Global Interferon Market By Product Type (Alpha Interferons, Beta Interferons and Gamma Interferons), By Application (Cancer Treatment, Viral Infections, Autoimmune Diseases and Others), By Route of Administration (Subcutaneous Injection, Intravenous Injection and Intramuscular Injection), By End-User (Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, Research and Academic Institutes, and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: July 2025

- Report ID: 152770

- Number of Pages: 303

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Application Analysis

- Route of Administration Analysis

- End-User Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

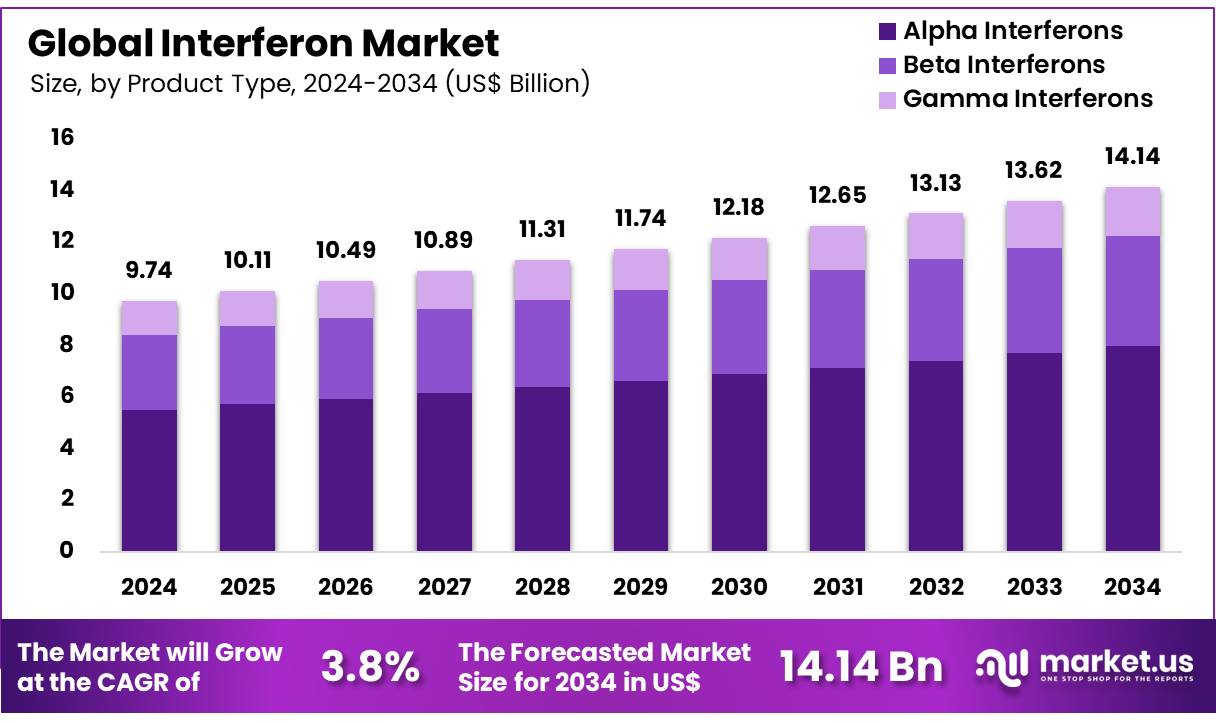

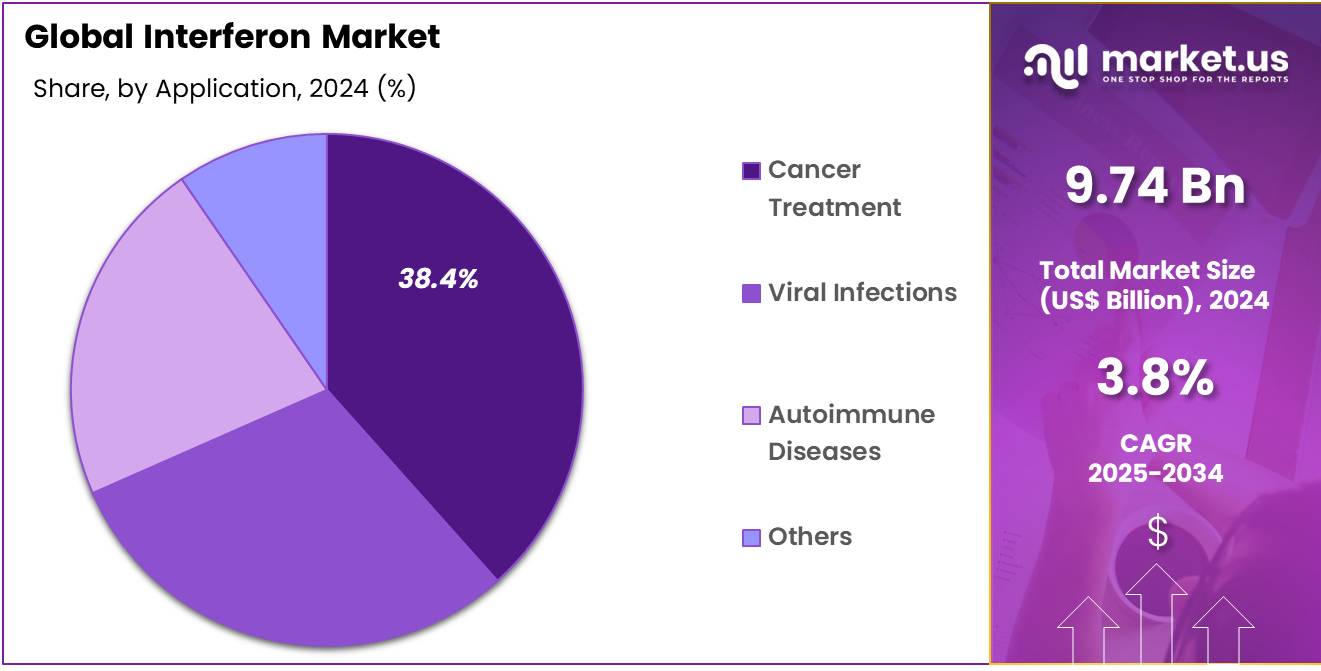

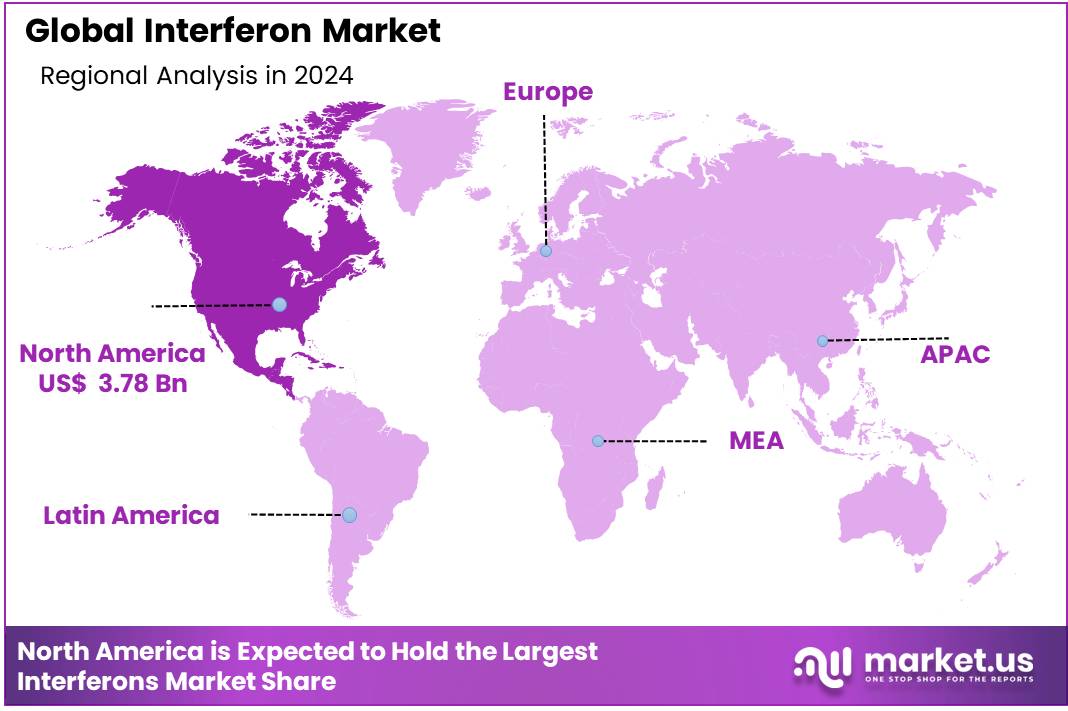

Global Interferon Market size is expected to be worth around US$ 14.14 billion by 2034 from US$ 9.74 billion in 2024, growing at a CAGR of 3.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.8% share with a revenue of US$ 3.78 Billion.

The Interferon Market is experiencing rapid growth within the global pharmaceutical sector, driven by the increasing incidence of chronic diseases, viral infections, and autoimmune disorders.

Interferons, a class of cytokines, play a crucial role in treating conditions like hepatitis, multiple sclerosis, and various cancers. As a vital component of immunotherapy, interferons help regulate the immune system, providing antiviral, anti-tumor, and immunoregulatory effects, which makes them essential for managing several serious conditions.

Market growth is further supported by advancements in biotechnology, particularly with the development of interferon biosimilars. These biosimilars present a more affordable alternative to branded interferon treatments, enhancing access, especially in emerging markets.

Additionally, the increasing demand for personalized medicine is expected to drive the market’s expansion, as genetic advancements enable therapies that are more tailored to individual patients, improving efficacy and minimizing side effects. Increased healthcare investments in both developed and developing regions are also contributing to market growth.

In September 2024, new research from The Wistar Institute’s Montaner lab, led by Luis Montaner, D.V.M., D.Phil., Executive Vice President and Director of the HIV Cure and Viral Disease Center, alongside Herbert Kean, M.D., Family Professor, has successfully isolated and cloned fully human antibodies capable of blocking specific Type-I interferon molecules in vitro. This breakthrough opens up a range of clinical and research possibilities, providing scientists with a novel method to study the role of specific Type-I interferons across various diseases.

Despite its growth, the market faces challenges such as the notable side effects of interferon therapies, including flu-like symptoms, fatigue, and potential bone marrow suppression. These adverse effects can affect patient adherence and limit the broader adoption of interferon treatments. Moreover, regulatory challenges and the high cost of branded interferon drugs pose barriers to market growth in certain regions.

Key Takeaways

- In 2024, the market for Interferons generated a revenue of US$ 74 billion, with a CAGR of 3.8%, and is expected to reach US$ 14.14 billion by the year 2034.

- The Product Type segment is divided into Alpha Interferons, Beta Interferons and Gamma Interferons with Alpha Interferons taking the lead in 2024 with a market share of 56.50%.

- By Application, the market is bifurcated into Cancer Treatment, Hepatitis, Viral Infections, Autoimmune Diseases and Others, with Cancer Treatment leading the market with 38.4% of market share.

- By Route of Administration, the market is fragmented into Subcutaneous Injection, Intravenous Injection and Intramuscular Injection, with Subcutaneous Injection taking the lead in 2024 with 45.8% market share.

- Furthermore, concerning the End-User segment, the market is segregated into Government & Regulatory Bodies, Healthcare Institutions, Agricultural Sector, Research & Academia, and

- Private & Commercial Sectors. The Hospitals and Clinics stands out as the dominant segment, holding the largest revenue share of 52.4% in the Interferons market.

- North America led the market by securing a market share of 38.8% in 2024.

Product Type Analysis

The Alpha Interferons segment dominates the Interferon Market with a market share of 56.5% due to their wide application in the treatment of various viral infections and certain types of cancers. Alpha interferons are commonly used to treat conditions like hepatitis B and C, and they also play a key role in the treatment of chronic myelogenous leukemia and melanoma.

Their established efficacy and broad clinical approval contribute significantly to their dominance in the market. The segment is expected to maintain a leading position, driven by the increasing global prevalence of viral infections, as well as the continued need for immunomodulatory treatments for cancer.

Application Analysis

The Cancer Treatment segment is the dominant application area in the Interferon Market which accounted for 38.4% market share, driven by the increasing global cancer burden and the growing adoption of immunotherapy. Interferons, particularly alpha interferons, have been pivotal in treating cancers such as melanoma, renal cell carcinoma, and certain leukemias.

A report from NCBI published in October 2024 states that renal cell carcinoma (RCC) is the most prevalent malignant kidney tumor, accounting for over 90 percent of all renal malignancies. RCC can be sporadic, making up about 96% of cases, or familial, which represents around 4%. It is a heterogeneous condition, comprising several distinct subtypes, each linked to specific genetic abnormalities. They work by stimulating the immune system to recognize and fight tumor cells more effectively, a key component of immunotherapy in oncology.

The rising incidence of cancer worldwide, coupled with an increasing focus on targeted and immuno-oncological therapies, has contributed to the growing adoption of interferon treatments in oncology. Alpha interferons have been widely used for years, with many regulatory bodies approving their use as part of cancer management regimens.

As cancer treatments evolve, the role of interferons is expanding into newer areas of oncology, increasing their market share. In addition, ongoing research into the synergistic effects of combining interferons with other cancer therapies, such as chemotherapy, checkpoint inhibitors, and monoclonal antibodies, is expected to further drive demand in this segment.

Route of Administration Analysis

In the Route of Administration category, Subcutaneous Injection is the dominant method for delivering interferons which accounted for over 45.8% market share in 2024, particularly in the treatment of chronic conditions such as hepatitis, multiple sclerosis, and certain cancers. Subcutaneous injections are preferred by both healthcare providers and patients due to their ease of administration and minimal discomfort compared to other methods like intravenous or intramuscular injections.

Subcutaneous administration allows for a more controlled and slower release of the medication, which is ideal for conditions requiring long-term, consistent treatment. For patients with chronic diseases, such as hepatitis C or multiple sclerosis, subcutaneous injection offers convenience and improved adherence to therapy. This method also supports the home administration of interferon treatments, which enhances patient compliance, reduces healthcare costs, and increases comfort, particularly for long-term therapies.

The availability of pre-filled syringes and auto-injectors has further increased the popularity of subcutaneous injections, making them even easier for patients to administer themselves. This route is also associated with fewer side effects, as it avoids the complications sometimes seen with intravenous injections, such as vein irritation or infections.

End-User Analysis

The Hospitals and Clinics segment is the leading end-user in the Interferons market with 52.4% market share, accounting for the majority of interferon administration worldwide. Hospitals and clinics are the primary settings for the diagnosis, treatment, and management of chronic diseases, cancers, and viral infections, all of which often require interferon therapy. These healthcare institutions provide an environment where specialized medical staff can closely monitor and manage patient care during interferon treatment, particularly in conditions requiring long-term administration, such as hepatitis C or multiple sclerosis.

The presence of advanced medical equipment, access to diagnostic tools, and expert clinicians make hospitals and clinics the ideal place for interferon therapy. Furthermore, the demand for interferon treatments is particularly high in these settings due to the rising prevalence of cancer and chronic diseases, which require specialized care. Hospitals also offer the infrastructure necessary for handling adverse reactions or side effects, providing patients with immediate care if needed.

Key Market Segments

Product Type

- Alpha Interferons

- Beta Interferons

- Gamma Interferons

Application

- Cancer Treatment

- Viral Infections

- Autoimmune Diseases

- Others

Route of Administration

- Subcutaneous Injection

- Intravenous Injection

- Intramuscular Injection

End-User

- Hospitals and Clinics

- Pharmaceutical and Biotechnology Companies

- Research and Academic Institutes

- Others

Drivers

Increasing Prevalence of Chronic Diseases

The rising incidence of chronic diseases, particularly cancer, viral infections, and autoimmune disorders, is a major driver for the Interferon Market. An estimated 129 million people in the US live with at least one major chronic disease, such as heart disease, cancer, diabetes, obesity, or hypertension, according to the US Department of Health and Human Services.

Five of the top 10 leading causes of death in the US are either directly linked to or strongly associated with preventable and treatable chronic diseases. Over the past two decades, the prevalence of these conditions has increased consistently, and this trend is expected to continue. A growing number of Americans are facing multiple chronic conditions, with 42% affected by two or more and 12% by at least five.

In addition to the personal toll, chronic disease places a significant strain on the US healthcare system, accounting for about 90% of the annual $4.1 trillion healthcare expenditure, which is spent on managing and treating these conditions and mental health disorders.

Interferons, being effective immunomodulatory agents, are widely used in the treatment of conditions such as multiple sclerosis, hepatitis, and various cancers. As healthcare awareness grows and diagnostic tools improve, more individuals are being diagnosed with conditions that require interferon-based therapies. For instance, in the case of hepatitis C, interferons have been used as a standard therapy, driving demand for these products.

Similarly, the expanding number of cancer patients, particularly those with solid tumors, is expected to increase the adoption of interferon treatments. The global aging population also contributes to the growing burden of chronic diseases, further boosting the demand for interferons as a part of effective treatment regimens. With increasing investment in healthcare infrastructure and rising awareness about these therapies, the market for interferons is expected to experience steady growth in the coming years.

Restraints

Side Effects and Safety Concerns

Despite the effectiveness of interferons in treating various conditions, their usage is often limited due to significant side effects. Common adverse reactions include flu-like symptoms, fatigue, and bone marrow suppression, which can affect patient compliance. These side effects can reduce the overall effectiveness of interferons, particularly for long-term treatments. In some cases, patients may be forced to discontinue therapy or switch to alternative medications, impacting the market’s growth potential.

Additionally, concerns about the long-term safety profile of interferons, particularly with chronic usage, can hinder their widespread adoption. Regulatory bodies such as the FDA and EMA are stringent in their approval processes, demanding comprehensive clinical data on safety and efficacy. These safety concerns may limit the adoption of interferons, especially in developing regions where healthcare infrastructure may not adequately support the management of side effects.

Opportunities

Advances in Biotechnology and Biosimilars

The development of biosimilar interferons represents a significant opportunity in the Interferon Market. As patents for original interferon products expire, pharmaceutical companies have the chance to introduce biosimilar versions, offering a more affordable alternative to the branded drugs. These biosimilars are expected to expand market access, particularly in developing regions where the cost of original interferons can be prohibitive.

With the increasing demand for cost-effective treatments, the entry of biosimilars is expected to improve the accessibility of interferons, thus broadening their patient base. Moreover, advances in biotechnology, including the development of next-generation interferons with improved efficacy and reduced side effects, present further opportunities for innovation.

Companies investing in research and development to enhance the therapeutic potential of interferons will benefit from capturing a larger market share and meeting unmet medical needs. In January 2025, Shanghai Henlius Biotech, Inc. (2696.HK) has today announced that it has entered into a product license and supply agreement with Abbott.

Under this agreement, Abbott will receive exclusive or semi-exclusive licenses to commercialize four self-developed biosimilars and one innovative biologic across 69 emerging markets in Asia, Latin America, the Caribbean, as well as the Middle East and Africa. This new agreement expands on the existing collaboration between the two companies for the commercialization of oncology biosimilars.

Impact of Macroeconomic / Geopolitical Factors

Economic growth and stability directly affect healthcare spending, particularly in emerging markets where economic conditions can influence the affordability and accessibility of expensive treatments like interferons. In developed regions, economic recessions or budget cuts in healthcare can lead to restrictions on drug pricing and reimbursement policies, potentially making interferon therapies less accessible.

Additionally, inflationary pressures on healthcare costs can further burden patients and governments, leading to a rise in demand for affordable biosimilars as alternatives to branded interferons. The rising healthcare expenditure in developed economies, however, has facilitated greater investments in biotechnology and pharmaceutical research, enabling advancements in interferon-based treatments and biosimilar options. Furthermore, rising disposable incomes in emerging economies can lead to increased healthcare access, fueling market demand.

Geopolitical tensions, trade barriers, and regulatory differences across regions can disrupt the global supply chain for interferons. Trade policies that impact the import or export of raw materials and finished pharmaceutical products could lead to shortages or price hikes. Political instability in regions with key manufacturing hubs may also delay the production and distribution of interferon therapies. Moreover, differing regulatory approvals across countries can impact the availability and timely access to interferon treatments, particularly in regions with stringent drug approval processes.

Latest Trends

Shift Toward Personalized Medicine

A notable trend in the Interferon Market is the shift toward personalized medicine. With advancements in genomics and precision medicine, there is increasing focus on tailoring interferon therapies to individual patients based on their genetic makeup and specific disease characteristics.

Personalized medicine allows healthcare providers to optimize treatment plans by selecting the most appropriate dosage and type of interferon for each patient, thus enhancing treatment outcomes. This trend is especially prevalent in the treatment of cancers and autoimmune diseases, where genetic differences can significantly influence the response to interferon therapies.

Personalized medicine also involves monitoring patient biomarkers to adjust treatment regimens over time, ensuring the best possible response. This trend is supported by the increasing availability of genetic testing and advanced diagnostic technologies, allowing clinicians to better match therapies to individual patient needs. As the understanding of molecular pathways and biomarkers improves, personalized interferon therapies are expected to become more common, driving innovation and market growth.

As per the report titled “Personalized Medicine at FDA: The Scope & Significance of Progress in 2023” by the Personalized Medicine Coalition (PMC) reports that personalized medicines accounted for more than one-third of new drug approvals by the U.S. Food and Drug Administration (FDA) in 2023, marking the fourth consecutive year this has occurred.

The trend toward personalized treatment approvals has been particularly noticeable in the rare disease sector, where the number of new treatment approvals more than doubled in 2023. The U.S. Food and Drug Administration (FDA) approved 16 new personalized treatments for rare disease patients in 2023, a significant increase from the six approved in 2022. Among the newly approved treatments, seven were for cancer, and three were for other diseases and conditions.

Regional Analysis

North America is leading the Interferon Market

The North American Interferon Market is the largest globally accounting for 38.8% market share, driven by advanced healthcare infrastructure, high disease prevalence, and robust research and development (R&D) activities. The U.S. and Canada lead in market share, supported by a strong presence of biopharmaceutical companies, well-established regulatory frameworks, and significant healthcare expenditure.

The U.S. reports approximately 1.75 million new cancer cases annually, with around 600,000 cancer-related deaths. Additionally, the prevalence of hepatitis and multiple sclerosis further drives the demand for interferon-based treatments. North America’s sophisticated medical facilities and access to cutting-edge technologies enable the effective administration of interferon therapies.

Significant investments in biotechnology and pharmaceutical research lead to the development of novel interferon therapies, including biosimilars, enhancing treatment options and accessibility.

According to data from the Centers for Disease Control and Prevention (CDC), updated in April 2024, the United States reported 13,300 new cases of hepatitis B in 2022, underscoring a major public health issue that demands continued monitoring and intervention. As a result, the increasing prevalence of hepatitis B is expected to elevate the demand for treatments, with interferons playing a key role in market expansion.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the Interferons market includes Bayer AG, Merck & Co., Inc., Novartis International AG, Roche Holding AG, Sanofi S.A., Pfizer Inc., Eli Lilly and Co., Biogen Inc., Amgen Inc., AbbVie Inc., Mylan N.V., Zydus Cadila, Hikma Pharmaceuticals, Genentech, Inc., Bristol-Myers Squibb Company, Teva Pharmaceutical Industries Ltd., GlaxoSmithKline plc, and Others.

Bayer AG is a key player in the Interferon Market, offering innovative interferon therapies, particularly in oncology and chronic viral infections like hepatitis. The company focuses on developing advanced treatments to improve patient outcomes and has a strong presence in the global biopharmaceutical industry, contributing to the growth of interferon-based therapies. Merck & Co., Inc.

Is a significant contributor to the Interferon Market, leveraging its expertise in immuno-oncology and antiviral therapies. Novartis International AG plays a crucial role in the Interferon Market, developing interferon therapies for conditions such as multiple sclerosis and viral infections. The company emphasizes innovation and personalized medicine, expanding the availability and effectiveness of interferon treatments while enhancing patient care and market reach across multiple therapeutic areas.

Recent Developments

- In March 2025, ANVISA approved BESREMi® (ropeginterferon alfa-2b) for treating adult patients with Polycythemia Vera (PV), a rare blood cancer. This approval marks a significant advancement in PV treatment options in Brazil.

- In September 2023, Eiger announced the discontinuation of the Phase 3 LIMT-2 trial of peginterferon lambda for chronic hepatitis delta due to safety concerns, including liver decompensation events.

- ILC Therapeutics is advancing Alfacyte™, a hybrid interferon designed for improved therapeutic profiles across multiple indications. The company completed a £2.5 million financing round in September 2024 to support its development.

- In 2023, NIH researchers reported that interferon alfa-2b treatment significantly improved survival rates in patients with low-grade lymphomatoid granulomatosis, a rare Epstein-Barr virus-associated condition.

Top Key Players

- Bayer AG

- Merck & Co., Inc.

- Novartis International AG

- Roche Holding AG

- Sanofi S.A.

- Pfizer Inc.

- Eli Lilly and Co.

- Biogen Inc.

- Amgen Inc.

- AbbVie Inc.

- Mylan N.V.

- Zydus Cadila

- Hikma Pharmaceuticals

- Genentech, Inc.

- Bristol-Myers Squibb Company

- Teva Pharmaceutical Industries Ltd.

- GlaxoSmithKline plc

- Others

Report Scope

Report Features Description Market Value (2024) US$ 9.74 Billion Forecast Revenue (2034) US$ 14.14 Billion CAGR (2025-2034) 3.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Alpha Interferons, Beta Interferons and Gamma Interferons), By Application (Cancer Treatment, Viral Infections, Autoimmune Diseases and Others), By Route of Administration (Subcutaneous Injection, Intravenous Injection and Intramuscular Injection), By End-User (Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, Research and Academic Institutes, and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Bayer AG, Merck & Co., Inc., Novartis International AG, Roche Holding AG, Sanofi S.A., Pfizer Inc., Eli Lilly and Co., Biogen Inc., Amgen Inc., AbbVie Inc., Mylan N.V., Zydus Cadila, Hikma Pharmaceuticals, Genentech, Inc., Bristol-Myers Squibb Company, Teva Pharmaceutical Industries Ltd., GlaxoSmithKline plc, and Others. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Bayer AG

- Merck & Co., Inc.

- Novartis International AG

- Roche Holding AG

- Sanofi S.A.

- Pfizer Inc.

- Eli Lilly and Co.

- Biogen Inc.

- Amgen Inc.

- AbbVie Inc.

- Mylan N.V.

- Zydus Cadila

- Hikma Pharmaceuticals

- Genentech, Inc.

- Bristol-Myers Squibb Company

- Teva Pharmaceutical Industries Ltd.

- GlaxoSmithKline plc

- Others

Our Clients

- 152770

- July 2025