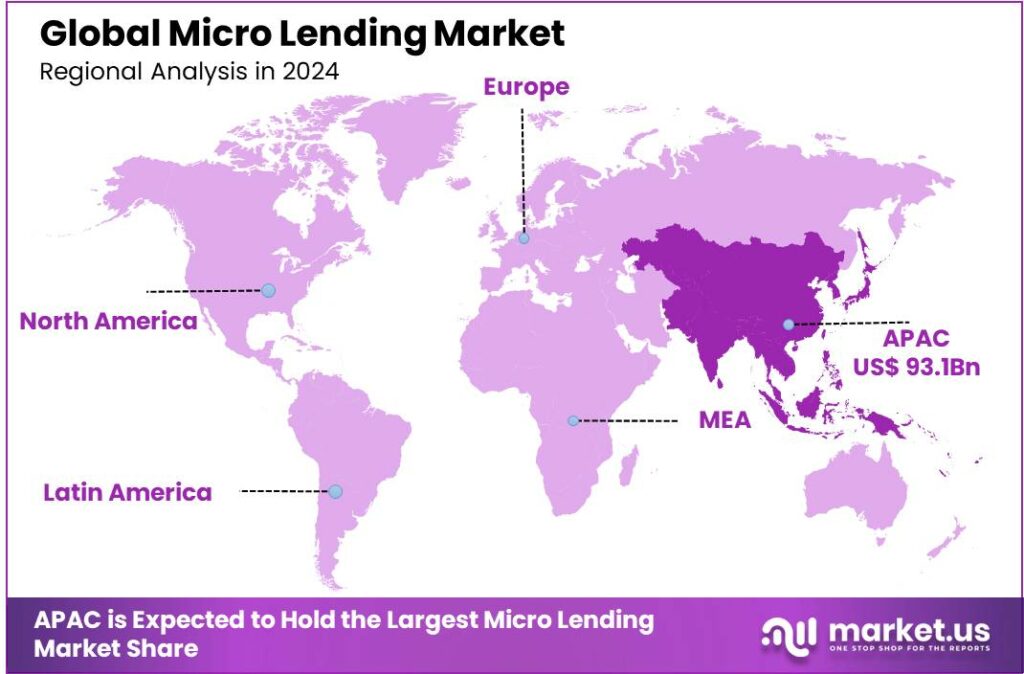

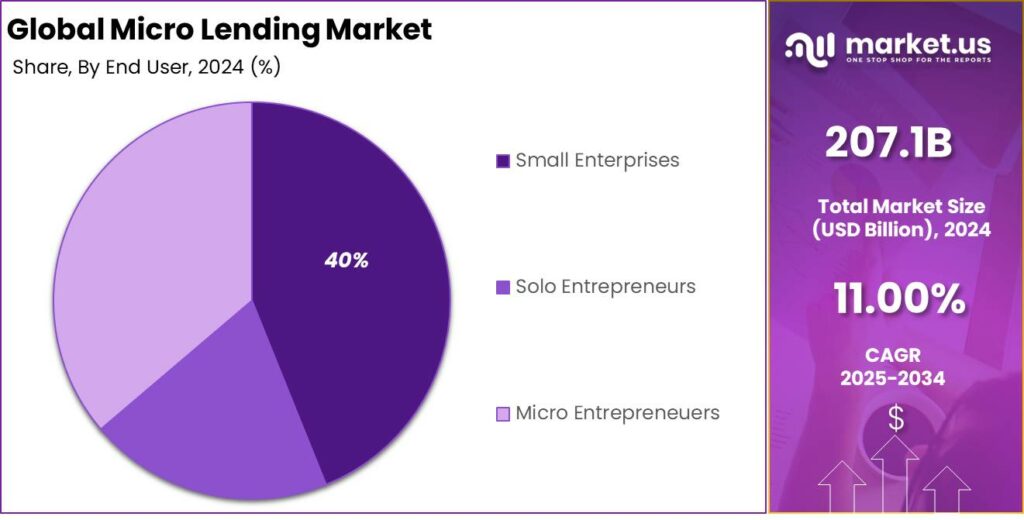

The Global Micro Lending Market size is expected to be worth around USD 588 Billion By 2034, from USD 207.1 Billion in 2024, growing at a CAGR of 11.00% during the forecast period from 2025 to 2034. In 2024, Asia-Pacific led the global micro-lending market with over 45% share and USD 93.1 billion in revenue. China alone contributed USD 30.5 billion, growing at a CAGR of 8.2%, fueled by demand from small businesses and individuals.

Micro lending is the practice of providing small loans to individuals or small businesses that lack access to traditional banking services. These loans are typically offered by microfinance institutions (MFIs), non-banking financial companies (NBFCs), and digital platforms, aiming to promote financial inclusion and support entrepreneurship among underserved populations.

Demand for micro-lending services has surged, especially in developing economies with limited access to traditional banks. SMEs, which make up a large share of these markets, often face funding barriers due to strict collateral and credit requirements. Micro-lending bridges this gap with customized financial solutions, driving entrepreneurship and job creation.

Technological advancements have been key to the evolution of micro-lending. AI, machine learning, and digital platforms have streamlined processes, allowing faster loan approvals and disbursements. Smartphone-based apps use alternative data for credit scoring, expanding access to credit for those without traditional credit histories.

The regulatory environment has also evolved to support the growth of micro lending. In India, initiatives like the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) provide collateral-free credit to micro and small enterprises, fostering entrepreneurship and economic development . Such policies have encouraged the participation of various financial entities in the micro lending space, including NBFCs and

The micro-lending sector offers abundant investment opportunities, especially in emerging markets with large unbanked populations. The growth of P2P lending platforms attracts investors seeking high returns and financial inclusion. Impact investing is also rising, with a focus on achieving social and environmental benefits alongside financial gains.

Businesses engaging in micro lending benefit from a vast and underserved market, the potential for high repayment rates, and the opportunity to leverage technology for operational efficiency. Moreover, by addressing the credit needs of micro and small enterprises, these businesses contribute to job creation and economic growth.

Key Takeaways

- In 2024, the Global Micro Lending Market was valued at USD 207.1 billion and is expected to reach USD 588 billion by 2034, growing at a CAGR of 11.00% during 2025–2034.

- In the same year, Microfinance Institutions (MFIs) held a leading position in the market, accounting for over 54% of the global share.

- Short-Term Loans (≤12 months) dominated the product segment in 2024, capturing more than 56% of the global market share.

- The Small Enterprises segment led the end-user category in 2024, holding over 40% of the global market.

- Asia-Pacific emerged as the top regional market in 2024, with a share of over 45%, generating around USD 93.1 billion in revenue.

- Within Asia-Pacific, China’s micro-lending market alone was valued at USD 30.5 billion in 2024, with a CAGR of 8.2%, driven by strong demand from small businesses and individuals seeking flexible credit.

Business Benefits

Micro-lending opens doors for small businesses that often can’t get traditional bank loans. These loans help businesses with needs like working capital, inventory, or equipment, supporting those who might otherwise have trouble securing funding. According to Fit Small Business report, 77% of microloan recipients report an increase in their savings balance after receiving a loan.

Access to microloans can lead to significant revenue growth for small businesses. A study by the Aspen Institute revealed that businesses benefiting from microloans saw their revenues soar by an average of 29% in just the first year. This financial boost helps businesses expand their operations and invest in new opportunities.

Micro-lending programs often include financial education, helping business owners manage their finances better. According to a survey by 60 Decibels Microfinance Index 2024, 91% of clients using microfinance services reported greater confidence in managing their finances, compared to 82% without such support. This empowerment leads to more sustainable business practices.

Government Initiatives

India, A cornerstone of government-led micro-lending is the Pradhan Mantri Mudra Yojana (PMMY), which continues to offer collateral-free loans up to ₹10 lakh for non-corporate, non-farm small businesses. In 2025, the scheme remains accessible through banks, NBFCs, and microfinance institutions, with a focus on promoting self-employment and financial inclusion, especially in rural and underserved areas.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) offers collateral-free credit up to ₹2 crore, with guarantee coverage ranging from 50% to 85%, supporting easier access to finance for small businesses.

Thailand government approved a 100 billion baht ($2.8 billion) soft loan scheme to assist small businesses in obtaining loans at subsidized interest rates. Administered through the state-owned Government Savings Bank, this program provides liquidity to commercial banks at 0.01% interest, enabling them to offer loans to small businesses at a maximum of 3.5% per annum.

Ghana Development Bank Ghana (DBG), established in 2021, focuses on providing indirect loans to SMEs. Supported by grants and loans from international institutions like the African Development Bank and the World Bank Group, DBG aims to foster collaborations that support economic growth and job creation.

China Market Analysis

In 2024, the China micro lending market was valued at USD 30.5 billion, reflecting the country’s growing shift towards alternative financial services. This growth stems from the unmet credit needs of underserved groups, such as small businesses, low-income individuals, and rural communities, which traditional banks often hesitate to serve due to strict collateral requirements and lengthy processing times.

The market is expanding at a compound annual growth rate (CAGR) of 8.2%, and this momentum is being sustained by the digital transformation of lending services across China. Key players in the space are heavily investing in artificial intelligence, mobile lending apps, and real-time risk assessment tools to streamline loan disbursement and reduce defaults.

The rise of small and micro enterprises (SMEs) in sectors like retail and logistics has increased demand for short-term working capital loans. Businesses prefer microloans for their fast approval, minimal paperwork, and flexible repayment. Partnerships between digital platforms like Alipay and WeChat Pay and micro-lending services have created a personalized loan ecosystem, driving growth and attracting new investments in China’s micro-lending sector.

In 2024, Asia-Pacific held a dominant market position, capturing more than 45% of the global micro lending market, with total revenue reaching approximately USD 93.1 billion. This leadership can be attributed to the region’s large unbanked population, high mobile penetration, and widespread digital transformation.

A key driver of Asia-Pacific’s dominance is the active role of governments in promoting financial inclusion through digital public infrastructure for micro and small businesses. In China, government support for peer-to-peer (P2P) micro-lending has filled gaps left by traditional banks. These initiatives have built trust in micro-lending ecosystems and encouraged borrowers to adopt formal, tech-enabled credit systems.

The Asia-Pacific market thrives on a dynamic fintech landscape, with startups, telecom providers, and e-commerce platforms integrating micro-lending services. In Indonesia, ride-hailing platforms offer loans to drivers, while in Vietnam and Thailand, microcredit is provided through embedded APIs in retail apps. These models are gaining popularity for their contextual credit, flexible repayments, and AI-driven risk profiling.

Cultural acceptance of informal borrowing has paved the way for micro-lending adoption in Asia-Pacific. The shift from traditional moneylenders to regulated, digital micro-lenders is accelerating, driven by tech-savvy younger populations seeking quick financing. As regulatory frameworks evolve, Asia-Pacific is poised to remain a leader in micro-lending innovation and volume.

Type Analysis

In 2024, Microfinance Institutions (MFIs) segment held a dominant market position, capturing more than a 54% share of the global micro lending market. This leadership can be attributed to the strong grassroots presence of MFIs in low-income and rural communities, where formal banking services are often inaccessible.

Unlike commercial banks and NBFCs, MFIs are structurally designed to serve the bottom-of-the-pyramid population with minimal collateral requirements and flexible repayment structures. Their ability to operate in remote areas and cater to individuals who lack credit histories has created a strong niche, which continues to grow with digital support systems.

Many MFIs are embracing digital tools such as mobile loan disbursement, biometric verification, and AI-powered credit scoring to streamline operations. This adoption improves efficiency, enabling faster processing and lower administrative costs. Additionally, MFIs are reaching mobile-first borrowers with user-friendly apps and SMS services, increasing accessibility and decreasing reliance on physical branches.

Government support and international funding for financial inclusion programs have also played a critical role in strengthening the position of MFIs. Regulatory frameworks in several emerging economies are designed to favor and empower MFIs through subsidies, priority lending norms, and capacity-building programs.

Loan Duration Analysis

In 2024, Short-Term Loans (≤12 months) segment held a dominant market position, capturing more than a 56% share of the global micro lending market. This strong position can be largely attributed to the high demand among micro-entrepreneurs, informal workers, and small traders who often require quick financial assistance to manage day-to-day cash flows.

These short-term loans are preferred for their quick disbursal process, minimal documentation requirements, and flexible repayment terms, which make them ideal for borrowers with limited or no formal credit history. As a result, this segment has become the most accessible and widely adopted form of microfinance across emerging economies.

Short-term micro loans are especially attractive in densely populated developing countries, where small business owners seek immediate funds to cover inventory purchases, equipment repairs, or seasonal demand fluctuations. The rapid turnaround time between loan application and approval further strengthens its appeal, helping borrowers avoid income disruption.

The dominance of the segment is also driven by lower risk exposure for lenders. Short-term loans, repaid within months, help microfinance institutions and P2P platforms maintain high liquidity and reduce default risks. This has attracted more private investors and digital lenders, increasing capital availability and fueling growth in the short-duration loan market.

End User Analysis

In 2024, the Small Enterprises segment held a dominant market position, capturing more than 40% share of the global micro lending market. This leadership is driven by the rising number of small businesses in emerging and developing economies that face challenges in accessing traditional bank loans due to lack of collateral, lengthy procedures, or limited credit history.

The digitalization of small business operations has further bolstered the segment’s dominance. With small enterprises using mobile payments, e-commerce, and digital accounting tools, lenders can access real-time data to assess creditworthiness and customize loan offers. These fintech innovations have lowered borrowing barriers and advanced financial inclusion at the grassroots level.

A key factor in the small enterprise segment’s strength is the supportive policy environment. Government schemes and credit guarantee funds have enabled micro-lenders to offer unsecured loans with lower risk. In countries like India, Brazil, and Kenya, micro-lending platforms are partnering with public agencies and banks to create hybrid financing models, blending private capital with government-backed guarantees to make microloans more scalable and secure.

Small enterprises, key job creators in local communities, are a priority for inclusive finance initiatives. Microloans to these businesses support entrepreneurship and broader economic development. With strong demand, technological advancements, and policy backing, the small enterprise segment will continue to dominate and shape the global micro-lending market.

Key Market Segments

By Type

- Banks

- Microfinance Institute (MFI)

- Non-Banking Financial Institutions (NBFC)

By Loan Duration

- Short-Term Loans (up to 12 months)

- Medium-Term Loans (1 to 3 years)

- Long-Term Loans (more than 3 years)

By End User

- Small Enterprises

- Solo Entrepreneurs

- Micro Entrepreneuers

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Digital Transformation Enhancing Financial Inclusion

The proliferation of digital technologies has significantly propelled the growth of micro-lending by enhancing financial inclusion. Mobile banking platforms and digital payment systems have bridged the gap between traditional financial institutions and underserved populations, particularly in remote and rural areas.

By leveraging technology, micro-lenders can offer services with greater efficiency and at reduced operational costs. This digital shift not only streamlines loan disbursement and repayment processes but also facilitates better tracking and management of financial transactions. Consequently, individuals who previously lacked access to formal financial services can now participate in the financial ecosystem, fostering economic empowerment and entrepreneurship.

Restraint

High Interest Rates and Over-Indebtedness

A significant restraint in the micro-lending sector is the prevalence of high interest rates, which can lead to over-indebtedness among borrowers. The operational costs associated with servicing small loans are relatively high, prompting lenders to charge elevated interest rates to maintain profitability.

For borrowers with limited income, these rates can be burdensome, potentially leading to a cycle of debt where new loans are taken to repay existing ones. This situation is exacerbated in areas lacking stringent regulatory frameworks, where predatory lending practices may occur. The resultant financial stress can negate the intended benefits of micro-lending, undermining efforts toward poverty alleviation and financial inclusion.

Opportunity

Integration of Micro-Insurance Products

The integration of micro-insurance products presents a substantial opportunity for the micro-lending sector. By offering insurance services tailored to low-income individuals, micro-lenders can provide a safety net that protects borrowers against unforeseen events such as health emergencies or natural disasters.

This not only enhances the financial resilience of clients but also mitigates the risk of loan defaults due to unexpected hardships. Furthermore, bundling insurance with micro-loans can diversify the product offerings of microfinance institutions, potentially attracting a broader client base and fostering long-term customer relationships. Such integrated services can contribute to the sustainability and scalability of micro-lending operations.

Challenge

Regulatory Compliance and Risk Management

Navigating the complex landscape of regulatory compliance and risk management poses a significant challenge for micro-lenders. As the sector expands, institutions must adhere to varying legal and regulatory requirements across different jurisdictions, which can be resource-intensive and complicated.

Ensuring compliance involves implementing robust internal controls, conducting regular audits, and maintaining transparency in operations. Additionally, micro-lenders must effectively manage credit risk, especially when dealing with clients who have limited or no credit history. Balancing the need for financial inclusion with prudent risk management practices is critical to maintaining the integrity and stability of micro-lending institutions.

Emerging Trends

One significant trend is the rise of digital lending platforms. These platforms use alternative data sources, such as mobile usage and transaction history, to assess creditworthiness, enabling lenders to reach individuals without traditional credit histories. This approach is particularly beneficial in developing regions where many people lack access to formal banking services.

Another notable development is the integration of artificial intelligence (AI) and machine learning in credit assessment. By analyzing vast amounts of data, AI can provide more accurate risk evaluations, allowing lenders to offer loans to a broader range of borrowers while managing default risks effectively.

Furthermore, there’s a growing emphasis on social impact investing within micro lending. Investors are increasingly interested in funding ventures that not only yield financial returns but also contribute positively to society. This shift encourages the development of microfinance initiatives aimed at empowering marginalized communities and fostering sustainable economic growth.

Key Player Analysis

The micro lending market has been growing rapidly in recent years as more individuals and small businesses seek quick and easy access to funds.

Accion International is a leading nonprofit organization in the micro lending space. Accion stands out for its global work in emerging markets, combining microloans with financial education and business support. This holistic approach empowers low-income individuals and small businesses to achieve long-term success, not just short-term relief.

Bluevine Inc. has made its mark with a tech-first approach to small business financing. Known for speed and flexibility, Bluevine offers lines of credit and term loans that can be accessed online, with quick approval processes. Their unique selling point is how they blend technology with customer service, offering fast funding while still maintaining a personal touch.

Fundera Inc., now a part of NerdWallet, operates as a loan marketplace rather than a direct lender. Fundera stands out by connecting small businesses with the best-fit lenders from a wide network, simplifying loan comparisons. Its transparent, convenient model makes it a top choice for business owners seeking multiple financing options in one place.

Top Key Players in the Market

- Accion International

- Bluevine Inc.

- Fundera Inc.

- Funding Circle

- Kabbage Inc.

- American Express

- OnDeck

- Fundbox

- LendingClub Bank

- Zopa Bank Limited

- Others

Top Opportunities for Players

The micro-lending industry is undergoing a significant transformation, driven by digital innovation, supportive policies, and the growing financial needs of underserved communities.

- Digital Lending for MSMEs: MSMEs are increasingly seeking credit from NBFCs, which offer faster, more accessible digital loans as traditional banks often fail to meet their needs. This shift is creating a robust avenue for micro-lenders to expand their reach and support the backbone of the economy.

- Fintech and AI Integration: Artificial intelligence (AI) and machine learning (ML) are transforming credit assessment by leveraging alternative data like mobile usage and transaction history to more accurately determine creditworthiness. This technological advancement enables micro-lenders to extend credit to individuals lacking traditional credit histories, thereby broadening financial inclusion.

- Supportive Regulatory Environment: Recent regulatory changes, including the easing of capital requirements by the Reserve Bank of India (RBI), are fostering a more conducive environment for micro-lending. These reforms are enhancing the operational flexibility of NBFCs and microfinance institutions, allowing them to better serve their target markets and expand their lending portfolios.

- Focus on Women’s Financial Empowerment: Empowering women through micro-lending has demonstrated significant socio-economic benefits. Women are more likely to invest in their families and communities, leading to broader developmental impacts. Targeted lending programs that address the unique needs of women entrepreneurs can unlock new markets and contribute to gender equity in financial services.

- Expansion into Rural and Agricultural Sectors: There is a substantial unmet demand for financial services in rural and agricultural communities. Micro-lenders can tap into this opportunity by offering tailored financial products that address the specific needs of farmers and rural entrepreneurs.

Recent Developments

- In September 2024, Accion invested in FlexiLoans, contributing to a $34.5 million funding round aimed at supporting Indian MSMEs, particularly in Tier 2 and Tier 3 cities.

- In November 2023, Funding Circle and Atom Bank announced a new lending partnership aimed at providing GBP ~150 million (USD 180.88 million) in fresh funding to small businesses. This initiative builds on their existing collaboration, which had already facilitated GBP 350 million (USD 422.4 million) in lending through the Funding Circle platform.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 207.1 Bn |

| Forecast Revenue (2034) | USD 588 Bn |

| CAGR (2025-2034) | 11.00% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Type (Banks, Microfinance Institute (MFI), Non-Banking Financial Institutions (NBFC)), By Loan Duration (Short-Term Loans (up to 12 months), Medium-Term Loans (1 to 3 years), Long-Term Loans (more than 3 years)), By End User (Small Enterprises, Solo Entrepreneurs, Micro Entrepreneuers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Accion International, Bluevine Inc., Fundera Inc., Funding Circle, Kabbage Inc., American Express, OnDeck, Fundbox, LendingClub Bank, Zopa Bank Limited, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |