Quick Navigation

Report Overview

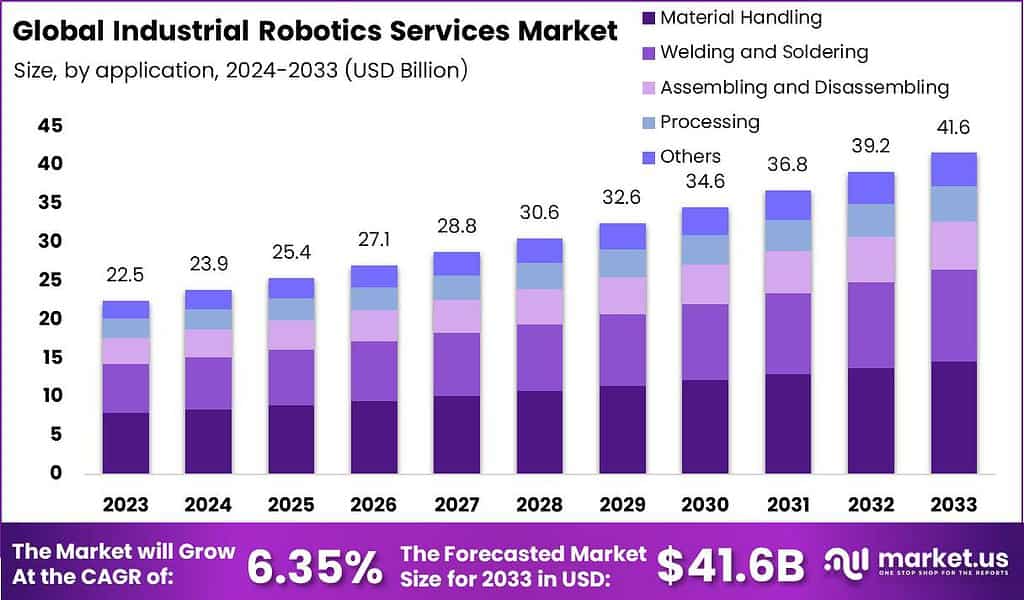

The Global Industrial Robotics Services Market size is expected to be worth around USD 41.6 Billion By 2033, from USD 22.5 Billion in 2023, growing at a CAGR of 6.35% during the forecast period from 2024 to 2033. In 2023, APAC held a dominant market position, capturing more than a 35.4% share, holding USD 7.9 Billion revenue.

Industrial robotics services involve the management, maintenance, and optimization of industrial robots. These services ensure that robotic systems operate efficiently and effectively in manufacturing and production settings. The aim is to maximize uptime, enhance production quality, and extend the lifespan of robots through timely repairs, software updates, and performance tuning.

The industrial robotics services market is growing as more industries adopt automation to increase precision and efficiency in their operations. This market includes service providers who are skilled in the technical, operational, and maintenance aspects of industrial robots, offering tailored solutions to meet the diverse needs of manufacturers.

The primary growth factors for the industrial robotics services market include the increasing adoption of automation across various industries and the need for regular maintenance to ensure operational efficiency. Advances in technologies like AI and machine learning are also enhancing the capabilities of industrial robots, thereby driving the demand for expert services to manage more complex systems.

Market demand for industrial robotics services is driven by the continuous need for operational excellence in manufacturing processes. As robots play a crucial role in production, the demand for skilled services to maintain and optimize these robots remains high. Industries such as automotive, electronics, and heavy machinery heavily rely on robotic services to maintain their production lines and reduce labor costs.

Industrial robotics services have gained significant popularity due to their critical role in maximizing the efficiency of automation investments. With the widespread adoption of robots, industries recognize the importance of regular maintenance and updates provided by these services. This popularity is also spurred by the need for expertise in managing advanced robotics technologies, which are becoming increasingly sophisticated.

There are substantial opportunities within the industrial robotics services market, especially in developing customized solutions for unique manufacturing environments. Additionally, the shift towards Industry 4.0 and smart factories presents opportunities for integrating IoT and AI with robotics services, creating smarter and more predictive maintenance strategies that can foresee and prevent potential downtimes.

The market is set to expand with the broader adoption of robotics in industries that have traditionally been less automated, such as food and beverage or textiles. As robots become more integrated into general manufacturing processes worldwide, the demand for specialized services to install, maintain, and repair these robots is expected to grow, opening new regional markets for service providers.

According to Exploding Topics, Asia controls over one-third of the global robotics industry’s revenue. Today, there are more than 3.4 million industrial robots operating worldwide. The global robot-to-human ratio in the manufacturing industry is 1 to 71, indicating the increasing use of automation in industrial processes.

Industrial companies are planning to invest 25% of their capital in industrial automation over the next five years, which will further drive automation growth. However, this trend has impacted workers, as 14% of workers have lost their jobs to robots.

In 2023, the total unit sales of industrial robots reached 541,302, reflecting a slight decline of 2.1% compared to the previous year. Despite the sales dip, the operational stock of industrial robots grew by 9.7%, bringing the global total to 4,281,585 units. China holds the largest share at 41%, followed by Japan (10.2%), the United States (8.9%), South Korea (8.9%), and Germany (6.3%).

Global robot density in the manufacturing sector increased from 151 to 162 robots per 10,000 employees. South Korea leads with 1,012 robots per 10,000 employees, followed by China (470), Germany (429), and Japan (419).

According to Zippia, 88% of companies plan to invest in robotics, showcasing the continued interest in automation. Currently, there are 3 million industrial robots in use globally, and approximately 400,000 new robots enter the market each year. The global industrial robotics market is valued at around $43.8 billion in revenue

Key Takeaways

- The Industrial Robotics Services Market is expected to expand significantly, reaching USD 41.6 billion by 2033 from USD 22.5 billion in 2023, growing at a CAGR of 6.35% between 2024 and 2033.

- In 2023, the Material Handling segment emerged as a key player, holding 31.8% of the market share. This segment’s growth can be attributed to the increasing demand for automated solutions in manufacturing and logistics.

- The Automotive sector also captured a notable share, accounting for over 37% of the market in 2023. This is largely driven by the industry’s growing reliance on robotics for improving production efficiency and precision.

- Regionally, the Asia-Pacific (APAC) region led the market, securing over 35.4% of the total share and generating revenues of USD 7.9 billion in 2023. This dominance is due to the region’s strong manufacturing base and rising investments in automation technologies.

Application Analysis

In 2023, the Material Handling segment held a dominant market position in the industrial robotics services market, capturing more than a 31.8% share. This leading role is primarily attributed to the increasing need for automation in handling heavy and complex materials across various industries, including automotive, electronics, and food and beverages.

Material handling robots are crucial for reducing human error and enhancing efficiency, especially in environments that require precision and repetitive tasks. These robots can perform tasks such as picking, placing, and packaging with high consistency and speed, which are essential for maintaining production flow and meeting market demands.

The integration of advanced sensors and AI has further enhanced their capabilities, making them more adaptable to different operational setups and able to handle delicate and varied materials without damage. The rise in e-commerce has also significantly fueled the demand for material handling robots. Warehouses and distribution centers are increasingly deploying robots to streamline operations and increase throughput.

As online shopping continues to grow, the need for efficient logistics and rapid fulfillment is more critical than ever, driving investment in robotic systems that can quickly and accurately handle large volumes of products. Moreover, industries are focusing on reducing workplace injuries associated with heavy lifting and repetitive tasks.

Material handling robots not only alleviate these health risks but also reduce the labor costs associated with such operations. The ongoing improvements in robotic technology, making these systems more cost-effective and energy-efficient, continue to attract businesses seeking to enhance their operational efficiency and safety standards.

End-User Analysis

In 2023, the Automotive segment held a dominant market position in the industrial robotics services market, capturing more than a 37% share. This substantial market share is primarily due to the automotive industry’s high reliance on robotic systems for various manufacturing processes, from assembly lines to painting and welding.

Robots in the automotive sector are integral to achieving the precision and efficiency required in vehicle production. They are employed extensively to perform tasks that ensure high-quality standards are met consistently and cost-effectively. For instance, robots provide the necessary speed and accuracy for welding and assembling parts, which are critical operations that can significantly influence production timelines and overall product quality.

Furthermore, the push towards electric vehicles (EVs) and the adoption of new manufacturing technologies to accommodate EV production have spurred additional demand for advanced robotic systems. These systems are not only used for traditional manufacturing tasks but are also being adapted for new applications such as battery assembly and the handling of lightweight materials designed to improve fuel efficiency.

Additionally, the automotive industry is faced with stringent safety and environmental regulations, which drive the need for high precision in production processes to comply with these standards. Industrial robotics services are crucial for maintaining the robots that perform these tasks, ensuring they operate at peak efficiency with minimal downtime.

Key Market Segments

By Application

- Material Handling

- Welding and Soldering

- Assembling and Disassembling

- Processing

- Others

By End-User

- Healthcare and Pharmaceuticals

- Automotive

- Food and Beverages

- Electrical and Electronics

- Others

Driver

Increasing Automation Demand in Manufacturing

The industrial robotics services market is significantly driven by the escalating demand for automation within the manufacturing sector. Industries such as automotive, electronics, and consumer goods face ongoing pressures to boost productivity, minimize operational costs, and enhance quality.

Industrial robots address these challenges by automating repetitive and hazardous tasks, thereby improving efficiency and safety on production floors. This surge in automation prompts a corresponding increase in the need for robotics services including installation, maintenance, programming, and updates to ensure these robots operate effectively and efficiently.

Moreover, the incorporation of cutting-edge technologies like AI, machine learning, and IoT is making industrial robots smarter and more adaptable, further boosting the demand for specialized services to manage these advanced systems. Robotics service providers are pivotal in supporting the widespread adoption of automation across various industries.

Restraint

High Initial Costs of Robotics Services

A major restraint in the industrial robotics services market is the steep initial costs associated with implementing and maintaining robotic systems. Small and medium-sized enterprises (SMEs) often find the expenses for robot purchase, staff training, production line reconfiguration, and ongoing maintenance prohibitive. Although the long-term benefits include enhanced productivity and lower operational costs, the upfront investment can be daunting, especially for businesses with limited budgets.

Even with options like leasing or robotics-as-a-service, the financial burden can impede adoption rates, particularly in regions with lower labor costs where the financial justification for automation may not be as strong. The need for specialized knowledge for regular servicing adds additional costs, complicating the ROI calculations for potential adopters.

Opportunity

Rising Demand for Collaborative Robots (Cobots)

The market presents a significant opportunity with the growing interest in collaborative robots, or cobots, which are designed to operate alongside human workers safely. Cobots offer several advantages over traditional industrial robots: they are smaller, more cost-effective, and simpler to program, making them especially suitable for SMEs looking to adopt automation without substantial overheads.

As cobots gain traction across various industries, there is an increasing demand for services like installation, integration, and maintenance, ensuring they function effectively in collaborative environments. The advancement of Industry 4.0, emphasizing smart manufacturing and connected devices, further promotes cobot adoption. Service providers can capitalize on this by offering specialized services such as safety assessments, custom programming, and interface design to facilitate human-robot collaboration.

Challenge

Integration with Legacy Systems

Integrating modern robotic technologies with existing legacy systems poses a significant challenge in the industrial robotics services market. Many manufacturing facilities still operate with outdated equipment that may not seamlessly accommodate new robotic solutions. Such integrations are often complex, costly, and time-intensive, particularly for businesses without the necessary technical expertise.

Legacy systems might require extensive customization or retrofitting to align with new industrial robots, adding to deployment costs and potentially delaying automation adoption. Robotic service providers must develop innovative solutions, like custom software or hardware interfaces, to bridge these gaps. However, these solutions demand specialized skills and time, which could limit the scalability of robotic implementations in traditional manufacturing setups.

Emerging Trends

The industrial robotics services market is witnessing several emerging trends that are reshaping the landscape of automation and manufacturing. One of the most significant trends is the increasing integration of artificial intelligence (AI) and machine learning technologies into robotic systems.

Advances in humanoid robots are projected to transform numerous sectors by performing tasks in environments designed for humans. While promising, the widespread adoption of humanoid robots faces challenges like cost and the need to demonstrate clear ROI against established robotic systems.Cobots are gaining popularity for their ability to safely work alongside humans without the need for elaborate setups. This trend is particularly appealing to SMEs due to the lower cost and flexibility cobots offer.

These robots combine mobility and manipulative abilities, allowing them to perform tasks across various environments like logistics and manufacturing. The versatility and collaborative capabilities of mobile manipulators are expanding their use cases, making them increasingly common in settings that require dynamic human-robot interaction.

The use of digital twin technology is growing as it enables better simulation and optimization of robotic systems. By creating virtual replicas of physical systems, companies can test and modify configurations in a virtual environment before actual deployment, which helps in reducing costs and improving system performance.

Top Use Cases and Business Benefits

Industrial robotics services are transforming the operational landscape across various sectors by offering robust solutions to common industrial challenges. These robotic systems are increasingly being utilized for tasks that range from basic material handling to complex assembly operations, bringing substantial business benefits across the board.

One of the primary uses of industrial robots is in material handling, where they improve efficiency by automating the transportation and organization of materials. Robots can operate around the clock, reducing downtime and increasing productivity significantly. Similarly, in welding and soldering, robots provide precision and consistency that are difficult to achieve manually, thereby enhancing the quality of the final products.

Assembling and disassembling tasks benefit from robotics by speeding up these processes and reducing labor costs. Robots are adept at handling repetitive tasks with high precision, which minimizes errors and waste. In processing operations, such as painting or cutting, robots can deliver high-quality work at a pace that surpasses human capabilities.

The deployment of robotics in these areas not only fills labor gaps but also counters rising operational costs and helps industries stay competitive in tough economic conditions. Additionally, robots are instrumental in achieving high levels of digitalization within factories. They facilitate the integration of advanced technologies like AI and IoT, enhancing data connectivity and analytics, which lead to smarter, data-driven decision-making.

Impact of Generative AI

Generative AI is revolutionizing the industrial robotics sector by introducing levels of autonomy and efficiency previously unattainable. This technology enhances the capabilities of robots, making them not only faster and more reliable but also capable of performing more complex tasks with minimal human oversight.

One significant impact of generative AI in industrial robotics is its ability to enable machines to learn from their operations and improve over time. This learning capability is crucial for tasks that require adaptability, such as adjusting techniques or methods based on the material being processed or the specific requirements of a task.

Moreover, generative AI supports the optimization of robotic operations through predictive maintenance and real-time decision-making. By analyzing data collected from various sensors and operations, AI algorithms can predict when a robot might fail or when maintenance is needed, thereby reducing downtime and extending the lifespan of the machinery.

Generative AI also plays a pivotal role in enhancing the programming of robots. Traditional programming can be labor-intensive and complex; however, AI can simplify these processes, enabling quicker setup and deployment of robotic systems. This capability is particularly valuable in environments where customization and flexibility are critical, such as in bespoke manufacturing or dynamic processing operations.

As industries increasingly adopt cloud computing, 5G, and IoT, the synergies with AI become even more potent, allowing for seamless integration of robotics into digital production environments. This integration leads to highly efficient, scalable, and cost-effective robotic solutions that can dynamically adapt to changing market demands.

Technological Innovations

The integration of advanced technologies in industrial robotics services is driving profound changes across manufacturing sectors. Here’s how these innovations are shaping the industry:

- Enhanced Autonomy and Flexibility: Robotics technologies have evolved to include more autonomous functions, enabling machines to make decisions and adjust operations without human input. This autonomy is particularly beneficial in environments that require high precision or where human safety could be compromised.

- Improved Programming and Maintenance: Generative AI assists in simplifying the programming of robots through natural language processing and machine learning algorithms. It can generate programming code from simple text inputs, making the robots easier to adapt to different tasks without extensive manual programming. Additionally, AI-driven predictive maintenance can foresee potential system failures before they occur, scheduling preventive maintenance and thus reducing unexpected downtimes.

- Advanced Sensory Capabilities: Today’s robots are equipped with sophisticated sensors that help in detailed environmental analysis, which enhances their performance in complex scenarios. These sensors, combined with AI, allow robots to understand their surroundings better, adapt to changes, and perform tasks with higher precision.

- Collaborative Robots (Cobots): Cobots continue to be a significant trend, designed to work alongside humans without the need for protective barriers. This collaboration happens safely and efficiently, as cobots are equipped with advanced safety features and can learn and adapt to human workers’ habits and signals.

- Sustainability and Energy Efficiency: Modern robotics technology is also steering towards more sustainable practices, with robots being designed to operate with optimal energy efficiency and reduced waste. The use of materials and energy resources is carefully managed by AI systems, contributing to greener production processes.

Regional Analysis

In 2023, APAC held a dominant market position in the industrial robotics services market, capturing more than a 35.4% share and generating revenue of USD 7.9 billion. This leading status is largely attributed to the rapid industrialization across several APAC countries and the significant investments in automation technologies by major manufacturing and production industries.

The region’s dominance is further supported by the presence of several leading global manufacturers of robots and the availability of skilled labor for robotics programming and maintenance. Countries like China, South Korea, and Japan are at the forefront of robotics in manufacturing, significantly contributing to the market’s growth. These countries are home to some of the world’s largest automotive and electronics manufacturers, which heavily utilize robotics for production.

Additionally, the push from governments in the region for increased adoption of advanced technologies in manufacturing to maintain competitive advantage and boost productivity has fueled the growth of robotics services. Initiatives aimed at enhancing technological capabilities through subsidies and tax incentives have made it easier for companies to invest in robotics.

Moreover, the rising labor costs in the region have prompted companies to adopt robotics solutions to optimize production costs and enhance efficiency. The increasing demand for consumer electronics, driven by high consumer spending power in the region, also plays a crucial role in this dynamic market expansion. These factors collectively ensure that APAC continues to lead the global industrial robotics services market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The Industrial robotics services market features a competitive landscape marked by several key players that are driving innovation and growth. Major corporations like ABB,Carl Cloos Schweisstechnik GmbH, Fanuc and Yaskawa are at the forefront, leveraging their extensive expertise and established reputations to offer a wide range of robotic solutions.

ABB has been particularly active in expanding and innovating its industrial robotics services through strategic acquisitions and product launches. In 2024, ABB acquired Sevensense, a Swiss start-up specializing in AI-based navigation for autonomous mobile robots (AMRs). This acquisition highlights ABB’s focus on integrating cutting-edge AI technologies to enhance the capabilities of its robots, particularly in terms of navigation and autonomy in complex industrial environments

Daihen Corp., a veteran in the field of industrial robotics, has been actively pursuing growth through both product innovation and strategic mergers. In the past year, Daihen launched a series of cutting-edge robots designed to improve efficiency and automation in manufacturing processes. These new offerings reflect Daihen’s commitment to technology leadership. Furthermore, a recent merger with a European robotics firm has allowed Daihen to enhance its service range and market penetration, reinforcing its status as a key player in the global market.

DENSO Corp. continues to excel in the industrial robotics sector by focusing on transformative strategies such as launching innovative products and entering into pivotal mergers. Their latest product launches have focused on integrating AI and IoT into their robotics solutions, setting new standards for smart manufacturing. Moreover, DENSO’s strategic mergers have expanded their operational footprint and enabled them to tap into emerging markets, thereby solidifying their market presence and driving future growth.

Top Key Players in the Market

- ABB Ltd.

- Carl Cloos Schweisstechnik GmbH

- Daihen Corp.

- DENSO Corp.

- FANUC Corp.

- Kawasaki Heavy Industries Ltd.

- Mitsubishi Electric Corp.

- NACHI FUJIKOSHI Corp.

- OMRON Corp.

- Panasonic Holdings Corp.

- Seiko Epson Corp.

- Staubli International AG

- Teradyne Inc.

- Universal Robots AS

- Yaskawa Electric Corp

- Other Key Players

Recent Developments

- Yaskawa Electric Corp.(2023): Yaskawa introduced its HC30PL, a 30-kg payload cobot, designed for safe collaboration with humans in various industrial applications. This launch aligns with Yaskawa’s focus on automation and robotics innovation, particularly in automotive and electronics manufacturing.

- ABB Ltd.(2024): ABB acquired Meshmind, a software service provider, to boost its capabilities in AI, machine vision, and industrial IoT. This acquisition will establish a global R&D hub in Sarajevo, Bosnia, aimed at developing advanced AI-powered automation solutions. Additionally, ABB launched the OmniCore robotics control platform, enhancing robotic precision and energy efficiency. The new platform is designed to meet the growing demand for automation across sectors such as logistics and manufacturing.

- Universal Robots (2024 ): Launched an AI-powered machine tending solution at IMTS 2024. This system improves efficiency by utilizing deep learning-based part detection, enabling faster batch changeovers without needing fixtures. This innovation is set to help manufacturers streamline their processes.

- Kawasaki Robotics (2024 ): Introduced its new CL Series of collaborative robots (cobots) at IMTS 2024 in September. These cobots focus on high-speed performance with payload capacities ranging from 3 kg to 10 kg. The company has developed the CL Series to address labor shortages by providing advanced capabilities while maintaining industrial-grade performance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 22.5 Bn |

| Forecast Revenue (2033) | USD 41.6 Bn |

| CAGR (2024-2033) | 6.35% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Material Handling,Welding and Soldering,Assembling and Disassembling,Processing,Others), By End-User (Healthcare and Pharmaceuticals,Automotive,Food and Beverages,Electrical and Electronics,Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ABB Ltd., Carl Cloos Schweisstechnik GmbH, Daihen Corp., DENSO Corp., FANUC Corp., Kawasaki Heavy Industries Ltd., Mitsubishi Electric Corp., NACHI FUJIKOSHI Corp., OMRON Corp., Panasonic Holdings Corp., Seiko Epson Corp., Staubli International AG, Teradyne Inc., Universal Robots AS, Yaskawa Electric Corp, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |