Quick Navigation

Report Overview

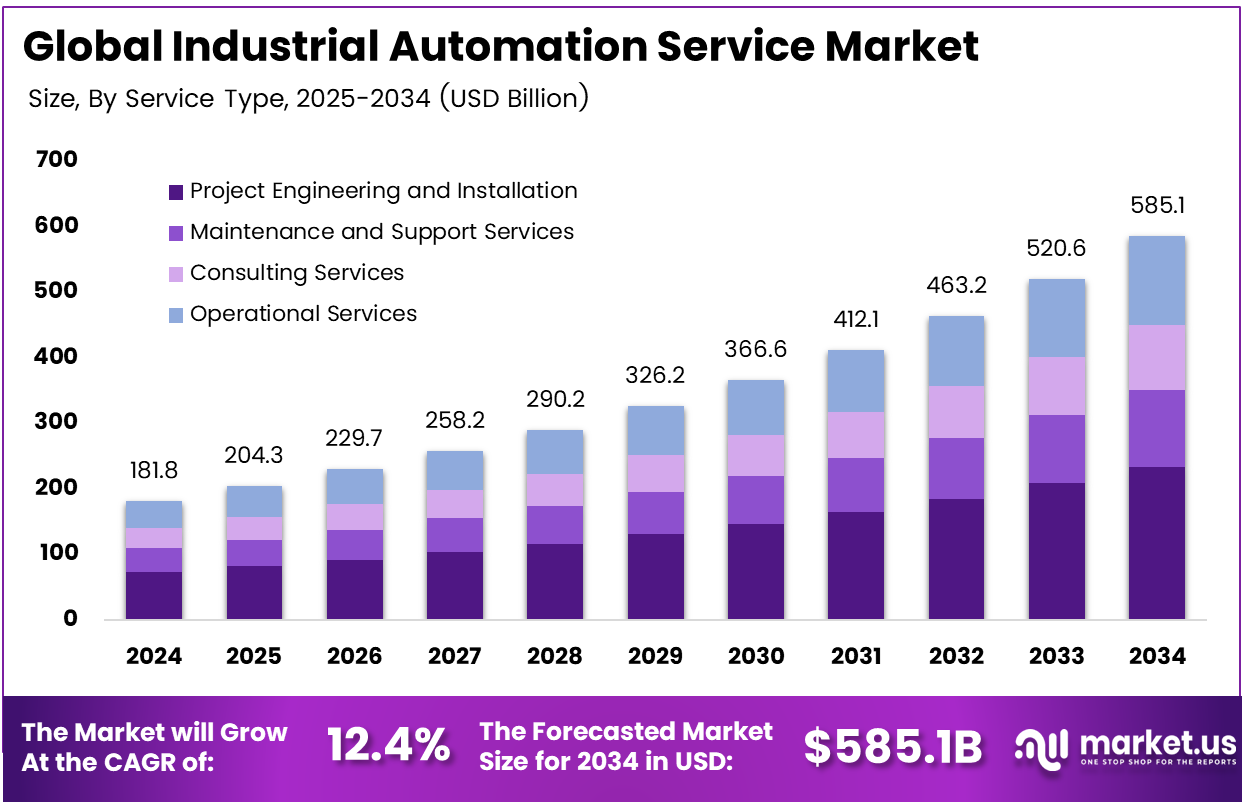

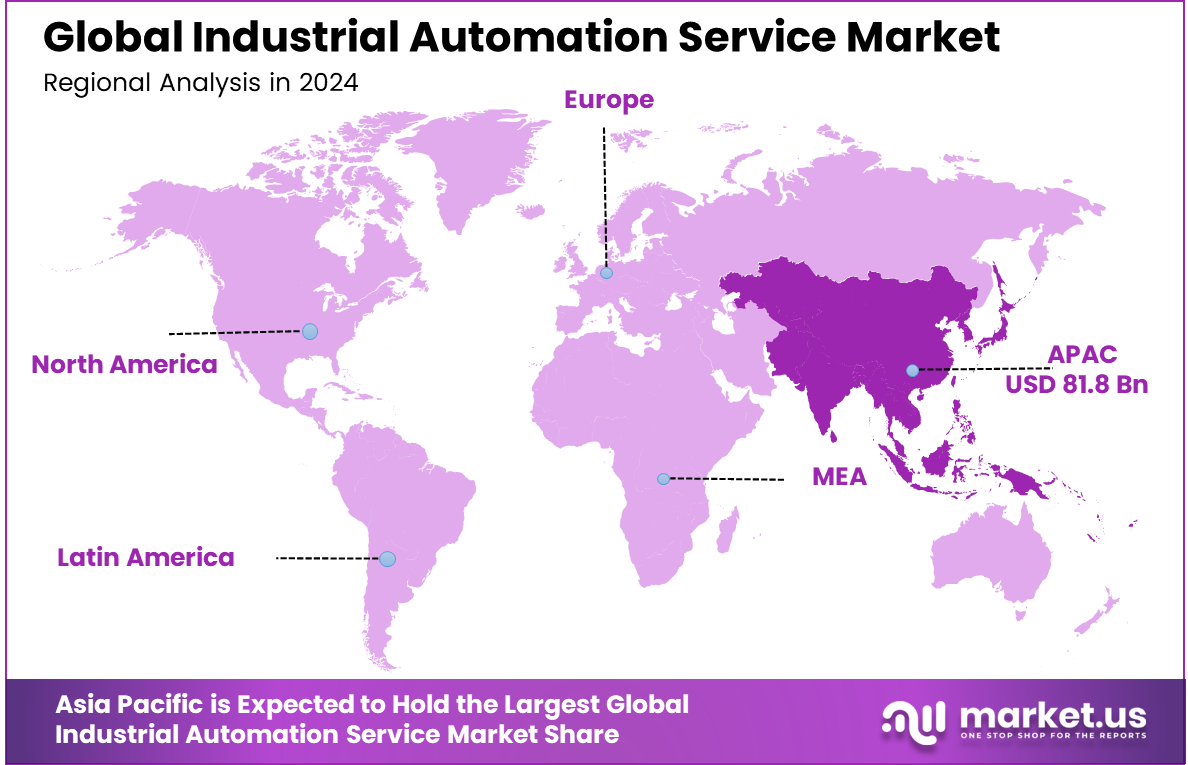

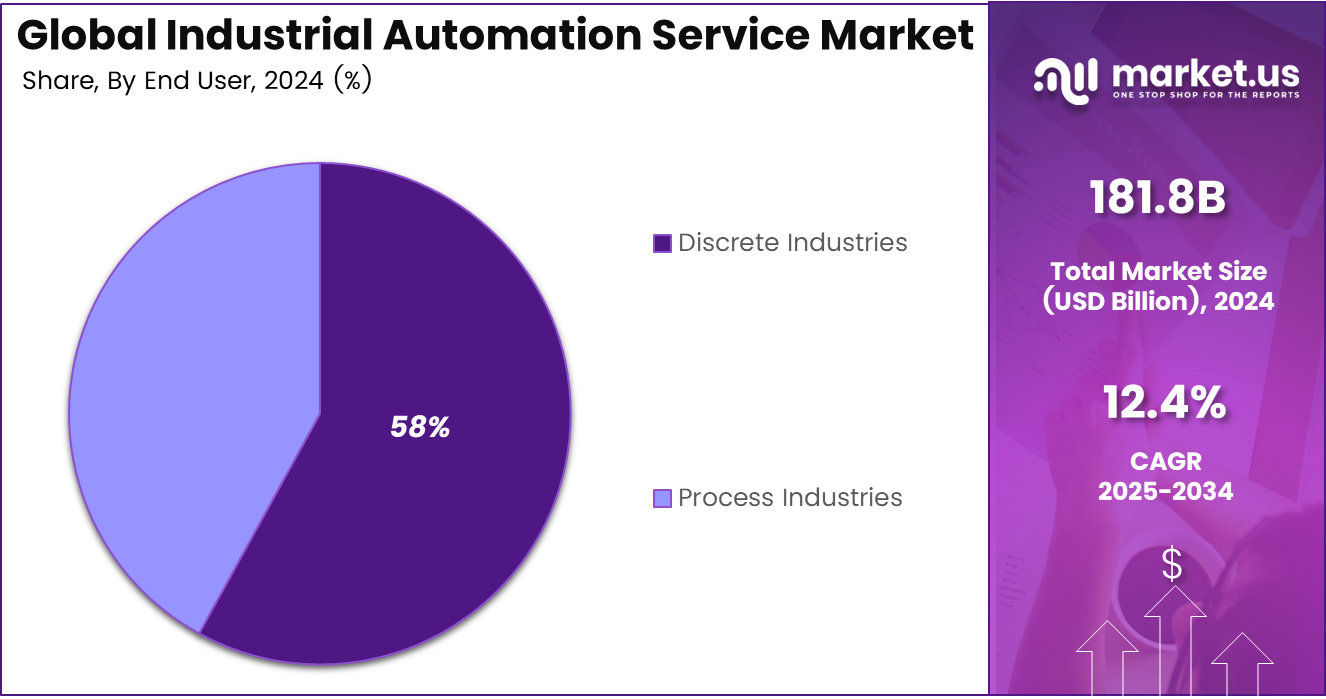

The Global Industrial Automation Service Market size is expected to be worth around USD 585.1 billion by 2034, from USD 181.8 billion in 2024, growing at a CAGR of 12.4% during the forecast period from 2025 to 2034. Asia Pacific held a dominant market position, capturing more than a 45% share, holding USD 81.8 billion in revenue.

The market for industrial automation services is driven by the increasing adoption of Industry 4.0 technologies, including IoT, artificial intelligence (AI), machine learning, and big data analytics. These advancements enable real-time monitoring, predictive maintenance, and data-driven decision-making, significantly improving operational efficiency.

Additionally, the growing need for higher productivity, cost reduction, and improved safety standards is pushing industries toward automation solutions. As manufacturers seek to stay competitive, the demand for integrated automation systems and services to streamline processes, reduce downtime, and enhance productivity is rapidly expanding across various sectors.

For instance, in April 2025, Rockwell Automation and AWS announced a collaboration to transform manufacturing through advanced industrial automation solutions at Hannover Messe. By combining Rockwell’s automation expertise with AWS’s cloud and AI technologies, the partnership aims to enhance operational efficiency, enable real-time insights, and optimize manufacturing processes.

Scope and Forecast

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 181.8 Billion |

| Forecast Revenue (2034) | USD 585.1 Billion |

| CAGR (2025-2034) | 12.4% |

| Largest market in 2024 | North America [38% market share] |

Key Takeaway

- In 2024, the Project Engineering and Installation segment held a dominant market position, capturing a 40% share of the Global Industrial Automation Service Market.

- In 2024, the Programmable Logic Controller (PLC) segment held a dominant market position, capturing a 25% share of the Global Industrial Automation Service Market.

- In 2024, the Discrete Industries segment held a dominant market position, capturing a 58% share of the Global Industrial Automation Service Market.

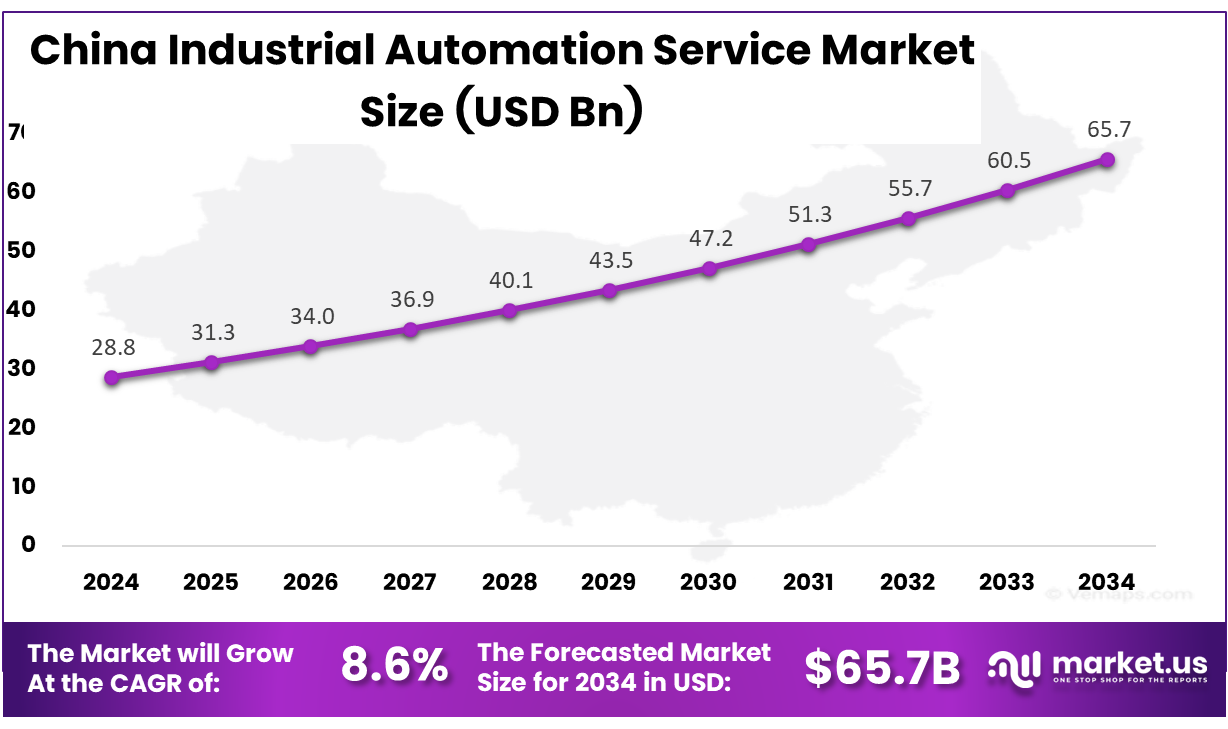

- The China Industrial Automation Service Market was valued at USD 28.8 billion in 2024, with a robust CAGR of 8.6%.

- In 2024, the Asia Pacific held a dominant market position in the Global Industrial Automation Service Market, capturing more than a 45% share.

Regional Analysis

In 2024, the Asia Pacific held a dominant market position in the Global Industrial Automation Service Market, capturing more than a 45% share, holding USD 81.8 billion in revenue. This dominance is due to the rapid industrialization and the growing adoption of advanced technologies like AI, IoT, and robotics. Government initiatives, such as China’s “Made-in-China 2025” and India’s Production-Linked Incentive schemes, are promoting digitalization and smart manufacturing. The region’s rising labor costs, along with a strong emphasis on operational efficiency and workplace safety, are further accelerating automation investments. Key markets, including China, India, Japan, and South Korea, benefit from expanding industries like automotive, electronics, and pharmaceuticals.

For instance, in December 2024, Schaeffler AG acquired Indian engineering and service provider Dhruva for smart automation, further strengthening its presence in the Asia-Pacific industrial automation service market. This acquisition highlights the region’s growing dominance in industrial automation, driven by increasing demand for advanced automation solutions in manufacturing.

China Industrial Automation Service Market Size

The market for Industrial Automation Service within China is growing tremendously and is currently valued at USD 28.8 billion. The market has a projected CAGR of 8.6%. The market is growing tremendously due to the country’s focus on enhancing manufacturing efficiency and embracing Industry 4.0 technologies. China’s manufacturing sector is undergoing digital transformation, driven by the adoption of IoT, AI, and robotics to improve productivity, reduce labor costs, and maintain competitiveness. Additionally, government initiatives promoting smart manufacturing, alongside rising labor costs and a shortage of skilled workers, are accelerating the demand for automation services.

For instance, in July 2025, the China-Africa Expo showcased leading innovations in coffee robotics and beverage automation, highlighting China’s growing dominance in industrial automation services. Chinese companies are at the forefront of developing advanced robotics and automation technologies, which are transforming sectors like food and beverage. This reflects China’s expanding influence in global industrial automation, particularly through advancements in robotics and smart manufacturing.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Service Type Analysis

In 2024, the Project Engineering and Installation segment held a dominant market position, capturing a 40% share of the Global Industrial Automation Service Market. This dominance is due to the increasing complexity of automation systems, which require specialized engineering and seamless installation to integrate advanced technologies like AI, robotics, and IoT.

The demand for end-to-end services, including system design, customization, installation, and commissioning, is rising as industries seek tailored solutions to optimize operations. Additionally, the focus on minimizing downtime and ensuring regulatory compliance during rollouts further boosts reliance on expert engineering services. As a result, this segment is crucial in enabling industries to transition to automated and digitized operations.

For instance, in October 2024, Vanderlande expanded its flexible automation offering by partnering with Hai Robotics to enhance material handling and logistics systems. The collaboration integrates Hai Robotics’ robotic solutions with Vanderlande’s Project Engineering and Installation services, addressing the rising demand for specialized automation services. This partnership aims to improve operational efficiency, reduce downtime, and support the seamless implementation of advanced automation technologies.

Product Type Analysis

In 2024, the Programmable Logic Controller (PLC) segment held a dominant market position, capturing a 25% share of the Global Industrial Automation Service Market. The demand has been primarily driven by the need for reliable, flexible, and scalable automation solutions in manufacturing. PLCs are essential for controlling complex machinery, enhancing precision, efficiency, and integrating with technologies like robotics and IoT. Their adoption across industries such as automotive, pharmaceuticals, and food processing continues to grow. Additionally, the rise of Industry 4.0 and smart factory initiatives has further fueled the demand for advanced PLC systems that enable seamless connectivity with IoT devices and cloud platforms.

For instance, in November 2024, Divcon Controls became a Rockwell Automation “Best-in-Class” partner, enhancing its position in the industrial automation service market. The partnership emphasizes Divcon’s expertise in advanced programmable logic controller (PLC) solutions, improving system integration and automation processes. By leveraging Rockwell’s technologies, Divcon aims to deliver high-performance PLC systems that boost manufacturing efficiency, reduce downtime, and meet the increasing demand for scalable automation solutions across industries.

End-User Analysis

In 2024, the Discrete Industries segment held a dominant market position, capturing a 58% share of the Global Industrial Automation Service Market. This dominance is due to the widespread adoption of automation technologies across sectors like automotive, electronics, consumer goods, and aerospace. The demand for precise, high-speed, and flexible manufacturing processes that can manage complex product variations and high production volumes is key.

Automation services enhance product quality, reduce cycle times, and improve efficiency while enabling customization and quick changeovers. Additionally, growing investments in Industry 4.0 technologies, such as robotics, AI, and IoT, further support smarter manufacturing and strengthen the segment’s market position.

For instance, in May 2024, Belden launched new solutions for discrete manufacturing, enhancing its industrial automation services. These solutions focus on improving connectivity, data integration, and system reliability, essential for automating processes in industries like automotive, electronics, and consumer goods. Belden’s technologies enable seamless device communication, boosting efficiency, flexibility, and productivity.

Key Market Segments

By Service Type

- Project Engineering and Installation

- Maintenance and Support Services

- Consulting Services

- Operational Services

By Product Type

- Programmable Logic Controller (PLC)

- Supervisory Control & Data Acquisition (SCADA)

- Distributed Control System (DCS)

- Manufacturing Execution System (MES)

- Management (PLM)

- Functional Safety

- Plant Asset Management (PAM)

- Others

By End-User

- Discrete Industries

- Process Industries

Latest Trends

Cobots are the latest and most advanced forms of industrial automation that combine safety and productivity with human workers, revolutionizing the industry. Unlike traditional industrial robots, cobots are designed to interact with humans safely and can be used for tasks such as assembly, quality control, packaging, and more. Small and medium-sized businesses find cobots highly attractive due to their affordability, ease of integration, and adaptability. With the increasing use of cobots in various industries, they can enhance efficiency while minimizing risks associated with repetitive and manual tasks.

For instance, in April 2025, Omron established a dedicated robotics organization aimed at enhancing its response time to the growing demand for collaborative robots (cobots) in industrial automation. This move underscores Omron’s commitment to advancing cobot technology, which is increasingly used in industries such as automotive, electronics, and consumer goods.

Market Dynamics

Drivers - Industry 4.0 Technologies Adoption

Industrial automation services are experiencing a surge in demand due to the convergence of Industry 4.0 technologies, such as IoT, artificial intelligence, machine learning, big data analytics, and smart factory solutions. These technologies enable real-time monitoring, data-driven decision-making, and predictive maintenance, which leads to increased operational efficiency and reduced downtime. As industries increasingly adopt these advanced systems, the need for robust automation services becomes essential, accelerating the transformation of manufacturing operations into more intelligent and automated processes.

For instance, in April 2024, Schneider Electric showcased its software and electrification solutions, driving Industry 4.0 adoption. By integrating IoT, AI, and cloud computing into industrial automation services, the company is advancing digital transformation. These technologies enable real-time monitoring, predictive maintenance, and data-driven decisions, enhancing efficiency and reducing costs.

Restraint - High Initial Investment

The high initial cost of implementing industrial automation technologies is a major restraint, particularly for small and medium-sized enterprises (SMEs). The substantial capital investment required for automation infrastructure, software, and system integration may deter businesses from adopting these solutions. Although automation may provide savings over time, it can be too expensive at the beginning, making it difficult for smaller companies with limited budgets to implement and maintain its adoption in a rapidly changing industrial environment.

Opportunities - Expansion into Emerging Markets

Industrial automation service providers are likely to experience significant growth in emerging markets, particularly those in the Asia-Pacific, Latin America, and Africa. The adoption of automation technologies is rapidly expanding in these regions to improve manufacturing efficiency, increase productivity, and compete globally. The increased emphasis on modernization, combined with the availability of better digital infrastructure, creates an ideal environment for automation services. These markets offer opportunities for organizations to capitalize on the growing demand for automation solutions, which can lead to long-term growth in untapped markets.

For instance, in March 2025, Schneider Electric announced plans to strengthen its presence in South Africa’s industrial automation space as part of its broader strategy to expand into emerging markets. The company aims to leverage its advanced automation solutions to enhance operational efficiency, sustainability, and digital transformation for businesses in South Africa and across the African continent.

Challenges - Regulatory Compliance

Navigating complex regulatory compliance requirements is a significant challenge for automation service providers. Industries must adhere to stringent safety, data privacy, and environmental regulations, which can vary widely across regions. Ensuring that automation systems meet these industry-specific standards requires significant investment in compliance management and regular updates. To mitigate risks, prevent legal complications, and ensure the secure, responsible, sustainable deployment of automation technologies, providers must remain flexible to changing regulations, particularly in sectors under intense regulatory scrutiny.

For instance, in July 2025, a report highlighted how professional services automation (PSA) is improving compliance and billing accuracy in U.S. healthcare, a trend also affecting industrial automation services. As industries face complex regulatory standards, automation technologies are being integrated to ensure compliance with safety, data privacy, and environmental regulations.

Key Players Analysis

One of the leading players in the market, in November 2024, Rockwell Automation and Microsoft announced a collaboration to accelerate industrial transformation through advanced automation technologies. This partnership aims to integrate Rockwell’s industrial automation solutions with Microsoft’s cloud and AI capabilities, offering businesses enhanced data analytics, predictive maintenance, and real-time insights. By combining Rockwell’s expertise in automation with Microsoft’s cloud and AI technologies, the two companies are enabling more efficient, scalable, and intelligent manufacturing processes. This collaboration underscores the growing trend of digitalization in industrial sectors, driving innovation and improving operational efficiency across industries.

Top Key Players in the Market

- Siemens AG

- ABB Ltd.

- Johnson Controls Inc.

- Schneider Electric SE

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Yokogawa Electric

- Rockwell Automation Inc.

- Ametek Inc.

- Advantech Co., Ltd.

- Dwyer Instruments LLC

- Emerson Electric Co.

- FANUC Bulgaria EOOD

- Fuji Electric Co., Ltd.

- General Electric Co.

- Hitachi Ltd.

- Other Key Players

Recent Developments

- In May 2025, Mouser Electronics announced that it would showcase its latest industrial automation solutions at the Automate 2025 event. The company plans to highlight its advanced components and systems that support automation in various industries, including robotics, machine vision, and smart manufacturing.

- In August 2024, Siemens, Schneider Electric, and Honeywell were recognized as leaders in ABI Research’s competitive ranking of energy management system vendors. These companies are at the forefront of the industrial automation service market, providing advanced solutions that integrate energy management with automation technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 181.8 Billion |

| Forecast Revenue (2034) | USD 585.1 Billion |

| CAGR (2025-2034) | 12.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Project Engineering and Installation, Maintenance and Support Services, Consulting Services, Operational Services), By Product Type (Programmable Logic Controller (PLC), Supervisory Control & Data Acquisition (SCADA), Distributed Control System (DCS), Manufacturing Execution System (MES), Management (PLM), Functional Safety, Plant Asset Management (PAM), Others), By End-User (Discrete Industries, Process Industries) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Siemens AG, ABB Ltd., Johnson Controls Inc., Schneider Electric SE, General Electric Company, Honeywell International Inc., Mitsubishi Electric Corporation, Yokogawa Electric, Rockwell Automation Inc., Ametek Inc., Advantech Co. Ltd., Dwyer Instruments LLC, Emerson Electric Co., FANUC Bulgaria EOOD, Fuji Electric Co. Ltd., General Electric Co., Hitachi Ltd., Other Key Players |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |