Quick Navigation

Report Overview

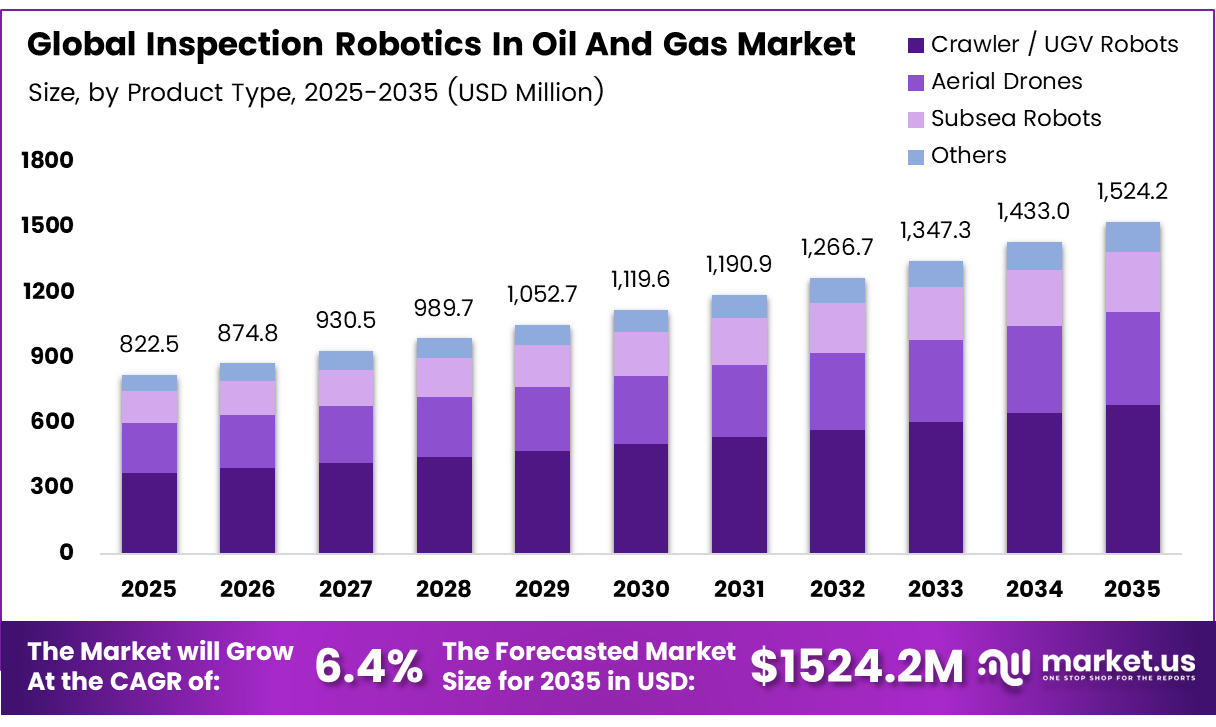

The Global Inspection Robotics in Oil and Gas Market size is expected to be worth around USD 1,524.2 million by 2035 from USD 822.5 million in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

Inspection robotics in oil and gas refers to automated systems — crawlers, oil and gas aerial drones, and subsea robots — deployed to inspect pipelines, offshore platforms, storage tanks, and refineries. These systems replace manual inspection in hazardous, remote, or confined environments. The shift toward robotic inspection reflects a structural change in how operators manage asset integrity.

Pipeline and platform operators face a direct tradeoff: send workers into dangerous environments for routine checks, or deploy robots that work continuously without safety risk. Robotic systems resolve this by delivering inspection data in real time from locations where human access is costly, slow, or dangerous. This operational logic drives consistent adoption across upstream and midstream segments.

Shell’s ExR-2.5 inspection robot completed 80% of missions without intervention and recorded 1,997 inspection points over six months on an unmanned offshore platform. This data point matters because it proves that autonomous robots can sustain operational continuity at offshore assets without permanent human presence — a threshold the industry needed to be cleared before broader adoption.

ADNOC’s HSE Cockpit.ai platform reduced safety incidents by 30% while deploying robots and drones for high-risk inspection and emissions monitoring. This outcome demonstrates that robotics delivers measurable safety returns, not just efficiency gains — a distinction that matters to boards managing ESG commitments and regulatory exposure.

Key Takeaways

- The Global Inspection Robotics in Oil and Gas Market is valued at USD 822.5 million in 2025 and forecast to reach USD 1,524.2 million by 2035 at a CAGR of 6.4% during the forecast period 2026 to 2035.

- Crawler / UGV Robots lead with a 34.7% share in 2025.

- Remotely operated systems dominate with a 54.3% share.

- OEM accounts for the largest share at 67.2%.

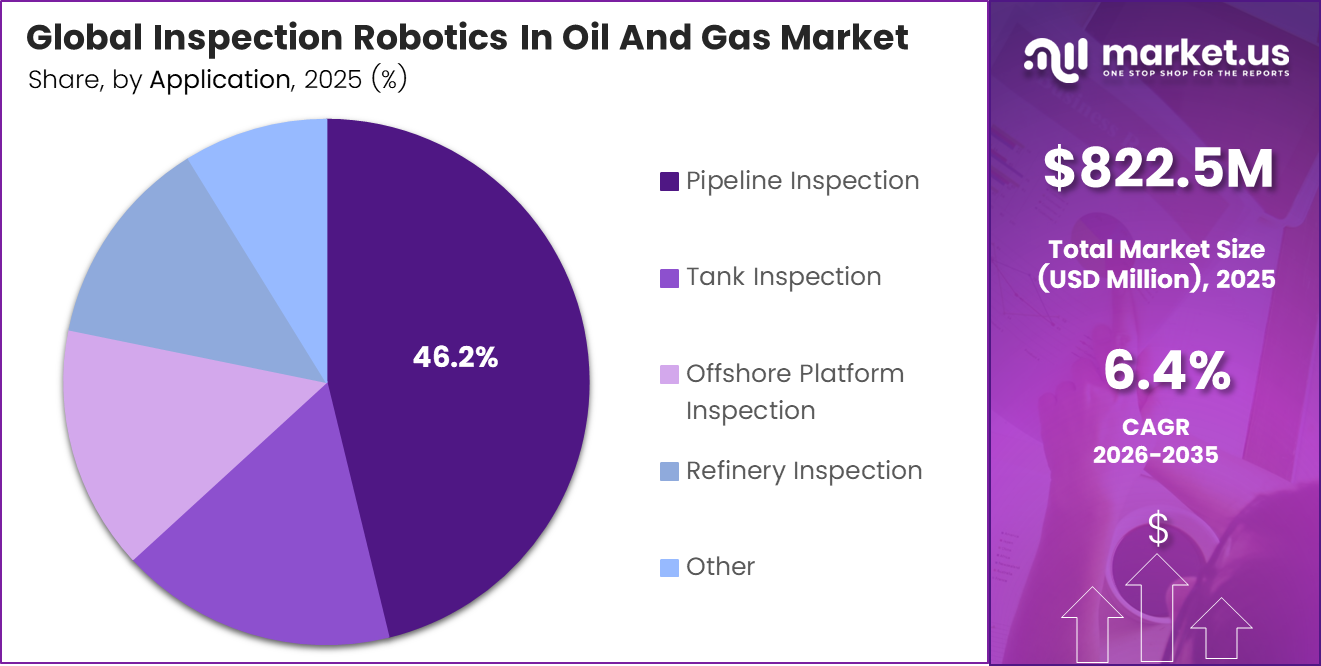

- Pipeline Inspection holds the dominant position with a 46.2% share.

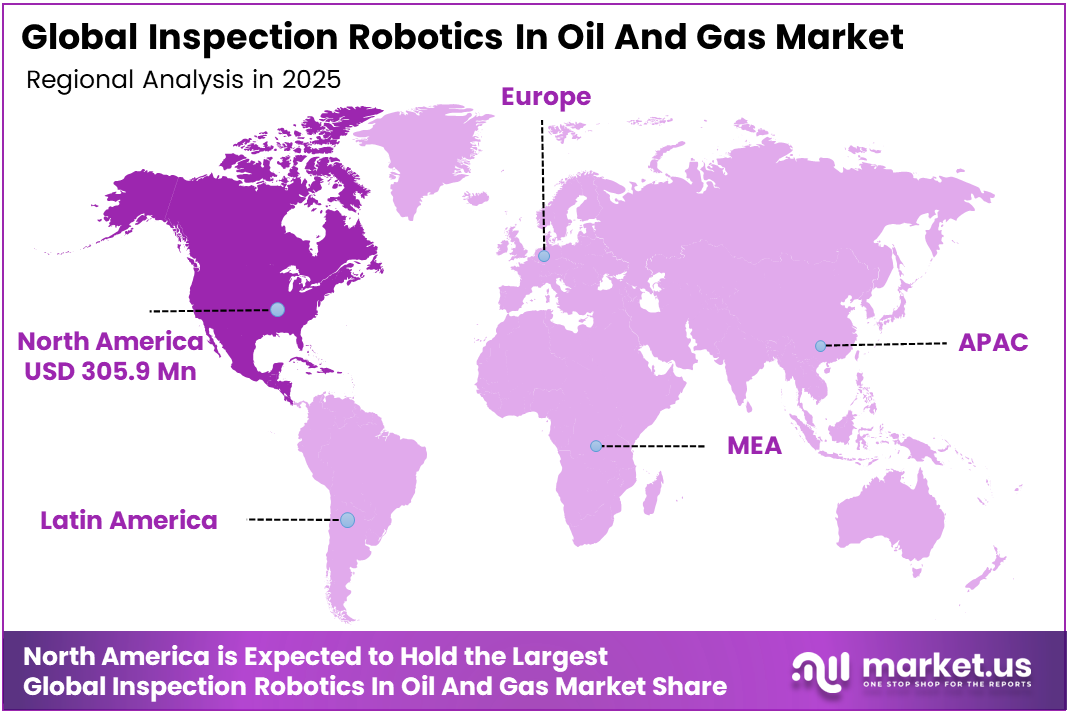

- North America leads regional markets with a 37.2% share, valued at USD 305.9 million in 2025.

Product Type Analysis

Crawler / UGV Robots dominate with 34.7% due to unmatched surface access in confined industrial environments.

In 2025, Crawler / UGV Robots held a dominant market position in the By Product Type segment of the Inspection Robotics in Oil and Gas Market, with a 34.7% share. Ground-based crawlers navigate confined spaces, pipe interiors, and complex deck structures where aerial systems cannot operate. Their ability to carry multiple sensor payloads — including ultrasonic, thermal, and gas detection tools — makes them the most versatile platform for close-contact asset inspection.

Aerial Drones (UAVs) serve as the fastest deployment option for above-ground and elevated infrastructure inspection. Drones cover flare stacks, storage tank rooftops, and offshore platform exteriors in minutes, replacing rope-access teams and scaffold setups. Their low mobilization cost and rapid data capture make them the preferred tool for routine visual inspection cycles, particularly where physical access is restricted.

Operation Type Analysis

Remote-operated systems dominate with 54.3% due to operator preference for supervised control in high-risk assets.

In 2025, Remote Operated Systems held a dominant market position in the By Operation Type segment of the Inspection Robotics in Oil and Gas Market, with a 54.3% share. Operators in oil and gas manage assets where a single inspection error can trigger multi-million dollar consequences. Remote-operated systems keep a trained human in the decision loop while eliminating physical exposure — the operational model that procurement teams trust most at this stage of technology maturity.

Autonomous inspection systems execute inspection missions without real-time human control, using pre-programmed routes and onboard AI for anomaly detection. Shell’s six-month offshore deployment — supervised from over 1,000 km away — demonstrates that autonomous robots can operate reliably on unmanned platforms. As reliability evidence accumulates and AI defect-detection accuracy improves, autonomous systems will progressively take a share from remote-operated configurations in routine inspection workflows.

Sales Channel Analysis

OEM dominates with 67.2% due to integrated system delivery with validated performance guarantees.

In 2025, OEM held a dominant market position in the By Sales Channel segment of the Inspection Robotics in Oil and Gas Market, with a 67.2% share. Oil and gas operators purchasing robotic inspection systems through OEM channels receive factory-integrated hardware, software, and support agreements in a single procurement. This reduces integration risk and assigns clear accountability for system performance — priorities that dominate large capital purchasing decisions in the energy sector.

Aftermarket channels supply replacement components, sensor upgrades, and software updates for existing robotic inspection fleets. As the installed base of inspection robots grows, aftermarket revenue will expand proportionally. Operators extending robot lifecycles through component replacement rather than full fleet replacement represent a structurally recurring revenue stream for specialist suppliers positioned in this channel.

Application Analysis

Pipeline Inspection dominates with 46.2% due to the scale and failure-consequence severity of global pipeline networks.

In 2025, Pipeline Inspection held a dominant market position in the By Application segment of the Inspection Robotics in Oil and Gas Market, with a 46.2% share. Pipelines form the arterial infrastructure of oil and gas operations — any undetected corrosion, crack, or joint failure carries immediate environmental and financial consequences. Robotic inspection systems that deliver continuous integrity data eliminate the inspection gaps that manual pig-and-probe methods leave between scheduled cycles.

Tank Inspection addresses the structural integrity of storage vessels that hold crude oil, refined products, and chemical feedstocks under continuous pressure and temperature cycling. Robotic crawlers and drones reduce tank inspection turnaround time from days to hours, cutting the revenue loss associated with taking storage capacity offline. This efficiency advantage is particularly material for refineries operating high-utilization tank farms.

Key Market Segments

By Product Type

- Crawler / UGV Robots

- Aerial Drones (UAVs)

- Subsea Robots (ROVs / AUVs)

- Others

By Operation Type

- Remote Operated

- Autonomous

By Sales Channel

- OEM

- Aftermarket

By Application

- Pipeline Inspection

- Tank Inspection

- Offshore Platform Inspection

- Refinery Inspection

- Other

Emerging Trends

Drone-Based Inspection and Edge-Enabled Robotics Reshape Real-Time Decision-Making Across Oil and Gas Assets

Aerial drones now handle flare stack, storage tank, and elevated structure assessments that previously required scaffold teams and extended shutdowns. Operators using UAVs cut inspection mobilization time sharply while generating continuous visual records. Gasfinder robot detects methane leaks as small as 2 g/second from 20 meters — a sensitivity level that fundamentally changes how operators manage emissions compliance at scale.

Edge computing integration in robotic inspection platforms allows data processing at the point of collection rather than after transmission to central servers. This eliminates latency between detection and decision — a critical advantage when identifying active leaks or structural anomalies during live plant operations. Industrial IoT connectivity further allows inspection robots to feed real-time data into plant management systems without manual data transfer steps.

Magnetic wheel and snake robots now access internal pipeline surfaces for corrosion mapping and crack detection without pipeline shutdown. Collaborative human-robot workflows, where operators supervise robotic rounds remotely and intervene only on flagged anomalies, are restructuring inspection labor models in refineries and offshore rigs. These trends compound: each technology layer reduces inspection cost per data point while improving detection accuracy.

Drivers

Autonomous Robot Deployment and Predictive Maintenance Investment Drive Structural Adoption Across Offshore and Refinery Operations

Offshore pipeline and platform operators deploy autonomous crawling and flying robots to maintain continuous integrity monitoring at assets where rotating inspection crews are cost-prohibitive. ExRobotics recorded over 1,000 successful deployments of Ex-certified autonomous inspection robots by 2025 — a volume that confirms commercial-scale adoption, not pilot-stage experimentation. Each deployment reduces the manual inspection hours required per asset per year.

Predictive maintenance investment directly converts into robotic inspection demand. When operators commit to condition-based maintenance programs, they require continuous sensor data from assets between scheduled shutdowns. Robots provide that data stream without requiring physical access for each reading. Consequently, every dollar invested in predictive maintenance infrastructure creates downstream demand for the robotic platforms that collect the underlying data.

Worker safety enhancement in hazardous refinery environments provides a non-negotiable driver that regulatory pressure reinforces. Remote inspection robotics eliminates personnel exposure to toxic gases, high-pressure systems, and elevated structures during routine inspection rounds. As regulators in North America and Europe tighten confined-space and HAZOPs requirements, operators face a compliance-driven incentive to replace manual inspection with robotic alternatives regardless of cost.

Restraints

High Capital Costs and Specialist Skill Shortages Limit Deployment Speed in Remote and Emerging Market Operations

Advanced robotic inspection infrastructure requires substantial upfront capital for hardware, integration with existing SCADA and asset management systems, and site-specific customization. For midstream operators and national oil companies managing constrained capital budgets, this deployment cost creates a genuine adoption barrier. The integration complexity — connecting robotic systems to legacy plant infrastructure — adds project timelines and engineering costs that delay return on investment.

Remote oil and gas production regions face a compounding restraint: the shortage of skilled operators and robotics maintenance specialists in locations far from technology centers. A robot that requires specialist intervention for recalibration or repair creates operational dependency on personnel who may be days of travel away. This risk is particularly acute for deepwater and Arctic operations, where logistics costs for technical support are structurally high.

Together, these constraints mean that the total cost of ownership for robotic inspection systems remains underestimated at the procurement stage. Operators who calculate hardware cost alone undercount integration, training, and maintenance expenses. Until Robotics-as-a-Service models mature sufficiently to absorb these costs within a subscription structure, capital intensity will continue to slow adoption among smaller and mid-tier operators.

Growth Factors

AI-Enabled Detection, RaaS Models, and Digital Twin Integration Open New Revenue Pathways for Inspection Robotics Providers

AI-enabled inspection robots that automate defect detection and asset performance analytics convert raw sensor data into prioritized maintenance actions without human review of every data point. This capability shift changes the value proposition from data collection to decision support — a higher-value position that justifies premium pricing and longer service contracts. ExRobotics secured up to €7 million in growth capital in 2025 specifically to expand its Robot-as-a-Service inspection fleet, signaling investor confidence in this model’s commercial viability.

Robotics-as-a-Service models restructure the financial barrier to adoption by replacing capital expenditure with operating expenditure. Midstream and upstream operators who cannot justify large upfront purchases can access robotic inspection capabilities through subscription arrangements, paying per inspection cycle or per asset monitored. This model expands the addressable market by bringing inspection robotics within reach of operators who were previously priced out of full system ownership.

Hydrogen terminals, LNG facilities, and carbon capture infrastructure represent entirely new inspection environments where conventional methods have limited precedent. Specialized robotic platforms designed for these settings face no entrenched competition from established inspection workflows. Additionally, digital twin integration — connecting physical robot inspection data to virtual asset models — creates continuous remote visualization that allows operators to track structural changes between inspection cycles without deploying additional field teams.

Regional Analysis

North America Dominates the Inspection Robotics in Oil and Gas Market with a Market Share of 37.2%, Valued at USD 305.9 Million

North America holds a 37.2% share valued at USD 305.9 million in 2025, underpinned by the density of pipeline infrastructure across the US and Canada and by mature regulatory frameworks that mandate regular integrity inspections. The US pipeline network spans hundreds of thousands of miles, creating a structurally large and recurring inspection workload that robotic systems address more cost-effectively than manual crews at scale.

Europe’s adoption of inspection robotics is shaped by North Sea offshore operations, aging onshore refinery infrastructure, and increasingly stringent emissions monitoring requirements under EU environmental directives. Operators in the UK, Norway, and the Netherlands face regulatory pressure to reduce fugitive emissions — creating direct demand for gas-detection robotic platforms that deliver continuous monitoring across complex process facilities.

Asia Pacific drives inspection robotics adoption through expanding LNG infrastructure in Australia, deepwater offshore developments in Southeast Asia, and refinery capacity additions across China and India. National oil companies in this region are investing in technology modernization to extend asset life and reduce operational costs — priorities that align directly with robotic inspection’s core value proposition.

Latin America’s inspection robotics market centers on Brazil’s offshore pre-salt deepwater fields and Mexico’s onshore and shallow-water production assets. Petrobras and Pemex face aging infrastructure challenges that require cost-effective inspection solutions across large, geographically distributed asset portfolios. Subsea robotic systems are particularly relevant to Brazil’s deepwater operating environment, where ROV and AUV deployments support platform and pipeline integrity at depths beyond conventional methods.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Analysis

Baker Hughes positions itself at the intersection of oilfield services and industrial technology, deploying inspection robotics as part of its broader asset integrity and digital solutions portfolio. Its scale across upstream and midstream operations gives it direct access to the largest inspection contracts globally. This integration advantage allows Baker Hughes to bundle robotic inspection into long-term service agreements rather than competing on hardware cost alone.

Anybotics builds legged autonomous robots designed for industrial inspection in complex, unstructured environments where wheeled crawlers cannot navigate. Its ANYmal platform addresses inspection scenarios in refineries, offshore platforms, and chemical plants that require adaptable mobility across stairs, obstacles, and varying surface conditions. This hardware differentiation targets the inspection environments where conventional robotic systems have historically failed to perform reliably.

Petrobot specializes in robotic inspection platforms designed specifically for the oil and gas sector’s confined-space and hazardous-area requirements. Its focus on Ex-rated environments — where explosion-proof certification is mandatory — positions it in the highest-barrier segment of inspection robotics procurement. Operators in refineries and processing plants cannot substitute non-rated equipment, giving certified specialist providers a structurally protected market position.

SLB integrates inspection robotics within its digital and automation product lines, leveraging its global field services infrastructure to deploy and support robotic systems at remote and offshore locations. Its strength lies not only in the technology but in the logistics and support network that makes robotic inspection operationally viable at scale. For operators in remote geographies, SLB’s service coverage addresses the specialist skill shortage restraint that limits adoption by smaller providers.

Key Players

- Baker Hughes

- Anybotics

- Petrobot

- SLB

- Energy Robotics

- SMP Robotics

- Eddyfi Technologies

- Autel Robotics

- Boston Dynamics

- Oceaneering International

- TechnipFMC

- Schlumberger

- GE Inspection Robotics

- Inuktun Services Ltd.

- Honeybee Robotics

- Cyberhawk Innovations

- Flyability

- ExRobotics

- Petrofac

- Diakont

Recent Developments

- In 2026, Baker Hughes agreed to sell its Waygate Technologies inspection/NDT business to Hexagon for about $1.45 billion, shifting ownership of Baker Hughes’ industrial inspection portfolio. Baker Hughes’ Waygate Technologies introduced the Krautkrämer WheelStar RPS robotic inspection solution.

- In 2025, ANYbotics launched a robotic gas leak detection solution for ANYmal, combining autonomous navigation, modular gas detectors, and 360° acoustic imaging for leak localization and real-time alerts. Yokogawa and ANYbotics announced the integration of Yokogawa’s OpreX Robot Management Core Software with ANYmal robotic inspection solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 822.5 Million |

| Forecast Revenue (2035) | USD 1,524.2 Million |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Crawler / UGV Robots, Aerial Drones (UAVs), Subsea Robots (ROVs / AUVs), Others), By Operation Type (Remote Operated, Autonomous), By Sales Channel (OEM, Aftermarket), By Application (Pipeline Inspection, Tank Inspection, Offshore Platform Inspection, Refinery Inspection, Other) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Baker Hughes, Anybotics, Petrobot, SLB, Energy Robotics, SMP Robotics, Eddyfi Technologies, Autel Robotics, Boston Dynamics, Oceaneering International, TechnipFMC, Schlumberger, GE Inspection Robotics, Inuktun Services Ltd., Honeybee Robotics, Cyberhawk Innovations, Flyability, ExRobotics, Petrofac, Diakont |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |