Quick Navigation

Report Overview

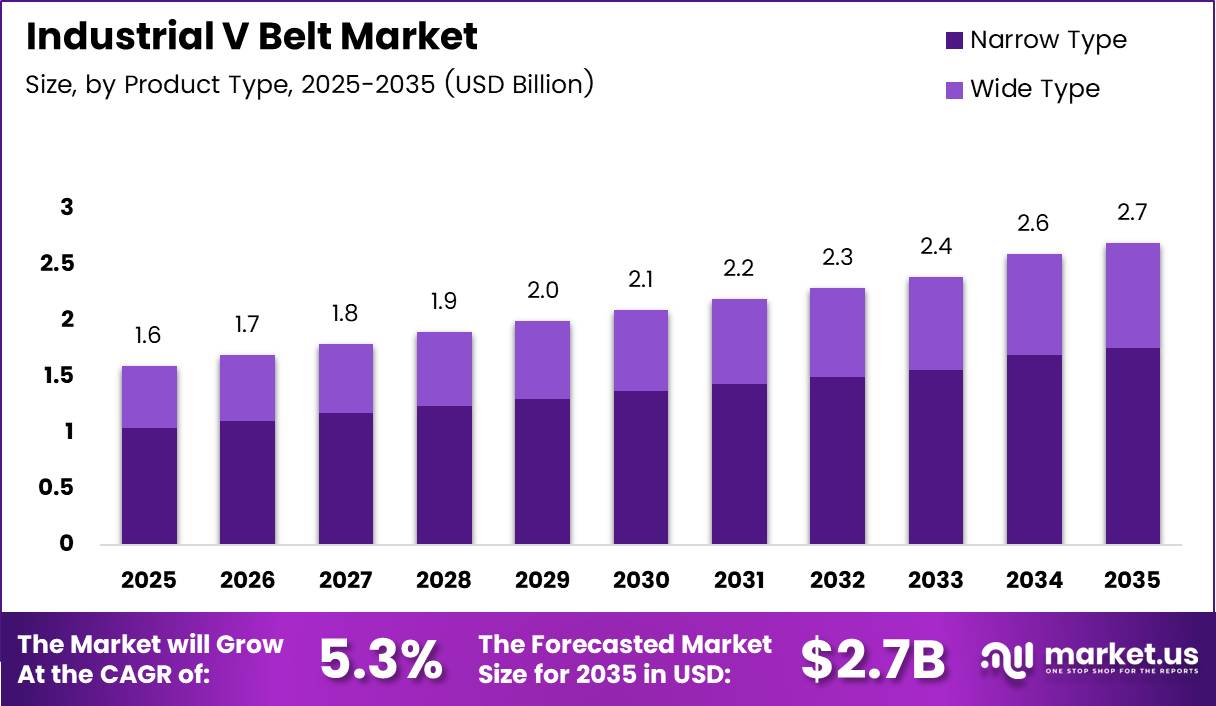

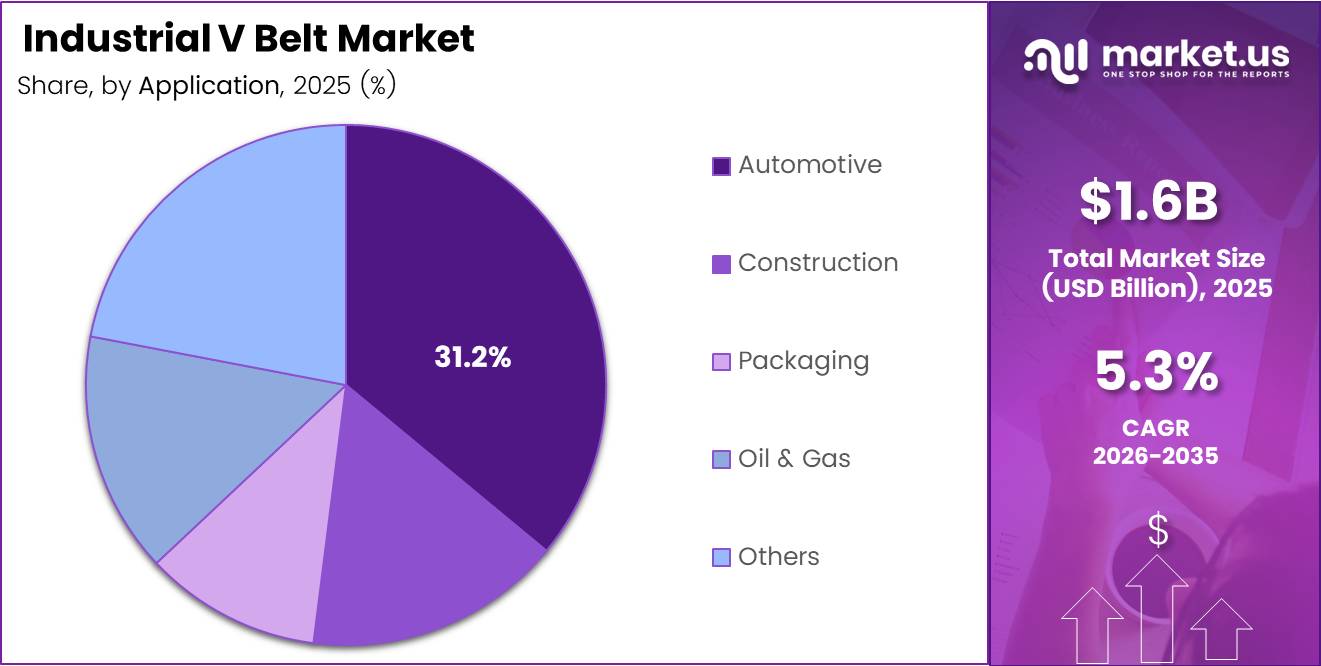

Global Industrial V Belt Market size is expected to be worth around USD 2.7 Billion by 2035 from USD 1.6 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The industrial V belt market covers rubber, polyurethane, and neoprene belt drives used in mechanical power transmission across factories, processing plants, and material handling facilities. These belts connect motors to driven equipment by transferring torque through wedge-shaped contact with grooved pulleys. This structural role makes V belts a foundational component in industrial machinery worldwide.

The market segments by product type into narrow and wide variants, by material into rubber, polyurethane, and neoprene, and by application into automotive, construction, packaging, oil and gas, and others. Narrow type belts hold the largest product share. Automotive applications represent the single largest end-use segment. This segmentation reflects both legacy industrial demand and new application-driven requirements.

Manufacturing expansion across Asia Pacific continues to anchor global demand for reliable belt drive systems. Warehouse automation projects and material handling equipment installations create steady replacement and new-installation cycles. Governments in emerging economies are prioritizing industrial modernization, which pulls V belt consumption upward across multiple end-use sectors.

Regulatory focus on industrial energy efficiency is reshaping procurement decisions. Facilities managers increasingly evaluate belt drive performance using measurable energy loss benchmarks. This shift creates pressure on belt manufacturers to demonstrate verified efficiency ratings rather than rely on general product claims.

According to our research, a correctly installed wrapped industrial V belt attains 95 to 98% efficiency soon after installation. This performance level declines to approximately 93% without periodic re-tensioning. Buyers who overlook maintenance scheduling face measurable energy cost penalties, which favors vendors offering maintenance service contracts alongside product sales.

As reported by our research, high-quality V belts in properly maintained applications operate at up to 98% efficiency, meaning only 2% of input power is lost in transmission. This efficiency benchmark positions premium V belt products as cost-justified alternatives to cheaper belts with higher energy loss. Procurement teams can calculate payback periods directly from this figure.

Key Takeaways

- The Global Industrial V Belt Market is valued at USD 1.6 Billion in 2025 and is forecast to reach USD 2.7 Billion by 2035.

- The market grows at a CAGR of 5.3% during the forecast period 2026 to 2035.

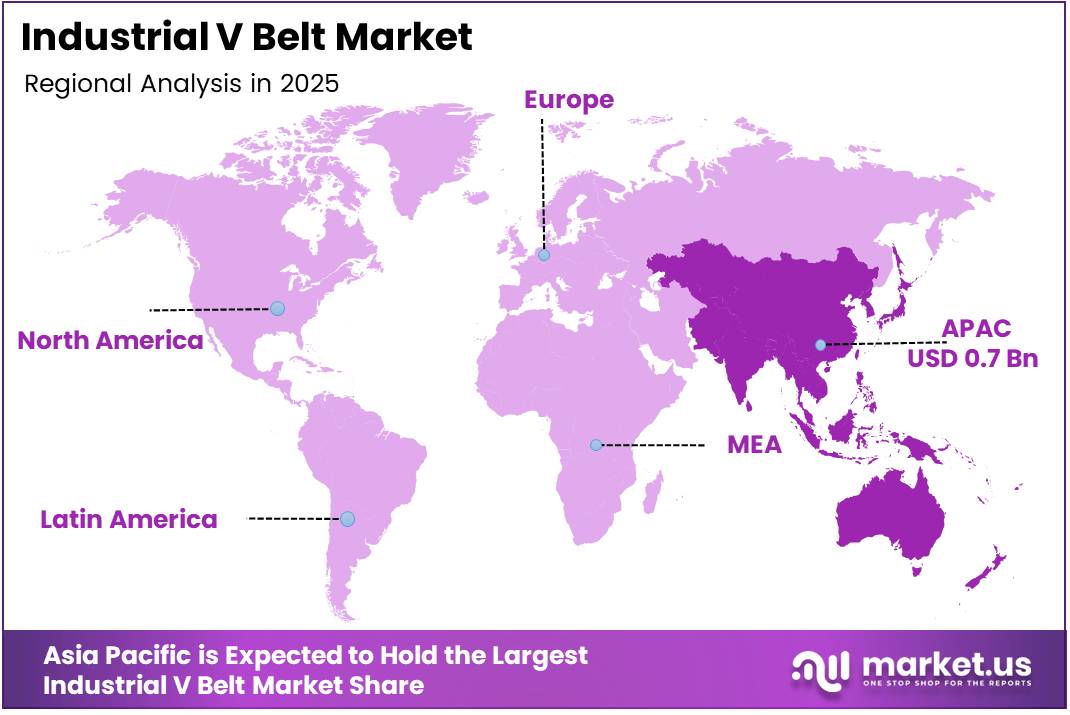

- Asia Pacific dominates the regional landscape with a 43.80% share, valued at USD 0.7 Billion.

- By Product Type, Narrow Type belts hold the dominant position with a 65.3% share.

- By Material, Rubber Belt leads with a 56.1% share across industrial applications.

- By Application, Automotive represents the largest end-use segment with a 31.2% share.

Product Type Analysis

Narrow Type dominates with 65.3% due to compact design and high torque transfer efficiency.

In 2025, Narrow Type V belts held a dominant market position in the By Product Type segment of the Industrial V Belt Market, with a 65.3% share. Their compact cross-section allows higher speed ratios in tighter drive configurations. This design advantage makes them the preferred choice for modern industrial equipment where space efficiency and power density are both required.

Wide Type V belts serve heavy-duty drive applications where torque loads exceed the capacity of narrow profiles. Industrial sectors such as mining, heavy processing, and large-scale agricultural equipment rely on wide belt configurations for sustained power transfer. Their lower speed capability is offset by higher load tolerance, which maintains demand in equipment categories where reliability under stress is the primary procurement criterion.

Material Analysis

Rubber Belt dominates with 56.1% due to established supply chains and proven durability.

In 2025, Rubber Belt held a dominant market position in the By Material segment of the Industrial V Belt Market, with a 56.1% share. Rubber compounds offer a combination of flexibility, heat resistance, and tensile strength that suits a wide range of factory environments. This material’s cost advantage over synthetic alternatives keeps it embedded in standard procurement specifications across global manufacturing facilities.

Polyurethane V-belt products address applications requiring resistance to oil, abrasion, and higher ambient temperatures than standard rubber allows. These belts carry a price premium but deliver longer service intervals in chemically exposed environments. Buyers in food processing, pharmaceutical, and petrochemical sectors justify the additional cost through reduced replacement frequency and lower downtime risk.

Neoprene V-belt variants offer superior resistance to ozone, weathering, and moderate chemical contact. This makes them relevant for outdoor installations and equipment operating in variable climate conditions. Their share of the material segment remains smaller than rubber but represents a stable niche within applications where environmental exposure is a primary design constraint.

Application Analysis

Automotive dominates with 31.2% due to high-volume OEM and aftermarket replacement cycles.

In 2025, Automotive held a dominant market position in the By Application segment of the Industrial V Belt Market, with a 31.2% share. Vehicle assembly lines and aftermarket service networks both drive consistent belt replacement volumes. This dual demand channel, combining original equipment manufacturing with aftermarket servicing, gives the automotive segment structural resilience that other application categories do not share.

Construction equipment relies on V belt drives in compressors, concrete mixers, and lifting systems where direct drive alternatives are cost-prohibitive. Construction sector growth in emerging markets generates parallel demand for belt drive components. This application segment benefits from infrastructure investment cycles, which tend to run in multi-year phases and provide predictable demand windows for belt suppliers.

Packaging machinery uses V belt drives extensively in conveyor systems, filling equipment, and labeling lines operating at high cycle rates. Manufacturers in food, beverage, and consumer goods sectors prioritize belt reliability to reduce line stoppage risk. This performance requirement favors premium belt grades, giving suppliers an opportunity to compete on total cost of ownership rather than unit price alone.

Key Market Segments

By Product Type

- Narrow Type

- Wide Type

By Material

- Rubber Belt

- Polyurethane V-belt

- Neoprene V-belt

By Application

- Automotive

- Construction

- Packaging

- Oil & Gas

- Others

Market Dynamics

Drivers - Industrial automation expansion and efficiency benchmarks create durable procurement demand

Industrial automation projects across manufacturing and processing sectors require reliable power transmission components to sustain continuous equipment operation. Automated assembly lines, conveyor systems, and robotic work cells all depend on belt drives running without unplanned failure. This reliability requirement makes V belts a non-discretionary input rather than a discretionary purchase, which protects demand even during capital expenditure slowdowns.

According to our research, a correctly installed wrapped industrial V belt attains 95 to 98% efficiency soon after installation, declining to approximately 93% without periodic re-tensioning. This efficiency gap creates a quantifiable cost argument for scheduled maintenance programs. Suppliers who package belts with maintenance service agreements gain a recurring revenue stream and reduce customer churn by embedding themselves into facility operations cycles.

Material handling equipment installations in warehouses, distribution centers, and logistics hubs require belt drive systems rated for continuous duty under variable loads. Warehouse automation infrastructure investment has accelerated across North America, Europe, and Asia Pacific. Each new automated facility represents a fresh installation opportunity for V belt suppliers, and every operational facility creates an ongoing replacement demand cycle that sustains market revenue between new-build phases.

Restraints - Maintenance gaps, temperature limits, and competing technologies constrain market penetration

Direct drive and gear-based transmission systems compete with V belts in applications where zero-slip torque transfer is required. As automation precision requirements increase, some equipment designers specify gear or direct drive systems to eliminate belt slippage risk. This substitution pressure is most acute in high-precision manufacturing environments, where V belt market share faces structural erosion from technically superior alternatives for specific duty conditions.

As reported by our research, improperly maintained V belts lose up to 20% efficiency from the initial installed level due to slippage and stretch. This degradation translates directly into higher energy costs and increased heat generation in drive systems. Facilities with poor maintenance discipline face compounding costs, which in some cases leads procurement managers to replace V belt systems with lower-maintenance alternatives rather than invest in tensioning programs.

Data from our research shows standard industrial V belts are rated for continuous operation between -30°C and +60°C. Applications outside this temperature window require specialty belt compounds at a cost premium. Facilities operating in extreme heat environments, such as foundries or tropical outdoor installations, face limited product options and higher unit costs. This constraint restricts V belt penetration in temperature-extreme segments and pushes buyers toward alternative transmission technologies.

Growth Factors - Efficiency upgrades, energy savings, and emerging economy expansion unlock new revenue

Renewable energy installations, including wind turbines and solar tracking systems, require mechanical power transmission components suited for outdoor, long-service-interval operation. V belt manufacturers who develop products meeting the load and environmental specifications of renewable energy equipment gain access to a capital-intensive and growing equipment category. This application expansion reduces the market’s dependence on traditional manufacturing end-use demand.

Our research indicates that upgrading from a wrapped V belt to a raw-edge cogged V belt yields an average efficiency increase of approximately 2 percentage points for the belt drive. This measurable improvement translates into direct energy cost savings for facility operators. Suppliers who can demonstrate this upgrade payback with plant-level energy data create a value-based sales argument that accelerates replacement cycles beyond standard wear-driven timelines.

Figures from our research show switching from wrapped to raw-edge cogged V belts reduces belt-drive energy use by roughly 2% for the same mechanical load. Across large facilities with hundreds of drive systems, this saving compounds into material operational cost reductions. This positions cogged V belt products as an energy efficiency upgrade with a calculable return, making them relevant to sustainability procurement programs now active in large industrial companies globally.

Emerging Trends - Smart monitoring, low-noise design, and synchronous belt adoption redefine performance standards

Predictive maintenance platforms now integrate belt condition monitoring using vibration, temperature, and tension sensors embedded in drive systems. Manufacturers who supply belts compatible with smart sensor integration gain a competitive advantage as facilities migrate from reactive to predictive maintenance schedules. This technology shift creates a new product differentiation axis beyond material grade and belt geometry, rewarding technically capable suppliers.

In Spring 2025, Continental launched the CONTI NXT Multi V-Belt incorporating recycled PET tension cords, recycled carbon black, and renewable materials. This product development signals that sustainability credentials are becoming a competitive differentiator in the industrial belt market. Buyers operating under corporate emissions reduction commitments will increasingly specify products with verified recycled content, creating a market segment where environmental performance is as important as mechanical performance.

Based on our research data, designing industrial drives with synchronous belts instead of V belts can improve belt-drive efficiency by approximately 5 percentage points under comparable load conditions. Our research also confirms synchronous belts reduce belt-drive energy consumption by about 5% versus V belt configurations. This performance gap creates pressure on V belt manufacturers to close the efficiency differential through advanced belt compounds or risk losing specification preference in new industrial drive designs.

Regional Analysis

Asia Pacific Dominates the Industrial V Belt Market with a Market Share of 43.80%, Valued at USD 0.7 Billion

Asia Pacific holds a 43.80% share of the global Industrial V Belt Market, valued at USD 0.7 Billion. China, India, and Southeast Asian economies continue to expand manufacturing output, generating direct demand for power transmission components. Government-backed industrial modernization programs in these economies accelerate equipment installation timelines and create steady procurement cycles for V belt suppliers operating in the region.

North America maintains a structurally strong position through its advanced automotive manufacturing base and active replacement aftermarket. The US accounts for the majority of regional belt consumption, supported by large installed bases of industrial machinery across processing, packaging, and energy sectors. Replacement demand in mature industrial facilities provides a consistent revenue floor for belt distributors and OEM suppliers serving this region.

Europe holds a notable share driven by strict energy efficiency standards applied to industrial drive systems. German and Italian manufacturing clusters maintain high equipment utilization rates that require frequent belt inspection and replacement. Regulatory pressure on industrial energy consumption in the European Union pushes facility operators toward verified high-efficiency belt products, which supports premium pricing for compliant manufacturers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

PIX Transmissions Ltd. competes across a broad product range covering standard and specialty V belts for industrial and automotive applications. This breadth allows PIX to serve both OEM and aftermarket channels simultaneously. However, maintaining quality consistency across a wide SKU base creates operational risk, particularly when raw material costs fluctuate and margin pressure increases across standard belt grades.

In October 2025, Solve Industrial Motion Group acquired B&B Manufacturing, adding synchronous belts, V-belt sheaves, and timing pulleys to its manufacturing portfolio. This acquisition extended Solve’s vertical integration in power transmission components. By controlling more of the drivetrain supply chain, Solve reduces dependency on third-party component suppliers and strengthens its cost position against competitors who rely on external sourcing for sheave and pulley components.

Key Players

- PIX Transmissions Ltd.

- Mitsuboshi Belting Ltd.

- Bando Chemical Industries Ltd.

- SKF Group

- Dunlop Belting Products

- Goodyear Belts

- Hutchinson Belt Drive Systems

- Arntz Optibelt Group

- Sanlux Co., Ltd.

- Sumitomo Rubber Industries Ltd.

Recent Developments

- December 2025 – Solve Industrial Motion Group acquired D&D Global, a vertically integrated manufacturer of power drive belts specializing in V-belts and timing belts with more than 35,000 belt configurations, expanding its belt manufacturing portfolio.

- May 2026 – The Timken Company entered into an agreement to sell its belts business to Gates Industrial Corporation, a transaction that expands Gates’ industrial power transmission portfolio and broadens its coverage across OEM and aftermarket belt channels.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.6 Billion |

| Forecast Revenue (2035) | USD 2.7 Billion |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Narrow Type, Wide Type); By Material (Rubber Belt, Polyurethane V-belt, Neoprene V-belt); By Application (Automotive, Construction, Packaging, Oil & Gas, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | PIX Transmissions Ltd., Mitsuboshi Belting Ltd., Bando Chemical Industries Ltd., SKF Group, Dunlop Belting Products, Goodyear Belts, Hutchinson Belt Drive Systems, Arntz Optibelt Group, Sanlux Co., Ltd., Sumitomo Rubber Industries Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |