Global Locum Tenens Staffing Market By Specialty (Primary Care, Hospitalist, Emergency Medicine, Psychiatry, Radiology, Anesthesiology, Surgery, Pediatrics, Obstetrics and Gynecology, Cardiology and Others), By Setting (Hospitals, Private Practices, Government Facilities, Long-term Care Facilities, Urgent Care Centers and Others), By Provider Type (Physicians (MDs/DOs), Advanced Practice Providers and Dentists), By Staffing Type (Temporary Coverage, Permanent Placement and Temp-to-Perm), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183122

- Number of Pages: 385

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

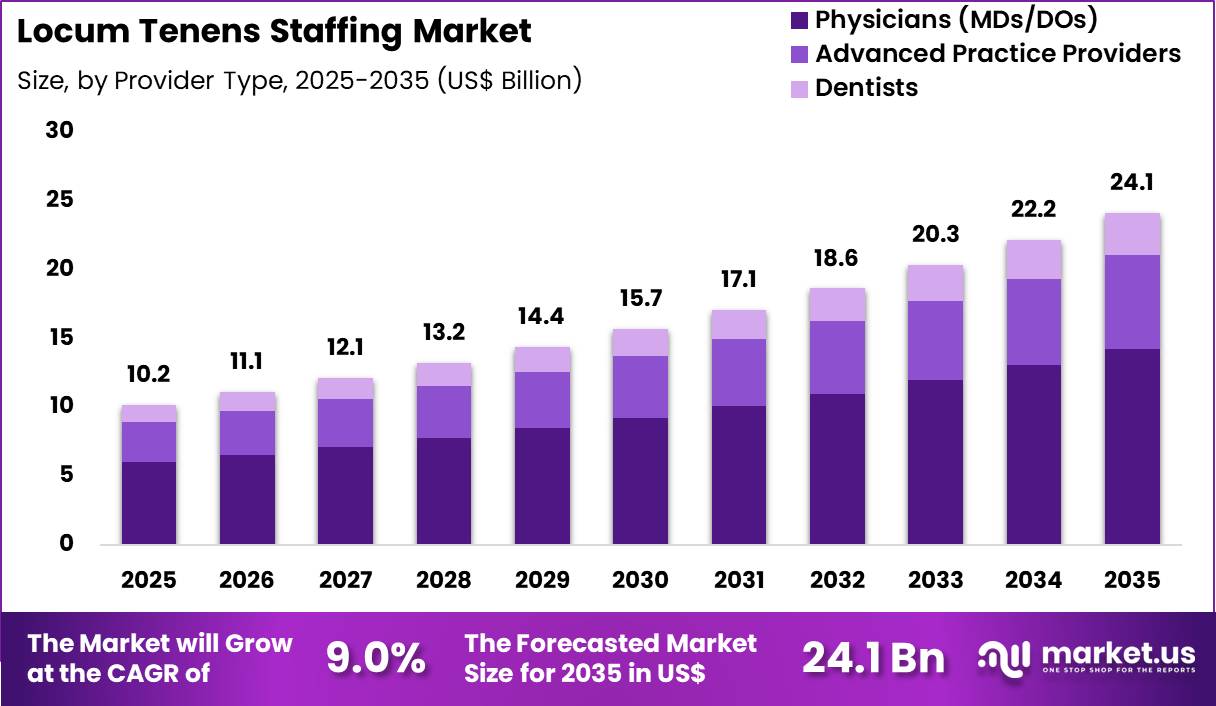

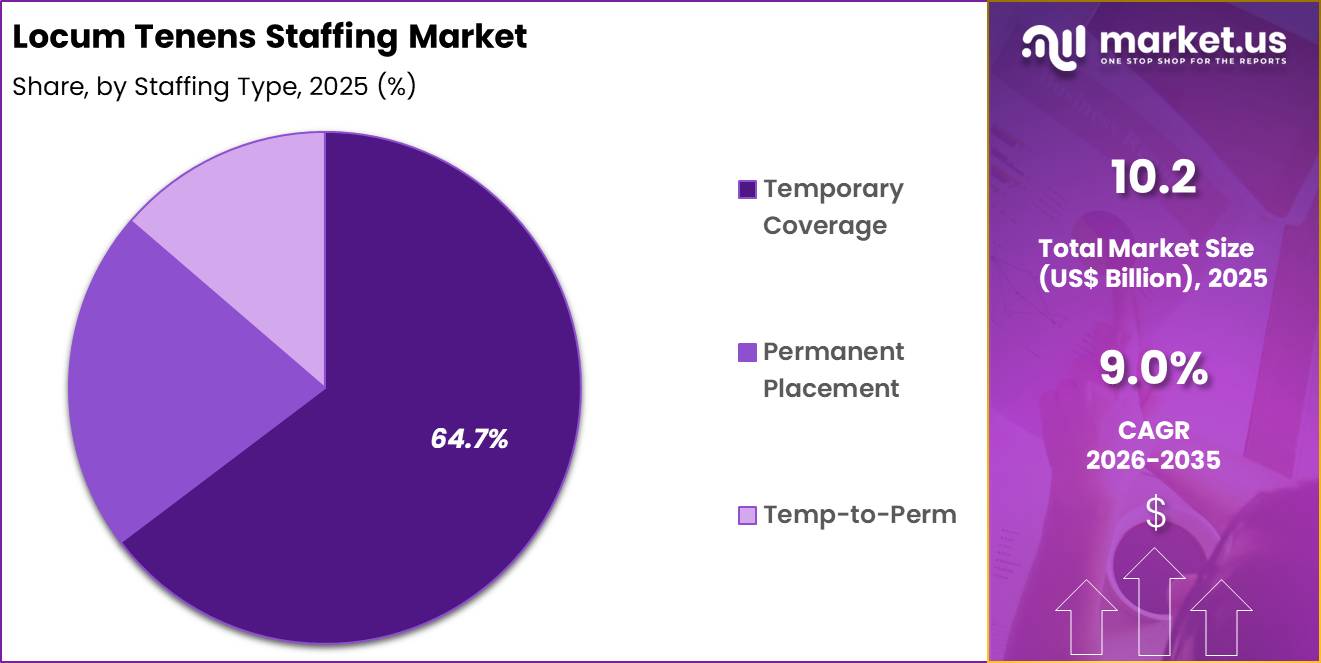

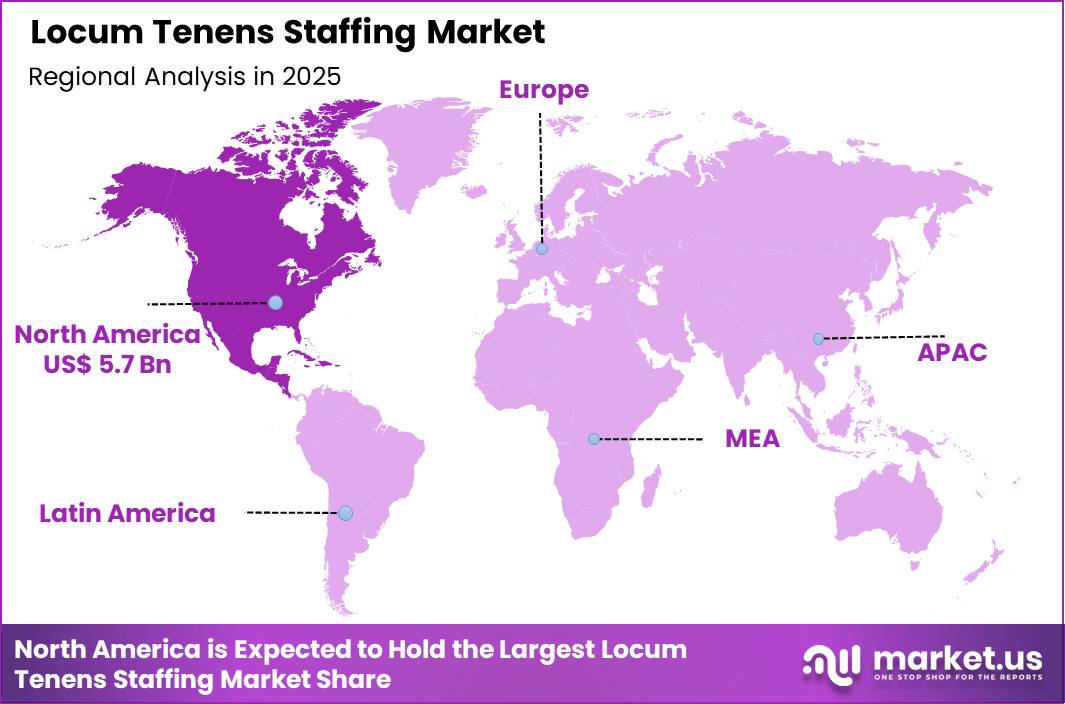

The Global Locum Tenens Staffing Market size is expected to be worth around US$ 24.1 Billion by 2035 from US$ 10.2 Billion in 2025, growing at a CAGR of 9.0% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 55.6% share with a revenue of US$ 5.7 Billion.

Rising physician shortages and increasing demand for flexible staffing solutions drive the Locum Tenens Staffing market as healthcare facilities seek to maintain continuous coverage without compromising quality of care. Hospitals and clinics increasingly engage locum tenens physicians to address temporary gaps caused by vacations, illness, or sudden resignations in specialties such as emergency medicine, anesthesiology, and hospitalist care, ensuring uninterrupted patient services and preventing burnout among permanent staff.

These staffing arrangements support rural and underserved facilities by providing specialist coverage in fields like psychiatry, neurology, and orthopedics, where recruitment of full-time providers remains challenging. Health systems utilize locum tenens to manage seasonal demand surges, such as flu outbreaks or elective surgery backlogs, maintaining operational stability during peak periods.

The model also enables facilities to test new service lines or cover maternity leaves without long-term financial commitment. In February 2026, CHG Healthcare marked a decade of its philanthropic foundation, which has contributed millions of dollars to community initiatives.

At the same time, the company continues to expand its digital capabilities through platforms such as Locumsmart and Modio Health, which help streamline credentialing processes and reduce onboarding time for healthcare providers.

Staffing agencies pursue opportunities to develop AI-powered matching platforms that accelerate credentialing and placement, expanding applications in high-acuity environments where rapid deployment of qualified specialists is critical. These digital tools facilitate real-time availability tracking and automated compliance checks, improving efficiency for both facilities and providers.

Opportunities emerge in specialized locum tenens programs for advanced practice providers, including nurse practitioners and physician assistants, to support team-based care models in primary and specialty settings. Companies invest in comprehensive support services that include licensing assistance, malpractice coverage, and travel coordination, enhancing provider satisfaction and retention.

Recent trends emphasize hybrid models that combine short-term locum assignments with permanent recruitment pipelines, allowing facilities to evaluate candidates while addressing immediate staffing needs. The market continues to evolve toward technology-enabled, flexible staffing solutions that balance workforce shortages with high standards of clinical excellence and operational resilience.

Key Takeaways

- In 2025, the market generated a revenue of US$ 10.2 Billion, with a CAGR of 9.0%, and is expected to reach US$ 24.1 Billion by the year 2035.

- The provider type segment is divided into primary care, hospitalist, emergency medicine, psychiatry, radiology, anesthesiology, surgery, pediatrics, obstetrics and gynecology, cardiology and others, with physicians (mds/dos) taking the lead with a market share of 58.9%.

- Considering staffing type, the market is divided into hospitals, private practices, government facilities, long-term care facilities, urgent care centers and others. Among these, temporary coverage held a significant share of 64.7%.

- Furthermore, concerning the setting segment, the market is segregated into physicians (MDs/DOs), advanced practice providers and dentists. The hospitals sector stands out as the dominant player, holding the largest revenue share of 45.8% in the market.

- The specialty segment is segregated into temporary coverage, permanent placement and temp-to-perm, with the primary care segment leading the market, holding a revenue share of 22.5%.

- North America led the market by securing a market share of 55.6%.

Specialty Analysis

Physicians accounted for 58.9% of growth within provider type and dominate the locum tenens staffing market due to their central role in delivering specialized and primary medical care across healthcare systems. Hospitals and clinics rely heavily on licensed physicians to fill workforce gaps caused by staff shortages, burnout, and uneven geographic distribution of healthcare professionals.

Healthcare workforce studies indicate persistent physician shortages in many regions, particularly in rural and underserved areas, which increases reliance on temporary staffing solutions. Physicians are expected to remain the leading provider group as healthcare demand continues to rise due to aging populations and increasing chronic disease burden.

Healthcare facilities are likely to prefer locum physicians for maintaining continuity of care without long-term hiring commitments. The segment benefits from high demand in critical specialties where full-time recruitment remains challenging.

Locum physician roles also offer flexibility, which attracts professionals seeking better work-life balance. Growing acceptance of flexible workforce models is projected to strengthen adoption. As healthcare systems continue to face staffing constraints, physicians are estimated to retain their dominant position in this market.

Setting Analysis

Temporary coverage accounted for 64.7% of growth within staffing type and dominates the locum tenens staffing market because healthcare providers frequently require short-term staffing solutions to manage workforce gaps and fluctuating patient volumes. Facilities often use temporary staff to cover leaves, seasonal demand spikes, or sudden vacancies, which makes this model highly practical.

Industry observations show that many hospitals experience periodic staffing shortages, especially in emergency and critical care departments. Temporary coverage is expected to expand as healthcare systems prioritize operational continuity and patient care quality. Providers are likely to prefer short-term contracts because they offer flexibility and cost control without long-term commitments.

The segment benefits from rapid onboarding processes and the ability to deploy professionals quickly. Increasing physician burnout and workforce mobility are projected to support demand for temporary staffing solutions. As healthcare systems adapt to dynamic workforce needs, temporary coverage is anticipated to remain the dominant staffing type.

Provider Type Analysis

Hospitals accounted for 45.8% of growth within setting and dominate the locum tenens staffing market due to their high patient volumes, complex care requirements, and continuous need for medical professionals. Hospitals operate around the clock and require consistent staffing across multiple departments, including emergency care, surgery, and inpatient services.

Healthcare systems report increasing hospital admissions and procedural volumes, which intensifies staffing requirements. Hospitals are expected to remain the largest users of locum tenens services as they address staffing shortages and maintain service quality. The segment benefits from the need for specialized expertise in critical care and surgical departments.

Hospitals are likely to rely on temporary staff to manage peak demand and unexpected workforce gaps. Expansion of hospital infrastructure and services is projected to further support demand. As patient care complexity increases, hospitals are anticipated to maintain their dominant position in the locum tenens staffing market.

Staffing Type Analysis

Primary care accounted for 22.5% of growth within specialty and dominates the locum tenens staffing market due to its essential role in first-contact healthcare and ongoing patient management. Primary care physicians handle a wide range of health conditions, which creates consistent demand across healthcare settings. Health organizations highlight that primary care services form the foundation of healthcare systems and manage a large share of patient interactions.

The segment is expected to grow as demand for preventive care and chronic disease management increases. Primary care roles are likely to experience staffing shortages in rural and underserved areas, which drives higher reliance on locum tenens professionals.

Healthcare providers use temporary staffing to ensure continuity of care and reduce patient wait times. The segment benefits from steady patient inflow and the need for regular consultations. As healthcare access expands and population health needs increase, primary care is estimated to remain the leading specialty segment in this market.

Key Market Segments

By Specialty

- Primary Care

- Hospitalist

- Emergency Medicine

- Psychiatry

- Radiology

- Anesthesiology

- Surgery

- Pediatrics

- Obstetrics and Gynecology

- Cardiology

- Others

By Setting

- Hospitals

- Private Practices

- Government Facilities

- Long-term Care Facilities

- Urgent Care Centers

- Others

By Provider Type

- Physicians (MDs/DOs)

- Advanced Practice Providers

- Dentists

By Staffing Type

- Temporary Coverage

- Permanent Placement

- Temp-to-Perm

Drivers

Physician and provider shortages are driving the Locum Tenens Staffing market.

Persistent gaps in the healthcare workforce have compelled facilities to rely on temporary staffing solutions to maintain service continuity and patient access. The Association of American Medical Colleges projects that the United States will face a physician shortage of up to 86,000 by 2036, with estimates from earlier projections indicating deficits ranging from 37,800 to 124,000 physicians by 2034.

This shortfall encompasses between 17,800 and 48,000 primary care physicians and additional gaps in surgical and medical specialties. An aging physician workforce exacerbates the situation, as more than two of every five active physicians will reach age 65 or older within the coming decade. Rising patient demand, driven by population growth and chronic conditions, further intensifies the need for flexible coverage

Healthcare organizations utilize locum tenens to address unfilled positions, with 67 percent employing them until a permanent candidate is secured. Actual utilization in 2024 exceeded expectations by 25 percentage points, reflecting strategic integration into workforce planning.

Facilities also deploy locums to mitigate burnout and supplement staff during peak periods, with 35% citing rising patient demand as a key factor. The model supports testing new service lines and maintaining operations amid transitions. Consequently, these structural workforce imbalances serve as a primary driver sustaining market expansion during the 2022–2025 period.

Restraints

Rising staffing costs and rate pressures are restraining the Locum Tenens Staffing market.

Escalating compensation rates for temporary providers have prompted health systems to scrutinize expenditures and seek cost containment measures. Hospitals face pressure to control bill rates amid broader efforts to stabilize operational budgets following post-pandemic volatility.

Although demand remains robust, some facilities delay permanent hires or negotiate aggressively, tempering volume growth in certain segments. The requirement for rapid credentialing and compliance adds administrative overhead that increases overall deployment expenses. Reimbursement uncertainties and varying payer policies complicate billing efficiency for locum services.

Smaller or rural facilities encounter disproportionate challenges in affording premium rates for specialized providers. These financial dynamics contribute to moderated expansion despite underlying need. Persistent focus on value-based care models encourages optimization of staffing mixes to minimize reliance on higher-cost temporary solutions.

Organizations balance short-term coverage requirements against long-term fiscal sustainability. As a result, such cost-related constraints impose measurable restraint on accelerated market momentum throughout the 2022–2025 timeframe.

Opportunities

Growing reliance on advanced practice providers within locum models is creating growth opportunities in the Locum Tenens Staffing market.

Expansion of roles for nurse practitioners, physician assistants, and certified registered nurse anesthetists offers cost-effective alternatives to address specialty-specific gaps. Demand for locum CRNAs exhibited notable increases, with client spending rising from 37 million U.S. dollars in the prior year to 59 million U.S. dollars in 2024.

Utilization of advanced practice providers in searches reached 8.1% in 2024, marking elevated engagement compared to previous periods. Opportunities emerge for hybrid staffing strategies that combine physicians and advanced practitioners to optimize coverage and control expenses. This approach supports scalability in outpatient, hospitalist, and procedural settings where full physician availability is limited.

Integration with telehealth platforms further extends the reach of locum advanced practice providers to underserved areas. Providers benefit from flexible schedules and supplemental income, enhancing recruitment pools.

Health systems gain flexibility to upsize or downsize capacity in response to fluctuating demand. These dynamics foster diversified service offerings and recurring engagements. Overall, the shift toward advanced practice integration unlocks substantial prospects for market broadening and operational efficiency.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical factors are reshaping demand, pricing, and workforce mobility in the locum tenens staffing market. Rising healthcare demand and clinician shortages are driving greater reliance on temporary staffing, while inflation is increasing wage expectations and placement costs for providers.

Budget pressures within hospitals can limit hiring flexibility, especially in smaller or rural facilities. Geopolitical developments influence visa policies and cross-border movement of healthcare professionals, which affects the available talent pool in key markets. Licensing complexity and regional credentialing requirements also create operational friction for staffing firms.

Current US tariff policies have minimal direct impact on service-based staffing, but they indirectly increase operational costs by raising prices of medical equipment and supplies used by healthcare facilities. These higher costs can reduce staffing budgets and delay contract approvals in some cases. At the same time, ongoing workforce shortages and the need for flexible staffing models are expected to keep demand strong and support continued market growth.

Latest Trends

Strategic incorporation of locum tenens into long-term workforce planning represents a recent trend in the Locum Tenens Staffing market.

In 2024 and extending into 2025, healthcare organizations have shifted from viewing locum tenens primarily as short-term gap fillers to embedding them within comprehensive staffing strategies. Actual utilization in 2024 surpassed projections by 25 percentage points, with 80 percent of facilities anticipating flat or increased usage in 2025. Locum tenens featured in 16.4% of physician searches in 2024, the highest rate recorded, alongside 8.1% for advanced practice providers.

Facilities increasingly employ locums to meet rising patient demand, mitigate burnout, and test new service lines rather than solely for vacancy coverage. The U.S. locum tenens market reached an estimated 9.6 billion U.S. dollars in 2025, reflecting 5% year-over-year growth and continued outperformance relative to other staffing segments.

This evolution aligns with efforts to protect revenue, as a single physician vacancy can risk approximately 2.6 million U.S. dollars annually. Enhanced technology platforms have streamlined credentialing and deployment, facilitating faster integration. The trend underscores a maturing industry focus on flexibility and proactive capacity management. Prominent in 2024–2025, this strategic orientation redefines locum tenens as an essential component of resilient healthcare workforce models.

Regional Analysis

North America is leading the Locum Tenens Staffing Market

North America accounted for 55.6% of the locum tenens staffing market in 2025 as healthcare systems increasingly relied on temporary physician and clinician placements to manage workforce shortages and fluctuating patient demand. Hospitals and clinics across the United States are facing persistent staffing gaps due to physician burnout, retirements, and uneven distribution of specialists, which has accelerated the use of flexible staffing models.

According to the Association of American Medical Colleges, the United States could face a shortage of up to 124000 physicians by 2034, underscoring the urgency for interim staffing solutions that maintain care continuity. Healthcare providers are using temporary staffing to fill roles in rural areas, emergency departments, and high-demand specialties where permanent hiring remains difficult.

Telehealth expansion has also enabled locum professionals to deliver care remotely, increasing flexibility and coverage. Staffing agencies are leveraging digital platforms to match clinicians with assignments more efficiently and reduce onboarding time. Health systems are adopting locum staffing as a strategic workforce tool to manage peak demand and reduce patient wait times.

Competitive compensation and flexible work arrangements are attracting more clinicians to temporary roles. These dynamics collectively strengthened the expansion of flexible healthcare staffing solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as healthcare systems work to address workforce shortages and expand access to medical services across diverse populations. Countries such as India, China, Australia, and Southeast Asian nations are facing uneven distribution of healthcare professionals between urban and rural regions, which is encouraging adoption of temporary staffing models.

The World Health Organization estimates a global shortage of about 10 million health workers by 2030, with a significant portion of the gap affecting low- and middle-income countries across Asia. Healthcare providers in the region are increasingly turning to short-term staffing solutions to fill immediate gaps in hospitals and clinics.

Governments are also exploring policy reforms that allow more flexible workforce deployment and cross-regional medical staffing. Private healthcare networks are partnering with staffing agencies to ensure continuous service delivery in high-demand specialties. Digital platforms are enabling faster recruitment and credential verification for temporary medical professionals.

Training institutions are also producing a growing pool of healthcare workers open to flexible employment arrangements. These developments are expected to accelerate adoption of temporary healthcare staffing solutions across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Locum Tenens Staffing Market expand growth by strengthening physician placement networks, leveraging digital staffing platforms, and building long-term partnerships with hospitals and healthcare systems facing workforce shortages. Companies invest in data-driven matching tools and credentialing automation that accelerate provider onboarding and improve placement efficiency.

They also focus on flexible staffing models, competitive compensation structures, and telehealth integration to attract qualified clinicians across specialties. CHG Healthcare represents a prominent participant in the Locum Tenens Staffing Market and operates as a U.S.-based healthcare staffing company that provides physician placement, workforce solutions, and staffing services through multiple specialized brands.

The company emphasizes extensive provider networks and streamlined staffing processes to meet evolving healthcare demands. Industry competitors continue to expand geographic reach, enhance digital staffing capabilities, and strengthen client relationships to support consistent workforce availability and long-term market growth.

Top Key Players

- CHG Healthcare Services Inc.

- AMN Healthcare Services Inc.

- Envision Healthcare Corporation

- TeamHealth Holdings Inc.

- Weatherby Healthcare

- CompHealth Inc.

- Global Medical Staffing

- VISTA Staffing Solutions Inc.

- Medestar

- LocumTenens.com

Recent Developments

- By early 2026, the locum tenens market in the US has moved into a more stable phase following the rapid expansion seen during the pandemic period. Growth has moderated but remains steady, with the segment continuing to outperform other healthcare staffing categories due to ongoing physician shortages and persistent coverage gaps across healthcare systems.

- A 2025 analysis by CHG Healthcare highlighted the financial impact of unfilled physician roles, showing that a single vacancy can result in significant annual revenue loss for hospitals. As a result, healthcare providers are increasingly using locum tenens staffing as a planned strategy rather than an emergency measure, leading to a notable rise in proactive placements to maintain service continuity and protect revenue streams.

- In January 2025, Barton Associates appointed April Hansen as chief executive officer, signaling a strategic shift in leadership. The company has since focused on attracting a younger physician workforce by promoting locum tenens as a flexible, long-term career option aligned with evolving work-life preferences.

Report Scope

Report Features Description Market Value (2025) US$ 10.2 Billion Forecast Revenue (2035) US$ 24.1 Billion CAGR (2026-2035) 9.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Specialty (Primary Care, Hospitalist, Emergency Medicine, Psychiatry, Radiology, Anesthesiology, Surgery, Pediatrics, Obstetrics and Gynecology, Cardiology and Others), By Setting (Hospitals, Private Practices, Government Facilities, Long-term Care Facilities, Urgent Care Centers and Others), By Provider Type (Physicians (MDs/DOs), Advanced Practice Providers and Dentists), By Staffing Type (Temporary Coverage, Permanent Placement and Temp-to-Perm) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape CHG Healthcare Services Inc., AMN Healthcare Services Inc., Envision Healthcare Corporation, TeamHealth Holdings Inc., Weatherby Healthcare, CompHealth Inc., Global Medical Staffing, VISTA Staffing Solutions Inc., Medestar, LocumTenens.com. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Locum Tenens Staffing MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Locum Tenens Staffing MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- CHG Healthcare Services Inc.

- AMN Healthcare Services Inc.

- Envision Healthcare Corporation

- TeamHealth Holdings Inc.

- Weatherby Healthcare

- CompHealth Inc.

- Global Medical Staffing

- VISTA Staffing Solutions Inc.

- Medestar

- LocumTenens.com

Our Clients

- 183122

- March 2026