Global Hot-Melt Self-Adhesive Labels Market By Adhesive Types (Acrylic-based Adhesive, Rubber-based Adhesive, and Others), By Release Liner Type (Silicone and Non-silicone), By Surface Substrate (Paper-based and Film-based), By Application (Commercial, Industrial, and Residential), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 180168

- Number of Pages: 198

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

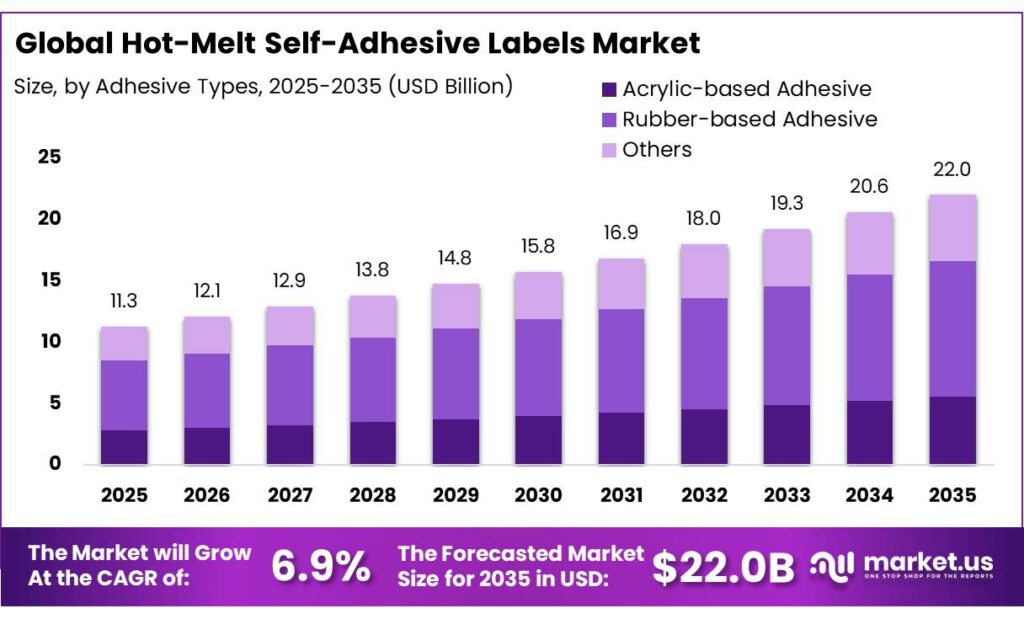

The Global Hot-Melt Self-Adhesive Labels Market is expected to be worth around USD 22.0 Billion by 2035, up from USD 11.3 Billion in 2025, at a CAGR of 6.9% from 2026 to 2035. The North America segment maintained 39.2%, supporting a Alcohol-Based Disinfectants value of USD 1.2 Bn.

The hot‑melt self‑adhesive labels market is characterized by widespread adoption in industrial and packaging applications, driven by performance, regulatory, and operational considerations. These labels are predominantly applied to paper-based substrates, which offer higher surface energy and porosity, ensuring reliable adhesion without pre-treatment, while film substrates require specialized processing. Rubber-based adhesives dominate due to high initial tack, rapid bonding, and conformability, whereas silicone release liners are favored for their low surface energy, predictable release force, and thermal stability.

The food, beverage, and personal care sectors constitute primary end-use segments, with regulatory compliance, such as PFAS-free formulations and food contact approvals, shaping material and adhesive selection. Industrial users leverage hot-melt labels for high-speed automated production, durability under thermal and mechanical stress, and compatibility with diverse substrates.

Strategic manufacturer focus includes sustainability, recyclable liners, digital integration, and high-performance chemistries to maintain technical differentiation. Geopolitical factors influence raw material availability, particularly petrochemical feedstocks, affecting production and operational planning.

Key Takeaways:

- The global hot-melt self-adhesive labels market was valued at USD 11.3 billion in 2025.

- The global hot-melt self-adhesive labels market is projected to grow at a CAGR of 6.9% and is estimated to reach USD 22.0 billion by 2035.

- On the basis of types of adhesives, rubber-based adhesives dominated the market, constituting 50.1% of the total market share.

- Based on the release liner type, silicone dominated the market, with a market share of around 85.7%.

- Based on the surface substrate, paper-based substrates led the market, comprising 64.2% of the total market.

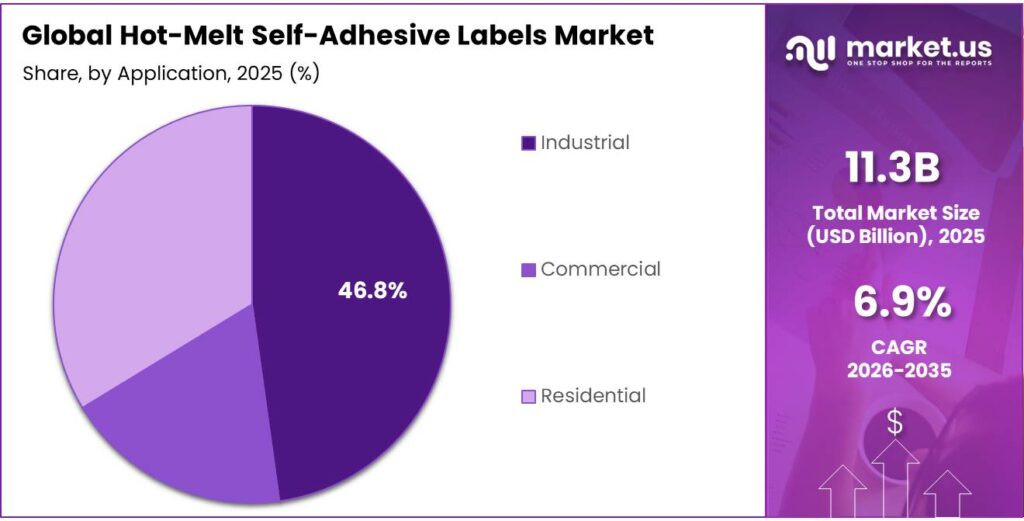

- Among the applications of hot-melt self-adhesive labels, the industrial sector held a major share in the market, 46.8% of the market share.

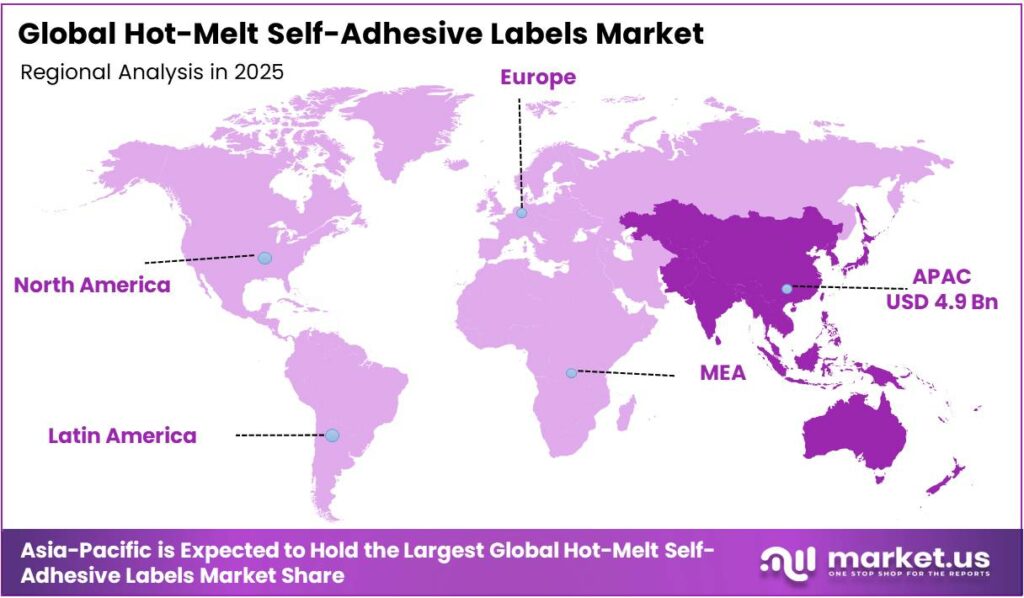

- In 2025, the Asia Pacific was the most dominant region in the hot-melt self-adhesive labels market, accounting for 43.2% of the total global consumption.

Adhesive Types Analysis

Rubber-based Adhesive Labels Are a Prominent Segment in the Market.

The hot-melt self-adhesive labels market is segmented based on adhesive types into acrylic-based adhesive, rubber-based adhesive, and others. The rubber-based adhesive labels led the market, comprising 50.1% of the market share, due to their intrinsic material and performance characteristics relative to acrylic alternatives. They provide high initial tack and rapid bond formation on contact, enabling labels to adhere quickly with minimal pressure, an important attribute for high-speed application lines and bonding to varied substrates. In addition, their soft, conformable formulation allows the adhesive to flow into surface irregularities, enhancing immediate attachment where surface smoothness is limited.

Similarly, rubber adhesives are relatively economical to formulate, contributing to broad use in everyday packaging and food-grade label stock where extreme environmental resistance is not required. By contrast, acrylic-based adhesives, which exhibit superior resistance to UV exposure, high temperatures, oxidation, and long-term aging, generally have lower initial tack and develop full adhesion over longer dwell times.

Release Liner Type Analysis

Silicone Release Liner Dominated the Market.

On the basis of release liner type, the hot-melt self-adhesive labels market is segmented into silicone and non-silicone. The silicone release liner dominated the market, comprising 85.7% of the market share, as they consistently provide highly controlled release performance that aligns with the technical demands of pressure-sensitive adhesive systems. The cured silicone (often polydimethylsiloxane) exhibits very low surface energy and low friction, which enables easy delamination and predictable release force between the liner and adhesive, reducing the risk of label distortion or adhesive transfer during peeling.

Additionally, silicone coatings offer thermal stability across a wide temperature range and chemical compatibility with a broad spectrum of adhesive chemistries, allowing converters to tune release characteristics for diverse substrates and production speeds. In contrast, many non-silicone liners may not deliver equivalent low release force or consistent performance across varied adhesive systems, which can complicate high-speed converting and automated applying processes.

Surface Substrate Analysis

The Hot-Melt Self-Adhesive Labels Industry is Mostly Utilized on Paper-based Substrate.

Based on the surface substrate, the hot-melt self-adhesive labels market is divided into paper-based and film-based. Paper-based substrate consumers dominated the hot-melt self-adhesive labels market, with a notable market share of 64.2%, as paper inherently offers physical and processing advantages that align with the demands of traditional labeling operations.

Paper face stock exhibits higher surface energy and porosity, which supports reliable wetting and anchorage of hot-melt pressure-sensitive adhesives without requiring surface treatments, often necessary for low-energy plastics. Furthermore, paper is readily printable and easy to die-cut and convert, facilitating complex shapes and fine detail common in packaging labels, and can be produced in a variety of coated and uncoated finishes that support high-resolution graphics. While film substrates deliver enhanced moisture resistance and flexibility, they typically require higher-performance adhesives or pre-treatments to achieve equivalent bond reliability, and their lower surface energy challenges adhesion without specialized processing.

Application Analysis

The Industrial Sector Held a Major Share of the Hot-Melt Self-Adhesive Labels Market.

Among the applications, 46.8% of the total global consumption of hot-melt self-adhesive labels is in the industrial sector, as their performance characteristics and application environments align with industrial operational requirements more than typical commercial or residential uses. Industrial labeling often demands high‑speed application, consistent adhesion under variable temperatures and substrates, and durability through handling, storage, and transportation, conditions for which hot‑melt pressure‑sensitive adhesives are formulated. Their rapid bond formation and strong initial tack support automated production lines common in manufacturing, logistics, and warehousing.

In contrast, commercial and residential labeling generally involves lower application speeds, simpler substrates, and less stringent durability needs, effectively served by standard pressure‑sensitive labels with room‑temperature adhesives or removable systems. Additionally, industrial users require labels that resist moisture, abrasion, and thermal cycling over product lifecycles, attributes engineered into hot‑melt adhesives, whereas residential and most commercial applications seldom demand that level of robustness.

Key Market Segments

By Adhesive Types

- Acrylic-based Adhesive

- Rubber-based Adhesive

- Others

By Release Liner Type

- Silicone

- Non-silicone

By Surface Substrate

- Paper-based

- Film-based

By Application

- Commercial

- Industrial

- Residential

Drivers

Adoption of Self-Adhesive Labels in Food and Personal Care Industries Drives the Market.

In food and personal care packaging, the shift toward self-adhesive labels, particularly those employing hot-melt adhesives, is anchored in regulatory compliance and operational performance. Mandatory labelling requirements, in jurisdictions such as India’s Food Safety and Standards (Labelling and Display) Regulations, stipulate that pre-packaged foods carry clear, indelible information such as ingredient lists, batch identifiers, manufacturing and expiry dates, and licensing marks, with labels affixed so they will not become separated from the container.

Similarly, in the U.S., adhesives used on food packaging materials must meet FDA indirect food contact criteria (21 CFR 175.105) to ensure that migratory substances remain within safe limits, underscoring the need for specifically formulated hot-melt adhesives for labels. The hot-melt adhesives can be engineered to comply with such food contact standards, with migration testing confirming suitability for dry, moist, and refrigerated applications.

Moreover, self-adhesive technology is widely adopted in personal care packaging, where regulation mandates clear presentation of ingredients and safety information, driving demand for durable, moisture-resistant adhesive labels. The food and beverages represent the largest application segment for self-adhesive labels, accounting for a majority share, with personal care products forming a significant portion of the remainder due to branding and compliance needs.

Restraints

Competition from Alternative Adhesion Technology Poses a Significant Challenge to the Hot-Melt Self-Adhesive Labels Market.

Competition from alternative adhesion technologies presents a documented technical challenge to the adoption of hot-melt self-adhesive label systems. Hot-melt pressure-sensitive adhesives (HMPSAs) must be heated to 130-160 °C for coating, and their performance can be constrained by plasticizer migration and limited adhesion on certain substrates without formulation adjustments, creating performance gaps relative to other adhesive technologies.

In contrast, pressure-sensitive adhesive (PSA) technologies, inclusive of acrylic dispersions and solvent/water-based pressure-sensitive systems, are inherently tacky at room temperature and do not require heat activation, facilitating instantaneous bond formation without thermal input. Water-based acrylic PSAs have become broadly used by labelstock producers, offering alternative adhesion profiles where hot-melt formulations may underperform or where process constraints discourage high-temperature coating.

Moreover, multi-chemistry adhesive portfolios from major suppliers, such as hot-melt, water-based, UV, solvent-based acrylics, reflect industry responses to diverse substrate and sustainability requirements, indicating that alternatives compete directly with hot-melt systems for certain label applications. The functional differentiation of adhesive technologies, in terms of activation energy, substrate compatibility, and processing requirements, constitutes a verifiable challenge for hot-melt self-adhesive label uptake, where alternatives may offer process or performance advantages.

Opportunity

Demand for Regulatory Compliant Labels Creates Opportunities in the Market.

Regulatory actions targeting per- and polyfluoroalkyl substances (PFAS) in packaging create a defined compliance imperative for hot-melt self-adhesive label producers and converters, presenting an evidentiary basis for demand in PFAS-free adhesive solutions. In the U.S., the Food and Drug Administration (FDA) has announced that substances containing PFAS used as grease-proofing agents for paper and paperboard food packaging are no longer being sold and that associated food contact notifications are no longer effective as of January 2025, reflecting the elimination of this source of dietary PFAS exposure from food contact uses.

Concurrently, several U.S. states, such as Connecticut and Maine, have enacted and enforced restrictions that prohibit products containing intentionally added PFAS in food packaging, with definitions of packaging that expressly include labels, coatings, closures, and inks. In India, the Food Safety and Standards Authority of India (FSSAI) has published a draft amendment proposing that PFAS shall not be used in the manufacturing of food contact materials, signaling similar regulatory direction.

Consequently, label manufacturers have introduced PFAS-free self-adhesive label materials tailored for food products, demonstrating operational traction of regulatory-driven demand. These developments underscore a quantifiable regulatory push toward PFAS-free label components, reinforcing uptake of compliant hot-melt adhesive alternatives within regulated food and consumer packaging supply chains.

Trends

Shift Towards Linerless Hot-Melt Self-Adhesive Labels.

The shift toward linerless hot-melt self-adhesive labels is increasingly evident in the labeling industry, driven by environmental and operational benefits. Linerless labels eliminate the need for release liner materials, reducing waste and enhancing sustainability. A key benefit is the reduced carbon footprint of manufacturing and disposal, as the absence of liners cuts down on waste production and transportation costs associated with liner disposal. For instance, UPM Raflatac’s introduction of linerless label solutions, which, according to company reports, lead to a 15% reduction in label waste and a 10% increase in roll length due to the absence of liner materials, improves operational efficiency.

Moreover, the adoption of hot-melt adhesives, such as labels in the EVOLABEL product line, is gaining traction for its ability to bond securely to a variety of substrates without the need for additional curing processes. Regulatory trends, such as the European Union’s Waste Framework Directive, further support the move toward linerless options by incentivizing manufacturers to explore packaging solutions that minimize environmental impact. This regulatory push aligns with growing consumer and corporate demand for environmentally friendly alternatives, positioning linerless labels as a key innovation within the broader packaging sector.

Geopolitical Impact Analysis

Geopolitical Uncertainties Have Affected Global Petroleum Supply Chains.

The geopolitical tensions exert measurable impacts on the hot-melt self-adhesive labels market primarily through the global supply chain for crude oil and logistics. Key feedstocks for hot-melt adhesives, such as ethylene-vinyl acetate (EVA) and other petrochemical derivatives, are subject to volatile pricing and availability influenced by geopolitical disruptions affecting crude oil and natural gas markets.

For instance, conflicts in the Red Sea have forced maritime rerouting around the Cape of Good Hope. Similarly, the Russia-Ukraine conflict has led to a surge in the prices of crude oil. Similarly, the United Nations Conference on Trade and Development (UNCTAD) reported that transit through the Suez Canal dropped by 42% in early 2024, causing shipping container rates to spike by over 200% on certain Asia-to-Europe routes.

Governmental policy discussions reflect broader concerns about geopolitical supply chain risk, with the Organisation for Economic Co-operation and Development (OECD) emphasizing that dependencies on single regions for critical goods can create vulnerabilities that adversaries might exploit. Consequently, Henkel completed the divestment of its Russian operations for EUR600 million in 2023, while Avery Dennison accelerated the expansion of its manufacturing footprint in India and Southeast Asia to mitigate over-reliance on single-region supply hubs.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Hot-Melt Self-Adhesive Labels Market.

In 2025, the Asia Pacific dominated the global hot-melt self-adhesive labels market, led by India and China, holding about 43.2% of the total global consumption, due to its massive manufacturing output and evolving consumer standards. China’s dominant position within the region underscores the link between large-scale packaging activity and high regional demand for adhesive labels used across food, beverage, consumer goods, and logistics applications.

Furthermore, the Bureau of Indian Standards (BIS) and China’s National Health Commission (NHC) have introduced stringent food-contact material (FCM) regulations, such as GB 9685-2016, which specifies the use of additives in adhesives to ensure consumer safety in the massive domestic F&B market. This underscores the demand for safe labels, propelling the hot-melt self-adhesive labels market.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers in the hot-melt self-adhesive labels segment concentrate on product innovation, sustainability, and technology integration to strengthen competitive positioning and expand share. A recurring strategic focus is the development of recyclable and low-impact adhesive formulations that comply with emerging regulatory standards.

The producers are leveraging digital and smart technologies, which enhance functionality and supply chain traceability. R&D around high-performance hot-melt chemistries that deliver dependable adhesion across demanding substrates reinforces technical differentiation.

The Major Players in The Industry

- AKO Group

- Arkema (Bostik)

- Avery Dennison Corporation

- CCL Industries

- Golden Paper Company Limited

- B. Fuller Company

- Jiangmen Hengyuan Label Technology Co., Ltd.

- Jowat SE

- LINTEC Corporation

- UPM

- Henkel Ltd.

- Other Key Players

Key Development

- In April 2023, Dow Inc. and Avery Dennison jointly developed a sustainable hot-melt label adhesive that allows polyolefin filmic labels and polypropylene (PP) or polyethylene (PE) packaging to be mechanically recycled together within a single recycling stream.

- In December 2025, Henkel introduced a hot-melt adhesive, Technomelt EM 335 RE, designed to overcome the limitations associated with conventional hot-melt adhesives and to facilitate the clean separation of labels from PET bottles.

Report Scope

Report Features Description Market Value (2025) US$11.3 Bn Forecast Revenue (2035) US$22.0 Bn CAGR (2026-2035) 6.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Adhesive Types (Acrylic-based Adhesive, Rubber-based Adhesive, and Others), By Release Liner Type (Silicone and Non-silicone), By Surface Substrate (Paper-based and Film-based), By Application (Commercial, Industrial, and Residential) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape AKO Group, Arkema (Bostik), Avery Dennison Corporation, CCL Industries, Golden Paper Company Limited, H.B. Fuller Company, Jiangmen Hengyuan Label Technology Co., Ltd., Jowat SE, LINTEC Corporation, UPM, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Hot-Melt Self-Adhesive Labels MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Hot-Melt Self-Adhesive Labels MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- AKO Group

- Arkema (Bostik)

- Avery Dennison Corporation

- CCL Industries

- Golden Paper Company Limited

- B. Fuller Company

- Jiangmen Hengyuan Label Technology Co., Ltd.

- Jowat SE

- LINTEC Corporation

- UPM

- Henkel Ltd.

- Other Key Players

Our Clients

- 180168

- Mar 2026