Quick Navigation

Report Overview

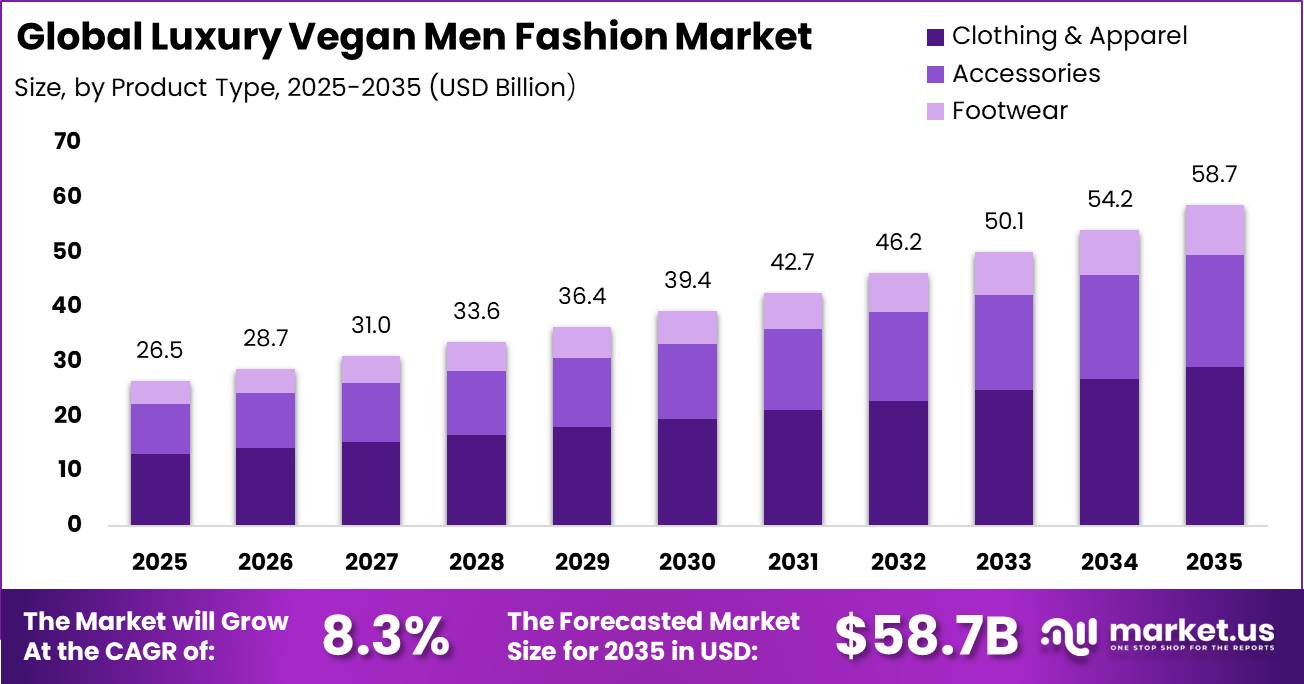

Global Luxury Vegan Men Fashion Market size is expected to be worth around USD 58.7 Billion by 2035 from USD 26.5 Billion in 2025, growing at a CAGR of 8.3% during the forecast period 2026 to 2035. This trajectory places luxury vegan menswear among the fastest-scaling segments within the broader sustainable fashion economy, offering a measurable long-term revenue case for brands, investors, and specialty retailers entering before category saturation.

The luxury vegan men fashion market covers premium menswear, accessories, and footwear produced entirely without animal-derived materials. This includes clothing and apparel, bags, belts, wallets, and shoes made from plant-based, mycelium-derived, or lab-engineered alternatives to leather, silk, wool, and exotic skins. Products are distributed through specialty stores, e-commerce channels, department stores, hypermarkets, and other retail formats targeting affluent male consumers with verified cruelty-free credentials.

Key Takeaways

- The global Luxury Vegan Men Fashion Market was valued at USD 26.5 Billion in 2025 and is forecast to reach USD 58.7 Billion by 2035.

- The market is set to expand at a CAGR of 8.3% from 2026 to 2035.

- By Product, Clothing & Apparel dominates with a 49.6% share in 2025.

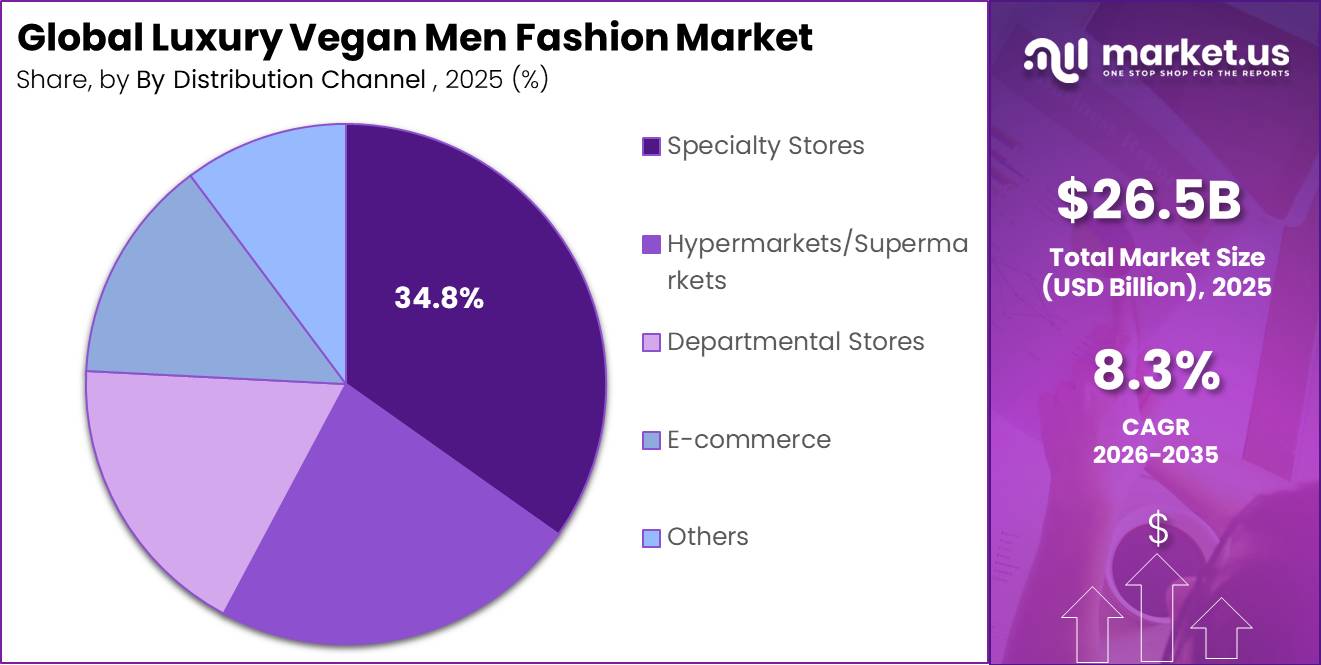

- By Distribution Channel, Specialty Stores hold the leading position at 34.8% share.

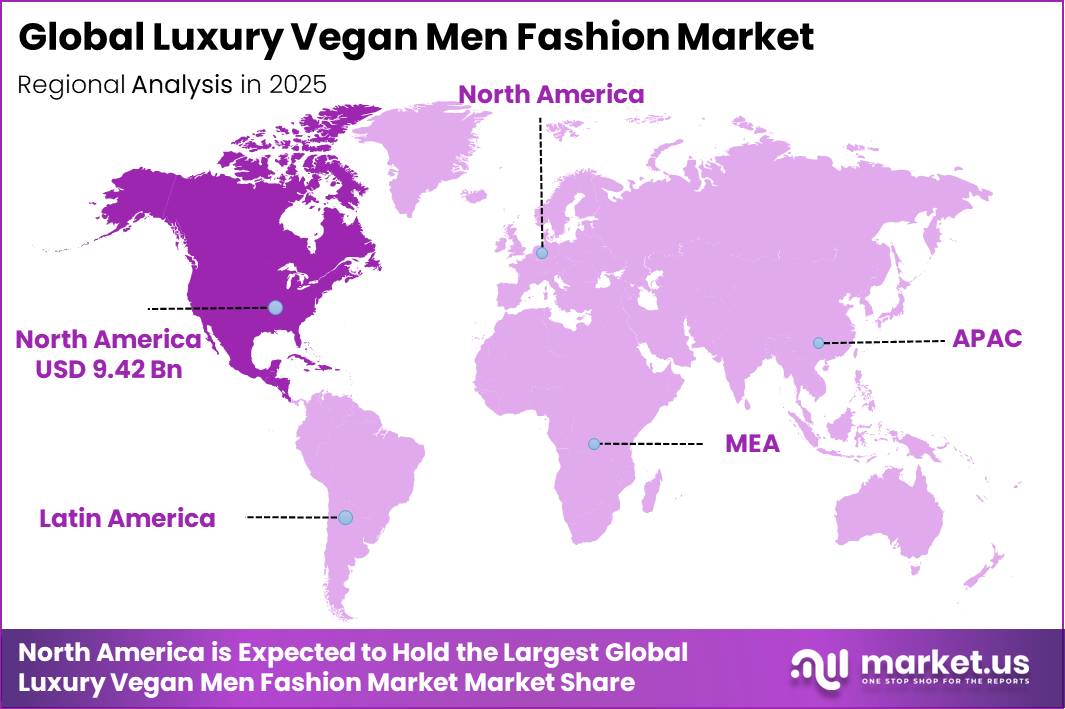

- North America leads all regions with a 35.6% market share, valued at USD 9.42 Billion in 2025.

The EU’s Ecodesign for Sustainable Products Regulation, which entered into force in July 2024, is reshaping how luxury vegan brands operate in Europe’s regulated retail ecosystem. Digital Product Passport requirements will attach serialized lifecycle data to textiles and footwear sold in the EU, with textiles rulemaking targeted from 2027 and compliance buildout toward 2028 to 2029. Brands with narrow SKUs and controlled supplier networks gain a structural pricing advantage. In 2025, Stella McCartney expanded commercial adoption of fungi-based luxury materials through its partnership with Hydefy, bringing NASA-research-derived fungal biomaterials into market-ready luxury fashion products, demonstrating how compliance-ready material innovation can accelerate brand credibility.

According to PwC’s 2024 Voice of Consumer Survey, 80% of consumers are willing to pay more for sustainably produced or sourced goods. This premium willingness directly supports the pricing architecture of luxury vegan menswear, where bio-based materials and cruelty-free credentials command above-average retail margins. Brands that align product positioning with verified sustainability claims can defend higher price points against conventional luxury competitors. A 2024 study published in Social Indicators Research found that Generation Z demonstrates a stronger inclination toward sustainable clothing purchases than previous young-adult cohorts, reinforcing the durability of the addressable buyer base across this forecast period.

Product Analysis

Clothing & Apparel dominates with 49.6% due to broad category coverage and volume of purchase occasions.

In 2025, Clothing & Apparel held a dominant market position in the By Product segment of the Luxury Vegan Men Fashion Market, with a 49.6% share. This dominance reflects the high purchase frequency of ready-to-wear categories and the expanding range of premium vegan fabrications across tailoring, outerwear, and casualwear. In May 2025, Stella McCartney launched the “Generation Falabella” limited-edition capsule collection using vegan and lower-impact materials, demonstrating how apparel-anchored product storytelling activates new luxury buyer cohorts at scale.

Accessories hold a 32% share and function as the primary entry point for male consumers new to the luxury vegan segment. Bags, wallets, belts, and small leather goods substitutes carry lower unit commitment than full apparel and enable brands to convert first-time buyers before cross-selling into higher-ticket categories. This pattern supports sustained revenue per customer as assortments deepen.

Footwear accounts for 18.4% of the product mix and represents the segment with the highest per-unit pricing potential among vegan alternatives. Premium vegan sneakers and dress shoes built on mycelium, cactus leather, or bio-based composites command prices competitive with traditional luxury footwear. This creates a durable margin opportunity for brands that secure exclusive biomaterial supply agreements.

Distribution Channel Analysis

Specialty Stores dominate with 34.8% due to curated brand environment and expert staff positioning.

In 2025, Specialty Stores held a dominant market position in the By Distribution Channel segment of the Luxury Vegan Men Fashion Market, with a 34.8% share. These retail environments allow brands to control the full purchase experience, from material storytelling to certified cruelty-free credentials, which matters disproportionately in a category where product provenance drives willingness to pay. Specialty retailers that integrate digital product passport scanning at point of sale will strengthen conversion on high-margin items.

E-commerce holds a 22% share and is the highest-growth distribution format within the channel mix. Based on PwC 2024 data, 67% of consumers use social media to discover new brands before making purchasing decisions, meaning digital-first vegan luxury brands that pair strong social presence with frictionless online checkout own the discovery-to-conversion funnel. Brands without a robust direct-to-consumer digital presence will cede early buyer relationships to platform-native competitors. Data from ThredUp’s 2024 Resale Report shows the global secondhand apparel market is projected to reach USD 350 Billion by 2028, and e-commerce is the primary channel enabling this resale expansion, which creates additional digital inventory liquidity for vegan luxury brands with serialized product architecture.

Hypermarkets and Supermarkets account for 18% of channel share, serving a different buyer profile than specialty retail. These formats attract aspirational male consumers seeking accessible entry points into vegan fashion without the premium specialty store environment. This channel drives volume across mid-tier price bands, supporting revenue breadth even as per-unit margins remain lower than specialty or direct-to-consumer formats.

Key Market Segments

By Product

- Clothing & Apparel

- Accessories

- Footwear

By Distribution Channel

- Specialty Stores

- E-commerce

- Hypermarkets/Supermarkets

- Departmental Stores

- Others

Market Dynamics

Technology and Innovation Landscape - Biomaterial scale-up, blockchain traceability, and digital authentication redefine competitive differentiation in luxury vegan menswear

Mycelium-based leather is moving from capsule collections to commercial luxury menswear lines. Hydefy’s Fy material, derived from fungi and sugarcane waste and originally developed from NASA research, has reached market-ready status in luxury handbag applications as demonstrated by Stella McCartney’s 2025 commercial launch. This transition from pilot to production signals that mycelium supply chains can now support SKU volumes relevant to luxury wholesale, giving brands with secured biomaterial agreements a structural advantage over those still sourcing conventional animal-derived materials.

Blockchain-enabled material traceability is a commercially deployed technology in this market, not a future concept. Brands using blockchain to verify supply chain provenance can surface material origin, chemical composition, and chain of custody data to consumers and wholesale buyers at point of sale. This directly increases conversion confidence for premium vegan bags, footwear, and jackets where material authenticity drives willingness to pay, and it reduces greenwashing risk in regulated markets where unverified sustainability claims carry growing legal exposure.

Digital Product Passports are becoming a differentiation tool for premium vegan fashion authentication. Early pilots in EU-adjacent markets indicate 25 to 30 consumer-visible data points and up to 126 structured backend fields attached to each product. Brands that build DPP infrastructure ahead of the 2027 textiles rulemaking deadline create a scan-enabled product storytelling capability that converts compliance cost into a customer-facing premium feature, supporting both retail pricing power and wholesale channel acceptance in Europe’s regulated fashion ecosystem.

Bespoke made-to-measure vegan formalwear platforms integrating digital body scanning technologies represent an emerging innovation category. These platforms pair animal-free fabrication with precision fit technology, addressing the fit gap that has historically limited formal occasion penetration for vegan luxury menswear. Carbon-footprint labeling is also emerging as a purchase influence factor in high-end men’s fashion collections, creating an additional data layer that brands with verified low-emission supply chains can use to justify premium pricing to environmentally motivated male consumers.

Market Opportunity Analysis - Undersupplied regional markets and structurally underbuilt distribution formats offer entry points for capital-efficient brands

Latin America remains structurally underserved within the luxury vegan menswear market, with distribution skewed toward department stores and early-stage e-commerce rather than the specialty retail formats that drive premium conversion in North America and Europe. Brazil and Mexico hold the largest near-term consumer base, but the absence of dedicated vegan luxury specialty retail means brands entering with a digital-first strategy face lower competitive density than in mature markets.

The GCC subregion within the Middle East and Africa holds a specific and underexploited opportunity in hospitality uniform adjacencies. The data block identifies GCC gateway cities as a core geographic target for this category, with an estimated +1.7% CAGR upside across a medium-term execution window. Luxury hotels, airlines, and premium service brands operating in the GCC have not yet standardized on vegan menswear uniform collections, leaving a procurement entry point that most vegan fashion brands have not addressed.

India metros, South Korea, Japan, and EU fashion capitals represent the geographic white space for occasionwear. This segment carries an estimated +1.4% CAGR upside and targets affluent male consumers who require premium formal and semi-formal vegan options for weddings, events, and corporate occasions. This segment remains structurally undersupplied because most current vegan luxury brands focus on casualwear and ready-to-wear rather than bespoke or made-to-measure formalwear.

The craft-label roll-up platform opportunity targets Italy, Portugal, France, the UK, and the US across a long-term execution window with an estimated +2.0% CAGR upside. Independent vegan luxury ateliers in these countries operate with strong material and craft credentials but lack the capital, distribution infrastructure, and digital presence to scale. A consolidation platform that acquires or partners with multiple craft labels can aggregate supply, standardize DPP compliance, and build a multi-brand portfolio serving affluent male buyers across price points.

Drivers

The EU’s Ecodesign for Sustainable Products Regulation entered into force in July 2024, with fashion brands preparing for Digital Product Passport requirements covering textiles and footwear sold in the EU. Early implementation data indicates roughly 25 to 30 consumer-visible data points and up to 126 structured fields across access layers. For luxury vegan menswear, this regulation converts sustainability claims into auditable product metadata, strengthening wholesale acceptance in Europe’s regulated retail ecosystem and allowing brands to defend premium pricing on bags, footwear, jackets, and accessories.

Bio-based and recycled material scale-up is a primary structural driver, contributing an estimated +2.1% CAGR impact across the Italy-France luxury manufacturing belt, North America, Japan, and South Korea. Luxury fashion houses eliminating exotic animal skins from men’s accessories and footwear portfolios create permanent demand for mycelium, cactus, apple, and bio-based leather alternatives at commercial scale. In March 2025, Stella McCartney introduced the Stella Ryder handbag made with Hydefy’s fungi-based Fy material derived from fungi and sugarcane waste, marking one of the first commercial luxury handbag launches using this next-generation biomaterial and validating the category’s material supply infrastructure.

A study of 1,018 consumers found that sustainable attitudes, social norms, and altruistic values significantly increase purchase intentions for sustainable clothing. This behavioral evidence supports the structural demand case for luxury vegan menswear at the product level, not just the marketing level. Affluent male buyer shifts toward value-verified sustainability are estimated to contribute +1.4% to CAGR in the US, Japan, Europe, and GCC premium clusters, confirming that verified cruelty-free credentials are a durable commercial differentiator rather than a niche preference.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU traceability and DPP compliance premiumization | +1.6% | EU core, UK alignment, North America export brands, APAC sourcing hubs | Medium term (2-4 years) |

| Textile EPR and circular resale economics | +1.3% | EU core, Nordics, France, Benelux, UK spill-over | Medium term (2-4 years) |

| Bio-based and recycled material scale-up in luxury menswear | +2.1% | Italy-France luxury manufacturing belt, North America core, Japan, South Korea | Medium term (2-4 years) |

| Affluent male buyer shift toward value-verified sustainability | +1.4% | US core, Japan core, Europe core, GCC premium clusters | Short term (≤ 2 years) |

| Luxury channel reset favors niche digital-first vegan brands | +1.1% | North America core, Western Europe, South Korea, urban China selective rebound | Short term (≤ 2 years) |

| Volatile macro backdrop increases animal-free sourcing appeal | +0.9% | EU, UK, US, import-dependent Asia luxury markets | Short term (≤ 2 years) |

Restraints

From 19 July 2026, the EU ban on destruction of unsold apparel, accessories, and footwear applies to large companies, alongside standardized disclosure obligations for discarded unsold volumes. This regulation fundamentally changes the economics of overproduction in luxury vegan menswear, where capsule launches and novelty materials carry uncertain replenishment curves. Brands that previously used product destruction as a quiet inventory clearing mechanism must now absorb reverse logistics, outlet dilution, donation sorting, or refurbishment costs estimated at 2 to 5 percentage points of additional carrying cost on slow-moving seasonal stock.

This compliance burden strategically pushes operators toward narrower assortments, lower preseason commitments, and more conservative channel fill. Business Insider data shows 59% of shoppers indicate they are likely to purchase secondhand luxury goods, which signals a structural shift toward resale as an inventory pressure valve. However, most vegan luxury brands still lack the serialized product architecture and reverse logistics infrastructure to capture this resale demand profitably, meaning the regulatory constraint and the resale opportunity remain disconnected for most current market participants.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium demand slowdown | -2.2% | EU, North America core, China, Japan, Korea | Short term (≤ 2 years) |

| Material cost inflation | -1.6% | EU sourcing hubs, North America, APAC manufacturing corridors | Short term (≤ 2 years) |

| EU traceability compliance | -1.3% | EU core, UK-linked supply chains, non-EU exporters to Europe | Medium term (2-4 years) |

| Unsold inventory restrictions | -1.0% | EU large-brand networks, premium wholesale channels | Medium term (2-4 years) |

| Tariff and trade friction | -1.4% | North America core, China-linked sourcing, EU-US corridors | Short term (≤ 2 years) |

| Logistics and lead-time volatility | -0.9% | Asia-Europe lanes, Asia-US lanes, Middle East transit corridors | Short term (≤ 2 years) |

Challenges

Luxury vegan menswear faces persistent shipping route volatility because products rely on multi-country sourcing chains for fabrics, coatings, trims, and assembly. UNCTAD indicated that maritime trade growth was expected to slow to just 0.5% in 2025 after 2.2% growth in 2024. Global shipping still carries more than 80% of world merchandise trade, meaning even modest network stress ripples directly into apparel and accessory delivery schedules. Brands without nearshore sourcing alternatives face structural replenishment risk.

Operational disruption can translate to 10 to 20 extra days across total replenishment cycles once ocean delay, customs variability, warehouse resequencing, and quality control are combined. This forces brands toward higher safety stock, lower full-price sell-through precision, and more expensive contingency planning. Shipping route volatility carries an estimated CAGR friction drag of -1.2% across APAC sourcing corridors, EU inbound gateways, and North America coastal distribution nodes.

The premium material consistency gap poses an additional challenge, estimated to drag CAGR by -1.3% across EU luxury clusters, US premium retail, and East Asia design centers. Next-generation vegan materials still face performance and durability gaps relative to traditional full-grain leather in high-wear luxury applications. This limits the share of luxury menswear categories where vegan alternatives can command parity pricing, narrowing the addressable premium product range until material science advances resolve consistency at scale.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Premium Material Consistency Gap | -1.3% | EU luxury clusters, U.S. premium retail, East Asia design centers | Medium term (2-4 years) |

| Product Passport Compliance Load | -1.0% | EU regulatory hubs, UK import channels, global textile exporters to Europe | Medium term (2-4 years) |

| Shipping Route Volatility | -1.2% | APAC sourcing corridors, EU inbound gateways, North America coastal distribution nodes | Medium term (2-4 years) |

| Specialist Craft Talent Deficit | -0.8% | Italy, Portugal, Spain, UK ateliers, U.S. premium small-batch manufacturers | Long term (≥ 4 years) |

| Multi-Tier Compliance Verification | -0.9% | South Asia sourcing bases, ASEAN production belts, EU and U.S. brand headquarters | Long term (≥ 4 years) |

| Cost Pass-Through Instability | -1.1% | North America premium wholesale, EU direct-to-consumer brands, cross-border online luxury channels | Short term (≤ 2 years) |

Opportunities

Brand-owned resale loops represent the highest near-term CAGR upside in this market, estimated at +2.3% above baseline across the EU, UK, US, Japan, and South Korea. A brand-controlled resale loop integrating buy-back, refurbishment, authenticity verification, and relisting can extend customer lifetime value by 20% to 32% and reduce blended acquisition cost by 12% to 20% through trade-in reactivation. Forbes data shows more than half of consumers purchased secondhand apparel in 2022, confirming mainstream appetite for circular purchase behavior that luxury vegan brands have not yet fully captured.

Bio-material exclusivity offers a +1.8% CAGR upside across the EU, US, Japan, and Singapore through medium-term execution. Brands that secure proprietary or co-developed biomaterial supply agreements for mycelium, lab-engineered silk, or animal-free textile innovations can build defensible product differentiation before these materials reach commodity availability. Vegan luxury menswear tailoring using these materials targets the highest-spending buyer segment and commands prices competitive with traditional luxury fabrications.

Digital Product Passport-linked service monetization adds an estimated +1.6% CAGR upside concentrated in EU core markets, the UK, and the Nordics. Brands that convert DPP compliance infrastructure into consumer-facing authentication services, scan-enabled product storytelling, and lifecycle documentation can charge a service premium alongside the physical product. This execution window is short term and executable within two years, making it an immediate strategic priority for brands already investing in DPP compliance buildout.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Brand-owned resale loops | +2.3% | EU, UK, US, Japan, South Korea | Short term (≤ 2 years) |

| Bio-material exclusivity | +1.8% | EU, US, Japan, Singapore | Medium term (2-4 years) |

| DPP-linked service monetization | +1.6% | EU core, UK, Nordics | Short term (≤ 2 years) |

| Hospitality uniform adjacencies | +1.7% | GCC, EU gateway cities, US luxury hubs | Medium term (2-4 years) |

| Occasionwear white-space | +1.4% | India metros, South Korea, Japan, EU fashion capitals | Medium term (2-4 years) |

| Craft-label roll-up platform | +2.0% | Italy, Portugal, France, UK, US | Long term (≥ 4 years) |

Regional Analysis

North America Dominates the Luxury Vegan Men Fashion Market with a Market Share of 35.6%, Valued at USD 9.42 Billion

North America holds a 35.6% share valued at USD 9.42 Billion in 2025, driven by a deep concentration of high-spending Gen Z and millennial male consumers who actively prioritize cruelty-free credentials in premium purchases. The US market benefits from a mature direct-to-consumer e-commerce infrastructure and a regulatory environment increasingly aligned with sustainability disclosure. Brands with blockchain-enabled material traceability gain measurable conversion advantages in this market.

Europe represents a structurally important region for luxury vegan menswear given the EU’s Ecodesign for Sustainable Products Regulation and the incoming Digital Product Passport requirements targeted from 2027. Luxury brands with narrow SKUs and controlled material supply chains are best positioned to comply and command premium pricing across the EU’s regulated retail ecosystem. France, Italy, and Germany anchor the luxury fashion manufacturing base and serve as key distribution hubs.

Asia Pacific is an expanding market for luxury vegan menswear, with Japan and South Korea serving as the primary adoption leaders due to established luxury consumer bases and high receptivity to sustainable material innovation. China presents selective rebound potential in urban premium clusters where male consumers are demonstrating interest in verifiable sustainability credentials. APAC sourcing corridors also play a structural role in bio-material supply chains for global luxury brands.

Latin America remains an early-stage market for luxury vegan menswear, with Brazil and Mexico representing the highest near-term entry potential given their growing affluent consumer bases. The channel mix skews toward department stores and emerging e-commerce platforms rather than specialty retail, which limits average transaction value. Brands entering this region should prioritize digital discovery channels before investing in physical retail infrastructure.

The Middle East and Africa region presents a niche but high-value opportunity concentrated in GCC markets where affluent male consumers with strong luxury fashion engagement are beginning to respond to international vegan luxury positioning. Hospitality and corporate sustainability buyers in GCC gateway cities represent an underexplored B2B adjacency. South Africa anchors a smaller but growing consumer segment on the African continent.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Thought Clothing positions itself as a vertically integrated sustainable menswear brand focused on natural and recycled fiber collections with transparent supply chain credentials. This positioning aligns directly with affluent male buyer behavior documented in research published in 2025 in ScienceDirect, which identified Generation Z as a key driver of eco-conscious fashion purchasing. Brands with established material certifications and direct-to-consumer reach hold a first-mover advantage as this buyer cohort matures into peak earning years.

Komodo Fashion operates as a specialist sustainable menswear label with a product range spanning clothing, accessories, and lifestyle pieces that target price-conscious premium buyers. In December 2025, Stella McCartney and LeMieux launched a luxury vegan equestrian collection combining performance riding apparel with cruelty-free materials, signaling that lifestyle-specific vegan collections are an emerging product architecture that specialists like Komodo can replicate across niche male consumer segments. Brands that extend into sport and lifestyle adjacencies ahead of mainstream adoption build defensible category positioning before larger luxury houses enter.

Key Players

- Thought Clothing

- Komodo Fashion

- Brave GentleMan

- Ecoalf

- Wuxly

- A.BCH

- CARPASUS

- Toad&Co.

- Will’s Vegan Shoes

- Vegan Outfitter

Recent Developments

- September 2025 – Stella McCartney showcased YATAY M mushroom-based vegan material across luxury bags, footwear, and apparel in its Fall 2025 collection, expanding commercial use of mycelium-derived alternatives to exotic animal skins across multiple product categories.

- October 2025 – Stella McCartney unveiled FEVVERS, a plant-based feather alternative, during its Spring/Summer 2026 Paris Fashion Week show, replacing conventional bird feathers with cruelty-free bio-based materials in a high-visibility commercial launch.

- May 2026 – Vêtir, an AI-powered luxury fashion platform serving premium fashion consumers, secured USD 5.5 Million in Series A funding at a USD 150 Million valuation to expand its luxury fashion technology ecosystem.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 26.5 Billion |

| Forecast Revenue (2035) | USD 58.7 Billion |

| CAGR (2026-2035) | 8.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Clothing & Apparel, Accessories, Footwear); By Distribution Channel (Specialty Stores, E-commerce, Hypermarkets/Supermarkets, Departmental Stores, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Thought Clothing, Komodo Fashion, Brave GentleMan, Ecoalf, Wuxly, A.BCH, CARPASUS, Toad&Co., Will’s Vegan Shoes, Vegan Outfitter |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |