Global Insurance Rating Software Market By Software (Core Rating Engines, Rules & Logic Management, API Integration Platforms, Others), By Deployment (Cloud-based, On-premise), By End-User (Insurance Carriers, Managing General Agents (MGAs), Insurance Agencies & Brokers, Third-Party Administrators (TPAs)), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2034

- Published date: Nov. 2025

- Report ID: 168100

- Number of Pages: 294

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

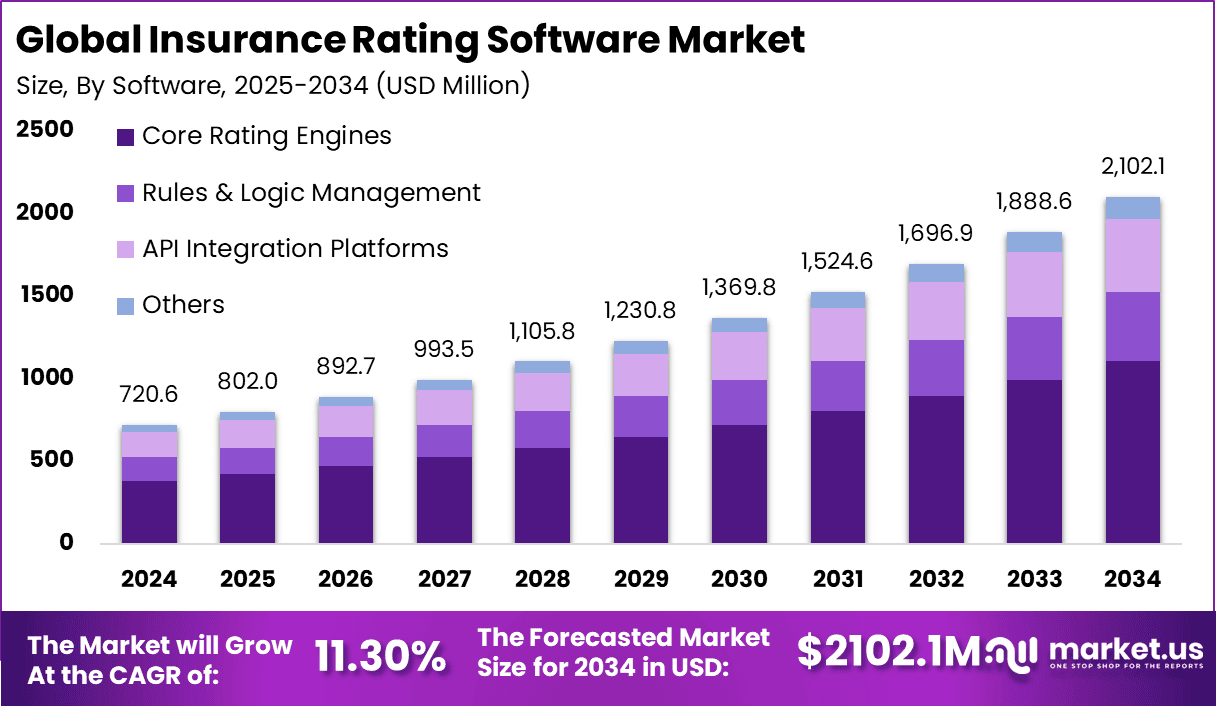

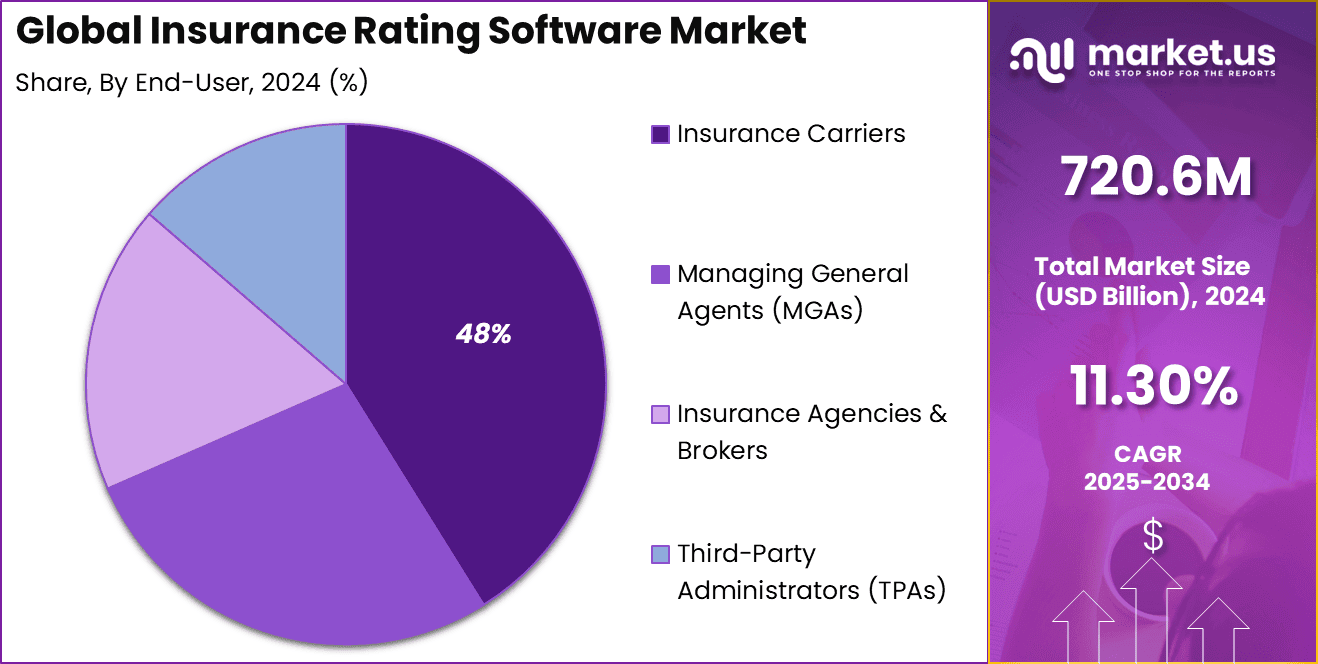

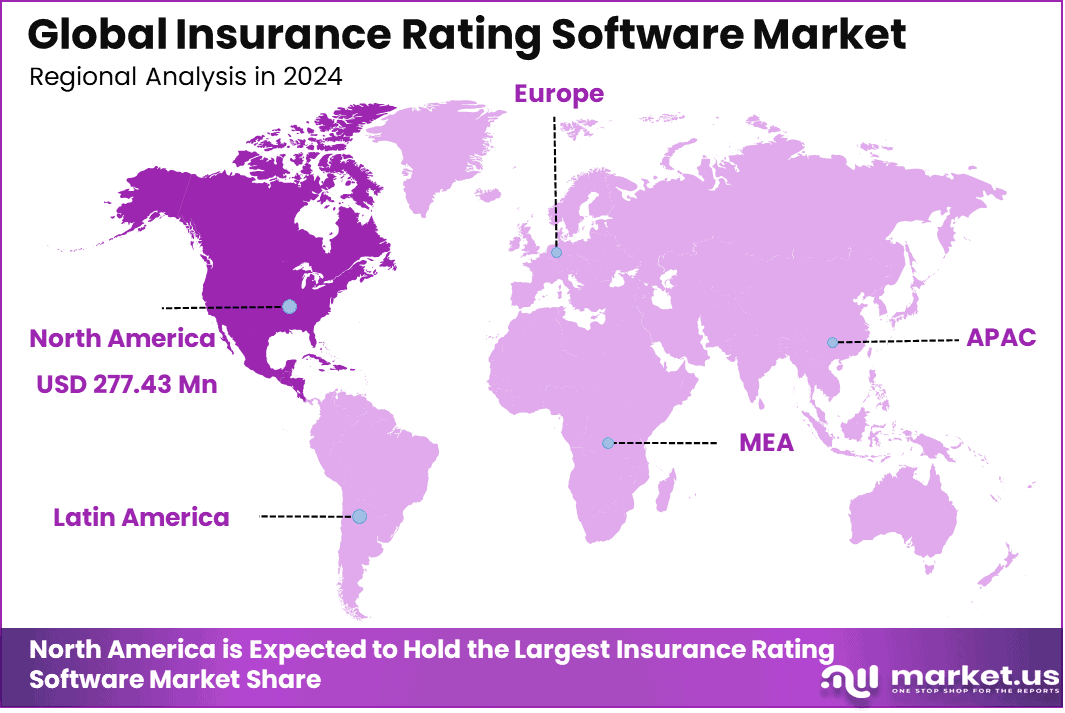

The Global Insurance Rating Software Market generated USD 720.6 million in 2024 and is predicted to register growth from USD 802.0 million in 2025 to about USD 2102.1 million by 2034, recording a CAGR of 11.30% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 38.5% share, holding USD 277.43 Million revenue.

The insurance rating software market has expanded as insurers move from manual rating methods to automated engines that calculate premiums with higher accuracy and speed. Growth reflects rising product complexity, increasing regulatory expectations and the need for consistent pricing across multiple policy types. Rating platforms now support personal, commercial and specialty insurance lines through centralised digital systems.

The growth of the market can be attributed to rising demand for real time pricing, stronger focus on underwriting discipline and the need to manage large volumes of rating data. Insurers face pressure to reduce pricing errors and respond to competitive market shifts more quickly. Digital transformation initiatives within insurance operations further accelerate adoption of automated rating systems.

Top Market Takeaways

- By software type, core rating engines lead with 52.7% share, serving as the central component for automated premium calculations, risk assessment, and policy quoting across various insurance lines.

- By deployment, cloud-based solutions dominate with 81.6% share, valued for scalability, real-time processing, reduced infrastructure costs, and seamless integration with AI-driven analytics and regulatory compliance tools.

- By end-user, insurance carriers hold 48.2% of the market, relying on rating software for efficient underwriting, personalized pricing, and competitive product launches amid rising regulatory demands and customer expectations.

- Regionally, North America commands about 38.5% market share, driven by mature insurance ecosystems, advanced digital infrastructure, and high adoption of cloud technologies.

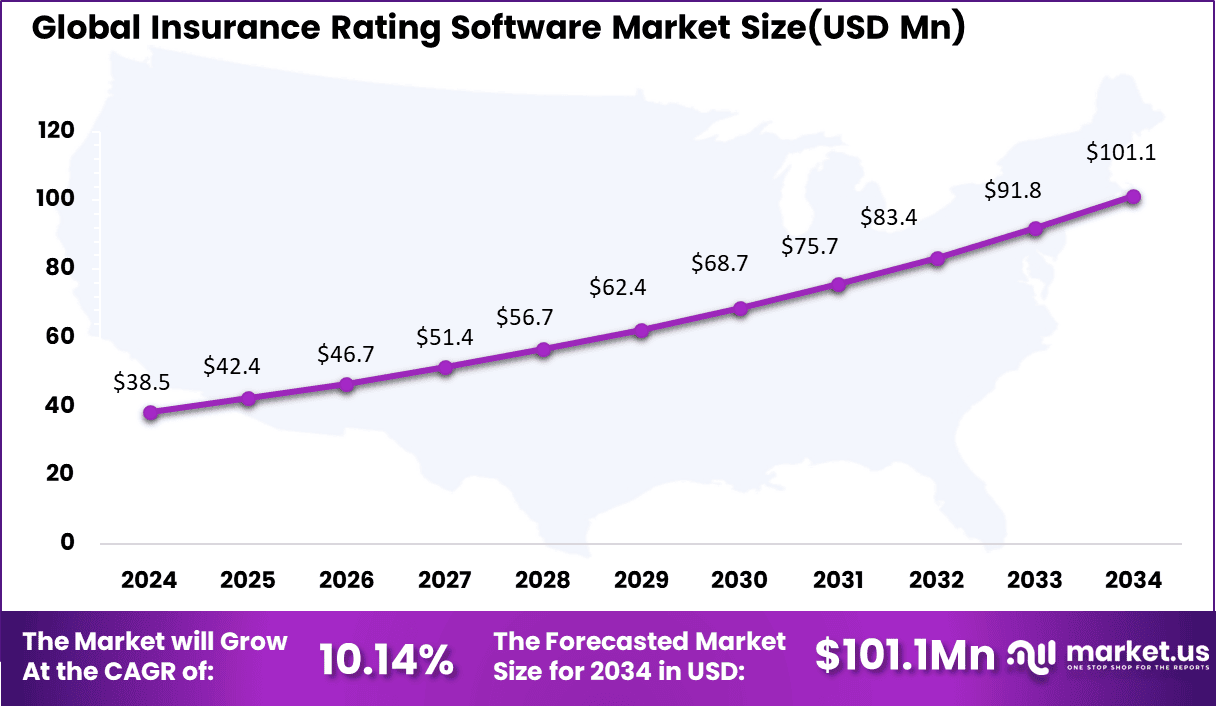

- The U.S. market size is approximately USD 249.7 million in 2025.

- The market grows at a CAGR of around 10.14%, fueled by AI integration for precise risk modeling, demand for usage-based insurance, and cloud migrations enabling faster product iterations and compliance.

By Software

Core rating engines lead the insurance rating software market with a strong 52.7% share. These engines form the heart of insurance operations by automating complex premium calculations based on risk factors, customer profiles, and regulatory rules. They handle everything from personal lines to commercial policies, ensuring accurate and consistent pricing that carriers rely on for profitability and competitiveness.

The flexibility of core engines allows quick adjustments to market changes, product launches, and compliance needs without overhauling entire systems. As insurers face pressure to deliver personalized quotes and respond to real-time data, core rating engines evolve with AI integration for better risk prediction and fraud detection. Their scalability supports growth from small agencies to large enterprises, making them indispensable for maintaining operational speed and customer trust in a fast-moving industry.

By Deployment

Cloud-based deployment dominates with an impressive 81.6% share, reflecting the shift toward flexible, scalable solutions that reduce IT overhead. Cloud platforms enable insurers to access rating software from anywhere, supporting remote teams and rapid scaling during peak seasons like renewal periods.

They offer automatic updates, robust security, and seamless integration with other insurtech tools, cutting costs while boosting agility. This deployment model suits modern insurers aiming for digital transformation without heavy upfront investments.

The appeal lies in cloud’s ability to handle massive data volumes for analytics and machine learning, driving smarter underwriting decisions. Insurers appreciate the disaster recovery features and compliance tools built into cloud environments, ensuring business continuity amid regulatory shifts and cyber threats.

By End-User

Insurance carriers represent the largest end-user group at 48%, as they depend on rating software for core underwriting and policy management. Carriers use these tools to process high volumes of quotes, assess risks across diverse portfolios, and optimize pricing strategies for profitability. The software streamlines workflows from quote generation to policy issuance, reducing manual errors and speeding up customer service.

Carriers benefit from advanced features like multi-line rating and scenario modeling, which help navigate competitive markets and regulatory demands. Their heavy adoption drives software innovation toward greater customization and integration with CRM and claims systems, enhancing overall operational efficiency.

Key Reasons for Adoption

- Automation of manual processes: Replaces time-consuming spreadsheets and hand calculations with instant, rule-based premium determinations.

- Regulatory compliance: Ensures calculations align with changing laws and standards across regions, reducing audit risks.

- Speed to market: Allows quick adjustments to rates and product offerings to match evolving customer needs and market shifts.

- Accuracy in risk assessment: Incorporates multiple data points for precise pricing that reflects true policyholder risks.

- Scalability for growth: Handles rising policy volumes without proportional staff increases, supporting business expansion.

Benefits

- Faster quoting and policy issuance: Cuts processing time dramatically, improving customer response and conversion rates.

- Error reduction: Minimizes human mistakes in calculations, leading to fairer pricing and fewer disputes.

- Cost efficiencies: Lowers operational overhead by streamlining workflows and eliminating redundant data entry.

- Better risk management: Enables data-driven insights for underwriting, helping avoid under- or over-pricing policies.

- Enhanced competitiveness: Supports personalized products and rapid innovation, helping win more business.

Usage

- Calculating premiums for property and casualty policies

- Personalizing life and health insurance quotes

- Managing commercial lines with complex risk factors

- Automating group insurance plan ratings

- Integrating with policy administration for end-to-end workflows

Emerging Trends

Key Trends Description AI and Machine Learning Integration AI-powered analytics enabling accurate risk assessment, predictive pricing, and fraud detection in real-time. Cloud-Based Deployments Shift to scalable cloud platforms for flexible, cost-effective rating software accessible across devices. Personalized Insurance Product Development Data-driven customization of policies and premiums based on individual customer profiles and behaviors. Automation of Underwriting Processes Streamlined automated workflows reducing manual intervention and accelerating quote generation. Integration with Telematics and IoT Real-time data from connected devices improving usage-based insurance rating accuracy. Growth Factors

Key Factors Description Digital Transformation in Insurance Industry-wide shift to digital platforms increasing demand for efficient rating automation. Regulatory Compliance Requirements Standards like IFRS 17 mandating transparent, detailed risk assessment and reporting capabilities. Rising Consumer Demand for Instant Quotes Customer expectation for quick, personalized pricing driving adoption of advanced rating tools. Growth in Complex Insurance Products Increasing product variety requiring sophisticated algorithms for accurate premium calculations. Expansion of Digital Insurance Platforms Proliferation of online insurers and apps necessitating robust backend rating infrastructure. Key Market Segments

By Software

- Core Rating Engines

- Rules & Logic Management

- API Integration Platforms

- Others

By Deployment

- Cloud-based

- On-premise

By End-User

- Insurance Carriers

- Managing General Agents (MGAs)

- Insurance Agencies & Brokers

- Third-Party Administrators (TPAs)

Regional Analysis

North America commanded a leading 38.5% share of the global insurance rating software market, fueled by a mature insurance industry and rapid digital transformation across property, casualty, life, and health sectors.

The region’s growth stems from stringent regulatory requirements that demand accurate risk assessment and compliance tools, alongside widespread adoption of AI-driven analytics for personalized pricing and underwriting efficiency.

Advanced IT infrastructure and cloud-based deployments enable real-time data processing, while major insurers invest heavily in automation to streamline operations and enhance customer experiences. North America’s competitive landscape, featuring established players, positions it as the innovation hub for insurance rating technologies.

The U.S. dominates within North America, with a market valuation of USD 249.7 million in 2024 and a solid CAGR of 10.14%. U.S. growth is propelled by high insurance penetration, regulatory mandates from state departments, and the proliferation of insurtech solutions integrating machine learning for dynamic rating models.

Leading providers focus on scalable platforms that support multi-line operations and seamless API integrations with legacy systems. Increasing demand for usage-based insurance and predictive risk modeling further accelerates adoption, solidifying the U.S. as the primary growth driver in the North American insurance rating software market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Growing Need for Efficient and Accurate Insurance Pricing

The insurance rating software market is driven by the rising need for efficient, accurate, and automated insurance pricing solutions. As insurance products diversify and consumer expectations for tailor-made policies increase, businesses require software that can quickly calculate premiums based on complex underwriting rules.

Automation reduces manual effort and errors, improving operational efficiency while providing fast and reliable quotes. Additionally, ongoing digital transformation in the insurance sector and regulatory compliance demands push companies to adopt advanced rating software. AI and machine learning integration further enhance risk assessment and premium accuracy, making rating software critical to both insurers and agents.

Restraint

High Implementation Costs and Integration Complexities

High initial costs and integration challenges restrain the market’s growth. Implementing advanced rating software requires significant investment in technology infrastructure, licenses, and training, posing barriers for smaller insurance firms or those with legacy systems. Integrating new software with existing policy and claims processing platforms adds complexity and may disrupt workflows.

Legacy systems lacking compatibility hinder seamless real-time data sharing and automation, prolonging deployment timelines. These factors slow adoption and require insurers to carefully plan digital transformation investments to mitigate operational risks.

Opportunity

Expansion through AI and Cloud-Based Analytics

AI-powered pricing engines and cloud-based rating software offer strong growth opportunities. AI enables predictive analytics, dynamic pricing, and fraud detection, which improve underwriting precision and customer personalization. Cloud deployment reduces IT overhead, supports scalability, and provides insurers with on-demand access and rapid upgrades.

The rise of usage-based insurance products and ongoing regulatory requirements for transparency drive adoption of flexible, AI-enhanced rating platforms. Collaboration between software vendors and insurers to develop industry-specific modules creates additional revenue streams and market expansion potential.

Challenge

Data Privacy Concerns and Regulatory Compliance

Data privacy and evolving regulatory requirements present significant challenges for the insurance rating software market. Handling massive volumes of sensitive customer data necessitates stringent security controls, with compliance to regional laws like GDPR increasing operational costs. Privacy breaches risk client trust and legal penalties.

Moreover, compliance with complex reporting and transparency standards, such as IFRS 17, demands adaptable software capable of updating frequently. Balancing innovation, compliance, and customer data protection while maintaining system performance is a critical hurdle faced by providers and insurers alike.

Competitive Analysis

Guidewire, Duck Creek Technologies, Oracle, SAP, and Salesforce lead the insurance rating software market with strong platforms that support automated rate calculation, regulatory compliance, and real-time policy pricing. Their systems help insurers modernize underwriting processes while improving speed and accuracy. These companies focus on flexible configuration, cloud deployment, and seamless integration with core policy systems.

Vertafore, Applied Systems, EIS Group, EIS Ltd, Sapiens, Majesco, and BriteCore strengthen the competitive landscape with modular rating engines and policy administration solutions. Their platforms support multi-line products, dynamic pricing models, and unified data management. These providers enable insurers to respond quickly to market changes and regulatory updates.

Insurity, OneShield, Cogitate, and other participants broaden the market with specialized cloud-native rating systems designed for speed, configurability, and ease of deployment. Their solutions offer low-code customization, automated rule updates, and strong integration with distribution channels. These companies support insurers seeking agile pricing capabilities and scalable technology frameworks.

Top Key Players in the Market

- Guidewire

- Duck Creek Technologies

- Oracle

- SAP

- Salesforce

- Vertafore

- Applied Systems

- EIS Group

- EIS Ltd

- Sapiens

- Majesco

- BriteCore

- Insurity

- OneShield

- Cogitate

- Others

Future Outlook

The Insurance Rating Software Market is poised for strong growth through 2032, fueled by digital transformation in the insurance sector, rising adoption of AI and machine learning for precise risk assessment, and demand for automated, personalized premium calculations.

Cloud-based deployments and integration with big data analytics will enhance operational efficiency and compliance with evolving regulations like IFRS 17. Emerging markets in Asia-Pacific are expected to drive faster expansion as insurers modernize to meet consumer demands for instant quotes and tailored products.

Opportunities lie in

- AI and machine learning integration for advanced risk modeling and fraud detection to improve accuracy and speed.

- Expansion of cloud-based solutions enabling scalable, real-time rating for property, casualty, and health insurance lines.

- Growth in personalized and usage-based insurance products supported by telematics and IoT data analytics.

Recent Developments

- October, 2025, Guidewire announced PricingCenter, a unified pricing and rating solution enabling insurers to rapidly adjust rates, analyze market impacts, and accelerate new product launches with AI-driven insights.

- September, 2025, Duck Creek Technologies formed a strategic partnership with Synechron to drive digital transformation, integrating AI-led solutions with Duck Creek’s SaaS platforms to enhance agility and customer experience

Report Scope

Report Features Description Market Value (2024) USD 720.6 Mn Forecast Revenue (2034) USD 2,102.1 Mn CAGR(2025-2034) 11.30% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Software (Core Rating Engines, Rules & Logic Management, API Integration Platforms, Others), By Deployment (Cloud-based, On-premise), By End-User (Insurance Carriers, Managing General Agents (MGAs), Insurance Agencies & Brokers, Third-Party Administrators (TPAs)) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Guidewire, Duck Creek Technologies, Oracle, SAP, Salesforce, Vertafore, Applied Systems, EIS Group, EIS Ltd, Sapiens, Majesco, BriteCore, Insurity, OneShield, Cogitate, and others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Insurance Rating Software MarketPublished date: Nov. 2025add_shopping_cartBuy Now get_appDownload Sample

Insurance Rating Software MarketPublished date: Nov. 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Guidewire

- Duck Creek Technologies

- Oracle

- SAP

- Salesforce

- Vertafore

- Applied Systems

- EIS Group

- EIS Ltd

- Sapiens

- Majesco

- BriteCore

- Insurity

- OneShield

- Cogitate

- Others

Our Clients

- 168100

- Nov. 2025