Global HD Map for Autonomous Driving Market Size, Share, Growth Analysis By Solution (Cloud-Based, Embedded), By Level of Automation (L2, L3, L4, L5), By Vehicle Type (Passenger Vehicle, Commercial Vehicle), By Services (Mapping & Navigation, Localization), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 177488

- Number of Pages: 339

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

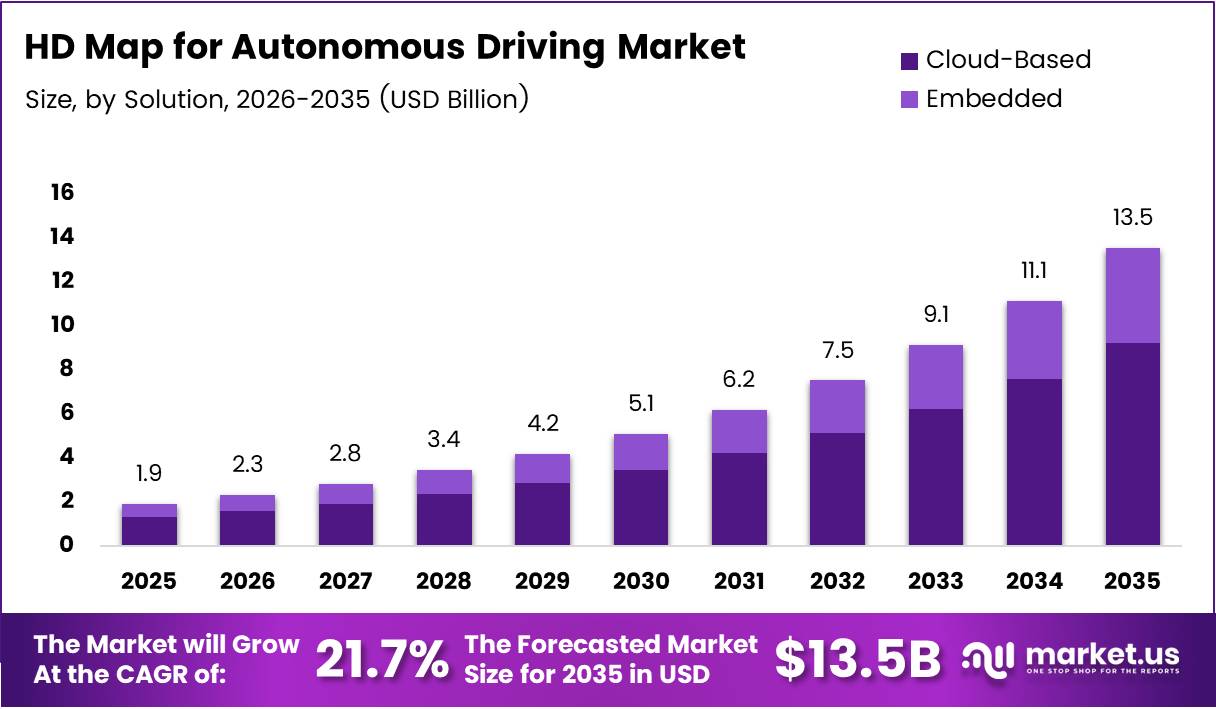

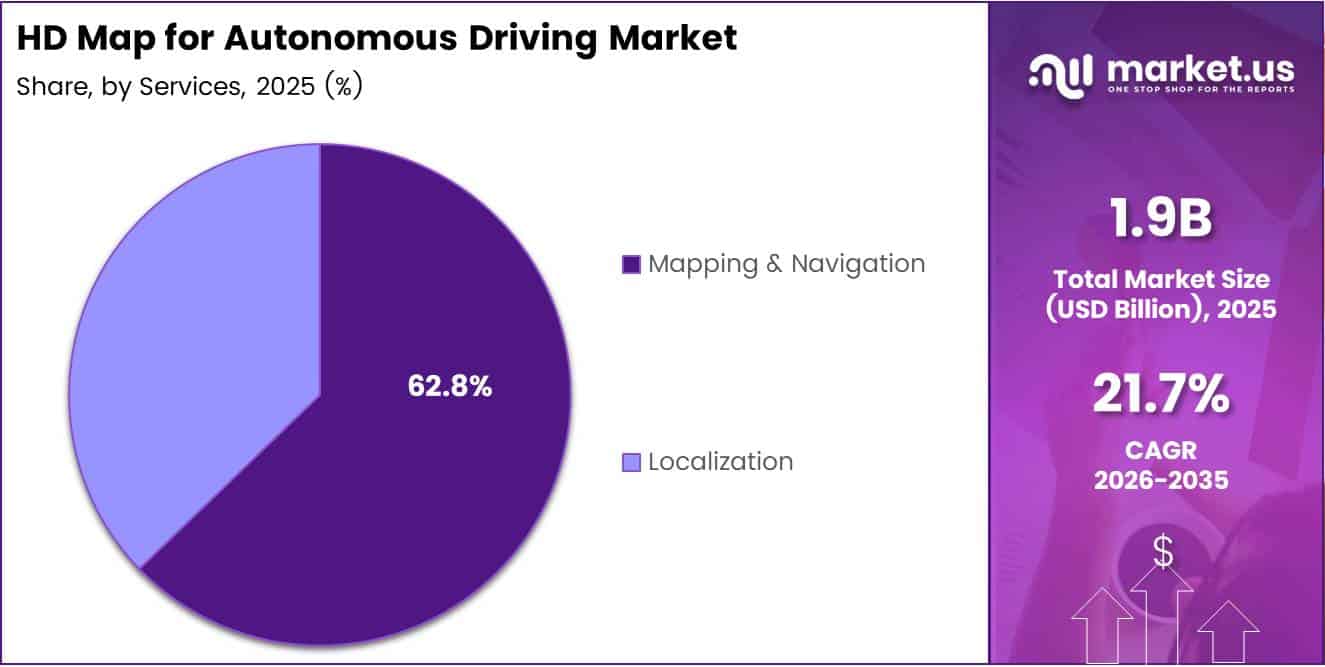

Global HD Map for Autonomous Driving Market size is expected to be worth around USD 13.5 Billion by 2035 from USD 1.9 Billion in 2025, growing at a CAGR of 21.7% during the forecast period 2026 to 2035.

HD maps deliver centimeter-level precision for autonomous vehicles. These digital mapping systems provide lane-level accuracy and real-time navigation data. Moreover, they enable safe path planning for self-driving cars across urban environments.

Autonomous driving platforms require high-definition cartography to function safely. HD maps combine LiDAR survey data with sensor fusion architectures. Additionally, they support localization systems that guide vehicles without human intervention.

Market expansion accelerates through Level 2 and Level 3 automation deployment. Passenger vehicles adopt advanced driver assistance systems rapidly. Consequently, automakers invest heavily in mapping infrastructure and connected vehicle technologies.

Cloud-based solutions dominate the mapping ecosystem with flexible scalability. Navigation services and localization capabilities drive commercial adoption. Furthermore, smart city initiatives create demand for real-time map updates and traffic intelligence.

Government regulations promote autonomous vehicle safety standards globally. Smart mobility policies encourage infrastructure development for self-driving technology. Therefore, urban planners integrate HD mapping into transportation modernization programs.

In early 2026, Waymo continued expanding autonomous driving operations following a $16 billion funding round that boosted its valuation to $126 billion. This investment signals strong market confidence in autonomous mobility platforms.

According to ISPRS research, Level 4/5 autonomous vehicles require positional accuracy of 0.1 meters at 95% confidence for safe operation. HD maps currently optimize to meet this benchmark in urban environments.

According to arXiv studies, autonomous vehicle localization systems using HD maps achieve approximately 8 cm positioning accuracy. This precision enables lane-level navigation and safe path planning in real-world driving conditions.

Key Takeaways

- Global HD Map for Autonomous Driving Market projected to reach USD 13.5 Billion by 2035 at 21.7% CAGR

- Cloud-Based solutions command 68.2% market share in solution segment

- L2 automation holds 39.6% share in level of automation segment

- Passenger vehicles dominate with 71.9% market share in vehicle type segment

- Mapping & Navigation services lead with 62.8% share in services segment

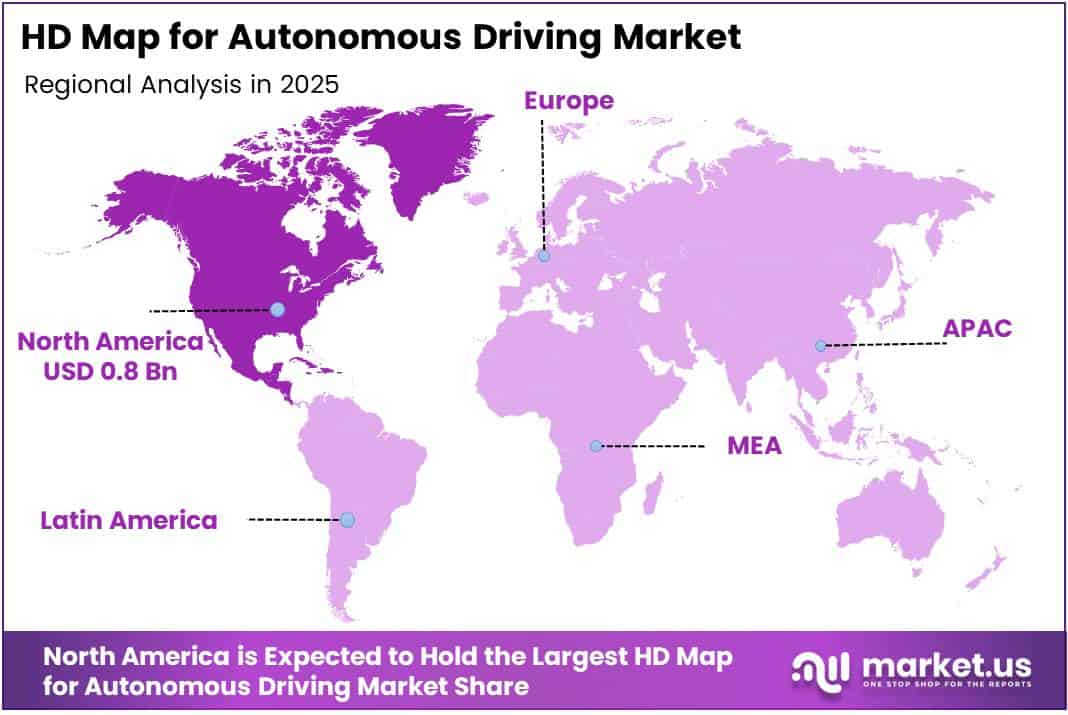

- North America dominates regional market with 45.80% share valued at USD 0.8 Billion

Solution Analysis

Cloud-Based dominates with 68.2% due to scalable infrastructure and real-time update capabilities.

In 2025, Cloud-Based held a dominant market position in the By Solution segment of HD Map for Autonomous Driving Market, with a 68.2% share. Cloud platforms enable continuous map updates and processing power for autonomous fleets. Moreover, they reduce onboard hardware requirements for connected vehicles. Therefore, automakers prefer cloud infrastructure for cost-effective deployment.

Embedded solutions provide offline navigation capabilities for autonomous systems. Onboard mapping processors deliver low-latency localization without network dependency. However, embedded architectures require frequent manual updates and higher storage capacity. Consequently, this segment serves applications where connectivity remains inconsistent or unreliable.

Level of Automation Analysis

L2 dominates with 39.6% due to widespread ADAS adoption in passenger vehicles.

In 2025, L2 held a dominant market position in the By Level of Automation segment of HD Map for Autonomous Driving Market, with a 39.6% share. Level 2 systems combine adaptive cruise control with lane-keeping assistance. Additionally, they represent the most commercially deployed autonomy level today. Therefore, automakers prioritize L2 mapping integration across mainstream vehicle models.

L3 automation enables conditional self-driving with driver oversight requirements. These systems demand higher precision mapping for safe handoff scenarios. Moreover, regulatory frameworks gradually approve L3 deployment in specific regions. Consequently, premium vehicle manufacturers invest in L3-compatible HD mapping infrastructure.

L4 systems deliver full autonomy within defined operational design domains. High-definition maps enable driverless operation in geofenced urban areas. However, L4 deployment remains limited to pilot programs and robotaxi services. Therefore, this segment grows through commercial autonomous mobility applications.

L5 represents complete autonomy without geographic or environmental limitations. Full self-driving capability requires comprehensive global mapping coverage and unlimited operational scenarios. Additionally, L5 development faces significant technical and regulatory challenges. Consequently, this segment remains in early research and development phases.

Vehicle Type Analysis

Passenger Vehicle dominates with 71.9% due to consumer demand for safety and convenience features.

In 2025, Passenger Vehicle held a dominant market position in the By Vehicle Type segment of HD Map for Autonomous Driving Market, with a 71.9% share. Private cars adopt autonomous technologies faster than commercial fleets. Moreover, passenger vehicles integrate ADAS and navigation systems as standard features. Therefore, automakers prioritize HD mapping for consumer vehicle platforms.

Commercial Vehicle applications focus on logistics, delivery, and public transportation. Autonomous trucks and shuttles require high-precision routing for efficiency gains. However, commercial deployment faces operational complexity and regulatory scrutiny. Consequently, this segment develops through targeted pilot programs and industrial applications.

Services Analysis

Mapping & Navigation dominates with 62.8% due to core positioning requirements for autonomous systems.

In 2025, Mapping & Navigation held a dominant market position in the By Services segment of HD Map for Autonomous Driving Market, with a 62.8% share. Navigation services deliver route planning and real-time traffic integration. Additionally, they provide lane-level guidance essential for safe autonomous operation. Therefore, mapping platforms prioritize navigation service development and continuous improvement.

Localization services enable precise vehicle positioning within HD map frameworks. Centimeter-level accuracy supports sensor fusion and path planning algorithms. Moreover, localization integrates LiDAR, camera, and GPS data for reliable positioning. Consequently, this segment grows through advanced perception system integration.

Key Market Segments

By Solution

- Cloud-Based

- Embedded

By Level of Automation

- L2

- L3

- L4

- L5

By Vehicle Type

- Passenger Vehicle

- Commercial Vehicle

By Services

- Mapping & Navigation

- Localization

Drivers

Rising Demand for Lane-Level Localization and Safety-Critical Autonomous Driving Capabilities

Autonomous vehicles require centimeter-accurate positioning for safe navigation decisions. Lane-level localization prevents unsafe lane departures and collision scenarios. Moreover, HD maps enable predictive path planning in complex traffic environments. Therefore, automakers prioritize precision mapping to meet safety certification requirements.

Advanced driver assistance systems depend on high-definition cartography for reliability. Sensor fusion architectures integrate map data with real-time perception inputs. Additionally, regulatory standards mandate specific accuracy thresholds for autonomous operation. Consequently, demand accelerates for mapping solutions that support safety-critical driving functions.

According to Financial Times data, human error causes over 42,000 U.S. traffic deaths annually as of 2022. This statistic strengthens the business case for HD-map-enabled autonomous systems designed to reduce driver mistakes and improve road safety outcomes.

Restraints

High Capital and Operational Cost of Continuous HD Map Data Collection, Processing, and Updates

HD mapping requires expensive LiDAR survey fleets and processing infrastructure. Data collection vehicles must continuously capture roadway changes and updates. Moreover, cloud processing demands significant computational resources and storage capacity. Therefore, mapping providers face substantial ongoing operational expenditures.

Map maintenance costs escalate with geographic coverage expansion and update frequency. Real-time change detection systems require constant monitoring and validation processes. Additionally, urban environments experience frequent infrastructure modifications requiring rapid map updates. Consequently, profitability challenges limit market entry for smaller mapping providers.

Standardization gaps create interoperability issues across autonomous vehicle platforms. Different automakers adopt incompatible map formats and data structures. Furthermore, regional variations in mapping protocols complicate global deployment strategies. Therefore, industry fragmentation increases costs and slows technology adoption.

Growth Factors

Integration of HD Maps with Smart Traffic Systems, V2X Networks, and Urban Mobility Platforms

Smart cities deploy connected infrastructure that communicates with autonomous vehicles. Vehicle-to-everything networks exchange real-time traffic and hazard information. Moreover, HD maps integrate this data to optimize routing and reduce congestion. Therefore, urban digitalization accelerates demand for intelligent mapping platforms.

Mobility-as-a-service platforms require precise mapping for efficient fleet operations. Robo-taxi services depend on HD maps for passenger pickup and route optimization. Additionally, autonomous logistics applications leverage mapping data for delivery scheduling. Consequently, commercial mobility operators drive mapping technology investments.

According to arXiv research, advanced perception frameworks reduce map matching processing time from 142 ms to approximately 39 ms. This improvement enhances real-time decision capability for autonomous navigation systems and operational efficiency.

Emerging Trends

Shift Toward Semantic HD Mapping Including Traffic Objects, Road Behavior, and Context Intelligence

Modern HD maps incorporate semantic layers beyond geometric road data. Traffic signal recognition and pedestrian behavior patterns enhance autonomous decision-making. Moreover, context-aware mapping enables vehicles to predict complex traffic scenarios. Therefore, mapping providers develop AI-driven semantic enrichment capabilities.

Blockchain technology secures map update integrity and data-sharing protocols. Distributed ledgers enable trusted crowdsourced mapping from connected vehicle fleets. Additionally, secure data exchanges protect proprietary mapping information between stakeholders. Consequently, blockchain adoption increases in autonomous mobility ecosystems.

According to Financial Times surveys, 66% of Americans fear self-driving technology as of 2024. This persistent consumer hesitation highlights the trust barrier HD map providers must address through transparency and demonstrated safety improvements.

Regional Analysis

North America Dominates the HD Map for Autonomous Driving Market with a Market Share of 45.80%, Valued at USD 0.8 Billion

North America leads autonomous vehicle development with 45.80% market share valued at USD 0.8 Billion. United States technology companies drive HD mapping innovation through substantial R&D investments. Moreover, regulatory frameworks support autonomous vehicle testing and deployment programs. Additionally, established automotive manufacturers partner with mapping providers to accelerate commercialization efforts.

Europe HD Map for Autonomous Driving Market Trends

Europe advances autonomous mobility through coordinated regulatory standards and smart city initiatives. Germany and France lead in automotive technology development and infrastructure modernization. Moreover, European Union policies promote connected vehicle ecosystems and digital transportation networks. Consequently, HD mapping adoption accelerates across major urban centers and highway corridors.

Asia Pacific HD Map for Autonomous Driving Market Trends

Asia Pacific experiences rapid autonomous vehicle deployment in China, Japan, and South Korea. Government investments in smart transportation infrastructure drive HD mapping demand. Moreover, technology companies develop proprietary mapping platforms for domestic markets. Therefore, regional growth outpaces other markets through aggressive commercialization strategies.

Latin America HD Map for Autonomous Driving Market Trends

Latin America explores autonomous vehicle technologies through pilot programs and partnerships. Brazil and Mexico attract international mapping providers seeking market expansion opportunities. However, infrastructure limitations and regulatory uncertainties slow widespread adoption. Consequently, market development focuses on urban mobility applications in major cities.

Middle East & Africa HD Map for Autonomous Driving Market Trends

Middle East and Africa invest in smart city projects incorporating autonomous transportation systems. Gulf Cooperation Council nations prioritize digital infrastructure and innovation-driven economic diversification. Moreover, South Africa develops autonomous vehicle testing frameworks and regulatory guidelines. Therefore, HD mapping opportunities emerge through government-led modernization initiatives.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

TomTom delivers comprehensive HD mapping solutions for automotive manufacturers globally. The company provides cloud-based map updates and navigation services for autonomous vehicles. Moreover, TomTom partners with major automakers to integrate precision mapping into production vehicle platforms. Consequently, the company maintains strong market position through established industry relationships and continuous technology innovation.

HERE Technologies operates as a leading provider of location intelligence and mapping platforms. The company develops open-standard HD maps supporting multiple autonomous vehicle architectures. Additionally, HERE Technologies collaborates with automotive consortiums to advance mapping interoperability. Therefore, its platform serves diverse customers across passenger and commercial vehicle segments.

Mapbox specializes in customizable mapping solutions and developer-friendly APIs for autonomous applications. The company enables real-time map customization and navigation experiences through cloud infrastructure. Moreover, Mapbox supports emerging mobility services including ride-hailing and delivery platforms. Consequently, it captures market share among technology-driven transportation companies.

Waymo combines autonomous driving expertise with proprietary HD mapping capabilities for robotaxi operations. In April 2025, UK AI startup Wayve secured its first major automotive collaboration with Nissan to integrate autonomous driving software starting in 2027. This partnership demonstrates growing demand for integrated mapping and autonomy solutions.

Key players

- TomTom

- HERE Technologies

- Mapbox

- Waymo

- Baidu (Apollo)

- Aptiv

- Huawei

Recent Developments

- October 2025 – Stellantis announced a global collaboration with NVIDIA, Uber Technologies, Inc., and Foxconn to jointly develop and deploy Level 4 (driverless) autonomous vehicles for robotaxi services worldwide, advancing commercial autonomous mobility infrastructure.

- October 2025 – NVIDIA announced a partnership with Uber to scale the world’s largest Level 4 autonomous mobility network using the NVIDIA DRIVE AGX Hyperion 10 platform and a joint AI data factory to curate robotaxi driving data.

- June 2025 – Waymo expanded its robotaxi operations to carry passengers in Atlanta as part of its partnership with Uber, further advancing commercial deployment of fully autonomous ride-hailing services across additional U.S. markets.

Report Scope

Report Features Description Market Value (2025) USD 1.9 Billion Forecast Revenue (2035) USD 13.5 Billion CAGR (2026-2035) 21.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Solution (Cloud-Based, Embedded), By Level of Automation (L2, L3, L4, L5), By Vehicle Type (Passenger Vehicle, Commercial Vehicle), By Services (Mapping & Navigation, Localization) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape TomTom, HERE Technologies, Mapbox, Waymo, Baidu (Apollo), Aptiv, Huawei Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  HD Map for Autonomous Driving MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

HD Map for Autonomous Driving MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- TomTom

- HERE Technologies

- Mapbox

- Waymo

- Baidu (Apollo)

- Aptiv

- Huawei

Our Clients

- 177488

- Feb 2026