Global Home Theater Market Market Size, Share, Growth Analysis By Type (Home Theatre-in-a-Box (HTiB), Component System, Soundbar System, Home Theatre PC and Media-Center, Custom Built-In Theatre), By Connectivity (Wired, Wireless (Wi-Fi and Bluetooth and RF)), By End Use (Residential, Commercial), By Distribution Channel (Offline, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: Nov 2025

- Report ID: 168102

- Number of Pages: 233

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

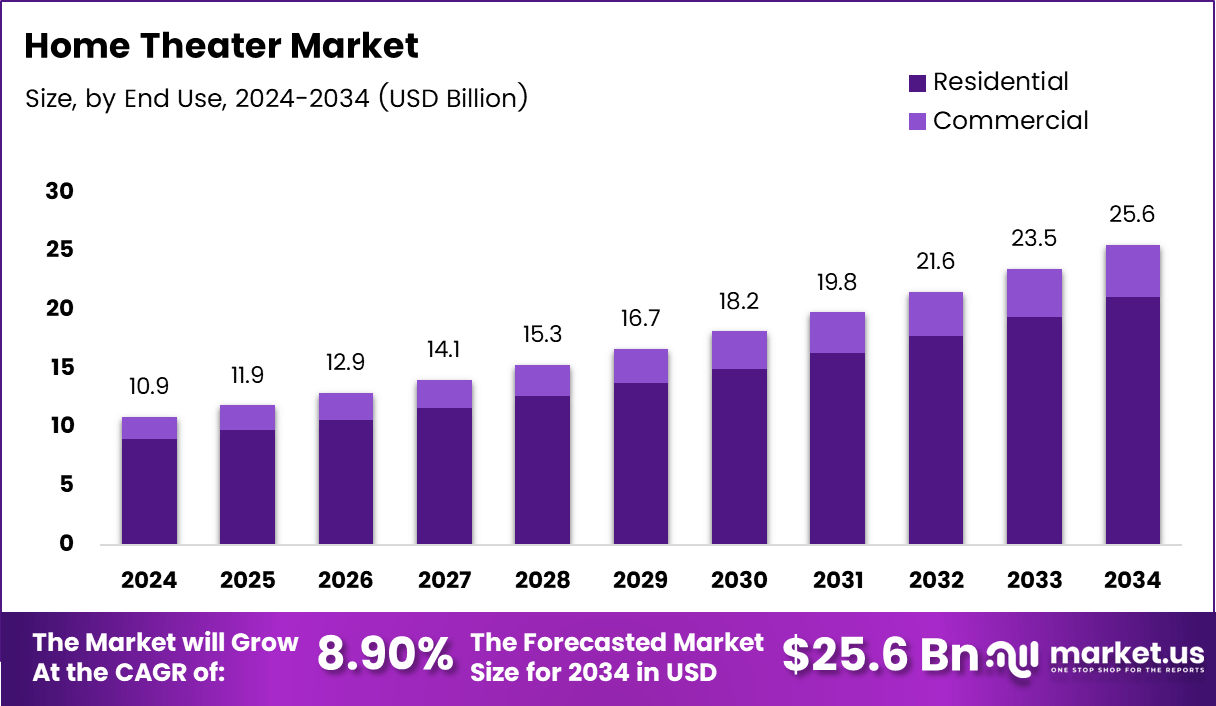

The Global Home Theater Market size is expected to be worth around USD 25.6 billion by 2034, from USD 10.9 billion in 2024, growing at a CAGR of 8.9% during the forecast period from 2025 to 2034.

The Home Theater Market represents a fast-evolving consumer electronics category shaped by rising demand for immersive entertainment, premium audio-visual hardware installations, and cinema-like ambience at home. The market combines high-definition displays, advanced surround-sound systems, and integrated media solutions that enhance viewing experiences across living rooms, dedicated theater rooms, and luxury residential setups.

Growing lifestyle upgrades continue strengthening adoption as households increasingly shift toward personalized entertainment environments. Consumers now prioritize large-screen clarity, multi-speaker depth, and wireless connectivity, encouraging brands to expand product innovations. This transition aligns with rising home-based leisure habits, prompting stronger replacement cycles for soundbars, AV receivers, projectors, and acoustically optimized home-theater accessories.

Additionally, rising disposable income supports the installation of high-value home theater projects. Upscale homes integrate acoustic paneling, subwoofer arrays, and 4K/8K projection systems, creating a premium ecosystem. This momentum is further influenced by consumer desire to replicate cinematic experiences at home, reducing reliance on external entertainment venues and improving the long-term demand outlook.

Government investments in broadband expansion, digital-media infrastructure, and residential modernization indirectly strengthen the home theater ecosystem. Policies promoting smart-home development, energy-efficient electronics, and domestic manufacturing support the wider availability of advanced entertainment products. These actions collectively improve accessibility, lower entry barriers, and stimulate market penetration across urban and semi-urban markets.

At the same time, regulatory guidelines on energy standards encourage manufacturers to develop more efficient amplifiers, displays, and wireless systems. Compliance with safety norms, connectivity standards, and low-emission component requirements shapes design innovation, allowing the market to benefit from stable long-term regulatory alignment.

Consumer behaviour strongly influences demand as households increasingly prioritize large-format viewing. According to research, 97% of American households own at least one TV, reflecting strong readiness for home-theater integration. This widespread device penetration accelerates upgrades toward high-performance screens, cinematic sound, and modular home-theater configurations.

Luxury installations also form a substantial segment. As per survey, 38% of dedicated home-theater projects exceed USD 100,000, and 9% surpass USD 200,000, indicating robust premium demand. Meanwhile, cinema industry benchmarks continue shaping expectations; AMC theaters typically use 40–50 foot screens, according to industry data, reinforcing the trend toward larger home displays that offer enhanced immersion.

Key Takeaways

- The Global Home Theater Market is expected to reach USD 25.6 billion by 2034, rising from USD 10.9 billion in 2024.

- The market grows steadily at a CAGR of 8.9% from 2025 to 2034.

- Soundbar System dominates the By Type segment with a leading share of 48.8% in 2024.

- Wireless connectivity leads the By Connectivity segment with a dominant share of 67.2% in 2024.

- Residential use accounts for the largest share of 82.5% in the By End Use segment in 2024.

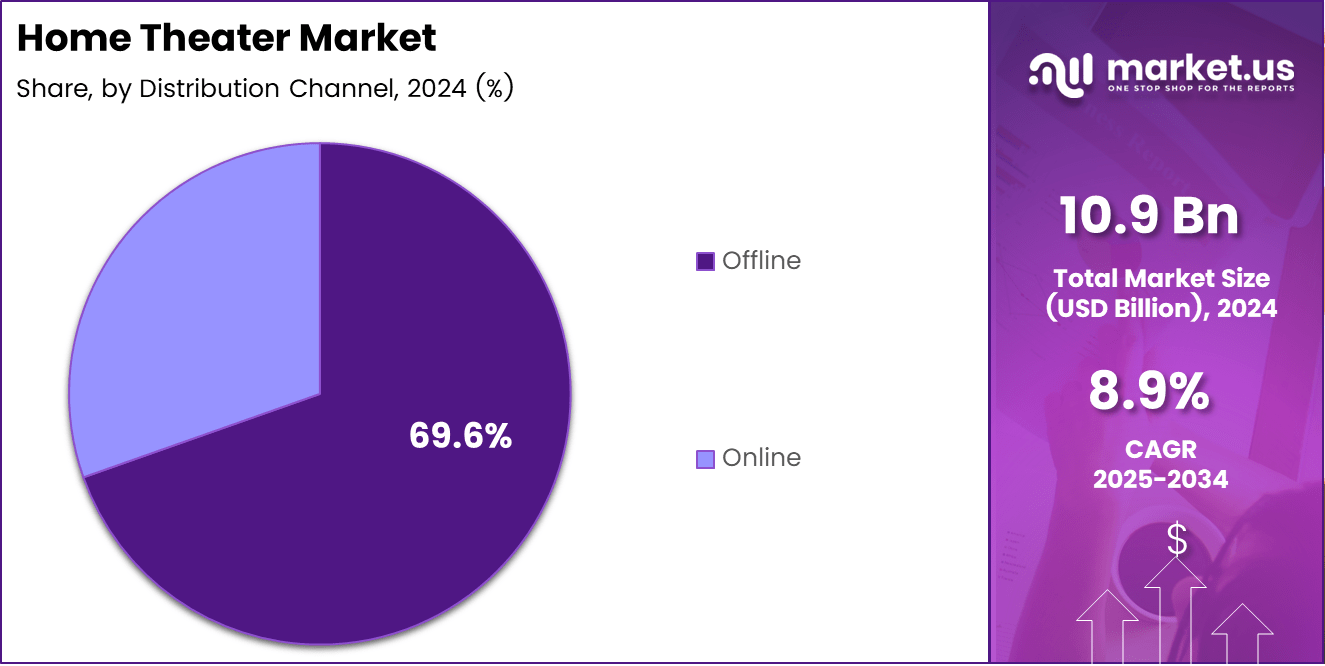

- Offline channels dominate the By Distribution segment with a share of 69.6% in 2024.

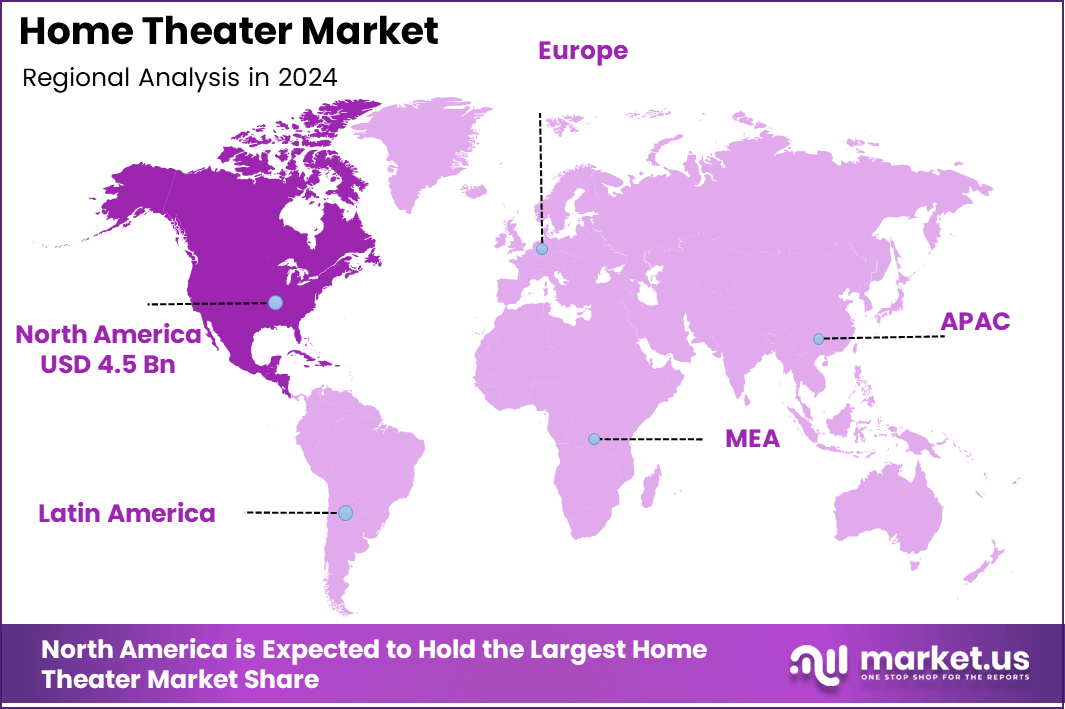

- Europe leads the regional landscape with a market share of 38.8%, valued at USD 309.2 million in 2024.

By Type Analysis

Soundbar System dominates with 48.8% due to easy installation and rising preference for compact audio solutions.

In 2024, Soundbar System held a dominant market position in the By Type Analysis segment of the Home Theater Market, with a 48.8% share. This segment advanced as consumers preferred slim, single-unit sound solutions that deliver cinematic sound without complex wiring. Its compatibility with large-screen TVs further strengthened demand.

Home Theatre-in-a-Box (HTiB) continued expanding as buyers sought bundled systems offering multiple speakers and unified control. This segment progressed due to affordability, simple assembly, and consistent audio performance for mid-sized rooms. Its appeal among entry-level home-theater users supported stable adoption across residential setups.

Component System gained traction as enthusiasts opted for customizable multi-speaker formats offering higher power output. This segment progressed with consumers selecting AV receivers, subwoofers, and satellite speakers separately to maximize flexibility. Its relevance increased among users upgrading from standard audio bars to advanced configurations.

Home Theatre PC / Media-Center evolved as users integrated computing, storage, and streaming functions within entertainment rooms. This segment advanced with digital libraries, high-resolution media playback, and smart-home automation features. Its usage increased among tech-savvy households demanding multifunction devices.

Custom-built-in theatre expanded with premium installations offering dedicated acoustics and luxury interiors. This segment progressed with higher spending on immersive in-home experiences, especially in large residences. Its demand grew with the rising interest in private cinema rooms.

By Connectivity Analysis

Wireless (Wi-Fi / Bluetooth / RF) dominates with 67.2% due to cable-free convenience and multi-room audio compatibility.

In 2024, Wireless (Wi-Fi / Bluetooth / RF) held a dominant market position in the By Connectivity Analysis segment of the Home Theater Market, with a 67.2% share. This segment advanced as consumers preferred clutter-free setups, seamless streaming, and device interoperability across TVs, projectors, and smartphones.

Wired connectivity maintained relevance among users, prioritizing stable audio transmission and zero-latency performance. This segment progressed as traditional multi-speaker layouts, including HTiB and component systems, continued relying on wired connections for better synchronization. Its adoption remained steady among professional installers and home-theater purists.

By End Use Analysis

Residential dominates with 82.5% supported by rising in-home entertainment investment.

In 2024, Residential held a dominant market position in the By End Use Analysis segment of the Home Theater Market, with an 82.5% share. This segment advanced as households upgraded viewing environments, purchased large-screen TVs, and preferred immersive sound systems for movies and entertainment, sports, and streaming.

Commercial applications grew as retail stores, hospitality spaces, and small auditoriums adopted advanced audio systems. This segment progressed with rising deployment in cafés, boutique cinemas, and experience-driven environments where high-fidelity sound enhances customer engagement.

By Distribution Channel Analysis

Offline dominates with 69.6% due to product demos and assisted purchasing.

In 2024, Offline held a dominant market position in the By Distribution Channel Analysis segment of the Home Theater Market, with a 69.6% share. This segment advanced as consumers preferred hands-on demonstrations, sound checks, and in-store expert guidance before purchasing integrated audio systems.

Online channels expanded rapidly as buyers compared models, accessed discounts, and relied on doorstep installation services. This segment progressed with rising e-commerce trust, influencer reviews, and the availability of bundled offers, enhancing adoption among digitally active consumers.

Key Market Segments

By Type

- Home Theatre-in-a-Box (HTiB)

- Component System

- Soundbar System

- Home Theatre PC / Media-Center

- Custom Built-In Theatre

By Connectivity

- Wired

- Wireless (Wi-Fi / Bluetooth / RF)

By End Use

- Residential

- Commercial

By Distribution Channel

- Offline

- Online

Drivers

Growing Popularity of Dolby Atmos Soundbars Influences Market Trends

The surge in Dolby Atmos and DTS: X-enabled soundbar sales is emerging as a strong market trend. These advanced soundbars replicate multi-dimensional audio without requiring multiple speakers. Consumers appreciate the combination of premium sound output and easy installation. This trend is supported by rising content availability in Atmos format, reinforcing demand for high-quality, theater-like sound at home.

The shift toward ultra-slim wall-mounted speaker systems is becoming another influential trend. Modern households prioritize sleek designs that blend seamlessly with wall-mounted TVs. Slim speaker bars and satellite units reduce clutter while enhancing the visual appeal of living spaces. Manufacturers are responding with low-profile designs that provide strong output without occupying floor space. This trend is expected to expand as home aesthetics gain importance.

Restraints

Rising Household Adoption of Large-Screen TVs Drives Market Growth

The widespread shift toward large-screen 4K and 8K TVs is expected to boost demand for advanced home-theater audio systems. As households upgrade display sizes, they naturally seek immersive sound to match the enhanced picture quality. This transition strengthens the need for multi-channel speakers, Dolby-enabled soundbars, and premium AV receivers. The growing affordability of large-screen TVs further accelerates the trend across middle-income homes, stimulating consistent market expansion.

The rapid expansion of streaming platforms offering multi-channel surround-sound content continues to create a strong pull for home-theater installations. Services such as Netflix, Disney+, and Prime Video now support Dolby Atmos soundtracks, encouraging users to upgrade their audio setup. The availability of high-resolution OTT content enhances viewing comfort at home, making immersive in-house entertainment a preferred choice for families and young consumers.

Growing consumer interest in premium home entertainment over frequent theater visits strengthens market momentum. Rising ticket prices and the preference for personalized viewing contribute to increased home-theater purchases. Many users now invest in dedicated entertainment areas, soundbars, and speaker clusters to replicate cinematic experiences. This shift toward convenience and customization supports steady demand across both urban and semi-urban households.

Growth Factors

Adoption of Wireless Home-Theater Systems Creates Strong Opportunities

The rising adoption of wireless and minimal-wiring home-theater solutions presents significant growth opportunities. Modern systems now support Bluetooth, Wi-Fi, and smart home integration, reducing dependency on cables. This convenience attracts tech-savvy users seeking clean aesthetics and easy installation. Wireless subwoofers and satellite speakers enhance flexibility, making the segment highly promising.

Growing demand for compact soundbars with subwoofer combos in smaller homes offers another strong opportunity. Space-efficient layouts in metros and small apartments encourage consumers to choose sleek audio solutions. These soundbars deliver powerful bass and clarity without requiring multiple speakers, making them a practical alternative to traditional setups. The trend aligns well with the rising popularity of minimalist interior designs.

The expansion of gaming-centric home-theater bundles integrated with spatial audio systems further boosts opportunity. Modern consoles such as PlayStation and Xbox support 3D Audio formats that enhance gameplay immersion. This encourages gamers to upgrade their home audio systems for better realism and directional sound. The rising gaming population strengthens demand for home-theater bundles designed specifically for entertainment versatility.

Emerging Trends

Growing Popularity of Dolby Atmos Soundbars Influences Market Trends

The surge in Dolby Atmos and DTS: X-enabled soundbar sales is emerging as a strong market trend. These advanced soundbars replicate multi-dimensional audio without requiring multiple speakers. Consumers appreciate the combination of premium sound output and easy installation. This trend is supported by rising content availability in Atmos format, reinforcing demand for high-quality, theater-like sound at home.

The shift toward ultra-slim wall-mounted speaker systems is becoming another influential trend. Modern households prioritize sleek designs that blend seamlessly with wall-mounted TVs. Slim speaker bars and satellite units reduce clutter while enhancing the visual appeal of living spaces. Manufacturers are responding with low-profile designs that provide strong output without occupying floor space. This trend is expected to expand as home aesthetics gain importance.

Regional Analysis

North America Dominates the Home Theater Market with a Market Share of 41.8%, Valued at USD 4.5 Billion

North America holds the leading position in the Home Theater Market, supported by strong consumer spending on premium audio-visual systems and the rapid adoption of large-screen entertainment formats. The region’s market value of USD 4.5 billion and dominant share of 41.8% reflect a mature ecosystem driven by high household penetration of smart TVs and advanced sound technologies. Increasing demand for immersive home-cinema setups and widespread availability of high-speed broadband further reinforce the region’s leadership.

Europe Home Theater Market Trends

Europe shows steady expansion as households increasingly invest in cinematic home-viewing environments and multi-room audio solutions. Rising interest in high-definition streaming, along with growing renovation activities in modern homes, supports ongoing adoption of advanced sound systems. The region also benefits from strong broadband infrastructure and a rising preference for stylish, space-efficient entertainment setups.

Asia Pacific Home Theater Market Trends

Asia Pacific emerges as one of the fastest-growing regions due to rising disposable income and expanding urban residential infrastructure. Consumers across China, Japan, South Korea, and India are shifting toward high-performance audio systems and large-format displays. Growing digital-content consumption and rapid e-commerce penetration further accelerate the region’s adoption of home-theater installations.

Middle East & Africa Home Theater Market Trends

The Middle East & Africa region experiences gradual growth driven by expanding luxury housing projects and rising interest in premium home-entertainment environments. Increasing broadband connectivity and lifestyle upgrades in major GCC countries boost consumer adoption of high-quality sound and display systems. The hospitality sector’s use of advanced audio-visual setups also contributes to market momentum.

Latin America Home Theater Market Trends

Latin America shows emerging demand as urban households adopt enhanced entertainment solutions and modernize living spaces. The growing popularity of streaming platforms and the rising affordability of large-screen TVs support market development across Brazil, Mexico, and Argentina. Economic recovery in key markets and broader retail availability of advanced home-theater equipment contribute to steady regional uptake.

U.S. Home Theater Market Trends

The U.S. market maintains strong traction with widespread household adoption of 4K and 8K TVs and high-performance audio equipment. Rising consumer interest in personalized entertainment experiences fuels demand for soundbars, multi-speaker setups, and immersive viewing environments. The market continues benefiting from robust digital infrastructure and a mature smart-home ecosystem.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Home Theater Market Company Insights

The global Home Theater Market in 2024 reflects strong competitive momentum driven by innovation-led product expansion, enhanced audio-visual engineering, and rising consumer demand for premium entertainment systems. Leading brands continue strengthening their portfolios through immersive sound design, wireless connectivity upgrades, and integration with 4K/8K ecosystems to enhance in-home cinematic experiences.

Bose Corporation remains influential due to its specialization in advanced acoustic engineering and minimalist premium sound systems. The company’s focus on voice-enabled smart home compatibility and refined surround-sound performance enhances its brand positioning among high-income home-entertainment buyers.

LG Electronics demonstrates solid growth through its integration of home theater systems with OLED and QNED TV technologies. The brand benefits from offering synchronized audio-video ecosystems, appealing to consumers seeking seamless multi-device entertainment environments.

Panasonic Corporation maintains market relevance through energy-efficient audio solutions and durable multi-channel setups targeted at a broad consumer base. Its emphasis on user-friendly interfaces and reliable hardware sustains its adoption across emerging and developed regions.

Sony Corporation strengthens its presence with advanced audio processing, high-resolution soundbars, and strong compatibility with PlayStation and Bravia TVs. Its commitment to spatial sound innovation improves user immersion and supports consistent demand across home-cinema users.

SAMSUNG leverages its dominance in display technologies by pairing its high-end TVs with integrated sound systems. The brand’s focus on Q-Series soundbars and smart connectivity functions aligns well with the expanding premium-home-entertainment trend.

Koninklijke Philips N.V. continues enhancing user experience through multi-room audio and minimalist soundbar solutions, while Bowers & Wilkins captures high-end consumers seeking audiophile-grade performance. Atlantic Technology, Definitive Technology, dba GoldenEar, and Yamaha Corporation remain competitively active through high-power speakers, subwoofer engineering, and expansion of wireless surround-sound ecosystems.

Top Key Players in the Market

- Bose Corporation

- LG Electronics.

- Panasonic Corporation

- Sony Corporation

- SAMSUNG

- Koninklijke Philips N.V.

- Bowers & Wilkins

- Atlantic Technology

- Definitive Technology

- dba GoldenEar

- Yamaha Corporation

Recent Developments

- In April 2025, Sony launched the BRAVIA Theatre Bar 8 and BRAVIA Theatre Quad systems, introducing advanced 360 Spatial Sound Mapping technology. This innovation creates a “phantom speaker” effect for immersive cinema-quality audio without needing multiple wired speakers.

- In August 2025, 26North Partners LP completed the acquisition of a controlling stake in AVI-SPL, the world’s largest AV integrator. This move is expected to expand global resources and influence the high-end luxury home cinema installation market by enhancing integration capabilities.

Report Scope

Report Features Description Market Value (2024) USD 10.9 billion Forecast Revenue (2034) USD 25.6 billion CAGR (2025-2034) 8.90% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Home Theatre-in-a-Box (HTiB), Component System, Soundbar System, Home Theatre PC / Media-Center, Custom Built-In Theatre), By Connectivity (Wired, Wireless (Wi-Fi / Bluetooth / RF)), By End Use (Residential, Commercial), By Distribution Channel (Offline, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Bose Corporation, LG Electronics, Panasonic Corporation, Sony Corporation, SAMSUNG, Koninklijke Philips N.V., Bowers & Wilkins, Atlantic Technology, Definitive Technology, dba GoldenEar, Yamaha Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Bose Corporation

- LG Electronics.

- Panasonic Corporation

- Sony Corporation

- SAMSUNG

- Koninklijke Philips N.V.

- Bowers & Wilkins

- Atlantic Technology

- Definitive Technology

- dba GoldenEar

- Yamaha Corporation

Our Clients

- 168102

- Nov 2025