Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By End-User Vertical Analysis

- By Deployment Mode Analysis

- By Application Analysis

- By Measurement Device Type Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

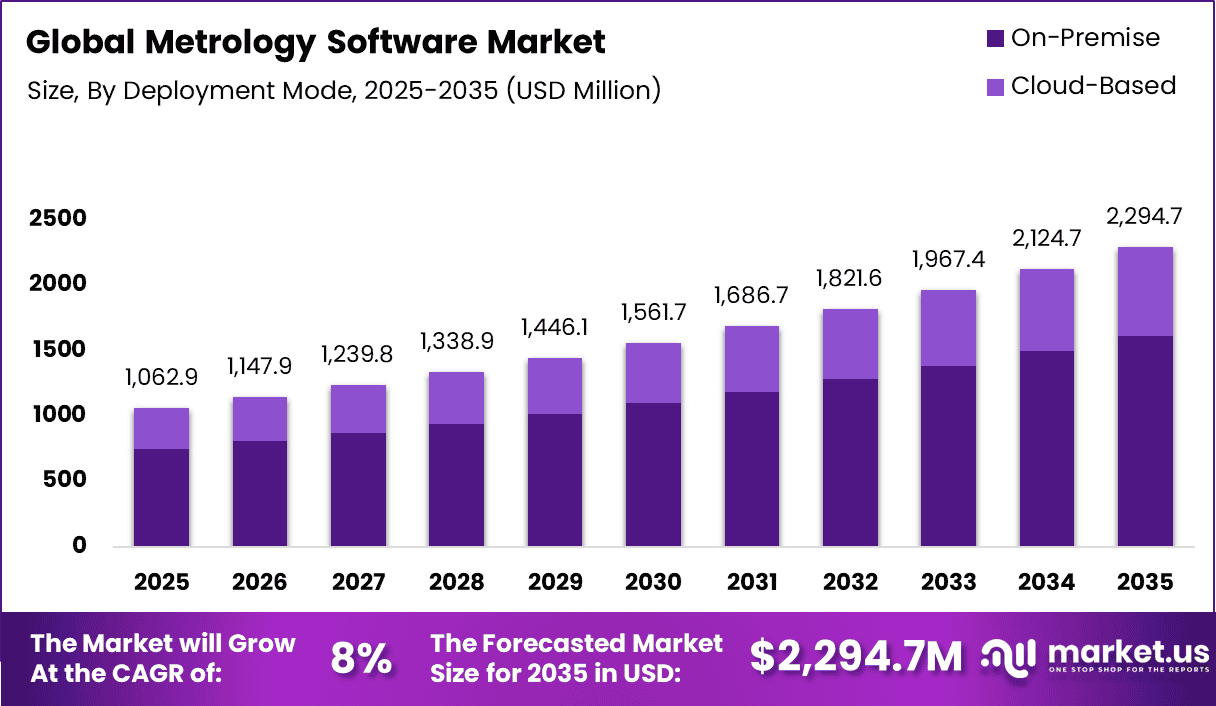

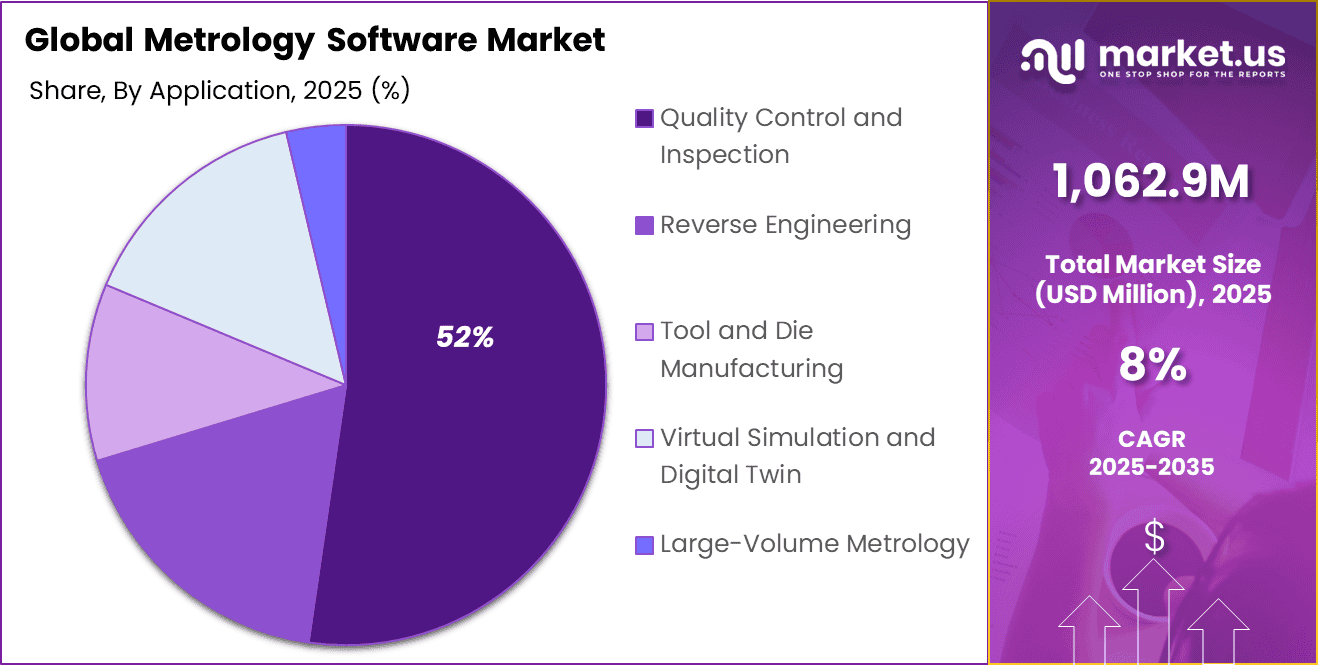

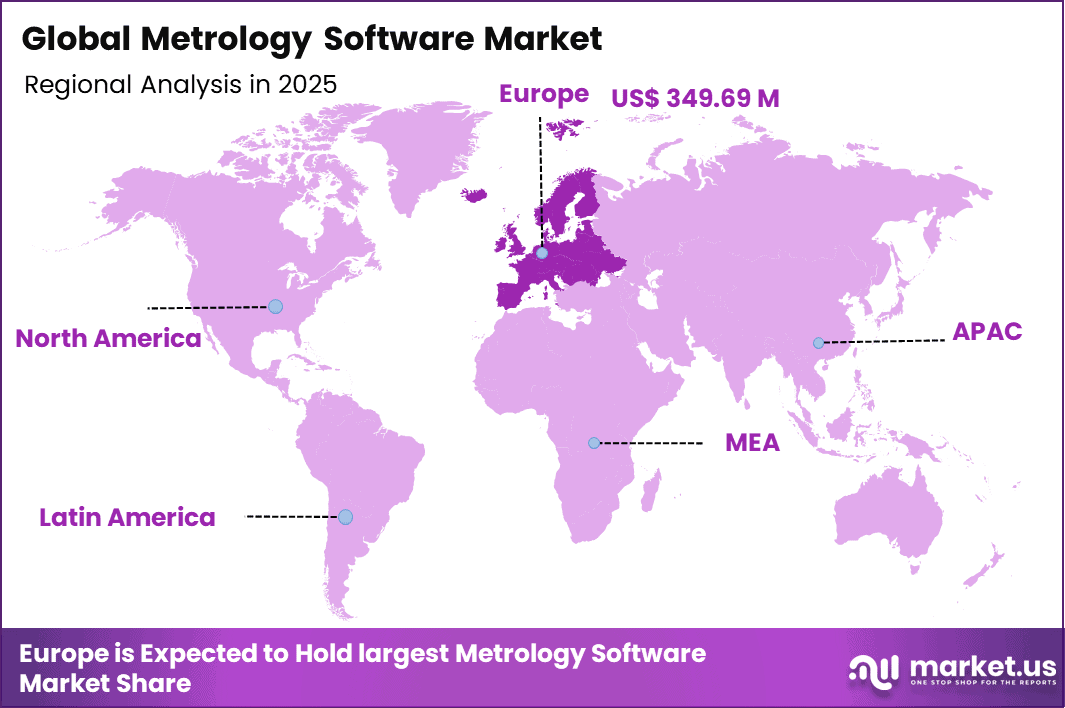

The Global Metrology Software Market generated USD 1,062.9 million in 2025 and is predicted to register growth from USD 1,147.9 million in 2026 to about USD 2,294.7 million by 2035, recording a CAGR of 8% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 32.9% share, holding USD 349.69 Million revenue.

Top Market Takeaways

- Automotive end-user vertical commands 34.7%, enabling dimensional analysis for engine components, body panels, and assembly tolerances to meet stringent safety standards.

- On-premises deployment dominates at 70.4%, providing data sovereignty, real-time processing, and integration with factory floor hardware for mission-critical operations.

- Quality control and inspection application captures 52.3%, automating defect detection, statistical process control, and traceability reporting across production lines.

- Coordinate measuring machines hold 30.8% by device type, leveraging advanced algorithms for non-contact probing, feature extraction, and GD&T compliance verification.

- Europe drives 32.9% global value, with Germany at USD 49.7 million and 6.5% CAGR, fueled by automotive OEMs and Industry 4.0 metrology advancements.

Metrology software is used to measure, analyze, and manage dimensional data in manufacturing and engineering processes. It works with inspection equipment such as coordinate measuring machines, laser scanners, and vision systems to ensure that products meet design specifications.

As production becomes more precise and quality requirements become stricter, this software is helping organizations maintain consistency and reduce defects. It also supports digital workflows by connecting measurement data with design and production systems, making quality control more efficient and traceable.

One of the main driving factors is the increasing need for high precision manufacturing across industries such as automotive, aerospace, and electronics. As product designs become more complex, companies require accurate measurement tools to ensure each component meets exact standards.

In addition, the shift toward automation and smart manufacturing is encouraging the use of software that can process large volumes of measurement data quickly. The focus on reducing waste and improving product quality is also pushing organizations to adopt better inspection and analysis solutions. Integration with computer aided design and manufacturing systems is further strengthening the role of metrology software in production environments.

Demand for metrology software is rising as manufacturers look for reliable and efficient ways to manage quality control. There is a strong preference for solutions that can handle different types of measurement data and provide clear analysis for decision making. Companies are also seeking software that can integrate with existing production systems and support automated inspection processes.

The demand is particularly strong in industries where precision and compliance are critical. As manufacturing continues to evolve toward more advanced and connected systems, the need for accurate and user friendly metrology solutions is expected to grow steadily.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Increasing demand for precision manufacturing and quality control | +2.9% | North America, Europe, Asia Pacific | Medium to long term | Quality standards drive software adoption |

| Growth in automotive and aerospace industries | +2.6% | Developed markets | Medium to long term | Complex components require accurate measurement |

| Rising adoption of automation and Industry 4.0 practices | +2.4% | Global | Medium term | Automation increases need for digital metrology |

| Expansion of 3D measurement and inspection technologies | +2.2% | Global | Medium term | Advanced inspection tools boost demand |

| Integration of metrology with digital manufacturing workflows | +2.0% | Global | Medium to long term | Enhances production efficiency |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High cost of advanced metrology software solutions | -2.3% | Emerging markets | Short to medium term | Cost limits small-scale adoption |

| Complexity in software operation and training requirements | -2.0% | Global | Medium term | Skill requirements slow usage |

| Integration challenges with legacy manufacturing systems | -1.7% | Global | Medium term | Compatibility issues arise |

| Limited awareness among small and medium enterprises | -1.5% | Developing regions | Medium term | Adoption remains low |

| Dependence on high-end hardware compatibility | -1.3% | Global | Long term | Hardware constraints affect performance |

By End-User Vertical Analysis

The automotive segment accounted for 34.7% of the market share, reflecting its strong reliance on precise measurement and inspection processes. This dominance is supported by the need to maintain strict quality standards in vehicle manufacturing, where even minor deviations can impact performance and safety. Metrology software helps manufacturers ensure dimensional accuracy and consistency across components, improving overall production quality.

Another factor driving this segment is the increasing complexity of automotive designs and the use of advanced materials. Manufacturers are adopting digital measurement solutions to support high-precision production and reduce defects. The integration of metrology software with production systems also enhances efficiency and supports continuous quality improvement.

By Deployment Mode Analysis

The on-premises segment held 70.4% share, driven by the need for secure and controlled data management in industrial environments. Organizations prefer on-premises deployment to maintain full control over sensitive measurement data and ensure compliance with internal standards. This approach also allows for better customization and integration with existing manufacturing systems.

In addition, industries with critical operations require stable and reliable systems that are not dependent on external connectivity. On-premises solutions provide consistent performance and reduce the risk of data breaches or downtime. This has reinforced their adoption in sectors where data security and operational reliability are essential.

By Application Analysis

The quality control and inspection segment captured 52% of the market, driven by the increasing focus on maintaining high production standards. Metrology software plays a key role in detecting defects, verifying product dimensions, and ensuring compliance with specifications. These capabilities help manufacturers reduce waste and improve product reliability.

Furthermore, the growing demand for precision manufacturing has increased the importance of accurate inspection processes. Companies are investing in advanced software tools to automate quality checks and improve efficiency. This supports better decision-making and enhances overall production performance.

By Measurement Device Type Analysis

The coordinate measuring machines segment accounted for 30.8% of the market share, reflecting their widespread use in precision measurement applications. CMM devices are known for their high accuracy and ability to measure complex geometries, making them essential in industries that require detailed inspection. Metrology software enhances their functionality by enabling data analysis and reporting.

Additionally, the integration of software with CMM systems allows for automated measurement processes and improved workflow efficiency. This reduces manual errors and ensures consistent results across different production stages. The growing adoption of advanced measurement technologies continues to support the demand for CMM-based metrology solutions.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Moderate to high | High | US, Europe | Investing in industrial software startups |

| Private equity firms | Moderate | Moderate | North America and Europe | Scaling precision manufacturing solutions |

| Corporate investors | High | Moderate | Global | Strategic investments in digital manufacturing |

| Institutional investors | Moderate | Low to moderate | Developed markets | Prefer stable industrial technology firms |

| Government and public funding bodies | Moderate to high | Low | Global | Supporting advanced manufacturing initiatives |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| AI-driven measurement and inspection systems | +3.1% | US, Europe | Medium to long term | Improves accuracy and efficiency |

| Cloud-based metrology platforms | +2.7% | Global | Short to medium term | Enables centralized data access |

| Integration with CAD/CAM systems | +2.5% | Global | Medium term | Streamlines design and inspection |

| 3D scanning and imaging technologies | +2.3% | Global | Medium to long term | Enhances measurement precision |

| Real-time data analytics and reporting tools | +2.0% | Global | Medium term | Supports faster decision-making |

Key Challenges

- High cost of software and setup makes it difficult for small companies to adopt.

- Complex software features require skilled professionals to operate.

- Integration challenges with existing measurement and production systems.

- Data accuracy issues if inputs or calibration are not correct.

- Lack of standardization across different industries and tools.

- Frequent updates and maintenance requirements increase workload.

- Compatibility issues with different hardware and devices.

- Resistance to change from traditional measurement methods.

- Data security concerns when handling sensitive industrial data.

- Difficulty in managing large volumes of measurement data.

Emerging Trends

The metrology software market is moving toward more intelligent and connected measurement systems that support higher precision and faster decision making in industrial environments. One key emerging trend is the integration of advanced analytics and AI within metrology platforms, allowing automatic detection of defects and deviations during inspection processes. This is reducing manual intervention and improving consistency in quality control.

Another important trend is the shift toward real time data integration, where metrology software connects directly with production systems to provide instant feedback during manufacturing. There is also growing adoption of 3D measurement and visualization tools, enabling detailed analysis of complex components across industries such as automotive and aerospace. In addition, cloud enabled metrology platforms are gaining traction, allowing centralized data management and easier collaboration across multiple sites. The use of digital twins is also becoming more common, helping manufacturers simulate and validate product quality before physical production.

Growth Factors

The growth of this market is driven by the increasing need for high precision and strict quality standards in manufacturing processes. As products become more complex, ensuring accuracy at every stage of production has become critical, which is encouraging the use of advanced metrology software. The expansion of automated and smart manufacturing environments is also supporting demand, as these systems require continuous measurement and validation.

Another major factor is the need to reduce production errors and material waste, which directly impacts operational efficiency. Manufacturers are also focusing on improving traceability and compliance with industry regulations, further driving adoption of digital measurement solutions. Additionally, the push toward Industry 4.0 is encouraging the integration of metrology software with broader digital ecosystems, enabling better data flow, improved process control, and more informed decision making across the production lifecycle.

Key Market Segments

By End-User Vertical

- Automotive

- Aerospace

- Electronics Manufacturing

- Energy and Power

- Medical Devices

- Other End-User Verticals

By Deployment Mode

- On-Premise

- Cloud-Based

By Application

- Quality Control and Inspection

- Reverse Engineering

- Tool and Die Manufacturing

- Virtual Simulation and Digital Twin

- Large-Volume Metrology

By Measurement Device Type

- Coordinate Measuring Machines (CMM)

- Optical Digitizers and Scanners

- Portable Arms

- Laser Trackers

- Structured Light Scanners

- Other Measurement Device Types

Regional Analysis

Europe accounted for 32.9% of the Metrology Software market, supported by the region’s strong industrial base and focus on precision manufacturing. Countries across Europe emphasize quality control and standardization, which has increased the adoption of advanced measurement and inspection software.

Industries such as automotive, aerospace, and industrial machinery are increasingly relying on metrology solutions to ensure product accuracy and compliance with strict regulatory standards. The growing shift toward digital manufacturing and automation is also encouraging the integration of software-driven measurement systems, improving efficiency and reducing production errors.

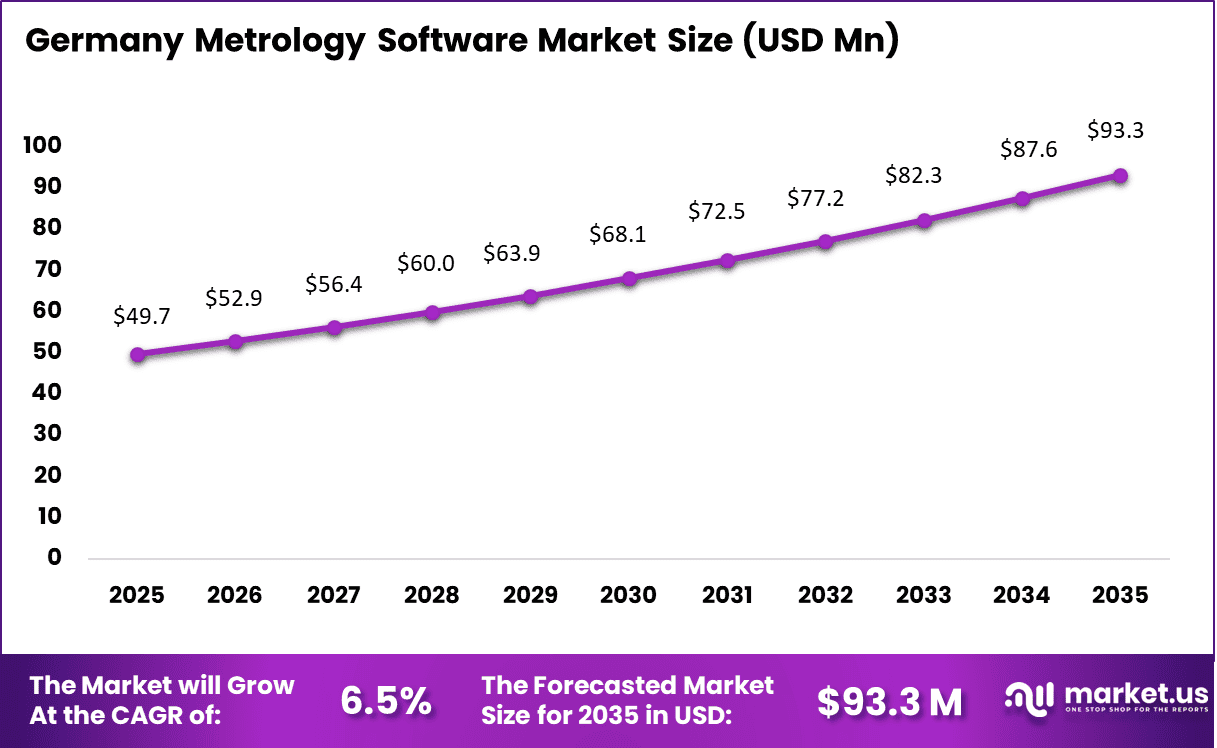

Germany market reached USD 49.7 Million and is projected to grow at a CAGR of 6.5%, driven by its leadership in high-precision engineering and manufacturing excellence. The country has a strong presence of automotive and industrial equipment manufacturers that require accurate measurement and quality assurance processes.

Companies are adopting metrology software to support advanced production techniques and maintain consistency in complex manufacturing environments. In addition, increasing focus on Industry 4.0 practices and smart factory initiatives is expected to support steady growth of the metrology software market in Germany over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Metrology Software Market is driven by a mix of precision measurement companies and advanced software providers. Companies such as Carl Zeiss AG, Hexagon AB, Renishaw plc, Nikon Metrology NV, and FARO Technologies Inc. focus on integrated metrology solutions that combine hardware and software for accurate measurement and quality control.

These players emphasize high precision, automation, and compatibility with industrial equipment used in manufacturing sectors such as automotive and aerospace. Their strong expertise in measurement technologies and global presence help them maintain a leading position in the market.

At the same time, software-focused companies such as Autodesk Inc., Dassault Systèmes SE, InnovMetric Software Inc., Verisurf Software Inc., and Metrologic Group SA (Sandvik AB) provide advanced platforms for 3D inspection, data analysis, and reporting. Companies like Creaform Inc. (AMETEK Inc.), Perceptron Inc. (Atlas Copco AB), Fluke Corporation, LK Metrology Ltd., Mapvision Ltd., GOM GmbH (Carl Zeiss AG), Capture 3D LLC, Stratasys Ltd. (Control Software), and Software Point Oy also compete by offering specialized and application-specific solutions. Competition in this market is driven by accuracy, ease of integration with manufacturing systems, and the ability to handle complex 3D measurement data efficiently.

Top Key Players in the Market

- Nikon Metrology NV

- 3D Systems Corporation

- Creaform Inc. (AMETEK Inc.)

- FARO Technologies Inc.

- Carl Zeiss AG

- Hexagon AB

- LK Metrology Ltd.

- Renishaw plc

- Perceptron Inc. (Atlas Copco AB)

- InnovMetric Software Inc.

- Fluke Corporation

- Metrologic Group SA (Sandvik AB)

- Autodesk Inc.

- Dassault Systèmes SE

- Verisurf Software Inc.

- Mapvision Ltd.

- GOM GmbH (Carl Zeiss AG)

- Capture 3D LLC

- Stratasys Ltd. (Control Software)

- Software Point Oy

- Others

Future Outlook

The future outlook for the Metrology Software Market looks strong as industries continue to focus on precision, quality control, and automation in manufacturing processes. The market is expected to grow with increasing use of advanced measurement and inspection tools across sectors like automotive, aerospace, and electronics. Companies are anticipated to adopt metrology software to improve accuracy, reduce errors, and meet strict quality standards. In the coming years, integration with AI, cloud platforms, and digital manufacturing systems is expected to enhance data analysis and real-time decision making, making metrology software a key part of modern industrial operations.

Recent Developments

March, 2026 – Nikon launches NEXIV AutoMeasure software automating CMM programming for VMZ-S series. One-click measurement creation cuts setup 70% while AI edge detection handles shiny surfaces. Video measure mode speeds 2D inspections.

January, 2026 – Creaform VXelements 9 adds dynamic referencing for handheld scanners. Real-time alignment while mesh-to-CAD comparison reports deviations instantly. Portable metrology standard.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,062.9 Million |

| Forecast Revenue (2035) | USD 2,294.7 Million |

| CAGR(2025-2035) | 8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By End-User Vertical (Automotive, Aerospace, Electronics Manufacturing, Energy and Power, Other End-User Verticals), By Deployment Mode (On-Premise, Cloud-Based), By Application (Quality Control and Inspection, Reverse Engineering), By Measurement Device Type (Coordinate Measuring Machines (CMM), Optical Digitizers and Scanners, Portable Arms, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Nikon Metrology NV, 3D Systems Corporation, Creaform Inc. (AMETEK Inc.), FARO Technologies Inc., Carl Zeiss AG, Hexagon AB, LK Metrology Ltd., Renishaw plc, Perceptron Inc. (Atlas Copco AB), InnovMetric Software Inc., Fluke Corporation, Metrologic Group SA (Sandvik AB), Autodesk Inc., Dassault Systèmes SE, Verisurf Software Inc., Mapvision Ltd., GOM GmbH (Carl Zeiss AG), Capture 3D LLC, Stratasys Ltd. (Control Software), Software Point Oy, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |