Global Herbal Shampoo Market Size, Share, Growth Analysis By Form (Liquid, Bars, Powder), By Gender (Women, Men, Unisex), By Application (Hair Growth, Scalp Care, Anti-dandruff, Styling), By Distribution Channel (Supermarket and Hypermarket, Specialty Stores, Online, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179551

- Number of Pages: 202

- Format:

-

keyboard_arrow_up

Quick Navigation

Market Overview

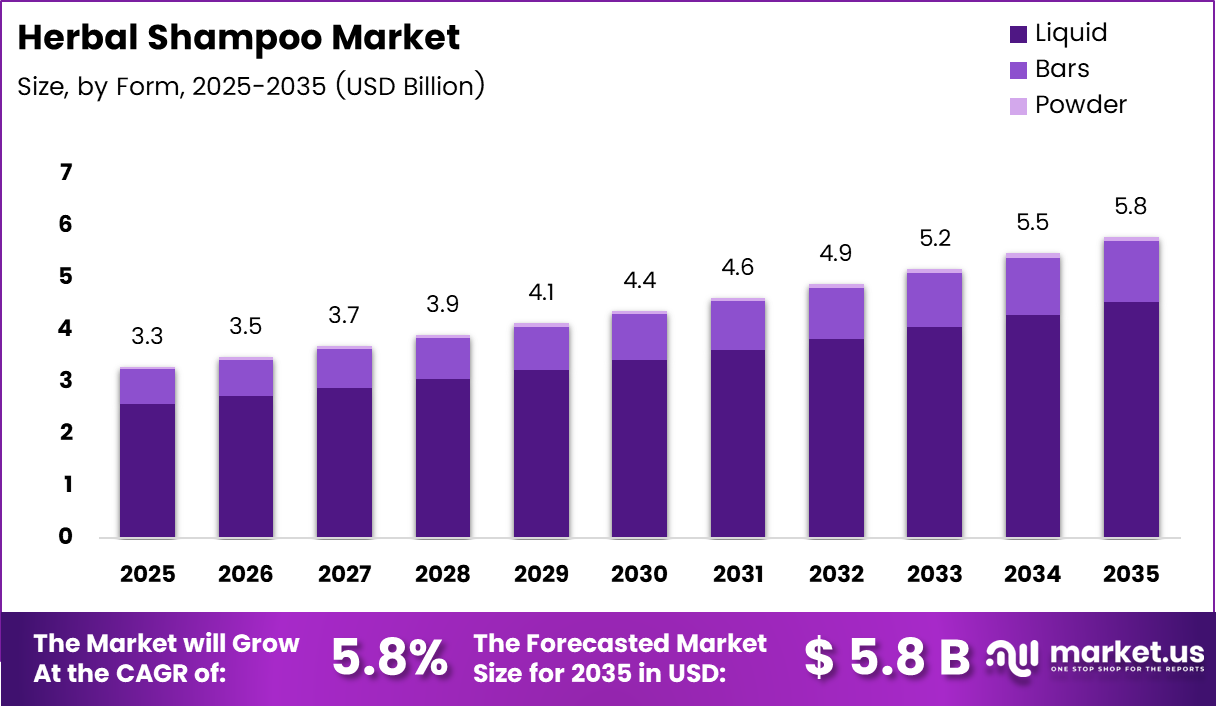

Global Herbal Shampoo Market size is expected to be worth around USD 5.8 Billion by 2035 from USD 3.3 Billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

The herbal shampoo market refers to the segment of the personal care industry focused on hair cleansing products formulated with plant-based, botanical, and natural ingredients. These products avoid harsh synthetic chemicals. Consumers prefer herbal shampoos for their gentler formulations and long-term scalp health benefits.

The market has seen strong growth as more consumers globally shift away from conventional chemical-laden hair care products. Growing awareness of scalp damage caused by sulfates, parabens, and silicones has accelerated this shift. Consequently, herbal shampoos are now mainstream across modern retail formats and online platforms.

Government regulations and clean beauty standards are further shaping the market landscape. Regulatory bodies in North America, Europe, and Asia are tightening guidelines on synthetic preservatives and chemical ingredients in personal care. Therefore, manufacturers are reformulating products with certified natural and organic components to remain compliant and competitive.

Investment in herbal and Ayurvedic beauty continues to rise globally. Brands are incorporating traditional herbs such as amla, neem, bhringraj, and shikakai into modern shampoo formulations. Additionally, clinical validation of plant-based ingredients is giving herbal shampoos stronger credibility among health-conscious consumers.

The market also benefits from a rapidly growing e-commerce ecosystem. Online platforms have expanded the reach of herbal shampoo brands into semi-urban and rural markets. Moreover, direct-to-consumer models allow brands to build trust through ingredient transparency and personalized recommendations.

Supporting data reinforces these trends strongly. According to The Good Trade, brands using naturally sourced ingredients report high consumer retention, with products made with 98% naturally sourced ingredients gaining shelf space in leading retail chains including Whole Foods and Walmart. Additionally, according to SEEN research, 93% of participants with flaky scalps saw improvement after using sulfate-free herbal formulations.

According to SEEN clinical studies, 70% of participants with acne saw improvement in body acne and 52% saw a reduction in facial acne after using plant-based, non-stripping shampoo formulations. These statistics highlight the growing clinical and consumer confidence in herbal shampoo products across global markets.

Key Takeaways

- The global Herbal Shampoo Market was valued at USD 3.3 Billion in 2025 and is projected to reach USD 5.8 Billion by 2035.

- The market is expected to grow at a CAGR of 5.8% during the forecast period 2026 to 2035.

- By Form, Liquid segment dominated the market with a share of 78.4% in 2025.

- By Gender, Women segment held the largest share at 67.5% in 2025.

- By Application, Anti-dandruff segment led the market with a 42.6% share in 2025.

- By Distribution Channel, Supermarket and Hypermarket segment dominated with a 44.8% share in 2025.

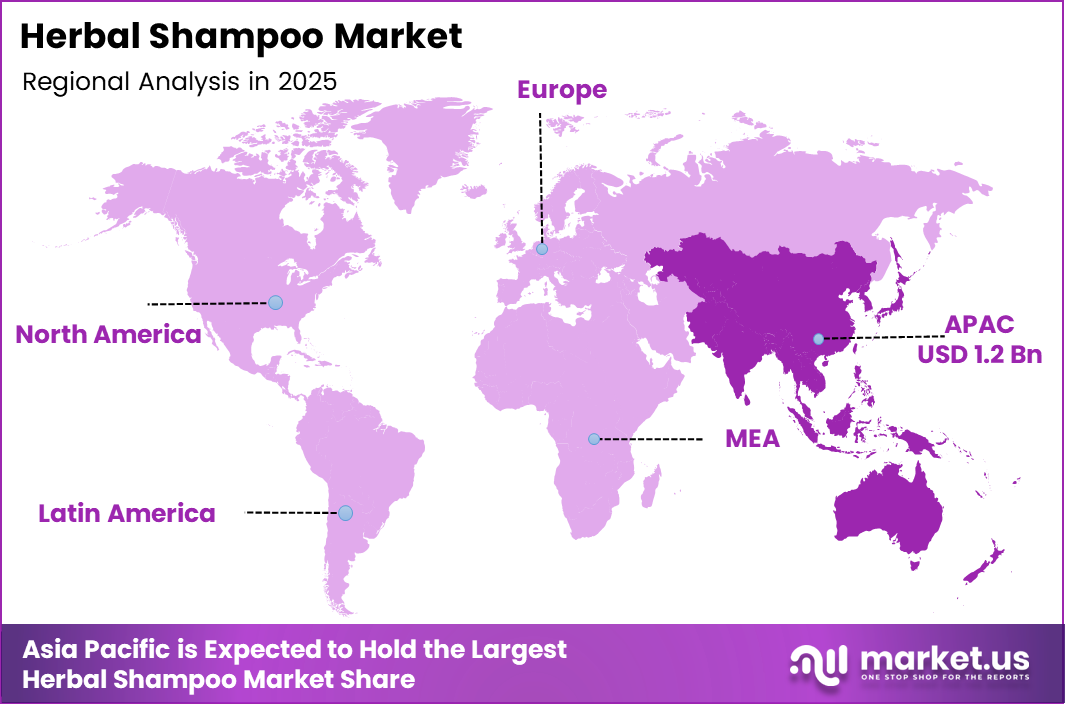

- Asia Pacific dominated the regional market with a share of 37.6%, valued at USD 1.2 Billion in 2025.

Form Analysis

Liquid dominates with 78.4% due to widespread consumer familiarity and ease of application.

In 2025, Liquid held a dominant market position in the Form segment of the Herbal Shampoo Market, with a 78.4% share. Liquid herbal shampoos remain the preferred choice globally due to their ease of use and lather performance. Moreover, their compatibility with a wide range of herbal ingredients and formulations supports continued dominance across retail channels.

Bars are gaining traction as a sustainable and travel-friendly alternative to liquid shampoos. Consumers increasingly favor bar formats for their minimal packaging and longer usage life. Additionally, herbal shampoo bars align well with the clean beauty and zero-waste movement that is growing in urban consumer segments worldwide.

Powder shampoos represent an emerging niche within the herbal hair care category. These waterless formulations appeal to eco-conscious consumers and those seeking extended shelf life without synthetic preservatives. Consequently, powder formats are gaining visibility in specialty wellness retail and online platforms targeting natural beauty enthusiasts.

Gender Analysis

Women dominates with 67.5% due to higher engagement with personal hair care routines and premium herbal products.

In 2025, Women held a dominant market position in the Gender segment of the Herbal Shampoo Market, with a 67.5% share. Women consistently represent the largest consumer base for herbal shampoos, driven by higher frequency of hair care routines and greater willingness to invest in premium botanical formulations. Moreover, targeted marketing has reinforced brand loyalty within this segment.

Men represent a fast-growing segment within the herbal shampoo market. Rising awareness of scalp health, hair fall, and dandruff among male consumers is fueling demand for dedicated herbal solutions. Additionally, the growing men’s grooming industry has encouraged brands to develop gender-specific herbal shampoos with targeted benefits such as hair strengthening and oil control.

Unisex herbal shampoos cater to a broad audience and are gaining popularity among households looking for versatile hair care solutions. These formulations appeal to consumers who prefer simplified routines. Consequently, unisex herbal shampoos are widely stocked in supermarkets and online retail formats due to their inclusive positioning and broad applicability.

Application Analysis

Anti-dandruff dominates with 42.6% due to high consumer prevalence of scalp issues and demand for natural remedies.

In 2025, Anti-dandruff held a dominant market position in the Application segment of the Herbal Shampoo Market, with a 42.6% share. Anti-dandruff herbal shampoos benefit from strong demand across age groups and geographies. Ingredients such as neem, tea tree, and salicylic acid from natural sources are clinically recognized for their efficacy. Moreover, consumer preference for non-medicated herbal solutions over chemical treatments drives this segment.

Hair Growth applications represent one of the most innovation-active areas within herbal shampoos. Formulations containing bhringraj, amla, and biotin-rich botanicals are widely promoted for reducing hair fall and stimulating growth. Additionally, increasing prevalence of stress-related hair loss globally is strengthening demand for herbal hair growth solutions among both men and women.

Scalp care herbal shampoos focus on addressing dryness, irritation, sensitivity, dandruff, and excess oil through gentle, plant-based ingredients. These formulations support scalp balance while maintaining the natural moisture barrier. As awareness of scalp health grows, consumers increasingly view scalp care as the foundation of overall hair wellness.

Styling Herbal styling shampoos combine cleansing with functional styling benefits such as frizz control, smoothness, volume, and texture enhancement. They appeal to users seeking manageable hair without relying on chemical-heavy styling products. As a result, brands are formulating multi-benefit shampoos that deliver both styling performance and scalp nourishment for holistic hair care results.

Distribution Channel Analysis

Supermarket and Hypermarket dominates with 44.8% due to wide product availability and high consumer footfall.

In 2025, Supermarket and Hypermarket held a dominant market position in the Distribution Channel segment of the Herbal Shampoo Market, with a 44.8% share. These retail formats offer consumers the convenience of comparing multiple herbal shampoo brands in one location. Moreover, established shelf visibility and promotional pricing support strong volume sales for mass-market and mid-premium herbal shampoo products.

Specialty Stores play a critical role in distributing premium and niche herbal shampoo brands. Stores focused on natural beauty, wellness, and Ayurvedic products attract highly engaged consumers who prioritize ingredient quality. Additionally, knowledgeable staff and curated assortments in specialty retail help drive trial and conversion for emerging herbal shampoo brands.

Online Channels are experiencing rapid growth in the herbal shampoo market due to increasing internet penetration and digital adoption. E-commerce platforms enable brands to reach consumers beyond traditional retail boundaries with greater efficiency. These channels also support personalized marketing, reviews, and doorstep delivery, enhancing consumer engagement and convenience.

Others segment includes direct-to-consumer websites, subscription-based models, and social commerce platforms. These channels allow brands to build stronger relationships with consumers through direct interaction and loyalty programs. As a result, they are becoming increasingly important for targeting urban, digitally active, and niche consumer segments.

Key Market Segments

By Form

- Liquid

- Bars

- Powder

By Gender

- Women

- Men

- Unisex

By Application

- Hair Growth

- Scalp Care

- Anti-dandruff

- Styling

By Distribution Channel

- Supermarket and Hypermarket

- Specialty Stores

- Online

- Others

Drivers

Rising Consumer Preference for Plant-Based Hair Care Drives Herbal Shampoo Market Growth

Consumers globally are increasingly shifting toward plant-based and chemical-free hair care solutions. Growing awareness of the long-term scalp and hair damage caused by synthetic shampoos is a key factor. Moreover, rising interest in clean beauty labels and ingredient transparency is encouraging consumers to choose herbal alternatives over conventional products.

The influence of Ayurveda, herbal science, and traditional hair care practices continues to expand across diverse demographics. Consumers in Asia, Europe, and North America are embracing botanical formulations rooted in centuries-old wellness traditions. Consequently, brands are integrating clinically validated herbs and natural actives to appeal to both health-conscious and culturally connected consumers.

Expanding availability of herbal shampoos across online and organized retail channels is removing earlier access barriers. E-commerce platforms and supermarket chains now stock a wide range of herbal shampoo variants. Therefore, broader distribution has enabled herbal shampoo brands to capture volume growth in both urban and semi-urban consumer markets worldwide.

Restraints

Shorter Shelf Life and Higher Costs Limit Wider Adoption of Herbal Shampoo Products

One significant challenge facing the herbal shampoo market is the shorter shelf life of preservative-free formulations. Natural ingredients without synthetic stabilizers are more susceptible to microbial contamination and oxidation. Consequently, manufacturers face difficulties in maintaining product quality across extended supply chains, which can impact consumer confidence and distribution efficiency.

Stability challenges add to the complexity of developing commercially viable herbal shampoo formulations. Achieving consistent texture, fragrance, and performance without synthetic additives requires advanced formulation expertise. Moreover, quality control for botanical raw materials varies significantly by region and season, creating supply inconsistencies that can affect production timelines and final product performance.

Higher product costs compared to conventional mass-market shampoos remain a barrier to broader market penetration. Premium pricing of herbal shampoos limits their accessibility among price-sensitive consumer segments, especially in developing markets. Therefore, bridging the affordability gap through cost-efficient sourcing and scaled production is a key challenge for brands targeting wider consumer adoption.

Growth Factors

Product Innovation and Emerging Consumer Segments Accelerate Herbal Shampoo Market Expansion

Product innovation using region-specific herbs and botanical extracts presents a strong growth opportunity for market players. Brands that incorporate locally sourced ingredients can differentiate their offerings and resonate with culturally aware consumers. Moreover, the development of premium and dermatologically tested herbal shampoo variants is building clinical credibility and attracting professional endorsement across key markets.

Rising demand from the men’s grooming segment is creating a new high-growth avenue for herbal shampoo brands. Male consumers are increasingly seeking natural solutions for hair fall control, scalp care, and dandruff management. Additionally, targeted product launches designed specifically for men are enabling brands to diversify their portfolios and capture incremental revenue from an underserved demographic.

Increasing market penetration in emerging urban and semi-urban consumer markets is further strengthening growth prospects. As disposable incomes rise and awareness of natural personal care grows, first-time herbal shampoo buyers are entering the category. Consequently, organized retail expansion and digital commerce are making herbal shampoos more accessible to a broader and younger consumer base globally.

Emerging Trends

Clean Formulations and Sustainable Packaging Reshape the Herbal Shampoo Market Landscape

A surge in sulfate-free, silicone-free, and paraben-free herbal shampoo launches is reshaping the product landscape. Consumers are actively seeking formulations free from harsh additives, and brands are responding with clean-label innovations. Moreover, regulatory pressure and retailer clean beauty standards are accelerating reformulation activity across both established brands and emerging herbal shampoo startups.

Growing popularity of customized and hair-type-specific herbal shampoo solutions is another key trend. Consumers want products that address their unique concerns, such as oily scalp, color-treated hair, or extreme dryness. Additionally, advances in personalization technology and direct-to-consumer platforms are enabling brands to offer tailored herbal formulations at scale for diverse hair types and conditions.

Adoption of sustainable, refillable, and eco-friendly packaging formats is gaining significant momentum across the herbal shampoo segment. Brands are investing in biodegradable packaging and certified sustainable materials to appeal to environmentally conscious consumers. Consequently, integration of clean labeling and full ingredient transparency is becoming a competitive differentiator that drives trust and long-term loyalty among modern buyers.

Regional Analysis

Asia Pacific Dominates the Herbal Shampoo Market with a Market Share of 37.6%, Valued at USD 1.2 Billion

Asia Pacific leads the global herbal shampoo market, holding a dominant share of 37.6% and valued at USD 1.2 Billion in 2025. The region benefits from deep-rooted traditions in Ayurvedic and herbal hair care, particularly in India, China, and Southeast Asia. Moreover, a large and growing middle-class consumer base, combined with expanding retail infrastructure, continues to drive strong regional demand.

North America Herbal Shampoo Market Trends

North America represents a mature and high-value market for herbal shampoos, driven by strong consumer awareness of clean beauty and ingredient safety. The United States leads regional demand, with a growing preference for certified natural and organic hair care products. Additionally, established retail distribution and e-commerce penetration support steady market growth across the region.

Europe Herbal Shampoo Market Trends

Europe holds a significant share of the global herbal shampoo market, supported by strict regulatory standards for personal care ingredients and high consumer demand for natural formulations. Germany, France, and the UK are key markets where sustainable beauty trends are well-established. Consequently, European brands are leaders in developing eco-certified and botanically rich herbal shampoo products.

Middle East and Africa Herbal Shampoo Market Trends

The Middle East and Africa region presents emerging opportunities for herbal shampoo brands. Growing urban populations, rising disposable incomes, and increasing awareness of natural hair care are driving demand. Moreover, the influence of traditional herbal remedies and a preference for chemical-free personal care products is encouraging market development across GCC countries and South Africa.

Latin America Herbal Shampoo Market Trends

Latin America is an evolving market for herbal shampoos, with Brazil and Mexico as the primary growth contributors. Rising consumer interest in natural and organic beauty products, combined with growing e-commerce access, is expanding the category. Additionally, local botanical ingredients unique to the region offer brands significant opportunities to develop differentiated herbal shampoo formulations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

The Procter and Gamble Company is a global leader in personal care and hair care, with a broad portfolio that includes herbal and naturally positioned shampoo variants. The company has invested significantly in research and development to reformulate products with plant-derived ingredients. Moreover, P&G’s extensive global distribution network ensures its herbal offerings reach consumers across both developed and emerging markets effectively.

Unilever PLC holds a strong position in the herbal shampoo segment through its diverse portfolio of natural and botanically inspired hair care brands. The company has made notable commitments to sustainable sourcing and clean formulations as part of its broader sustainability agenda. Additionally, Unilever’s deep retail penetration across Asia, Africa, and Latin America gives it a competitive advantage in high-growth herbal shampoo markets.

L’Oréal S.A. continues to strengthen its footprint in the natural and herbal hair care space through acquisitions and in-house product innovation. The company recently completed a significant acquisition to expand its premium beauty portfolio. Consequently, L’Oréal’s strong research capabilities, combined with its global brand presence, position it well to develop and market clinically validated herbal shampoo solutions across multiple consumer segments.

Kao Corporation is a leading Japanese personal care company known for its commitment to science-driven formulation using natural ingredients. Kao integrates botanical extracts and traditional Asian herbs into its hair care product lines. Moreover, the company’s strong focus on ingredient quality, safety, and sustainability aligns well with the growing global demand for premium herbal shampoo products in both Asian and international markets.

Key players

- The Procter and Gamble Company

- Unilever PLC

- L’Oréal S.A.

- Kao Corporation

- Biotique Ayurvedics Pvt. Ltd.

- Forest Essentials (A Luxasia Company)

- Khadi Natural Healthcare

- Shiseido Company, Limited

- Giovanni Cosmetics, Inc.

- Lush Retail Ltd.

Recent Developments

- October 2025 – China’s leading multi-brand beauty group JOY GROUP (Shanghai Juyi Cosmetics Co., Ltd.) announced the completion of its acquisition of Foltène, a dermatological hair care brand from Italy. This move strengthens JOY GROUP’s position in the premium herbal and dermatological hair care segment across Asian and European markets.

- January 2026 – L’Oréal Group completed its USD 2.525 Billion acquisition of the Aesop brand, significantly expanding its premium natural and botanical beauty portfolio. This acquisition reinforces L’Oréal’s strategic commitment to growing its presence in the clean and herbal personal care category globally.

Report Scope

Report Features Description Market Value (2025) USD 3.3 Billion Forecast Revenue (2035) USD 5.8 Billion CAGR (2026-2035) 5.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Liquid, Bars, Powder), By Gender (Women, Men, Unisex), By Application (Hair Growth, Scalp Care, Anti-dandruff, Styling), By Distribution Channel (Supermarket and Hypermarket, Specialty Stores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape The Procter and Gamble Company, Unilever PLC, L’Oréal S.A., Kao Corporation, Biotique Ayurvedics Pvt. Ltd., Forest Essentials (A Luxasia Company), Khadi Natural Healthcare, Shiseido Company Limited, Giovanni Cosmetics Inc., Lush Retail Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- The Procter and Gamble Company

- Unilever PLC

- L'Oréal S.A.

- Kao Corporation

- Biotique Ayurvedics Pvt. Ltd.

- Forest Essentials (A Luxasia Company)

- Khadi Natural Healthcare

- Shiseido Company, Limited

- Giovanni Cosmetics, Inc.

- Lush Retail Ltd.

Our Clients

- 179551

- Feb 2026