Global Linear Motor Market Size, Share, Growth Analysis By Design (Cylindrical, Flat Plate, U-Channel), By Application (Building and Construction, Electrical and Electronics, Food and Beverage, Textile, Agriculture, Automotive, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 28753

- Number of Pages: 203

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

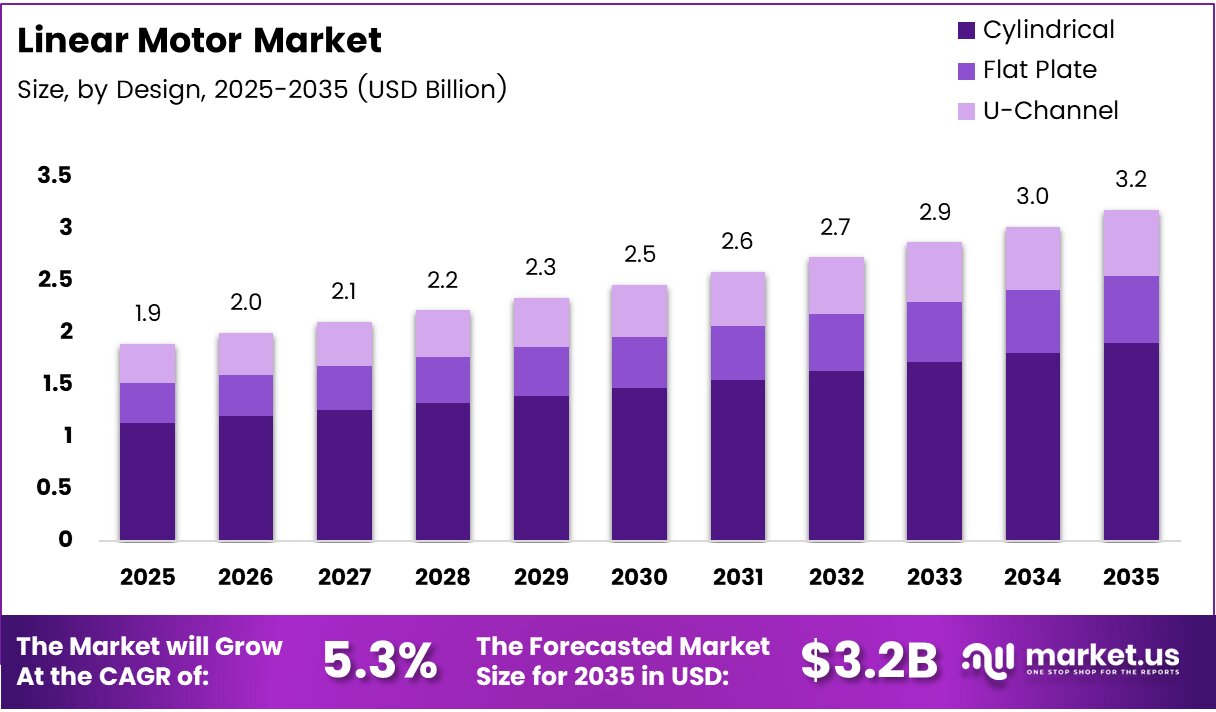

Global Linear Motor Market size is expected to be worth around USD 3.2 Billion by 2035 from USD 1.9 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

Linear motors convert electrical energy into straight-line mechanical motion without rotary-to-linear conversion mechanisms. This direct-drive approach eliminates gearboxes and lead screws, which removes mechanical slack and wear points. Manufacturers across precision-critical industries prefer this architecture because it delivers higher throughput with lower maintenance interruptions.

The market spans three primary design configurations — cylindrical, flat plate, and U-channel — each serving distinct force, speed, and space requirements. Cylindrical designs lead with a 48.6% share, reflecting their compact form factor advantage in constrained industrial installations. The diversity of configurations gives linear motors relevance across sectors from semiconductor fabrication to food processing lines.

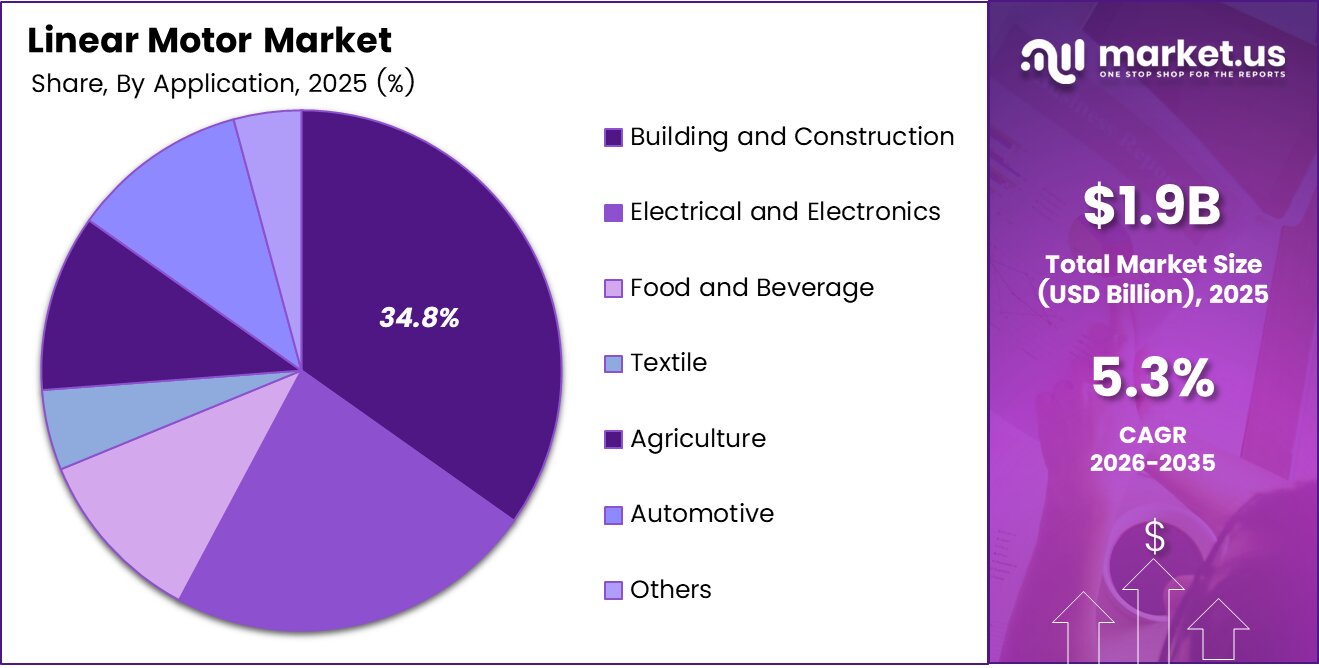

Building and construction applications anchor demand, holding a 34.8% share of the application segment. However, semiconductor manufacturing and electronics assembly represent the fastest-converting use cases, where submicron positioning accuracy is not optional but mandatory. This dynamic suggests that while construction anchors volume, precision electronics will anchor margin.

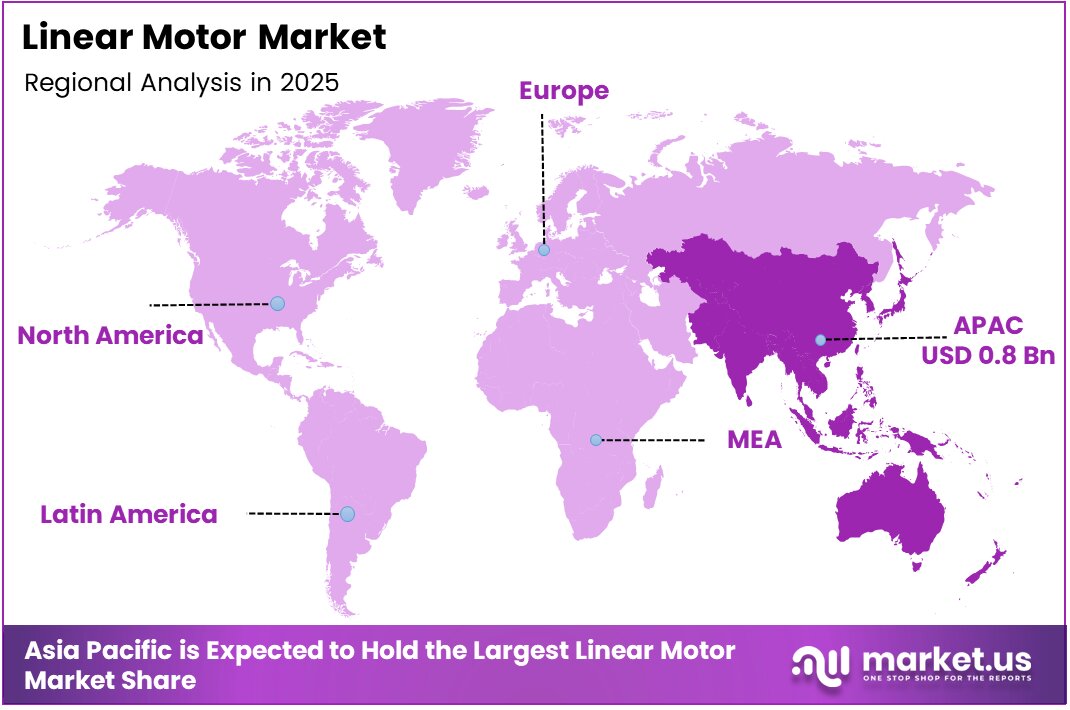

Asia Pacific commands the largest regional share at 42.70%, valued at approximately USD 0.8 Billion. The region’s dense concentration of electronics manufacturing, automotive assembly, and semiconductor fabrication plants creates structural demand that other regions cannot yet replicate at the same scale.

According to a survey cited by PR Newswire, 53% of manufacturers are in the early stages of adopting industrial robots, while 28% already have robots deployed and 40% view robotics as key to quality improvement. This adoption curve directly translates into linear motor procurement cycles, as robotic axes increasingly replace rotary-driven actuators with direct-drive linear alternatives.

According to SEMI, global semiconductor manufacturing equipment sales are projected to reach approximately USD 133 billion in 2025, rising to USD 145 billion in 2026 and USD 156 billion in 2027. Semiconductor fabrication tools depend on linear motors for wafer handling and lithography stages, meaning this equipment growth directly expands the serviceable market for high-precision linear motion suppliers.

Key Takeaways

- The global Linear Motor Market was valued at USD 1.9 Billion in 2025 and is forecast to reach USD 3.2 Billion by 2035, at a CAGR of 5.3%.

- By Design, Cylindrical linear motors dominate with a 48.6% share in 2025.

- By Application, Building and Construction leads with a 34.8% share in 2025.

- Asia Pacific holds the largest regional share at 42.70%, valued at USD 0.8 Billion.

Design Analysis

Cylindrical dominates with 48.6% due to compact form factor in constrained installations.

In 2025, Cylindrical linear motors held a dominant market position in the By Design segment of the Linear Motor Market, with a 48.6% share. Their tubular geometry fits tightly inside machine frames where flat configurations would require additional structural accommodation. Consequently, system integrators default to cylindrical designs when installation space is limited and force density matters.

Flat Plate linear motors carry the highest force-output-to-cost ratio within open-frame machine architectures. They serve as the preferred choice for long-stroke applications such as gantry systems and large-format semiconductor handling stages. Additionally, their modular stacking capability allows engineers to scale thrust output without redesigning the host machine, making them attractive for capital equipment builders managing multi-generation platform strategies.

U-Channel linear motors differentiate through their self-containing magnetic circuit, which eliminates attraction forces on the forcer. This structural advantage reduces bearing load and simplifies carriage design in high-speed transport applications. Therefore, U-channel configurations earn specification preference in pick-and-place automation and electronics assembly systems where carriage weight and bearing life directly affect throughput economics.

Application Analysis

Building and Construction dominates with 34.8% due to broad infrastructure automation demand.

In 2025, Building and Construction held a dominant market position in the By Application segment of the Linear Motor Market, with a 34.8% share. Automated facade installation, prefabricated component handling, and precision concrete forming systems increasingly incorporate linear motor actuators to reduce labor dependency and improve dimensional consistency. This volume position signals that construction automation is becoming a mainstream procurement driver, not a niche application.

Electrical and Electronics serves as the margin anchor within the application mix. PCB placement machines, chip bonding systems, and flat panel display assembly lines require nanometer-level positional repeatability that rotary-driven alternatives cannot deliver economically. Moreover, the semiconductor equipment investment cycle — projected to reach USD 133 billion in 2025 according to SEMI — directly funds new linear motor installations across wafer handling and lithography tool upgrades.

Food and Beverage applications prioritize hygienic drive architectures that tolerate wash-down environments without lubrication contamination risks. Linear motors with sealed forcer designs meet food safety standards while delivering the speed and positioning accuracy that high-throughput packaging lines demand. This segment therefore provides a steady replacement cycle as facilities upgrade legacy pneumatic and belt-driven systems.

Textile manufacturing adopts linear motors in precision loom shuttle systems and automated fabric cutting equipment, where positional accuracy directly affects material yield and waste rates. Reduced fabric waste translates into measurable cost savings per production run, giving linear motor retrofits a calculable return on investment that procurement teams can defend to finance leadership.

Agriculture represents an early-stage but structurally compelling application pathway, particularly in automated seeding, transplanting, and greenhouse harvesting equipment. As labor costs in agricultural economies rise, farm equipment manufacturers face pressure to automate repetitive planting and harvesting tasks — creating a conversion opportunity for compact linear actuator suppliers targeting outdoor-rated motor specifications.

Automotive production lines deploy linear motors primarily in body shop automation, battery module assembly for electric vehicles, and precision welding gantries. The EV production ramp across Asia and Europe creates a direct pull for linear motor systems capable of handling larger battery packs with the accuracy tolerances required for cell-to-cell placement. In April 2025, Kollmorgen introduced a high-voltage IC Ironcore DDL direct drive linear motor supporting 400/480 VAC systems with up to approximately 13,448 N peak force, directly addressing high-force automotive assembly requirements.

Others encompass medical device manufacturing, additive manufacturing equipment, and defense applications — segments where unit volumes remain modest but average selling prices are substantially higher. Suppliers that establish early technical relationships in these verticals benefit from long qualification cycles that create durable revenue streams even as mainstream industrial segments cycle through procurement pauses.

Key Market Segments

By Design

- Cylindrical

- Flat Plate

- U-Channel

By Application

- Building and Construction

- Electrical and Electronics

- Food and Beverage

- Textile

- Agriculture

- Automotive

- Others

Drivers

Precision Automation Mandates and Semiconductor Equipment Growth Accelerate Linear Motor Adoption Across Industrial Sectors

High-precision automation systems in semiconductor fabrication, electronics assembly, and automotive production require positioning accuracy that conventional rotary-driven actuators cannot achieve without complex mechanical transmission. Linear motors eliminate these transmission stages, delivering direct positional control. This architectural advantage makes them the default specification in new capital equipment programs where throughput accuracy is a contractual performance requirement.

Contactless linear motor operation removes wear surfaces between moving and stationary components, which fundamentally changes maintenance economics. Facilities that replace ball-screw actuators with linear motors report extended mean-time-between-failures and lower unplanned downtime. According to SEMI, semiconductor test equipment sales are projected to surge approximately 48.1% to USD 11.2 billion in 2025 — a capital deployment wave that directly funds linear motor content in new test handler and wafer prober designs.

In October 2025, SoftBank Group agreed to acquire ABB’s robotics division in a deal valued at approximately USD 5.4 billion, signaling that major capital allocators view precision motion as a strategic infrastructure asset. This consolidation compresses the timeline for robotic integration across factory floors and raises the specification baseline for embedded linear motion systems. Suppliers with established design-in relationships in robotic joints and end-effectors stand to capture disproportionate share as robot unit volumes scale.

Restraints

High System Acquisition Costs and Skilled Technician Shortages Limit Linear Motor Penetration in Cost-Sensitive Facilities

Linear motor systems carry significantly higher upfront purchase prices than rotary motor and lead-screw assemblies of comparable load capacity. For small and mid-sized manufacturers operating on thin margins, this capital differential is difficult to justify against productivity gains that materialize over multi-year payback periods. Consequently, adoption concentrates in tier-one facilities with established capital investment frameworks rather than diffusing broadly across the supplier base.

Installation and commissioning of linear motor systems requires technicians with specialized knowledge of magnetic circuit tuning, encoder calibration, and servo amplifier configuration. This skill set remains scarce outside major industrial economies, limiting deployment speed in emerging manufacturing regions where labor cost savings would otherwise create a strong adoption rationale. The technician shortage effectively caps market penetration velocity even when financial conditions support investment.

Maintenance and fault diagnosis for linear motor systems also demand technical expertise that standard electricians or mechanical maintenance teams do not possess. Facilities that lack trained personnel face extended repair windows when motors experience cogging anomalies or encoder drift — operational risks that conservative plant managers weigh heavily against the system’s performance advantages. This risk perception slows replacement of legacy rotary systems even in facilities that could financially justify the upgrade.

Growth Factors

Medical Device Expansion, Smart Factory Connectivity, and Energy Efficiency Requirements Open New Revenue Pathways for Linear Motor Suppliers

Medical device manufacturers deploy linear motors in surgical robotics, MRI-compatible positioning stages, and automated laboratory analyzers where electromagnetic cleanliness and sub-millimeter accuracy are non-negotiable. This segment commands premium pricing and involves long qualification timelines that, once cleared, create durable supply relationships. Suppliers that invest in medical-grade linear motor certifications today build a defensible revenue base that insulates them from commodity pricing pressure in industrial segments.

IoT connectivity integration converts standalone linear motors into data-generating nodes within smart factory architectures. Real-time position telemetry, temperature monitoring, and force feedback data feed directly into manufacturing execution systems, enabling predictive maintenance and yield optimization. According to data from Worldmetrics, as of 2023, approximately 35% of industrial robots were integrated with AI, up from 22% in 2020 — a trajectory that accelerates demand for intelligent linear motion components capable of communicating with robot control networks.

Energy-efficient linear motor designs that reduce resistive losses and optimize flux density directly lower the total cost of ownership calculation that procurement engineers use to evaluate capital equipment. As industrial energy costs remain elevated across Europe and North America, facilities actively seek actuator technologies that reduce per-cycle energy consumption. Suppliers that quantify and certify energy savings in standardized test conditions gain a measurable commercial advantage in competitive bid processes.

Emerging Trends

AI-Driven Predictive Maintenance and Lightweight Motor Designs Reshape the Linear Motor Value Proposition for Next-Generation Factories

AI-powered predictive maintenance platforms analyze vibration signatures, thermal profiles, and positional error trends in linear motors to forecast failure events before they cause production stoppages. According to Worldmetrics, AI-driven robotics applications can reduce production defects by 18–25% and cut unplanned downtime by 20–30%. For linear motor operators, these figures translate directly into measurable output gains that justify the software and sensor investment required to implement predictive maintenance programs.

Lightweight and compact linear motor designs reduce the moving mass within high-speed automation cells, which directly improves acceleration performance and lowers motor heating at equivalent thrust levels. Additive manufacturing equipment represents an emerging pull for compact linear actuators where print head positioning speed determines throughput and dimensional accuracy simultaneously. Suppliers that optimize motor geometry for additive manufacturing platforms position themselves in a segment whose capital equipment base is still in formation.

Collaboration between original equipment manufacturers and technology providers to develop application-specific linear motor configurations accelerates qualification timelines for end-users. Rather than adapting standard catalog motors to specialized machine requirements, co-development programs produce optimized magnetic circuit geometries and winding configurations from the outset. This trend shifts competitive differentiation from catalog breadth toward engineering partnership capability — a structural change that favors suppliers with application engineering resources over pure component distributors.

Regional Analysis

Asia Pacific Dominates the Linear Motor Market with a Market Share of 42.70%, Valued at USD 0.8 Billion

Asia Pacific holds a 42.70% share valued at approximately USD 0.8 Billion, driven by the region’s concentration of semiconductor fabrication, consumer electronics production, and automotive assembly capacity. China, Japan, South Korea, and Taiwan operate the world’s highest densities of precision manufacturing facilities — conditions that generate structural, recurring linear motor demand rather than cyclical project-based procurement.

North America Linear Motor Market Trends

North America benefits from strong semiconductor capital expenditure cycles, defense-grade automation procurement, and a mature industrial robotics installed base. The United States houses the largest concentration of advanced semiconductor fabs outside Asia, and ongoing domestic chip manufacturing investment programs create sustained demand for precision linear motion systems embedded in wafer handling and lithography equipment.

Europe Linear Motor Market Trends

Europe drives adoption through its automotive manufacturing heritage and strict energy efficiency regulations that incentivize replacement of legacy actuation technologies. Germany’s machine tool and automotive production ecosystem creates consistent specification demand, while EU industrial policy programs supporting smart factory transitions provide financial mechanisms that lower the capital barrier for linear motor integration in mid-tier facilities.

Middle East and Africa Linear Motor Market Trends

The Middle East and Africa region presents a long-cycle opportunity tied to manufacturing diversification programs in Gulf Cooperation Council economies. Saudi Arabia and the UAE are actively building industrial manufacturing bases to reduce commodity export dependence, and these greenfield facilities specify modern direct-drive automation infrastructure from the outset rather than retrofitting legacy rotary systems.

Latin America Linear Motor Market Trends

Latin America adoption concentrates in Brazil and Mexico, where automotive assembly plants operated by global OEMs serve as the primary pull channel for linear motor procurement. These facilities follow global parent company equipment specifications, meaning linear motor penetration in this region tracks the broader automotive industry’s shift toward electric vehicle production architectures that favor precision direct-drive actuation.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ETEL SA positions itself as a high-precision linear motor specialist serving semiconductor, medical, and metrology applications where standard catalog products cannot meet specification requirements. Its strength lies in engineering customization depth — the ability to co-develop application-specific motor geometries gives ETEL a defensible position in segments where performance differentiation commands premium pricing and long supply relationships.

Mitsubishi Electric Corporation leverages its vertically integrated servo and motion control ecosystem to deliver linear motor solutions pre-optimized for its own amplifier and controller hardware. This integration advantage reduces commissioning time for system integrators and lowers total system cost by eliminating cross-vendor compatibility engineering. Mitsubishi’s broad installed base of factory automation hardware creates a natural pull channel for linear motor adoption within existing customer facilities.

Tecnotion focuses on ironless and iron-core direct drive linear motor platforms designed for high-dynamics applications in semiconductor equipment and precision inspection systems. Its modular coil and magnet track architecture allows customers to configure stroke length and force output without custom motor design, which compresses lead times for capital equipment builders managing aggressive product launch schedules. This flexibility is a commercial differentiator in fast-moving semiconductor tool development cycles.

Rockwell Automation integrates linear motor motion into its broader connected enterprise architecture, enabling customers to manage linear drive performance data within unified plant-wide control and analytics platforms. On March 3, 2025, Zebra Technologies completed its acquisition of Photoneo to expand machine vision and automation capabilities — a complementary development that signals the broader automation ecosystem is converging sensing and motion into unified smart manufacturing platforms, reinforcing Rockwell’s integrated control strategy.

Key players

- ETEL SA

- Mitsubishi Electric Corporation

- Tecnotion

- Rockwell Automation

- Aerotech, Inc.

- FANUC CORPORATION

- Hiwin Corporation

- Sinotech, Inc.

- FAULHABER GROUP

- YASKAWA ELECTRIC CORPORATION

Recent Developments

- April 2025 – Kollmorgen introduced a high-voltage IC Ironcore DDL direct drive linear motor supporting 400/480 VAC systems with up to approximately 13,448 N peak force. This product targets high-force industrial and automotive assembly applications where existing lower-voltage linear motor platforms previously required oversized mechanical amplification stages.

- September 2025 – EVS announced the acquisition of French robotics and control systems provider XD Motion, creating an integrated T-Motion solution for advanced media production robotics. The deal expands EVS’s motion control capabilities into precision broadcast production environments where linear positioning accuracy directly affects camera movement quality.

Report Scope

Report Features Description Market Value (2025) USD 1.9 Billion Forecast Revenue (2035) USD 3.2 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Design (Cylindrical, Flat Plate, U-Channel), By Application (Building and Construction, Electrical and Electronics, Food and Beverage, Textile, Agriculture, Automotive, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ETEL SA, Mitsubishi Electric Corporation, Tecnotion, Rockwell Automation, Aerotech, Inc., FANUC CORPORATION, Hiwin Corporation, Sinotech, Inc., FAULHABER GROUP, YASKAWA ELECTRIC CORPORATION Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Parker-Hannifin Corporation

- YASKAWA Electric Corporation

- Panasonic Corp.

- Rockwell Automation Inc.

- ETEL S.A.

- ETEL S.A.

- ESR Pollmeier GmbH

- Jenny Science AG

- Oswald Elektromotoren GmbH

Our Clients

- 28753

- Feb 2026