Global Insulated Lunch Box Market Size, Share, Growth Analysis Material (Plastic, Steel, Glass, Others), Application (School, Workplace, Others), Sales Channel (Hypermarkets/Supermarkets, Convenience Stores, Online, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178169

- Number of Pages: 249

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

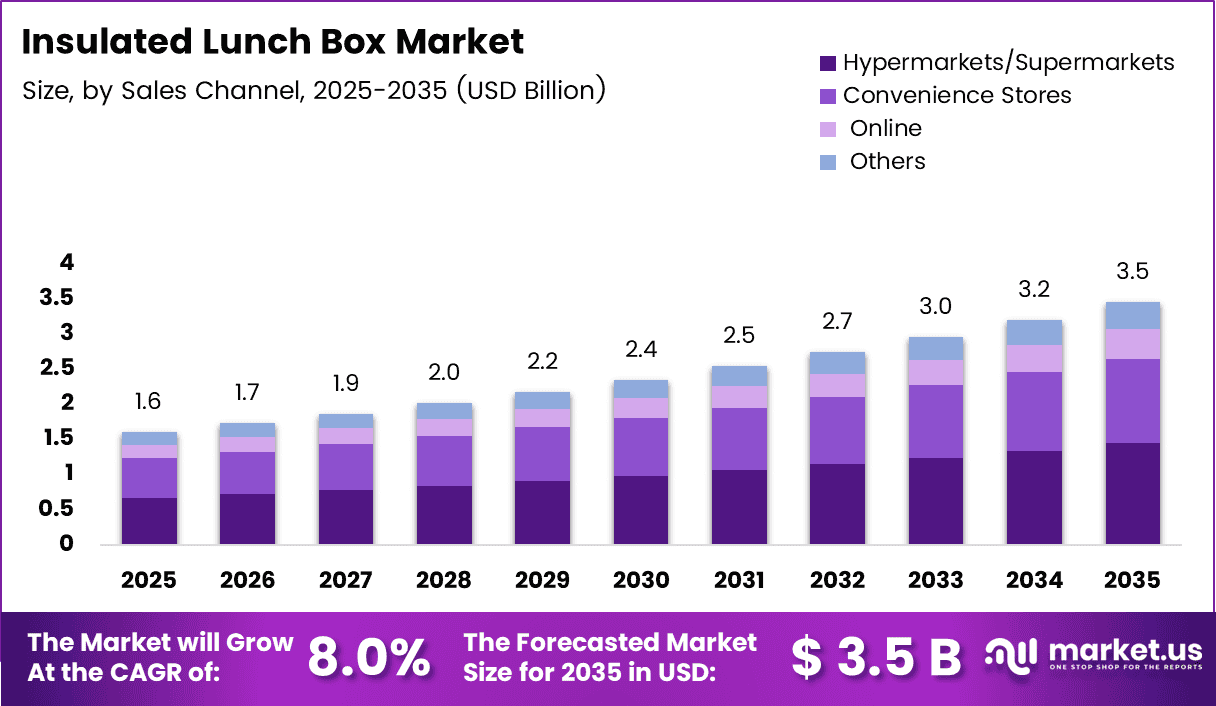

Global Insulated Lunch Box Market size is expected to be worth around USD 3.5 Billion by 2035 from USD 1.6 Billion in 2025, growing at a CAGR of 8.0% during the forecast period 2026 to 2035.

The insulated lunch box market encompasses portable food storage containers designed with thermal insulation properties. These products maintain food temperature for extended periods, enabling consumers to carry home-cooked meals safely. The market serves diverse demographics including students, working professionals, and outdoor enthusiasts seeking convenient meal transportation solutions.

Market growth stems from increasing health consciousness and preference for homemade meals over restaurant food. Additionally, rising awareness about food safety and temperature maintenance drives adoption. The shift toward sustainable eating habits further accelerates demand for reusable insulated containers across global markets.

Government regulations regarding food safety standards influence product development significantly. Manufacturers increasingly focus on BPA-free materials and antimicrobial coatings to comply with health guidelines. Moreover, workplace wellness initiatives encouraging packed lunches contribute to market expansion across corporate segments.

Technological advancements in insulation materials enhance product performance considerably. Vacuum insulation technology and advanced thermal retention capabilities extend food freshness duration. Consequently, premium product segments experience robust growth as consumers prioritize quality and functionality over price considerations.

E-commerce platforms revolutionize distribution channels by offering extensive product variety and convenience. Direct-to-consumer sales models enable brands to establish stronger customer relationships. Therefore, online retail channels witness accelerated growth compared to traditional brick-and-mortar establishments.

According to USDA guidelines, perishable foods maintain safety for only 2 hours at room temperature. Proper insulation technology addresses this critical concern by maintaining temperatures at 165°F or appropriate cold storage levels. This regulatory framework underscores the essential role of quality insulated lunch boxes in food safety.

According to Vaya Life product specifications, advanced insulated lunch boxes utilizing VacuTherm Technology maintain meal temperatures for 5-6 hours. Such innovations demonstrate industry commitment to extending food freshness duration. Furthermore, manufacturers incorporate 304 food-grade stainless steel construction ensuring non-reactive, odor-resistant surfaces that meet stringent quality standards.

Key Takeaways

- Global Insulated Lunch Box Market projected to reach USD 3.5 Billion by 2035 from USD 1.6 Billion in 2025

- Market expected to grow at CAGR of 8.0% during forecast period 2026-2035

- Plastic material segment dominates with 49.1% market share in 2025

- School application segment leads with 47.4% market share

- Hypermarkets/Supermarkets sales channel holds 41.7% market share

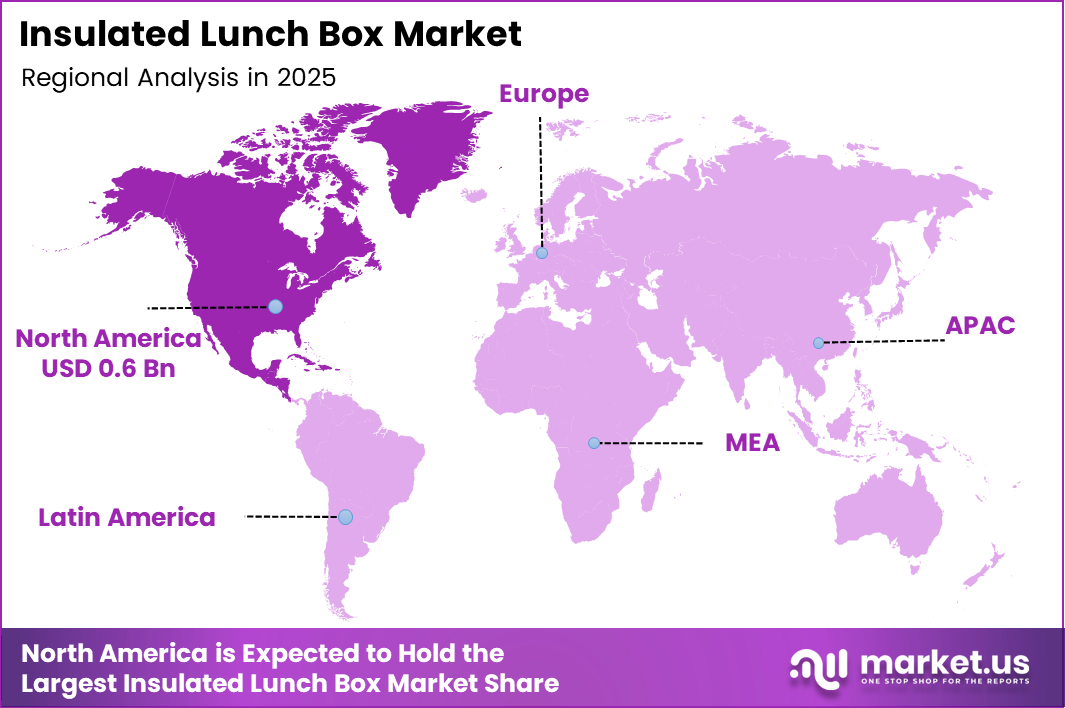

- North America dominates regional market with 42.70% share, valued at USD 0.6 Billion

- Rising health awareness and home-cooked meal culture drive market growth

- E-commerce channels and sustainable materials present significant growth opportunities

Material Analysis

Plastic dominates with 49.1% due to lightweight properties, cost-effectiveness, and versatile design options.

In 2025, ‘Plastic’ held a dominant market position in the ‘Material’ segment of Insulated Lunch Box Market, with a 49.1% share. Plastic materials offer exceptional affordability and manufacturing flexibility, enabling mass production at competitive price points. Moreover, advanced polymer technologies deliver improved insulation performance while maintaining lightweight characteristics preferred by consumers.

Steel materials gain prominence among premium segment consumers prioritizing durability and hygiene. Stainless steel construction provides superior temperature retention and resistance to odors or stains. Additionally, steel lunch boxes appeal to environmentally conscious buyers seeking long-lasting alternatives to disposable containers.

Glass materials attract health-focused consumers concerned about chemical leaching from plastics. Glass containers offer non-reactive surfaces preserving food taste and nutritional quality. However, increased weight and fragility limit widespread adoption compared to plastic and steel alternatives.

Others category encompasses innovative materials including bamboo fiber composites and bio-based polymers. These sustainable alternatives address environmental concerns while delivering adequate insulation properties. Consequently, eco-friendly material innovations represent emerging opportunities within the market landscape.

Application Analysis

School dominates with 47.4% due to widespread adoption among parents prioritizing nutritious meals for children.

In 2025, ‘School’ held a dominant market position in the ‘Application’ segment of Insulated Lunch Box Market, with a 47.4% share. Educational institutions increasingly discourage cafeteria meals, prompting parents to pack homemade lunches. Furthermore, child nutrition awareness campaigns reinforce demand for quality lunch boxes maintaining food freshness throughout school hours.

Workplace applications witness substantial growth as corporate professionals embrace healthy eating habits. Remote work arrangements and flexible schedules encourage employees to carry home-prepared meals. Additionally, workplace wellness programs promoting nutritious eating behaviors drive adoption among office-going populations globally.

Others application segment includes outdoor recreation, travel, and fitness activities requiring portable meal solutions. Hikers, gym enthusiasts, and frequent travelers utilize insulated lunch boxes for convenient food transportation. Therefore, lifestyle diversification expands market opportunities beyond traditional school and workplace demographics.

Sales Channel Analysis

Hypermarkets/Supermarkets dominate with 41.7% due to extensive product variety and immediate purchase convenience.

In 2025, ‘Hypermarkets/Supermarkets’ held a dominant market position in the ‘Sales Channel’ segment of Insulated Lunch Box Market, with a 41.7% share. Large-format retail stores provide consumers with hands-on product evaluation opportunities before purchase. Moreover, competitive pricing strategies and promotional offers attract budget-conscious shoppers seeking value-for-money options.

Convenience Stores channels serve urban consumers requiring quick purchase solutions near residential or workplace locations. Compact store formats stock popular lunch box designs catering to immediate replacement needs. Additionally, extended operating hours accommodate diverse shopping schedules of busy professionals and parents.

Online sales channels experience rapid expansion driven by e-commerce platform growth and digital consumer behavior shifts. Virtual marketplaces offer comprehensive product comparisons, customer reviews, and doorstep delivery convenience. Consequently, online channels capture increasing market share particularly among younger, tech-savvy demographics.

Others category encompasses specialty stores, brand outlets, and direct sales channels targeting niche consumer segments. These alternative distribution methods enable personalized customer experiences and premium product positioning. Therefore, diversified channel strategies strengthen brand presence across multiple consumer touchpoints.

Key Market Segments

Material

- Plastic

- Steel

- Glass

- Others

Application

- School

- Workplace

- Others

Sales Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Online

- Others

Drivers

Rising Adoption of Home-Cooked Meal Culture Drives Market Growth

Working professionals increasingly prioritize homemade meals over restaurant food due to health and cost considerations. This behavioral shift reflects growing awareness about nutritional quality and ingredient transparency. Consequently, demand for reliable insulated lunch boxes enabling safe meal transportation witnesses substantial acceleration across urban demographics.

Corporate wellness initiatives and flexible work arrangements further reinforce home-cooked meal preferences. Employees seek convenient solutions maintaining food temperature and freshness throughout workdays. Moreover, rising concerns about food additives and preservatives in commercial meals strengthen consumer inclination toward packed lunches requiring quality insulated containers.

School-going children represent another significant consumer segment driving market expansion. Parents emphasize nutritious homemade meals ensuring proper child development and health. Additionally, expanding middle-class populations in developing economies adopt packed lunch practices, thereby broadening market reach and creating sustained growth momentum.

Restraints

Availability of Low-Cost Non-Insulated Alternatives Limits Market Penetration

Budget-conscious consumers frequently opt for inexpensive non-insulated food containers despite inferior temperature retention capabilities. Price sensitivity particularly affects emerging markets where disposable income levels constrain premium product adoption. Consequently, competitive pressure from low-cost alternatives restricts market growth potential across price-sensitive consumer segments.

Durability concerns regarding insulation performance degradation over extended usage periods discourage repeat purchases. Consumers report reduced thermal efficiency after prolonged use, diminishing product value proposition. Moreover, limited awareness about proper maintenance practices accelerates insulation deterioration, thereby shortening product lifecycle expectations.

Manufacturing costs associated with advanced insulation technologies and premium materials elevate retail prices significantly. This pricing gap between standard and insulated containers limits mass market accessibility. Therefore, balancing affordability with performance quality remains critical challenge for manufacturers seeking broader market penetration across diverse economic demographics.

Growth Factors

Innovation in Sustainable Materials Accelerates Market Expansion

Environmental consciousness drives manufacturers toward eco-friendly insulation materials reducing plastic waste and carbon footprints. Biodegradable composites and recycled materials gain consumer preference aligning with sustainability values. Additionally, regulatory pressures regarding single-use plastics encourage development of reusable, environmentally responsible lunch box solutions.

Fitness enthusiasts and outdoor recreation participants represent rapidly expanding consumer segments requiring specialized insulated containers. Meal prep culture among gym-goers necessitates portion-controlled, temperature-maintaining food storage solutions. Furthermore, adventure tourism and hiking activities create demand for durable, portable insulated lunch boxes suitable for extended outdoor use.

E-commerce platforms and direct-to-consumer business models transform distribution dynamics enabling personalized customer engagement. Online channels facilitate product customization options including monogramming and color selections. Moreover, subscription-based lunch box services offering regular product upgrades establish recurring revenue streams while enhancing customer loyalty and retention rates.

Emerging Trends

Smart Technology Integration Reshapes Product Functionality

Lightweight aluminum alloys and advanced polymer composites enable compact designs without compromising insulation performance. Manufacturers prioritize portability catering to mobile lifestyles and space-constrained storage environments. Consequently, slim-profile lunch boxes fitting standard bags and backpacks gain significant market traction among commuters and students.

Leak-proof sealing mechanisms and multi-compartment configurations address consumer demands for versatile meal organization. Separate compartments prevent food mixing while accommodating diverse dish varieties in single containers. Additionally, modular designs allow customizable capacity adjustments based on portion requirements and dietary preferences.

Antimicrobial surface treatments and BPA-free material certifications respond to heightened health and safety awareness. Consumers increasingly scrutinize product compositions seeking chemical-free, hygienic food contact surfaces. Moreover, premium aesthetic designs featuring minimalist styling and sophisticated color palettes transform lunch boxes into fashion accessories reflecting personal style preferences.

Regional Analysis

North America Dominates the Insulated Lunch Box Market with a Market Share of 42.70%, Valued at USD 0.6 Billion

North America leads global market share at 42.70%, valued at USD 0.6 Billion, driven by established packed lunch culture and high disposable incomes. The region benefits from widespread adoption across schools and corporate workplaces. Additionally, strong emphasis on food safety regulations and premium product preferences sustains robust market performance throughout the forecast period.

Europe Insulated Lunch Box Market Trends

Europe demonstrates steady growth supported by increasing environmental consciousness and sustainable consumption patterns. European consumers prioritize eco-friendly materials and durable product designs aligning with circular economy principles. Moreover, stringent food safety regulations drive demand for certified, high-quality insulated containers across the region.

Asia Pacific Insulated Lunch Box Market Trends

Asia Pacific exhibits fastest growth potential fueled by expanding middle-class populations and urbanization trends. Rising health awareness and westernization of eating habits promote packed lunch adoption. Furthermore, growing student populations and increasing female workforce participation create substantial demand across diverse consumer segments.

Latin America Insulated Lunch Box Market Trends

Latin America presents emerging opportunities as economic development improves consumer purchasing power. Urban populations increasingly adopt convenient meal transportation solutions matching busy lifestyles. Additionally, growing awareness about nutrition and food safety gradually transforms traditional eating habits toward packed meal preferences.

Middle East & Africa Insulated Lunch Box Market Trends

Middle East and Africa represent nascent markets with significant long-term growth potential. Expatriate populations and international school systems drive initial adoption patterns. Moreover, rising urbanization and lifestyle modernization create favorable conditions for market expansion despite current infrastructure and distribution challenges.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

TIGER CORPORATION maintains strong market presence through innovative vacuum insulation technology and premium product positioning. The Japanese manufacturer leverages decades of thermal container expertise delivering superior temperature retention performance. Their focus on compact, high-capacity designs particularly resonates with student demographics, establishing significant competitive advantages in educational market segments across Asia Pacific and North America regions.

Zojirushi America Corporation differentiates through advanced thermal retention capabilities and ergonomic design innovations. The company emphasizes food safety features including antimicrobial coatings and leak-resistant sealing mechanisms. Strategic collaborations with electronics manufacturers enable technological integration enhancing product functionality. Moreover, their premium brand positioning attracts quality-conscious consumers willing to invest in long-lasting, high-performance insulated containers.

Bentology targets family-oriented consumers through customizable, colorful lunch box designs featuring modular compartment configurations. The brand emphasizes child-friendly aesthetics combined with practical functionality appealing to parents prioritizing both nutrition and convenience. Their direct-to-consumer e-commerce strategy enables personalized customer engagement and subscription-based revenue models. Additionally, social media marketing effectively reaches millennial parents seeking innovative meal preparation solutions.

Vaya Life pioneered patented VacuTherm technology delivering exceptional 5-6 hour temperature maintenance using 304 food-grade stainless steel construction. The company emphasizes sustainability through reusable, chemical-free materials addressing environmental concerns. Their slim, bag-friendly designs cater to urban professionals and commuters requiring portable meal solutions. Furthermore, comprehensive warranty programs and fast shipping services enhance customer satisfaction and brand loyalty across competitive markets.

Key Players

- TIGER CORPORATION

- Zojirushi America Corporation

- Bentology

- Vaya Life

- My Borosil

- Hamilton Housewares Pvt. Ltd.

- Signoraware

- Tupperware

- Thermos LLC

- LunchBots

Recent Developments

- April 2023 – Zojirushi introduced a smart lunch box with temperature monitoring capabilities, integrating IoT technology to help consumers track and maintain optimal food temperatures. This innovation represents a significant advancement in combining traditional thermal insulation with digital monitoring features for enhanced food safety and convenience.

- October 2024 – Borosil announced plans to invest USD 29.45 Million in augmenting its production capacity to meet growing consumer demand. This significant capital investment reflects the company’s strategic expansion initiative to capture increasing market opportunities in the insulated lunch box segment across Asia Pacific region.

Report Scope

Report Features Description Market Value (2025) USD 1.6 Billion Forecast Revenue (2035) USD 3.5 Billion CAGR (2026-2035) 8.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Material (Plastic, Steel, Glass, Others), Application (School, Workplace, Others), Sales Channel (Hypermarkets/Supermarkets, Convenience Stores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape TIGER CORPORATION, Zojirushi America Corporation, Bentology, Vaya Life, My Borosil, Hamilton Housewares Pvt. Ltd., Signoraware, Tupperware, Thermos LLC, LunchBots Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- TIGER CORPORATION

- Zojirushi America Corporation

- Bentology

- Vaya Life

- My Borosil

- Hamilton Housewares Pvt. Ltd.

- Signoraware

- Tupperware

- Thermos LLC

- LunchBots

Our Clients

- 178169

- Feb 2026