Global Makeup Market Size, Share, Growth Analysis By Product (Powders, Gels, Lotions, Others), By Application Area (Face, Lips, Eyes, Nails), By Distribution Channel (Supermarkets and Hypermarkets, Exclusive Brand Stores, Online/E-Commerce Channels, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181798

- Number of Pages: 257

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

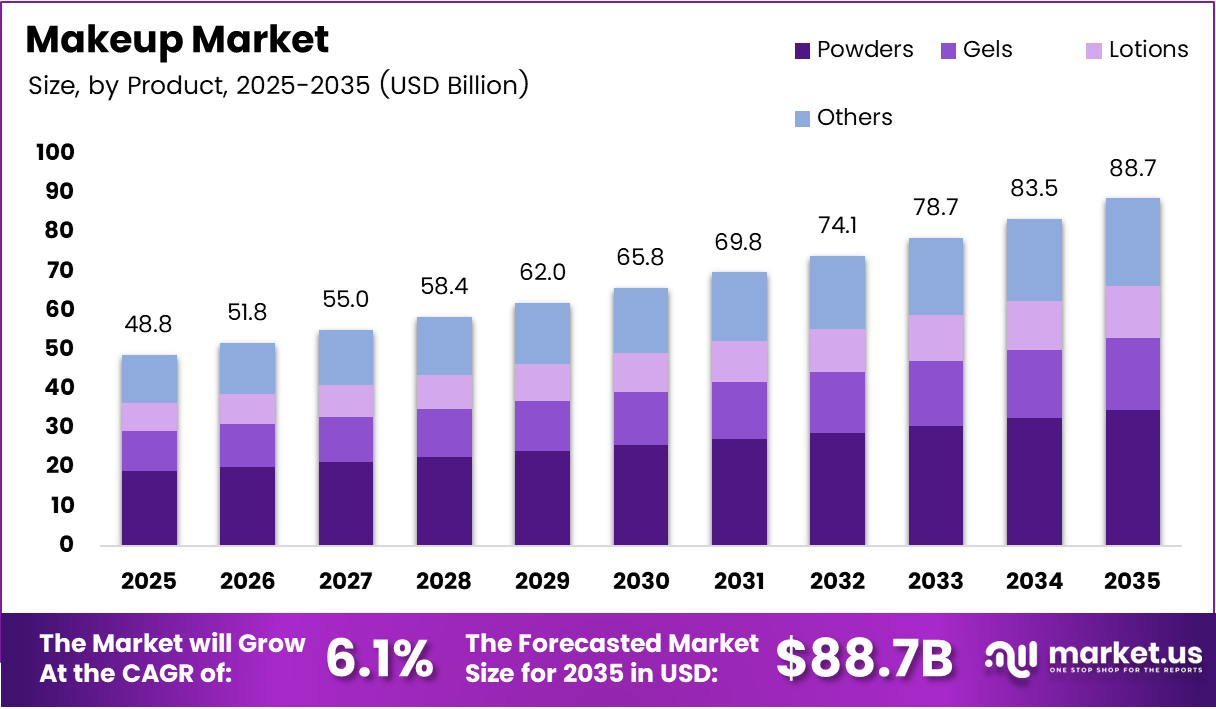

Global Makeup Market size is expected to be worth around USD 88.7 Billion by 2035 from USD 48.8 Billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

The global makeup market spans color cosmetics formulated for face, lip, eye, and nail application. Products range from mass-market powders and lotions to premium skin-tinted gels and hybrid skincare-cosmetic hybrids. This breadth of formats allows the market to serve consumers across income levels, cultural preferences, and beauty philosophies simultaneously.

Consumer behavior is shifting away from passive product use toward active self-expression. Younger demographics treat color cosmetics as identity tools, not just enhancement aids. This behavioral shift expands purchase frequency and average basket size, which directly supports the revenue trajectory from USD 48.8 billion in 2025 toward the forecast ceiling.

Social media platforms amplify product discovery cycles far beyond traditional retail. Influencer demonstrations and celebrity endorsements compress the time between trend emergence and purchase intent. Brands that invest in creator partnerships gain faster market penetration than those relying solely on conventional advertising channels.

E-commerce infrastructure now enables brands to reach consumers in geographies where physical retail remains underdeveloped. This digital access layer is especially important for emerging markets, where a growing middle class seeks international beauty brands but lacks proximity to specialty stores or department counters.

In May 2025, e.l.f. Beauty acquired Hailey Bieber’s skincare and color cosmetics brand Rhode for approximately $1 billion, with Bieber retained as chief creative officer. This transaction signals that celebrity-anchored brand equity now commands acquisition premiums that rival established legacy labels — a structural shift in how the industry values consumer loyalty.

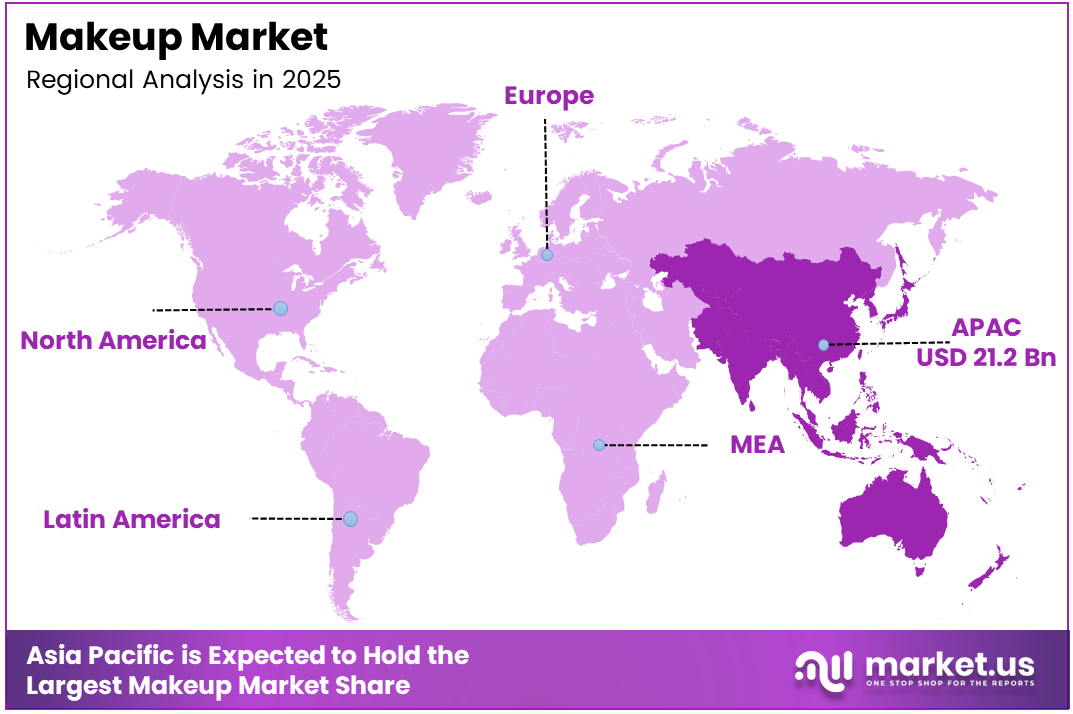

According to market data, Asia Pacific holds a 43.50% share of the global makeup market, valued at USD 21.2 Billion. This concentration reflects the region’s scale of middle-class expansion, strong beauty culture across China, Japan, South Korea, and India, and the outsized role of K-beauty and J-beauty trends in shaping global formulation standards.

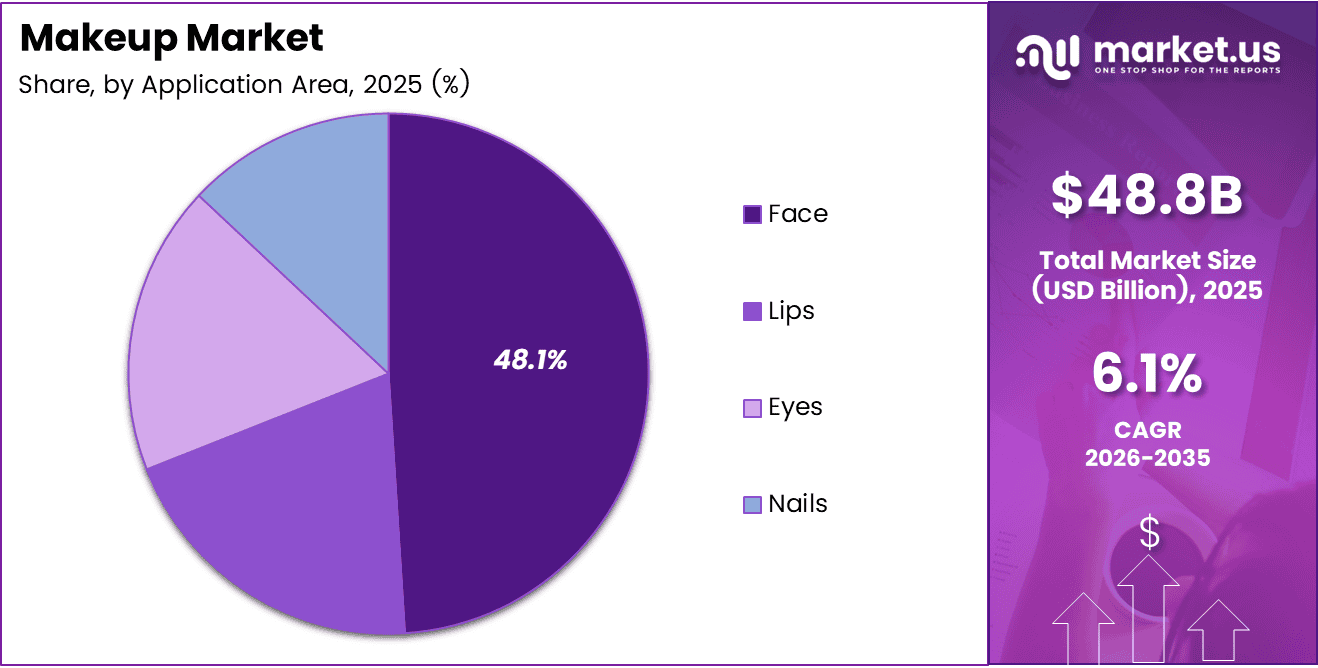

The face application area commands 48.1% of product demand by application. This dominance tells a clear story: consumers prioritize complexion products — foundations, concealers, powders — above all other categories, making face the highest-volume and most contested segment for brand competition and product innovation investment.

Key Takeaways

- The global makeup market was valued at USD 48.8 Billion in 2025 and is forecast to reach USD 88.7 Billion by 2035.

- The market advances at a CAGR of 6.1% during the forecast period 2026 to 2035.

- By product, Powders lead with a 38.5% market share, followed by Gels, Lotions, and Others.

- By application area, Face dominates with a 48.1% share, followed by Lips, Eyes, and Nails.

- By distribution channel, Supermarkets and Hypermarkets hold the largest share at 37.4%, followed by Exclusive Brand Stores, Online/E-Commerce Channels, and Others.

- Asia Pacific leads all regions with a 43.50% share, valued at USD 21.2 Billion.

Product Analysis

Powders dominate with 38.5% due to mass-market accessibility and format versatility.

In 2025, Powders held a dominant market position in the By Product segment of the Makeup Market, with a 38.5% share. Pressed and loose powders serve dual roles — finishing and complexion coverage — which drives repeat purchase across consumer income brackets. Their long shelf life and low formulation cost also make them the default entry point for value-oriented launches in emerging markets.

Gels carry the highest innovation density within the makeup product landscape. Gel-format products — including brow gels, lip gels, and hybrid skin tints — attract premium price points because consumers associate their texture with skincare-grade performance. Consequently, gel formats are outpacing powders in new product development activity among prestige brands seeking to blend cosmetic function with skin benefit claims.

Lotions serve as the bridge between skincare and color cosmetics in the product hierarchy. Tinted moisturizers, BB creams, and liquid foundations in lotion consistency dominate the everyday-wear segment. Their lighter coverage profile aligns with the parallel trend toward natural-finish aesthetics, positioning lotion formats as a structural beneficiary of the no-makeup makeup shift.

Others in the product category — including sticks, pencils, balms, and pressed compacts in non-powder formats — represent the fastest-growing niche by new SKU count. Stick-format products, in particular, respond to on-the-go application preferences that prioritize convenience over precision, which expands the total addressable buyer pool beyond traditional beauty enthusiasts.

Application Area Analysis

Face dominates with 48.1% due to complexion product breadth and high purchase frequency.

In 2025, Face held a dominant market position in the By Application Area segment of the Makeup Market, with a 48.1% share. Foundation, concealer, blush, bronzer, and highlighter collectively occupy more retail shelf space than all other application categories combined. This breadth sustains high replenishment rates and gives face products the largest share of promotional investment from both mass and prestige brands.

Lips function as the highest-margin subcategory per unit within the makeup portfolio. Lipstick, lip liner, and lip gloss carry strong emotional purchase drivers — occasion-based buying, impulse decisions, and gifting — which insulate the segment from recessionary pullback more effectively than complexion categories. Moreover, lip products serve as accessible entry points for first-time color cosmetics buyers.

Eyes attract the highest consumer experimentation rate within the makeup market. Mascara, eyeliner, eyeshadow, and brow products benefit directly from the maximalist eye makeup trend, where bold pigments and textured finishes drive consumers to purchase across multiple subcategories in a single occasion. This behavior inflates average transaction values in the eyes segment beyond face or lip equivalents.

Nails occupy a distinct position in the makeup market because professional application services — salons — compete directly with at-home retail products. However, the proliferation of gel-at-home kits and hybrid nail treatments is shifting share from salon services back to retail, expanding the addressable consumer base for nail cosmetics sold through conventional makeup distribution channels.

Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 37.4% due to physical accessibility and impulse purchase conditions.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Makeup Market, with a 37.4% share. Mass retail formats provide unmatched foot traffic, product trial access, and co-purchase convenience alongside grocery and personal care. These structural advantages sustain their lead even as online channels expand, because physical trial remains a decisive factor in color cosmetic purchase decisions.

Exclusive Brand Stores deliver the highest revenue-per-transaction within makeup distribution. Monobrand retail environments allow companies to control consumer education, product demonstration, and brand storytelling in ways that mass retail cannot replicate. Additionally, in-store beauty consultants drive upselling from single products to multi-step regimens, compressing the consumer journey from awareness to high-value purchase.

Online and E-Commerce Channels are the fastest-scaling distribution route for the makeup market, particularly in markets where physical beauty retail infrastructure remains sparse. According to purchase behavior data, digital-native brands like Wonderskin — which raised $50 million in a Series A round led by Insight Partners in May 2025 — demonstrate that direct-to-consumer e-commerce can build substantial market share before entering physical retail at scale.

Others in distribution — including direct selling networks, specialty beauty retailers, pharmacy chains, and duty-free outlets — serve specific geographic or demographic niches that mass retail and branded stores underserve. Direct selling, in particular, remains the primary channel in markets with low formal retail penetration, sustaining strong volume in parts of Latin America, Southeast Asia, and Sub-Saharan Africa.

Key Market Segments

By Product

- Powders

- Gels

- Lotions

- Others

By Application Area

- Face

- Lips

- Eyes

- Nails

By Distribution Channel

- Supermarkets and Hypermarkets

- Exclusive Brand Stores

- Online/E-Commerce Channels

- Others

Drivers

Vegan Formulations, E-Commerce Access, and Social Media Influence Converge to Accelerate Makeup Adoption

Consumer demand for vegan and cruelty-free makeup has moved from niche preference to mainstream procurement criterion. Retailers now require ethical sourcing declarations from suppliers before granting shelf space. This regulatory and retail pressure forces reformulation across product lines, which simultaneously raises product development costs and filters out brands unable to meet certification thresholds.

E-commerce platforms remove the geographic barriers that historically limited makeup market reach to dense urban retail corridors. Brands now sell directly to consumers in Tier 2 and Tier 3 cities across Asia, Latin America, and Africa without building physical distribution infrastructure. In June 2025, L’Oréal acquired the UK-based clinical skincare brand Medik8 for $1.1 billion, signaling that digital-first prestige positioning now justifies billion-dollar acquisition valuations.

According to The Estée Lauder Companies’ Sustainability Report, the company achieved a 37.6% reduction in absolute Scope 1 and 2 GHG emissions in fiscal 2025 from a 2018 baseline. This operational discipline reflects how leading makeup brands now embed sustainability performance into their core business model — a positioning advantage that resonates with younger, values-driven consumers who directly link ethical manufacturing to purchase loyalty.

Restraints

Regulatory Ingredient Bans, Supply Chain Pressures, and Counterfeit Proliferation Cap Market Growth Potential

Regulatory agencies across the EU, US, and key Asian markets continue to expand restricted ingredient lists for color cosmetics. Each new ban requires brands to reformulate existing SKUs, re-test for safety compliance, and re-label packaging — a process that costs time and capital that smaller brands often cannot absorb. This compliance burden consolidates market share toward large, well-resourced players.

Climate-driven raw material disruptions now add structural volatility to makeup supply chains. Key inputs — plant-derived waxes, mineral pigments, and specialty emulsifiers — face irregular supply and price spikes tied to agricultural and extraction disruptions. According to The Estée Lauder Companies’ Sustainability Report, the company achieved a 41% reduction in water withdrawal at direct manufacturing sites in fiscal 2025 from a 2019 baseline — evidence that even leading brands must invest heavily in resource efficiency just to maintain stable production economics.

Counterfeit makeup products undermine brand equity across every distribution channel, but the problem concentrates most severely in online marketplaces with low seller verification. Fake products expose consumers to unregulated ingredients while diverting revenue from legitimate brands. This erosion of trust is particularly damaging in emerging markets where consumers are still forming brand preferences and have limited ability to distinguish authentic from counterfeit goods.

Growth Factors

AI-Driven Personalization, Men’s Grooming Expansion, and Emerging Market Income Growth Open New Revenue Channels

AI-powered beauty recommendation engines now enable brands to offer custom formulations matched to individual skin tone, texture, and lifestyle preferences. This hyper-personalization model shifts consumer expectations from product discovery toward product prescription — a fundamentally higher-value relationship that supports premium pricing and reduces churn. Brands that deploy AI tools early build proprietary consumer datasets that compound into durable competitive advantages.

Men’s grooming and gender-neutral makeup represent an underpenetrated revenue opportunity with structural tailwinds. Cultural acceptance of cosmetic use among male consumers is expanding across North America, Europe, and East Asia, driven by influencer culture and mainstream retail normalization. In September 2025, Society Brands acquired clean-label cosmetics brand Crunchi, a move that illustrates how acquirers are targeting functional, gender-inclusive positioning ahead of the mainstream adoption curve.

According to Unilever’s Annual Report, the company reduced operational Scope 1 and 2 GHG emissions by 77% in 2025 from a 2015 baseline. This operational efficiency gain frees capital that Unilever can redeploy toward product innovation and market expansion — particularly in India and other high-growth emerging markets where rising disposable incomes are creating a first-generation premium cosmetics consumer base for the first time.

Emerging Trends

Maximalist Eye Looks, Minimalist Everyday Wear, and Wellness-Infused Formulations Redefine Product Development Priorities

The maximalist eye makeup renaissance — characterized by bold pigment payoff, graphic liner, and textured finishes — is driving a surge in eyeshadow palette SKU counts and limited-edition launches. Brands that execute this trend effectively generate disproportionate social media coverage relative to product cost, because dramatic eye looks create high-engagement visual content that organic creators willingly amplify at zero media cost to brands.

Simultaneously, the no-makeup makeup trend pulls from the opposite direction — driving demand for lightweight, skin-tone-matched products that require minimal skill to apply. This creates a bifurcated product development mandate: brands must serve both expressive and effortless aesthetics within the same catalog. In October 2025, Rare Beauty Brands acquired Unilever’s luxury skincare brand Kate Somerville, reflecting how beauty companies are embedding skincare credibility into makeup positioning to capture minimalist beauty consumers.

According to Unilever’s Annual Report, the company reduced its virgin plastic footprint in packaging by 29% in 2025 from a 2019 baseline, while increasing recycled plastic content to 25% of total packaging. This packaging transition reflects a broader industry trend toward wellness-aligned, environmentally responsible product presentation — a trend that consumers increasingly treat as a product attribute itself, not merely a compliance requirement.

Regional Analysis

Asia Pacific Dominates the Makeup Market with a Market Share of 43.50%, Valued at USD 21.2 Billion

Asia Pacific leads the global makeup market with a 43.50% share, valued at USD 21.2 Billion. This dominance reflects the region’s unmatched consumer base depth, with China, South Korea, Japan, and India each operating as distinct high-volume markets with different aesthetic preferences and price sensitivities. K-beauty and J-beauty export influence also positions Asian brands as global trend originators, not just domestic players.

North America Makeup Market Trends

North America maintains a structurally mature makeup market supported by high per-capita spending, well-developed specialty retail, and strong direct-to-consumer infrastructure. The US market in particular generates premium price points across both prestige and mass segments, driven by consumer willingness to pay for clean-label, ethically sourced, and clinically tested formulations that address specific skin concerns alongside color coverage.

Europe Makeup Market Trends

Europe’s makeup market operates under the world’s most stringent cosmetics regulatory framework, which restricts over 1,300 ingredients compared to far fewer in other markets. This regulatory environment raises entry barriers for foreign brands but simultaneously drives European manufacturers toward safer, higher-quality formulations that command premium positioning globally — making European-origin or European-compliant products trusted across international markets.

Latin America Makeup Market Trends

Latin America’s makeup market benefits from a large and youthful population with strong cultural emphasis on personal presentation. However, persistent currency volatility and economic uncertainty in key markets like Brazil and Argentina compress consumer spending on discretionary beauty items. Brands that localize pricing strategies and product formats — smaller unit sizes, entry-level price tiers — maintain volume in economically pressured periods.

Middle East and Africa Makeup Market Trends

The Middle East generates disproportionately high makeup revenue relative to its population size, driven by premium consumption patterns in Gulf Cooperation Council markets. Halal-certified formulations command strong consumer preference across the broader region. Africa’s long-term trajectory depends on retail infrastructure investment, but urban beauty markets in Nigeria, Kenya, and South Africa already attract dedicated brand launches targeting middle-class consumers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

L’Oréal S.A. operates as the global makeup market’s most diversified competitor by brand portfolio, price tier, and geography. The company’s acquisition of UK clinical skincare brand Medik8 for $1.1 billion in June 2025 signals a deliberate strategy to elevate its Luxe Division with science-backed credibility — a positioning move that directly targets the consumer segment prioritizing skin health outcomes alongside color cosmetic performance.

Avon Products, Inc. built its market position on direct selling infrastructure across emerging markets in Latin America, Eastern Europe, and Asia — channels that traditional retail-dependent competitors cannot easily replicate. This distribution moat sustains Avon’s volume in markets with low formal retail density. However, the direct selling model faces mounting pressure from e-commerce platforms that offer similar accessibility at lower consumer acquisition costs.

Oriflame Cosmetics AG combines its direct selling network with a strong product positioning around natural ingredients and Scandinavian beauty philosophy. This combination provides differentiation in markets where natural and botanical formulation claims resonate strongly with consumers. Oriflame’s geographic concentration in Central and Eastern Europe, Russia, and South Asia makes its revenue sensitive to macroeconomic and political conditions in those corridors.

Revlon, Inc. competes primarily on brand heritage and mass-market accessibility, with strong recognition in North America and Western Europe. The company’s strategic challenge is repositioning legacy brand equity — built over decades — toward the clean-label and vegan formulation expectations that now define mainstream consumer standards. Revlon’s ability to reformulate existing hero SKUs without alienating loyal buyers will determine its medium-term competitive relevance.

Key Players

- L’Oréal S.A.

- Avon Products, Inc.

- Oriflame Cosmetics AG

- Revlon, Inc.

- Coty Inc.

- The Estée Lauder Companies Inc.

- The Procter and Gamble Company

- Kao Corporation

- Shiseido Co. Ltd

- Unilever Plc.

Recent Developments

- Fiscal 2025 — The Estée Lauder Companies achieved a 37.6% reduction in absolute Scope 1 and 2 GHG emissions from a fiscal 2018 baseline through energy efficiency measures and renewable sourcing, as reported in its Sustainability Impact Report. The company also sourced 100% renewable electricity for all global direct operations in fiscal 2025, including 192.2 thousand MWh from on-site solar, utility contracts, energy attribute certificates, and virtual power purchase agreements.

- 2025 — Unilever reduced operational Scope 1 and 2 GHG emissions by 77% from a 2015 baseline via energy efficiency programs and renewable transitions, while achieving 88% renewable electricity across total electricity consumption alongside a 19% decrease in overall energy consumption versus 2024, per its Annual Report and Accounts.

- Fiscal 2025 — The Estée Lauder Companies delivered a 41% reduction in water withdrawal at direct manufacturing sites from a fiscal 2019 baseline of 1.5 million cubic meters, exceeding the 20% target through site-specific efficiency projects. At its Shimotsuma, Japan manufacturing facility, the company cut purified water use for kettle cleaning by 30% and cleaning chemical use by 94%.

- 2025 — Unilever reduced total water consumption by 18% versus 2024, with 2 million m³ recycled and reused internally while operating 29 water stewardship programs in water-stressed areas, per its Annual Report.

- 2025 — Unilever reduced its virgin plastic footprint in packaging by 29% from a 2019 baseline while raising recycled plastic content to 25% of total packaging, and collected and processed 111% of the plastic packaging it sold through EPR schemes and recycled material purchases, per its Annual Report.

Report Scope

Report Features Description Market Value (2025) USD 48.8 Billion Forecast Revenue (2035) USD 88.7 Billion CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Powders, Gels, Lotions, Others), By Application Area (Face, Lips, Eyes, Nails), By Distribution Channel (Supermarkets and Hypermarkets, Exclusive Brand Stores, Online/E-Commerce Channels, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape L’Oréal S.A., Avon Products Inc., Oriflame Cosmetics AG, Revlon Inc., Coty Inc., The Estée Lauder Companies Inc., The Procter and Gamble Company, Kao Corporation, Shiseido Co. Ltd, Unilever Plc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- L'Oréal S.A.

- Avon Products, Inc.

- Oriflame Cosmetics AG

- Revlon, Inc.

- Coty Inc.

- The Estée Lauder Companies Inc.

- The Procter and Gamble Company

- Kao Corporation

- Shiseido Co. Ltd

- Unilever Plc.

Our Clients

- 181798

- Mar 2026