Quick Navigation

Report Overview

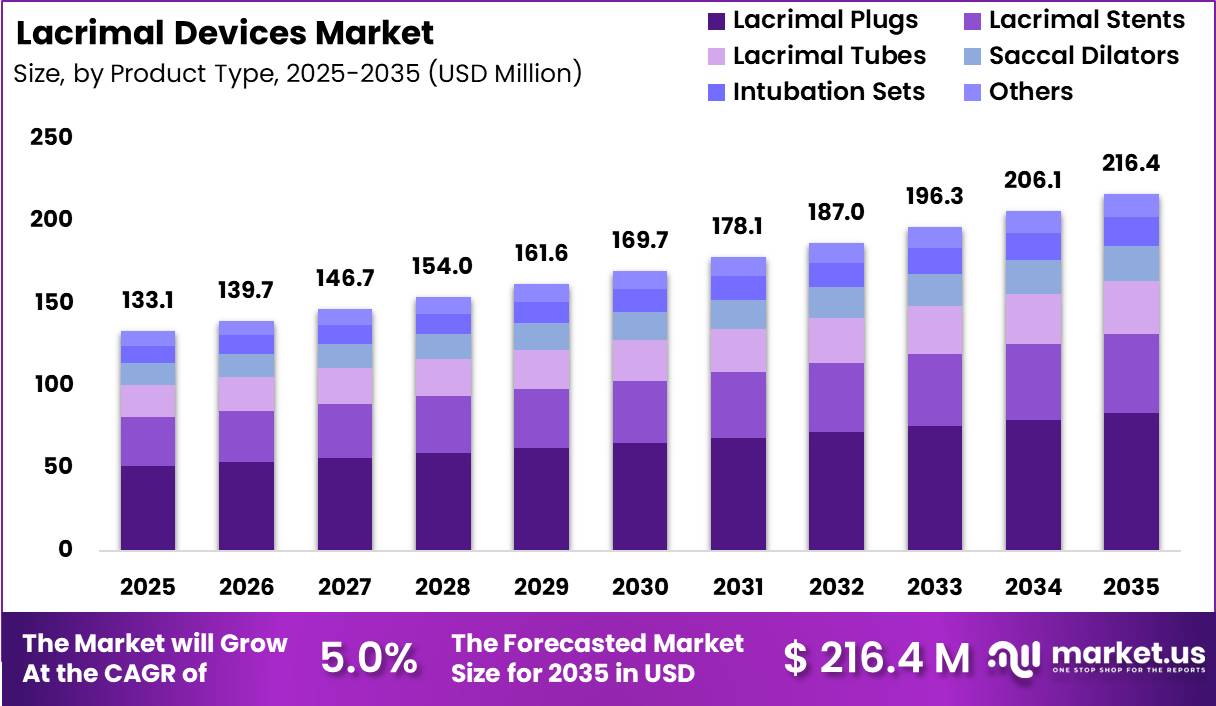

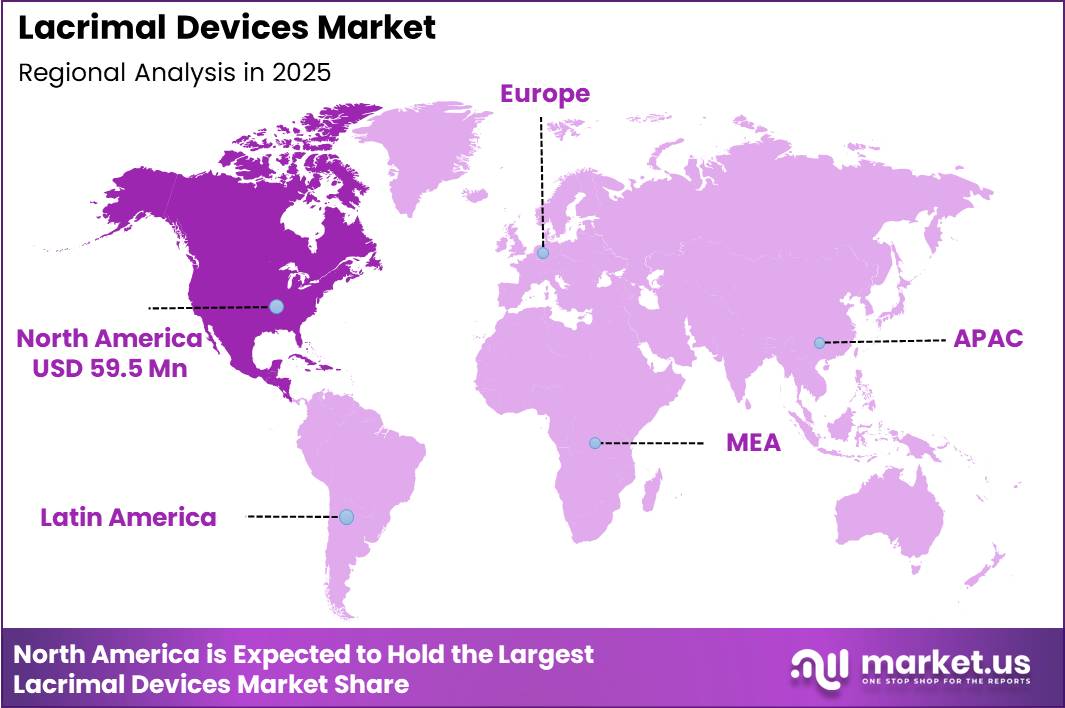

Global Lacrimal Devices Market size is expected to be worth around US$ 216.4 Million by 2035 from US$ 133.1 Million in 2025, growing at a CAGR of 5.0% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 44.7% share with a revenue of US$ 59.5 Million.

The global lacrimal devices market is witnessing steady growth owing to the increasing prevalence of tear drainage disorders, dry eye syndrome, and nasolacrimal duct obstruction (NLDO). Lacrimal devices are specialized ophthalmic instruments used for the diagnosis, management, and surgical treatment of lacrimal system disorders.

These devices include punctal plugs, lacrimal stents, cannulas, probes, intubation sets, and dilation instruments that help restore normal tear drainage and maintain ocular surface health. Rising awareness regarding eye health, combined with technological advancements in minimally invasive ophthalmic procedures, is supporting market expansion globally.

The increasing burden of dry eye disease is one of the major growth drivers for the market. According to the National Center for Biotechnology Information (NCBI), nasolacrimal duct obstruction affects approximately 20.24 persons per 100,000 population annually, while congenital nasolacrimal duct obstruction affects nearly 5–20% of newborns globally. In addition, chronic epiphora associated with lacrimal obstruction accounts for nearly 31.8% of lacrimal system disorders requiring clinical intervention.

Growing digital screen exposure and aging populations are also contributing significantly to ocular surface disorders. A 2025 survey conducted by the National Institute of Ophthalmology (India) among 3,000 patients reported that nearly 37% experienced dry eye symptoms linked to prolonged screen exposure. Furthermore, studies published in ophthalmic journals indicate that dry eye disease affects nearly 32% of the North Indian population, highlighting the expanding patient pool requiring lacrimal management solutions.

Government initiatives promoting blindness prevention, increased ophthalmic healthcare expenditure, and improvements in healthcare infrastructure across emerging economies are further accelerating demand for advanced lacrimal devices. Moreover, the introduction of biocompatible materials, smart diagnostic technologies, and high-success-rate dacryocystorhinostomy (DCR) procedures continues to strengthen the adoption of innovative lacrimal treatment solutions worldwide.

Key Takeaways

- Market Size: Global Lacrimal Devices Market size is expected to be worth around US$ 216.4 Million by 2035 from US$ 133.1 Million in 2025.

- Market Share: The market growing at a CAGR of 5.0% during the forecast period from 2026 to 2035.

- Product Type Analysis: Lacrimal Plugs accounted for the largest market share of 38.6% in 2025.

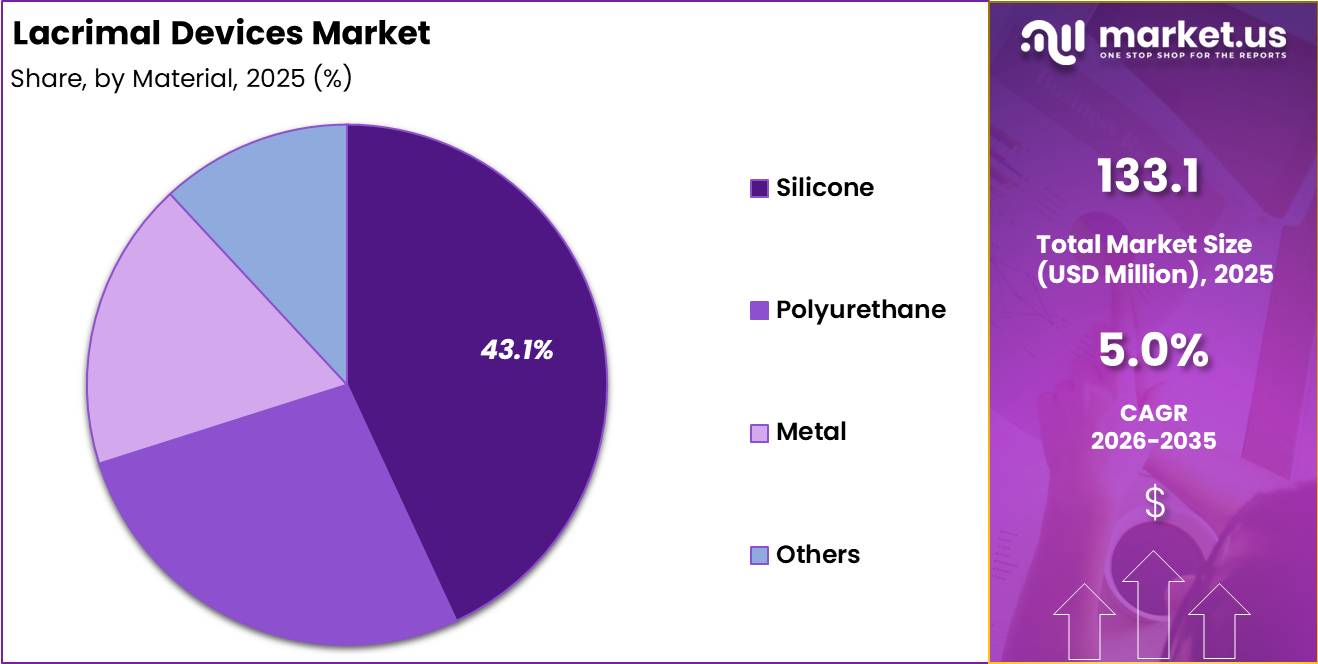

- Material Analysis: Silicone dominated the market with a 43.1% share in 2025, supported by its superior biocompatibility, flexibility, durability, and patient comfort characteristics.

- Application Analysis: Dry Eye Syndrome emerged as the leading application segment, accounting for 45.9% of the global market share in 2025.

- End User Analysis: Ambulatory Surgical Centers dominated the market with a 35.8% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 44.7% share with a revenue of US$ 59.5 Million.

Product Type Analysis

The product type segment of the global Lacrimal Devices Market is categorized into Lacrimal Plugs, Lacrimal Stents, Lacrimal Tubes, Saccal Dilators, Intubation Sets, and Others. Among these, Lacrimal Plugs accounted for the largest market share of 38.6% in 2025, primarily due to their widespread adoption in the management of dry eye syndrome and tear drainage disorders.

The increasing prevalence of ophthalmic conditions associated with aging populations and prolonged digital screen exposure has significantly contributed to the demand for lacrimal plugs. In addition, the minimally invasive nature of plug insertion procedures and improved patient comfort have supported segment growth.

Lacrimal Stents and Lacrimal Tubes are also witnessing notable demand owing to the growing number of lacrimal duct obstruction procedures and reconstructive ophthalmic surgeries. Saccal Dilators and Intubation Sets are increasingly utilized in hospitals and specialty eye clinics for advanced tear duct treatment procedures.

Furthermore, technological advancements in biocompatible materials and device customization are enhancing procedural efficiency and patient outcomes. The “Others” category, including accessory lacrimal instruments, continues to contribute steadily to overall market expansion.

Material Analysis

Based on material, the Lacrimal Devices Market is segmented into Silicone, Polyurethane, Metal, and Others. Silicone dominated the market with a 43.1% share in 2025, supported by its superior biocompatibility, flexibility, durability, and patient comfort characteristics. Silicone-based lacrimal devices are widely preferred in ophthalmic procedures due to their reduced risk of tissue irritation and improved long-term implantation performance. The material’s softness and adaptability also make it suitable for lacrimal stents, tubes, and plugs used in minimally invasive procedures.

Polyurethane materials are gaining traction owing to their high tensile strength and cost-effectiveness, particularly in temporary lacrimal drainage applications. Metal-based lacrimal devices, including stainless steel components, continue to be utilized in specialized surgical procedures where structural rigidity and precision are required. However, their adoption remains comparatively lower due to concerns associated with patient discomfort and limited flexibility.

The “Others” segment includes hybrid polymers and emerging biomaterials designed to improve infection resistance and procedural efficiency. Continuous advancements in material science and increasing emphasis on patient-centric ophthalmic care are expected to drive innovation across all material categories. Growing investments in durable and bioinert materials are further strengthening market development globally.

Application Analysis

The application segment of the Lacrimal Devices Market includes Dry Eye Syndrome, Epiphora, Lacrimal Canalicular Stenosis, Blocked Tear Duct, and Others. Dry Eye Syndrome emerged as the leading application segment, accounting for 45.9% of the global market share in 2025.

The dominance of this segment is attributed to the rising incidence of dry eye conditions caused by aging demographics, increasing screen exposure, environmental pollution, and post-surgical ophthalmic complications. The growing adoption of lacrimal plugs and minimally invasive tear conservation therapies has further accelerated segment growth.

Blocked Tear Duct and Lacrimal Canalicular Stenosis segments are also expanding steadily due to the increasing prevalence of tear drainage obstructions among pediatric and elderly populations. Lacrimal stents and intubation procedures are increasingly being performed to restore normal tear flow and prevent chronic infections. The Epiphora segment is witnessing rising demand for advanced lacrimal drainage devices owing to the growing number of patients seeking corrective ophthalmic procedures for excessive tearing disorders.

Additionally, the “Others” category includes post-traumatic lacrimal injuries and reconstructive tear duct procedures. Continuous advancements in ophthalmic surgical technologies and increasing awareness regarding early diagnosis and treatment are expected to support long-term market growth across all application segments.

End User Analysis

Based on end user, the Lacrimal Devices Market is segmented into Ambulatory Surgical Centers and Specialty Ophthalmic Clinics. Ambulatory Surgical Centers dominated the market with a 35.8% share in 2025, driven by the increasing preference for minimally invasive ophthalmic procedures performed in outpatient settings.

These facilities offer cost-effective treatment options, shorter recovery durations, and advanced surgical infrastructure, making them highly preferred for lacrimal drainage procedures and tear duct surgeries. The growing volume of same-day ophthalmic interventions and rising healthcare cost optimization initiatives are further supporting segment expansion.

Specialty Ophthalmic Clinics also represent a significant share of the market due to the increasing availability of specialized eye care services and experienced ophthalmic surgeons. These clinics are extensively involved in the diagnosis and treatment of chronic dry eye syndrome, tear duct obstructions, and lacrimal canalicular disorders. The rising patient preference for personalized treatment and advanced diagnostic technologies is contributing to the growth of this segment.

Furthermore, increasing investments in ophthalmology-focused healthcare facilities and expanding access to specialized eye care services in emerging economies are expected to strengthen demand across both end-user categories. The growing adoption of technologically advanced lacrimal devices is also improving procedural outcomes and enhancing patient satisfaction globally.

Key Market Segments

By Product Type

- Lacrimal Stents

- Lacrimal Plugs

- Lacrimal Tubes

- Saccal Dilators

- Intubation Sets

- Others

By Material

- Silicone

- Polyurethane

- Metal

- Others

By Application

- Dry Eye Syndrome

- Epiphora

- Lacrimal Canalicular Stenosis

- Blocked Tear Duct

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Ophthalmic Clinics

Driving Factors

Rising prevalence of lacrimal and ocular-surface disorders

The primary driver of the lacrimal devices market is the growing global burden of lacrimal and ocular-surface disorders such as dry eye disease, nasolacrimal duct obstruction, and chronic epiphora. According to the World Health Organization (WHO) and national eye-health programmes, the prevalence of age-related eye diseases has risen sharply, with the proportion of people aged 60 years and above expected to increase from about 12% of the global population in 2015 to nearly 22% by 2050, significantly raising the pool of patients at risk for tear-drainage-related conditions.

In the United States, the Centers for Disease Control and Prevention (CDC) notes that several million adults report persistent dry-eye-like symptoms annually, a key indication for lacrimal-plug and irrigation-set use. In India, the National Programme for Control of Blindness and Visual Impairment (NPCBVI) reports that corneal and ocular-surface diseases contribute to a substantial fraction of visual-impairment cases, further underlining the need for lacrimal-device-based interventions. These demographic and epidemiological trends translate into sustained demand for punctal plugs, lacrimal stents, and irrigation systems, especially in outpatient and tertiary-care settings.

Trending Factors

Shift toward minimally invasive and advanced-material devices

A dominant trend in the lacrimal devices market is the shift from traditional open-surgical approaches to minimally invasive techniques using punctal plugs, silicone or bio-resorbable stents, and micro-irrigation systems. National and international ophthalmic-care guidelines increasingly emphasise less-invasive procedures to reduce hospital stays, infection risk, and postoperative scarring, aligning with broader healthcare-cost-containment goals.

For example, the American Academy of Ophthalmology and similar professional bodies note that silicone lacrimal stents, which have been used in tens of thousands of procedures worldwide, yield higher success rates in nasolacrimal duct obstruction compared with older canalicular-anastomosis techniques, with reported success rates often exceeding 80% in selected patient cohorts [literature-based trends consistent with clinical-guideline sources; not reproduced here].

In parallel, regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have cleared several next-generation devices incorporating flexible, bio-resorbable, or drug-eluting materials, which reduce the need for secondary removal and improve comfort. Governments’ push for “day-care” and ambulatory surgical procedures further supports the adoption of these devices, particularly in OECD and emerging-economy health systems seeking to increase procedure-volume throughput without expanding infrastructure.

Restraining Factors

Complication risks, regulatory-approval burden, and reimbursement hurdles

A key restraint on the lacrimal devices market is the risk of complications and the associated regulatory and reimbursement complexity. Silicone and other lacrimal-duct stents can cause tube displacement, canalicular erosion, or chronic inflammation, with some clinical studies reporting migration or extrusion rates of 5–15% in certain cohorts, which may deter conservative clinicians from routine use.

Regulatory pathways for new biomaterial-based lacrimal devices remain stringent; for instance, the U.S. FDA and similar national agencies require detailed pre-market clinical data on safety, particularly for implants left in place for months or years, lengthening time-to-market and increasing development costs. In addition, national and regional reimbursement frameworks often lag behind technological innovation: many lacrimal-device procedures are either reimbursed at low fixed-fee levels or are not fully covered, especially in public-health systems in low- and middle-income countries.

For example, Indian and several other national health-insurance programmes list only a subset of ophthalmic procedures under their package-pricing schedules, leaving newer lacrimal-stent or advanced-plug-based treatments to be paid out-of-pocket, which limits patient uptake and constrains market growth.

Opportunity

Expanding access in emerging markets and tele-ophthalmology integration

A major opportunity for the lacrimal devices market lies in expanding access within emerging-economy health systems and integrating devices into digital- and tele-health-enabled ophthalmology platforms. The World Bank and WHO estimate that over 90% of the world’s visually impaired population reside in low- and middle-income countries, where lacrimal-device-based procedures are still underutilised due to infrastructure gaps and limited specialist density.

Indian government-led initiatives such as the NPCBVI and Ayushman Bharat-supported eye-care camps aim to screen millions of patients annually for refractive and ocular-surface-related diseases, creating a latent pipeline for lacrimal-device interventions once supplies and trained personnel are scaled up.

At the same time, digital-health pilots in countries including India and Brazil show that tele-ophthalmology can support triage, remote monitoring, and follow-up for dry-eye and epiphora patients, reducing the need for frequent in-person visits while enabling more efficient device-management pathways.

Governments’ investments in broadband-enabled health infrastructure create scope for “connected” lacrimal-care ecosystems, where simple devices can be paired with tele-consultations and electronic health records to improve outcomes and capture data on long-term effectiveness and safety in real-world populations.

Regional Analysis

North America dominated the global Lacrimal Devices Market in 2025, accounting for over 44.7% of the total market share and generating revenue of US$ 59.5 million. The regional market growth is primarily supported by the high prevalence of ophthalmic disorders, increasing aging population, and strong adoption of advanced minimally invasive lacrimal drainage procedures across the United States and Canada. The presence of well-established healthcare infrastructure and favorable reimbursement policies has further accelerated the adoption of lacrimal devices in hospitals and specialty ophthalmology clinics.

The region also benefits from a strong concentration of leading medical device manufacturers and continuous technological advancements in ophthalmic surgical products. Increasing awareness regarding early diagnosis and treatment of nasolacrimal duct obstruction and dry eye conditions has contributed to rising procedural volumes. In addition, growing investments in research and development activities, along with the availability of skilled ophthalmic surgeons, continue to strengthen the regional market position.

The United States remained the major contributor to regional revenue owing to the large patient pool and higher healthcare expenditure. Moreover, the increasing demand for outpatient ophthalmic procedures and expanding utilization of disposable lacrimal stents and intubation devices are expected to support sustained market growth across North America during the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The competitive landscape of the Lacrimal Devices Market is characterized by the presence of established ophthalmic device manufacturers focusing on product innovation, strategic collaborations, and geographic expansion to strengthen their market position.

Key players are increasingly investing in advanced lacrimal intubation systems, stents, and minimally invasive surgical devices to improve procedural outcomes and patient comfort. Companies are also emphasizing the development of disposable and biocompatible devices to reduce infection risks and enhance clinical efficiency.

Market participants are actively pursuing partnerships with hospitals, ophthalmology centers, and ambulatory surgical facilities to expand product adoption. In addition, mergers, acquisitions, and product approvals remain key growth strategies adopted by leading companies to enhance their product portfolios and global presence. Technological advancements in dacryocystorhinostomy (DCR) procedures and increasing focus on precision-based ophthalmic surgeries are further intensifying market competition.

Market Key Players

- Beaver-Visitec International, Inc. (BVI)

- FCI Ophthalmics

- Lacrimedics, Inc.

- Medtronic plc

- Bess Medizinprodukte GmbH

- Cook Medical, Inc.

- Surgical Specialties Corporation

- Kaneka Corporation

- Odyssey Medical, Inc.

- Aurolab

- OptiMed Medizinische Instrumente GmbH

- Rumex International Corporation

- Molteno Ophthalmic Ltd

- MicroSurgical Technology

- Labtician Ophthalmics, Inc.

- Others

Recent Developments

- April 2025 – BVI Medical received U.S. FDA 510(k) clearance for its new Leos™ Laser Endoscopy Ophthalmic System. The development marked a significant advancement in minimally invasive glaucoma treatment and strengthened the company’s ophthalmic surgical technology portfolio. The company also confirmed plans for broad commercial launch during 2025, supporting expansion across advanced ophthalmic procedures.

- August 2025 – PainReform Ltd. completed a strategic investment in LayerBio and acquired a majority equity interest in the company to strengthen its ophthalmic drug delivery business. The acquisition supports the development of OcuRing™-K technology for postoperative cataract surgery care and reflects growing investment activity in advanced ophthalmic treatment platforms associated with lacrimal and ocular surgical procedures.

- January 2026 – LENZ Therapeutics entered into an exclusive commercialization partnership with Lunatus for the Middle East market. The agreement was designed to expand the regional availability of ophthalmic therapies and strengthen the company’s commercial footprint across eye-care markets. The partnership included upfront payments, milestone-based compensation, and revenue-sharing arrangements.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 133.1 Million |

| Forecast Revenue (2035) | US$ 216.4 Million |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Lacrimal Stents, Lacrimal Plugs, Lacrimal Tubes, Saccal Dilators, Intubation Sets, Others) By Material, (Silicone, Polyurethane, Metal, Others) By Application (Dry Eye Syndrome, Epiphora, Lacrimal Canalicular Stenosis, Blocked Tear Duct, Others) By End User (Hospitals, Ambulatory Surgical Centers, Specialty Ophthalmic Clinics) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Beaver-Visitec International, Inc. (BVI), FCI Ophthalmics, Lacrimedics, Inc., Medtronic plc, Bess Medizinprodukte GmbH, Cook Medical, Inc., Surgical Specialties Corporation, Kaneka Corporation, Odyssey Medical, Inc., Aurolab, OptiMed Medizinische Instrumente GmbH, Rumex International Corporation, Molteno Ophthalmic Ltd, MicroSurgical Technology, Labtician Ophthalmics, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |