Quick Navigation

Report Overview

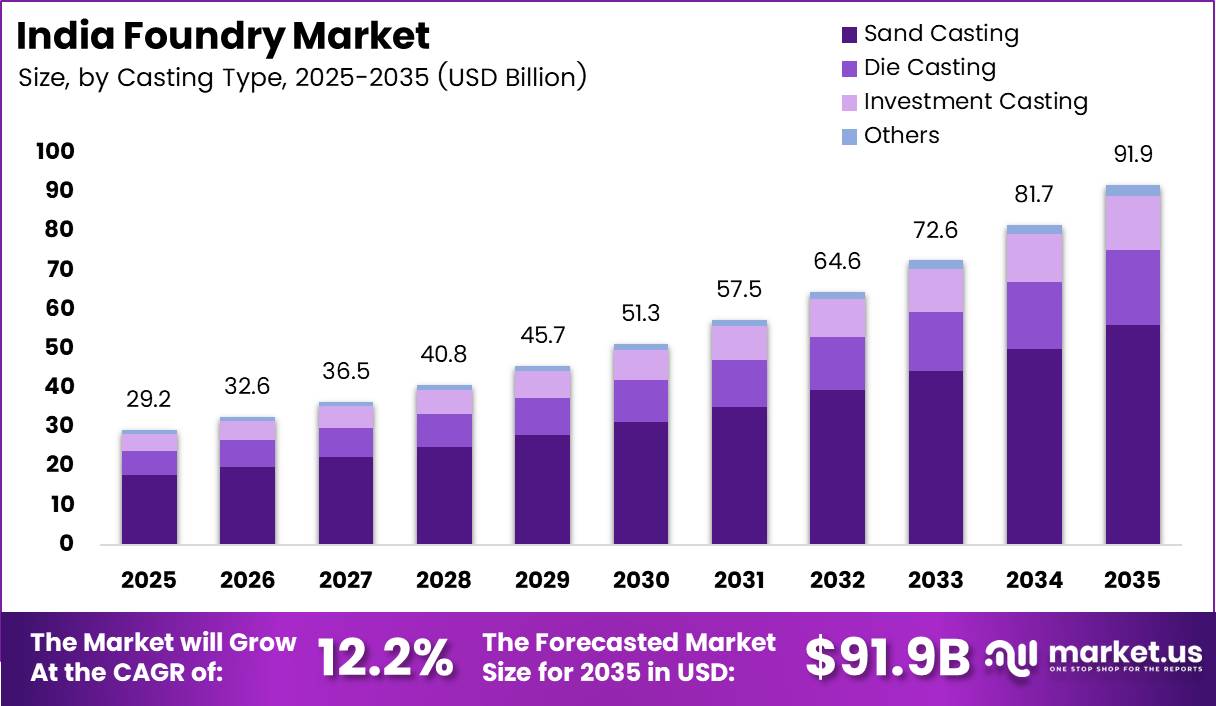

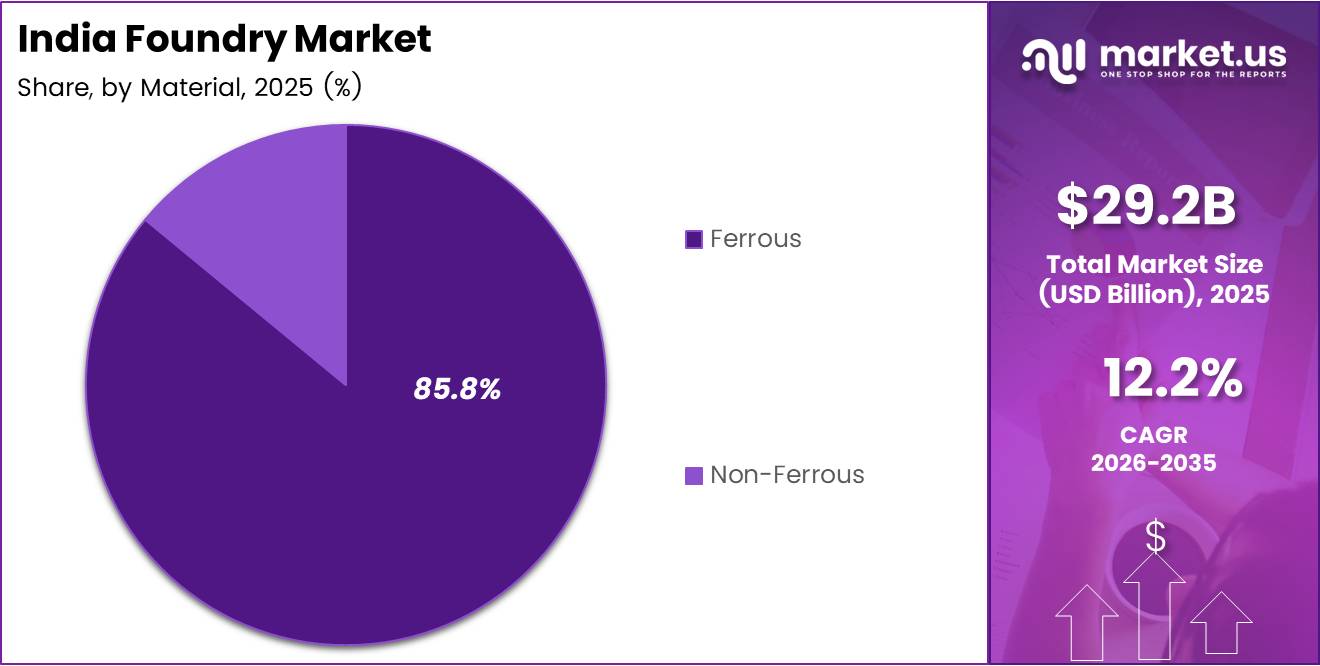

India Foundry Market size is expected to be worth around USD 91.9 Billion by 2035 from USD 29.2 Billion in 2025, growing at a CAGR of 12.2% during the forecast period 2026 to 2035.

India’s foundry sector holds a structurally strong position in global manufacturing. The country operates one of the largest casting production networks in the world, supplying cast components across automotive, infrastructure, railways, and heavy engineering industries. This industrial depth makes India a critical node in global OEM supply chains.

The automotive industry anchors demand for cast components in India. Vehicle manufacturers require grey iron, ductile iron, and aluminium castings for engine blocks, brake drums, and suspension parts. As domestic vehicle production scales and electric vehicle platforms expand, foundries face both volume pressure and a shift in material specifications toward lightweight alloys.

Government manufacturing policies directly support foundry sector expansion. Initiatives such as Production Linked Incentive schemes and infrastructure spending programs create consistent downstream demand for cast components. Railways, power generation, and construction segments benefit from public capital expenditure, giving foundries a stable order pipeline beyond private sector cycles.

Export competitiveness adds another structural advantage. India’s cost base, skilled workforce, and established casting infrastructure allow domestic producers to compete with European and East Asian foundries on precision and price. Global OEMs actively seek Indian casting suppliers as part of supply chain diversification strategies following recent disruptions.

According to the Institute of Indian Foundrymen (IIF), India has approximately 5,000 foundry units, of which 90% are small and medium enterprises. This SME concentration means the sector’s aggregate capacity is distributed across a fragmented base. Fragmentation limits individual unit scale but creates flexibility for buyers seeking specialized or lower-volume casting contracts.

According to the IIF, India’s casting production reached approximately 15.16 million metric tonnes in 2023-24, a 7% increase from the prior year, maintaining India’s rank as the world’s second-largest casting producer. This output volume confirms that India’s foundry infrastructure is not aspirational. It is already operating at industrial scale and competing directly with established casting nations.

Key Takeaways

- The India Foundry Market is valued at USD 29.2 Billion in 2025 and will reach USD 91.9 Billion by 2035.

- The market grows at a CAGR of 12.2% from 2026 to 2035.

- Sand Casting holds the dominant casting type share at 61.2% in 2025.

- Ferrous materials lead the material segment with an 85.8% share in 2025.

- Automotive is the largest end-user segment, capturing 34.6% of the market in 2025.

- India operates approximately 5,000 foundry units, with 90% classified as SMEs.

- India’s casting exports crossed USD 4 billion for the first time in 2023-24, reaching USD 4.11 Billion.

- North America holds the leading regional share in export demand for Indian castings.

Casting Type Analysis

Sand Casting dominates with 61.2% due to low tooling cost and broad application fit.

In 2025, Sand Casting held a dominant market position in the By Casting Type segment of the India Foundry Market, with a 61.2% share. Sand casting suits high-volume, low-complexity components that form the bulk of India’s automotive and infrastructure output. Its tooling economics make it the default process for SME foundries operating at mid-scale volumes.

Die Casting serves manufacturers requiring tight dimensional tolerances and smooth surface finishes. Automotive OEMs and electrical equipment producers increasingly specify die-cast aluminium and zinc parts. However, high capital investment in dies limits this process to larger foundry operators with stable order volumes and longer production runs.

Investment Casting addresses requirements where complexity and precision matter more than unit volume. Aerospace, defence, and pump manufacturers use investment casting for turbine blades, valve bodies, and impellers. This sub-segment carries higher per-unit value and attracts foundries seeking to exit commodity casting competition.

The Others category includes processes such as shell moulding, centrifugal casting, and continuous casting. These serve niche industrial applications and specialty alloy components. Their combined share remains modest, but niche process capabilities allow foundries to command pricing premiums unavailable in standard sand or die casting.

Material Analysis

Ferrous dominates with 85.8% due to cost advantage and established supply chains.

In 2025, Ferrous materials held a dominant market position in the By Material segment of the India Foundry Market, with an 85.8% share. According to the Institute of Indian Foundrymen (IIF), grey iron castings alone account for approximately 68% of total castings produced in India. This concentration reflects the automotive and machinery sectors’ preference for proven, cost-efficient ferrous alloys in high-volume applications.

Non-Ferrous castings represent a structurally smaller but strategically important segment. Aluminium, copper, and zinc alloys serve automotive lightweighting, electrical components, and precision engineering. Rising EV platform adoption is shifting specifications toward aluminium castings, creating a gradual but measurable rebalancing between ferrous and non-ferrous volumes over the forecast period.

End-User Analysis

Automotive dominates with 34.6% due to high-volume casting requirements across powertrain and chassis components.

In 2025, Automotive held a dominant market position in the By End-User segment of the India Foundry Market, with a 34.6% share. According to the IIF, the automotive sector consumes 32% of total castings nationally, covering engine blocks, brake assemblies, gearbox housings, and suspension arms. This off-take concentration makes automotive OEM production cycles a direct leading indicator for foundry capacity utilization.

Aerospace demands the highest precision standards among all end-user segments. Indian foundries supplying aerospace parts must meet stringent international quality certifications. Entry barriers are high, but so are margins. Foundries that secure aerospace approvals diversify their revenue away from cyclical automotive demand.

Construction relies on castings for structural fittings, drainage systems, and architectural hardware. Public infrastructure spending programs create predictable order flows. However, construction castings are largely commodity products, keeping margins thin and making this segment volume-sensitive rather than value-driven.

Machinery manufacturers consume castings for gear housings, pump casings, and machine frames across agricultural and industrial equipment. This segment sustains consistent base-load demand for mid-complexity grey iron and ductile iron castings, providing foundries with a reliable volume buffer independent of automotive cycles.

Railways represent a long-cycle procurement segment driven by government capital expenditure. Indian Railways’ modernization and network expansion programs generate durable demand for brake components, bogie frames, and coupling assemblies. Foundries with railway approvals benefit from long-term supply agreements and reduced customer concentration risk.

Power Generation requires castings for turbine casings, generator frames, and heat exchanger components. Thermal, hydro, and renewable energy infrastructure all consume cast parts at various project stages. Grid expansion plans and industrial energy investments sustain steady procurement activity in this segment.

Pumps and Valves constitute a specialized sub-segment demanding corrosion-resistant alloys and pressure-rated designs. Water infrastructure, oil and gas, and chemical processing industries drive volumes here. Export demand from Europe and the Middle East for Indian pump castings adds a trade dimension to this segment’s revenue potential.

Electrical Components require castings for transformer housings, switchgear enclosures, and motor frames. Domestic electrification programs and industrial power upgrades generate base demand. The transition to renewable energy also introduces new casting specifications for wind turbine hubs and solar mounting hardware.

The Others category captures castings for defence, marine, and consumer appliance applications. While individually smaller, these end-users often seek custom alloy specifications and low-to-medium annual volumes, creating margin opportunities for foundries with flexible production capability.

Key Market Segments

By Casting Type

- Sand Casting

- Die Casting

- Investment Casting

- Others

By Material

- Ferrous

- Non-Ferrous

By End-User

- Automotive

- Aerospace

- Construction

- Machinery

- Railways

- Power Generation

- Pumps & Valves

- Electrical Components

- Others

Drivers

Automotive and Infrastructure Expansion Creates Sustained Casting Demand Across India’s Foundry Base

India’s vehicle production growth generates the largest single block of casting demand in the country. Passenger vehicles, commercial trucks, and two-wheelers all require grey iron and aluminium castings throughout their powertrain and chassis assemblies. As domestic vehicle sales rise and OEM capacity expansions proceed, foundries receive longer order horizons and more stable capacity utilization.

Government manufacturing initiatives strengthen this demand further. Production Linked Incentive programs for automotive and engineering sectors directly translate into additional casting contracts for domestic foundries. Public infrastructure spending on roads, bridges, and urban utilities creates parallel demand for structural and drainage castings. These two demand streams reinforce each other through the forecast period.

Technology adoption adds a third driver layer. According to a 2026 peer-reviewed study, AI adoption in India’s foundry and industrial sector stands at approximately 28%. This low penetration rate signals a large base of foundries still operating below their efficiency ceiling. Foundries that adopt process monitoring, predictive maintenance, and AI-assisted quality control will gain measurable cost and yield advantages over peers, accelerating the competitive gap between early adopters and laggards.

Restraints

High Energy Costs and Environmental Compliance Pressures Constrain SME Foundry Profitability

Energy expenditure represents one of the largest variable costs in foundry operations. Melting furnaces, heat treatment, and ventilation systems consume significant electricity and fuel volumes. For SME foundries operating on thin margins, rising industrial power tariffs reduce profitability per tonne cast without a corresponding ability to pass costs through to established OEM customers on long-term contracts.

Environmental compliance compounds this cost pressure. Regulators require foundries to install emission control systems, manage waste sand disposal, and document environmental performance. For small units, capital investment in compliance infrastructure competes directly with investment in productive capacity. Larger foundries absorb these costs more easily, widening the competitive gap.

Technology integration creates a third structural constraint. According to a 2026 peer-reviewed study, 34% of Indian factories report difficulty integrating their systems, and 35% are not fully using available automation in their operations. For foundries, this means productivity gains from modern equipment remain partially unrealized. The investment case for automation is clear, but integration complexity slows adoption and delays the productivity benefit.

Growth Factors

Export Growth and EV-Driven Casting Demand Open New Revenue Streams for Indian Foundries

India’s export performance confirms that its foundry sector competes on a global basis, not just domestically. According to the Institute of Indian Foundrymen (IIF), casting exports reached USD 4.11 Billion in 2023-24, a 4.47% increase year-on-year, crossing the USD 4 billion threshold for the first time. The three-year CAGR of 12.84% since 2020-21 shows that global buyers are actively increasing their India-sourced casting volumes, not just testing suppliers.

In July 2025, Vedanta Aluminium expanded its Primary Foundry Alloy capacity by 120 KTPA at Jharsuguda to support automotive and engineering casting manufacturers. This upstream capacity addition directly improves material availability for non-ferrous foundries. Reliable aluminium alloy supply at scale allows casting producers to commit to larger OEM contracts without raw material risk.

Electric vehicle manufacturing creates a structurally new demand category for Indian foundries. EV platforms replace cast iron powertrain components with aluminium structural castings, battery housings, and motor frames. Foundries that develop EV-specific alloy and process capabilities position themselves for a segment where domestic production is still in early stages and import substitution is actively encouraged by policy.

Emerging Trends

Smart Foundry Technologies and Green Manufacturing Practices Redefine Operational Standards

Real-time process monitoring systems are entering Indian foundries at an accelerating pace. Sensors tracking melt temperature, mould fill rates, and solidification profiles allow operators to detect defects before they reach final inspection. This shift from reactive to predictive quality control reduces scrap rates and rework costs, directly improving per-tonne margins for adopting units.

Simulation software for mould design is changing how foundries approach new component development. Virtual casting trials reduce the physical iteration cycles needed before a component achieves dimensional compliance. Shorter development timelines make Indian foundries more competitive when bidding on new OEM platforms where speed-to-sample is a selection criterion alongside price.

According to the Institute of Indian Foundrymen (IIF), the foundry sector employs 2.0 million people, including 0.5 million direct employees, with the potential to generate an additional 2.0 million jobs over the next decade. Foundries investing in green technologies and energy-efficient furnaces do more than reduce emissions. They improve their eligibility for government incentives, qualify for export contracts with ESG requirements, and reduce operational exposure to rising energy tariffs simultaneously.

Key Company Insights

Aditya Birla Management Corp. operates within one of India’s largest diversified industrial conglomerates, giving its foundry and metals businesses access to integrated raw material sourcing and pan-India distribution. This vertical integration reduces input cost volatility. For OEM customers evaluating supply security, this group backing offers a procurement risk profile that standalone foundries cannot match.

Brakes India occupies a specialized position within the automotive casting supply chain, focusing on brake system components for passenger and commercial vehicles. Its deep OEM relationships with leading vehicle manufacturers create a captive demand base. As India’s vehicle production scales and safety regulations tighten, Brakes India’s component-specific expertise becomes a barrier to new entrant competition.

Larsen and Toubro brings engineering project execution scale to the foundry and heavy casting segment. Its ability to supply large, complex cast components for infrastructure, defence, and power generation gives it access to high-value, long-cycle government contracts. In August 2025, Foseco India signed a definitive agreement to acquire a 75% stake in Morganite Crucible (India) Limited, signaling that foundry supply chain consolidation is accelerating across the sector.

JSW Steel anchors its foundry-related operations within an integrated steel manufacturing platform. Access to captive raw materials and a large domestic steel customer base provides structural cost advantages. As ferrous castings maintain an 85.8% material share in India’s foundry output, JSW Steel’s upstream integration positions it to benefit directly from any volume expansion across the sector’s largest material category.

Key Players

- Aditya Birla Management Corp.

- Brakes India

- Larsen & Toubro

- JSW Steel

- CALMET

- Ashok Iron Works

- Gujarat Metal Cast Industries

- Electrosteel Castings

- Menon & Menon

- Kirloskar Ferrous Industries

Recent Developments

- December 2025 – Jaya Hind Industries announced a ₹200 crore investment to expand aluminium die-casting capacity at its Chennai facility, targeting automotive and engineering casting customers requiring lightweight non-ferrous components.

- February 2026 – Tube Investments of India acquired an 87% stake in Orange Koi to enter the metal injection molding and precision metal components segment, broadening its manufacturing scope beyond conventional casting operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 29.2 Billion |

| Forecast Revenue (2035) | USD 91.9 Billion |

| CAGR (2026-2035) | 12.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Casting Type (Sand Casting, Die Casting, Investment Casting, Others), By Material (Ferrous, Non-Ferrous), By End-User (Automotive, Aerospace, Construction, Machinery, Railways, Power Generation, Pumps and Valves, Electrical Components, Others) |

| Competitive Landscape | Aditya Birla Management Corp., Brakes India, Larsen & Toubro, JSW Steel, CALMET, Ashok Iron Works, Gujarat Metal Cast Industries, Electrosteel Castings, Menon & Menon, Kirloskar Ferrous Industries |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |