Global High-Purity Chemicals Market By Product Type (Acids, Bases, Solvents, Specialty Gases, and Others), By End-Use (Electronics And Semiconductors, Pharmaceutical And Life Sciences, Chemical Manufacturing, Energy And Power, Aerospace And Defense, Academic & Research Institutions, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 179039

- Number of Pages: 319

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

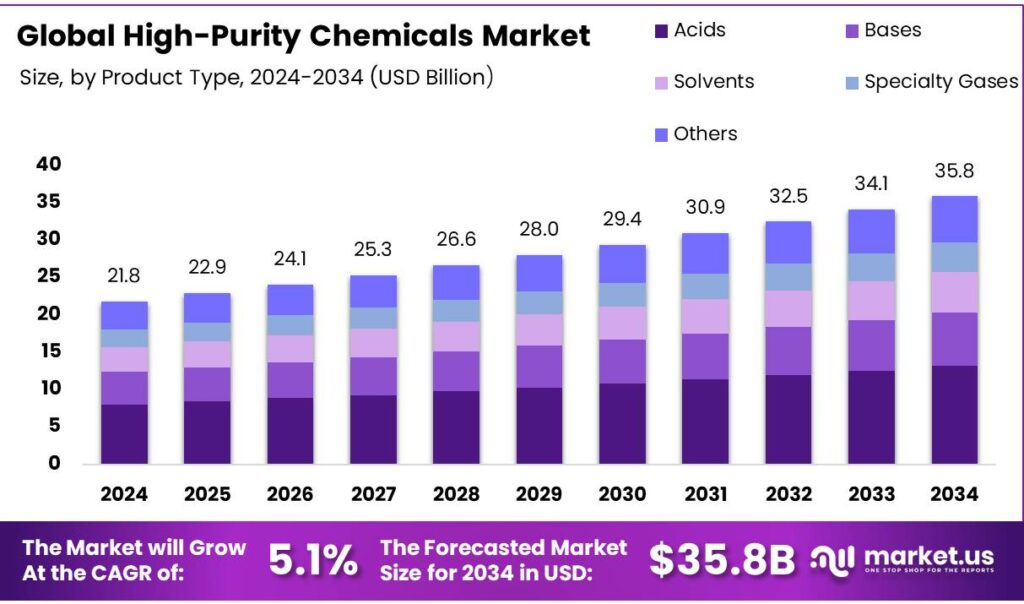

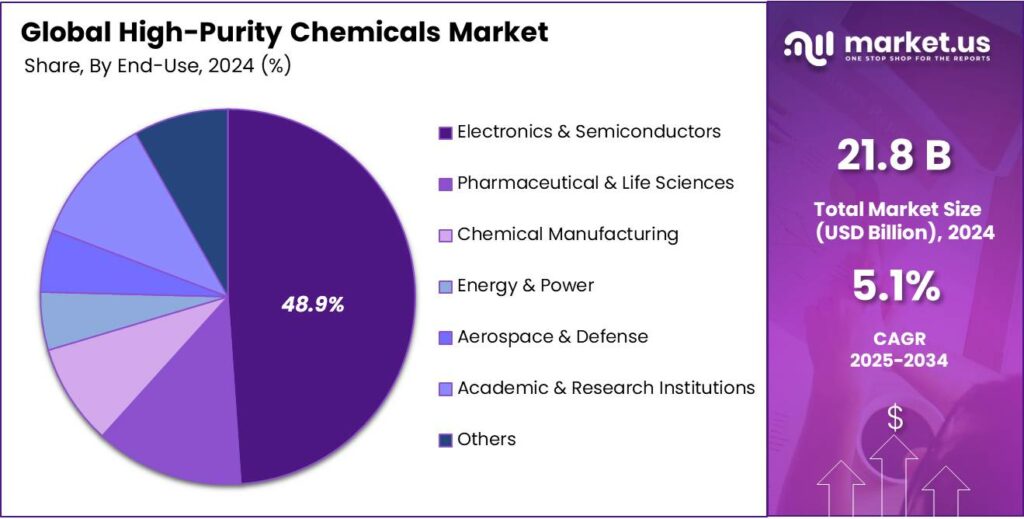

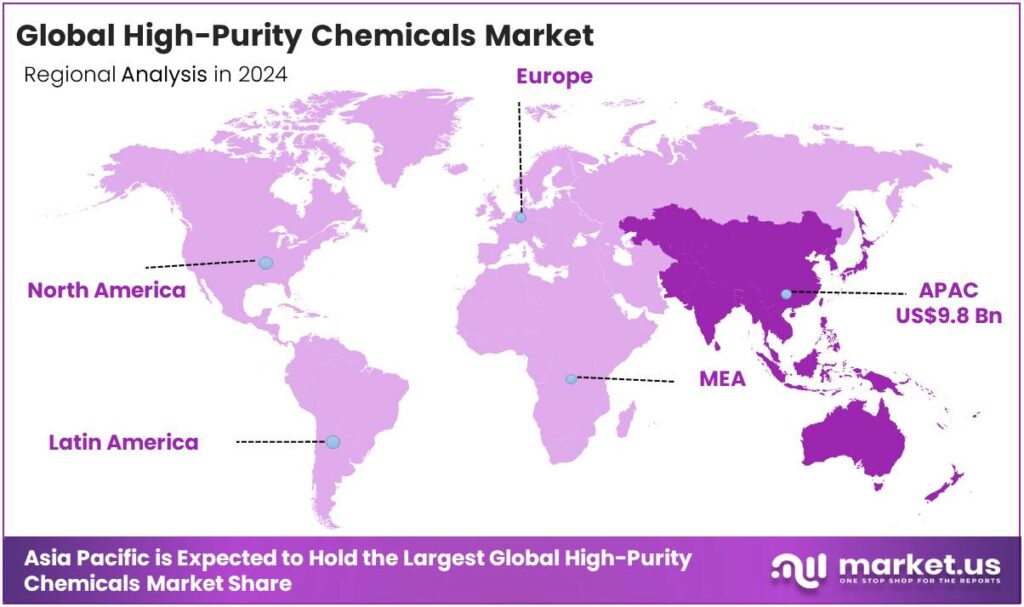

The Global High-Purity Chemicals Market is expected to be worth around USD 35.8 Billion by 2034, up from USD 21.8 Billion in 2024, and is projected to grow at a CAGR of 5.1% from 2025 to 2034. The Asia Pacific segment maintained 45.2%, supporting a High-Purity Chemicals value of USD 9.8 Bn.

High-purity chemicals are substances refined to contain minimal contaminants, often achieving purity levels of 99.9% or higher. In advanced industries such as semiconductors, purity can reach ultra-high levels where impurities are measured in parts per billion (ppb) or parts per trillion (ppt). The market is primarily driven by demand from the semiconductor and electronics industries, where extreme precision and contamination control are essential for manufacturing microchips, displays, and other advanced electronic components.

- According to the Semiconductor Industry Association, global semiconductor industry sales totaled US$75.3 billion during the month of November 2025, an increase of 29.8% compared to the November 2024 total of US$58.0 billion and 3.5% more than the October 2025 total of US$72.7 billion.

The high-purity chemicals, such as photoresists, etching agents, and specialty solvents, are critical in processes such as lithography and doping, where even trace impurities can significantly affect device performance. Additionally, the pharmaceutical and biotech sectors require high-purity chemicals for drug formulation, cell culture, and biologics production, adhering to stringent regulatory standards for purity.

- According to the International Council on Clean Transportation, in 2025, projected lithium refining capacity reached 1,030 ktpa LCE in the United States alone to support large-scale energy transition goals.

Similarly, the renewable energy sector, particularly in solar panel and battery manufacturing, increasingly relies on high-purity chemicals for the production of efficient energy storage and conversion systems. Although high-purity chemicals are essential in various sectors, the environmental impact during the production of these chemicals might add complexities to the market. Furthermore, the geopolitical tensions and supply chain disruptions have introduced challenges, especially in sourcing critical materials such as rare earth elements and high-purity gases.

- According to the International Energy Agency IEA), global renewable power capacity is projected to increase almost 4,600 GW between 2025 and 2030, double the deployment of the previous five years from 2019 to 2024.

Key Takeaways:

- The global high-purity chemicals market was valued at USD 21.8 billion in 2024.

- The global high-purity chemicals market is projected to grow at a CAGR of 5.1% and is estimated to reach USD 35.8 billion by 2034.

- Based on the types of high-purity chemicals, acids dominated the market, with a substantial market share of around 36.7%.

- Among the end-uses of high-purity chemicals, the electronics & semiconductors sector held a major share in the market, 48.9% of the market share.

- In 2024, the Asia Pacific was the most dominant region in the high-purity chemicals market, accounting for around 45.2% of the total global consumption.

Product Type Analysis

Acids are a Prominent Segment in the High-Purity Chemicals Market.

The high-purity chemicals market is segmented based on type into acids, bases, solvents, specialty gases, and others. High-purity acids dominated the market, comprising around 36.7% of the market share, primarily due to their critical role in essential manufacturing processes, particularly in industries such as semiconductors, pharmaceuticals, and electronics. Acids such as hydrofluoric acid, nitric acid, and sulfuric acid are central to etching, cleaning, and doping processes in semiconductor fabrication, where precision and purity are paramount.

Additionally, high-purity acids are essential in pharmaceutical synthesis and in producing chemicals for specialty applications, where strict purity standards must be met. In contrast, while bases, solvents, and gases are also crucial, their roles are often less specialized or more standardized, limiting their comparative revenue potential.

End-Use Analysis

The High-Purity Chemicals Are Mostly Utilized for the Electronics & Semiconductors Sector.

Based on the end-uses of high-purity chemicals, the market is divided into electronics & semiconductors, pharmaceutical & life sciences, chemical manufacturing, energy & power, aerospace & defense, academic & research institutions, and others. The electronics & semiconductors sector dominated the market, with a market share of 48.9%, due to the extreme precision required in manufacturing microchips and electronic components. For instance, in semiconductor fabrication, minute impurities can significantly affect the performance and yield of devices, making high-purity chemicals essential.

Materials such as photoresists, etching acids, and solvents are used in highly controlled processes such as lithography and doping, where purity directly correlates to device quality. While industries such as pharmaceuticals and energy rely on high-purity chemicals, the level of precision and volume required for semiconductor production far exceeds that of other sectors. Additionally, the rapid growth and technological advancements in electronics and semiconductors drive consistent demand for specialized, ultra-pure materials to meet increasingly sophisticated manufacturing needs.

Key Market Segments:

By Product Type

- Acids

- Hydrofluoric Acid

- Nitric Acid

- Sulfuric Acid

- Hydrochloric Acid

- Phosphoric Acid

- Others

- Bases

- Ammonium Hydroxide

- Potassium Hydroxide

- Sodium Hydroxide

- Others

- Solvents

- Isopropyl Alcohol (IPA)

- Acetone

- Methanol

- Ethanol

- Propylene Glycol

- Others

- Specialty Gases

- Others

By End-Use

- Electronics & Semiconductors

- Pharmaceutical & Life Sciences

- Chemical Manufacturing

- Energy & Power

- Aerospace & Defense

- Academic & Research Institutions

- Others

Drivers

Booming Tech Industries Drive the High-Purity Chemicals Market.

The high-purity chemicals market has experienced significant growth, driven primarily by the increasing demand from key technological industries, notably semiconductors, electronics, and batteries. Semiconductor manufacturing, which relies heavily on ultra-pure chemicals such as silicon, hydrogen fluoride, and photoresist chemicals, represents a critical growth driver.

For instance, the semiconductor industry requires the use of high-purity chemicals in processes such as photolithography and etching. Similarly, in electronics, demand for high-purity chemicals is growing due to the miniaturization of components and the need for precision in products such as OLED screens, integrated circuits, and memory chips.

- According to the International Energy Agency (IEA), nickel and cobalt are key materials in several lithium-ion battery cathode materials, including lithium nickel manganese cobalt oxide (NMC) and lithium nickel cobalt aluminum oxide (NCA), which together made up about 70% of the global battery market share in 2022.

Apart from this, the battery industry, particularly lithium-ion batteries, relies on high-purity materials, such as lithium carbonate, cobalt, and nickel. The battery production requires high-purity chemicals to ensure safety, efficiency, and longevity of the cells, with an increasing focus on supply chain sustainability. As electric vehicle (EV) adoption rises, the demand for these materials is expected to continue expanding. These industries collectively push the demand for high-purity chemicals, with each sector relying on different specialized chemical products for advanced manufacturing processes.

- According to a 2024 report by the International Council on Clean Transportation, annual global BEV sales have grown from about 2.2 million in 2020, to about 4.8 million in 2021, and to about 7.7 million in 2022.

Restraints

The Environmental Impact of the Production of High-Purity Chemicals Might Pose a Challenge to the Market.

The environmental impact of producing high-purity chemicals presents a significant challenge for the industry. High-purity chemicals often involve complex, energy-intensive manufacturing processes that contribute to environmental degradation. Production of ultra-pure chemicals such as hydrogen fluoride and photoresists requires substantial energy consumption. According to the U.S. Environmental Protection Agency (EPA), semiconductor fabs can use up to 100 times more energy per square foot than typical office buildings.

Moreover, the waste generated during the production of high-purity chemicals presents environmental concerns. For instance, in lithium-ion battery production, the process of refining raw materials such as lithium and cobalt produces toxic by-products. The improper disposal or recycling of these chemicals can result in soil and water contamination, posing long-term environmental risks.

Additionally, stringent regulations add to the complexity. For instance, in the United States, the Environmental Protection Agency (EPA) finalized the HON Rule in May 2024, targeting air toxic emissions from synthetic organic chemical manufacturing. Similarly, in August 2025, South Korea reclassified over 1,100 toxic chemicals into new hazard categories, acute, chronic, and ecological, to ensure more nuanced environmental management.

Furthermore, the U.S. Occupational Safety and Health Administration (OSHA) has identified the production of certain high-purity chemicals as involving substantial risks of chemical exposure to workers. While the demand for high-purity chemicals continues to rise, their environmental impact remains a crucial challenge requiring stricter regulatory oversight and technological innovation.

Opportunity

Stringent Regulations in Pharmaceutical and Biotech Industries Create Opportunities in the High-Purity Chemicals Market.

Stringent regulations in the pharmaceutical and biotech industries represent a significant opportunity for the high-purity chemicals market. The production of biologics, vaccines, and active pharmaceutical ingredients (APIs) necessitates ultra-pure chemicals to ensure product safety, efficacy, and regulatory compliance. For instance, the U.S. Food and Drug Administration (FDA) enforces stringent Good Manufacturing Practices (GMP) guidelines, which mandate the use of high-purity reagents and solvents in drug production.

- In the United States, the United States Food and Drug Administration (FDA) reported a 50% increase in warning letters issued by the Center for Drug Evaluation and Research (CDER) during fiscal year 2025, signaling heightened enforcement of quality and manufacturing compliance.

Similarly, the European Medicines Agency (EMA) stipulates that pharmaceutical manufacturing must meet specific standards of purity, prompting demand for highly refined chemicals that meet these rigorous specifications. Furthermore, in biotech, the production of monoclonal antibodies, gene therapies, and cell-based therapies requires high-purity chemicals in processes such as cell culture, protein purification, and drug formulation.

- In Europe, the European Pharmacopoeia will permanently delete the Rabbit Pyrogen Test in January 2026, requiring manufacturers to adopt more sensitive, high-purity analytical testing methods for pyrogenicity.

Similarly, the International Council for Harmonisation (ICH) guidelines, such as Q3C (residual solvents) and Q3D (elemental impurities), establish permitted daily exposure (PDE) limits for trace contaminants. The stringent regulatory environment in the pharmaceutical and biotech sectors drives the demand for high-purity chemicals, presenting an opportunity for suppliers to meet the industry’s increasingly sophisticated and specific needs.

Trends

Growth in Applications of High-Purity Chemicals in the Renewable Energy Industry.

The growth of renewable energy technologies presents a significant trend in the high-purity chemicals market, driven by increasing demand for advanced materials in solar, wind, and energy storage systems. High-purity chemicals are essential for manufacturing critical components such as photovoltaic cells, wind turbine blades, and energy storage batteries.

- According to a report by the IEA, growth in utility-scale and distributed solar PV would more than double by 2030, representing nearly 80% of worldwide renewable electricity capacity expansion.

In the solar energy industry, the production of silicon-based solar cells requires high-purity chemicals such as silicon tetrachloride and hydrogen fluoride. The performance and efficiency of solar panels heavily depend on the purity of silicon used in photovoltaic cells, with any contamination leading to performance degradation. The growing adoption of solar energy is directly tied to advancements in high-purity materials for cell fabrication.

For energy storage, particularly in lithium-ion batteries, the purity of chemicals such as lithium carbonate, cobalt, and nickel is crucial. The impurities in these materials can significantly reduce the energy density and lifespan of batteries, which are critical for large-scale energy storage solutions used in conjunction with renewable energy grids.

- The global investment in clean energy technologies grew 70% in 2023, mainly in solar PV and batteries, accelerating the need for high-specification chemical inputs.

In recent years, more than ten countries have implemented policies aimed at enhancing dispatchability and energy storage, with many introducing firm-capacity auctions for solar photovoltaic (PV) and wind energy since 2020. As renewable energy technologies continue to expand, the demand for high-purity chemicals for manufacturing and energy storage is expected to grow, reinforcing their importance in achieving sustainable energy goals.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the High-Purity Chemicals market by disrupting the Essential Supply Chains in the Market.

The geopolitical tensions have created significant disruptions in the high-purity chemicals market, primarily through supply chain uncertainties, raw material shortages, and shifting trade dynamics. The trade conflicts, such as the U.S.-China trade war, have affected the availability of critical materials such as rare earth elements, which are essential in semiconductor and electronics manufacturing.

In 2020, China, the world’s leading supplier of rare earths, imposed export restrictions, causing global supply chain delays. However, in November 2025, the Chinese Ministry of Commerce (MOFCOM) suspended a previous ban on the export of gallium, germanium, and antimony to the United States, materials where China holds global production shares of approximately 94%, 83%, and over 70%, respectively. This suspension, effective until November 27, 2026, restored these critical inputs to standard licensing frameworks, though prohibitions on military end-uses remain.

Similarly, in October 2025, the EU announced plans for a Critical Raw Materials Center to jointly purchase and stockpile minerals. Furthermore, the RESourceEU Action Plan, adopted in December 2025, established a Critical Chemicals Alliance to identify and modernize essential production sites within the bloc. Furthermore, stringent sanctions on countries such as Iran and Russia have hindered the global movement of high-purity petrochemicals, particularly those used in the energy and chemical industries. These sanctions have created bottlenecks in the supply of chemicals critical for battery manufacturing and other high-tech sectors. The geopolitical tensions are exerting substantial pressure on the high-purity chemicals market, contributing to volatility in supply chains and increasing the cost of raw materials.

Regional Analysis

Asia Pacific Held the Largest Share of the Global High-Purity Chemicals Market.

In 2024, the Asia Pacific dominated the global high-purity chemicals market, holding about 45.2% of the total global consumption, driven by its dominance in manufacturing sectors such as semiconductors, electronics, and renewable energy. The region accounts for over 60% of global semiconductor production, a key driver for high-purity chemicals such as silicon, hydrogen fluoride, and photoresist materials.

In countries such as Taiwan, South Korea, and Japan, the semiconductor industry’s reliance on ultra-pure chemicals is critical for maintaining the precision and efficiency required in microchip fabrication. In addition, countries such as China, Japan, and South Korea are at the forefront of producing advanced electronic components, which require chemicals such as specialty solvents, dopants, and etching agents for manufacturing processes. Similarly, government initiatives further propel the industry.

- According to the Japanese Ministry of Economy, Trade, and Industry (METI), they aim to raise their total budget by around 50% in fiscal year 2026, reaching approximately JPY3.07 trillion, to focus on semiconductors and artificial intelligence, with nearly JPY1.23 trillion allocated to these areas, about four times the previous amount.

Furthermore, Asia Pacific’s growing focus on renewable energy, particularly solar and battery production, is further contributing to the demand for high-purity materials. The International Energy Agency (IEA) reports that, in 2025, China became the first nation with over 1,000 GW of solar capacity, which depends heavily on high-purity chemicals. Moreover, the refining of various materials is done in the Asia Pacific, which requires a substantial amount of high-purity chemicals.

- The lithium refining capacity in the major lithium-producing countries, such as the United States are comparatively very low. For instance, according to the Department of Industry, Science, and Resources of Australia, in 2023, 96% of Australian lithium spodumene concentrate was exported to China for refining.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis:

Manufacturers of high-purity chemicals invest in advanced purification technologies and manufacturing processes to ensure the highest possible purity levels, as even minor contamination can significantly impact performance in sectors such as semiconductors and pharmaceuticals. In addition, they prioritize innovation by developing more efficient chemical formulations tailored to specific industrial needs, such as high-purity photoresists for next-generation semiconductors.

Furthermore, these players focus on expanding production capacity and establishing global supply chain networks to meet the growing demand, particularly in the Asia Pacific. Additionally, manufacturers often focus on maintaining rigorous quality control and compliance with industry standards, which is crucial in sectors with strict regulatory requirements.

The Major Players in The Industry

- BASF SE

- Evonik Industries AG

- Honeywell International Inc.

- Solvay SA

- Arkema Group

- Mitsubishi Chemical Corporation

- Sumitomo Chemical Co., Ltd.

- LG Chem Ltd.

- SK Materials Co., Ltd.

- Wacker Chemie AG

- Cabot Corporation

- OCI Company Ltd.

- Tokuyama Corporation

- Asahi Kasei Corporation

- Other Key Players

Key Development

- In April 2025, BASF announced the expansion of its production capacity for semiconductor-grade sulfuric acid (H2SO4), a critical ultra-pure chemical. The facility, located at its Ludwigshafen site in Germany, incorporates advanced purity technologies to meet the rising demand for high-performance semiconductor chip manufacturing throughout Europe.

- In September 2025, Evonik introduced MaxiPure Polysorbate 80, a highly refined surfactant tailored for injectable and biopharmaceutical uses. This ultra-pure excipient is designed to meet the rigorous requirements of contemporary drug development, which effectively addresses critical challenges, including protein stability, viral inactivation, and the reliable solubilization of hydrophobic active pharmaceutical ingredients (APIs).

Report Scope

Report Features Description Market Value (2024) US$21.8 Bn Forecast Revenue (2034) US$35.8 Bn CAGR (2025-2034) 5.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Acids, Bases, Solvents, Specialty Gases, and Others), By End-Use (Electronics & Semiconductors, Pharmaceutical & Life Sciences, Chemical Manufacturing, Energy & Power, Aerospace & Defense, Academic & Research Institutions, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape BASF SE, Evonik Industries AG, Honeywell International Inc., Solvay SA, Arkema Group, Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., LG Chem Ltd., SK Materials Co., Ltd., Wacker Chemie AG, Cabot Corporation, OCI Company Ltd., Tokuyama Corporation, Asahi Kasei Corporation, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  High-Purity Chemicals MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

High-Purity Chemicals MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Evonik Industries AG

- Honeywell International Inc.

- Solvay SA

- Arkema Group

- Mitsubishi Chemical Corporation

- Sumitomo Chemical Co., Ltd.

- LG Chem Ltd.

- SK Materials Co., Ltd.

- Wacker Chemie AG

- Cabot Corporation

- OCI Company Ltd.

- Tokuyama Corporation

- Asahi Kasei Corporation

- Other Key Players

Our Clients

- 179039

- Feb 2026