Global Wax Emulsion Market Size, Share, And Enhanced Productivity By Material (Synthetic, Natural), By Product (Paraffin, Carnauba, Polyethylene, Polypropylene, Others), By End Use (Paints and Coatings, Adhesives and Sealants, Cosmetics, Textiles, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179596

- Number of Pages: 272

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

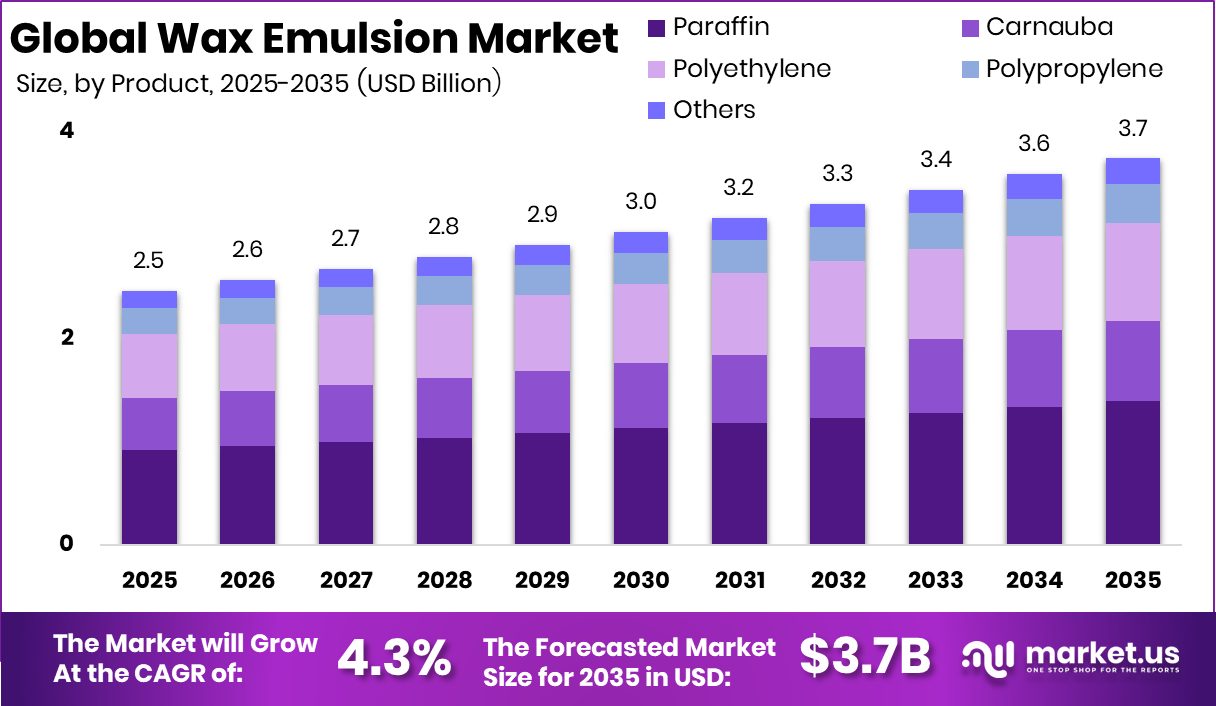

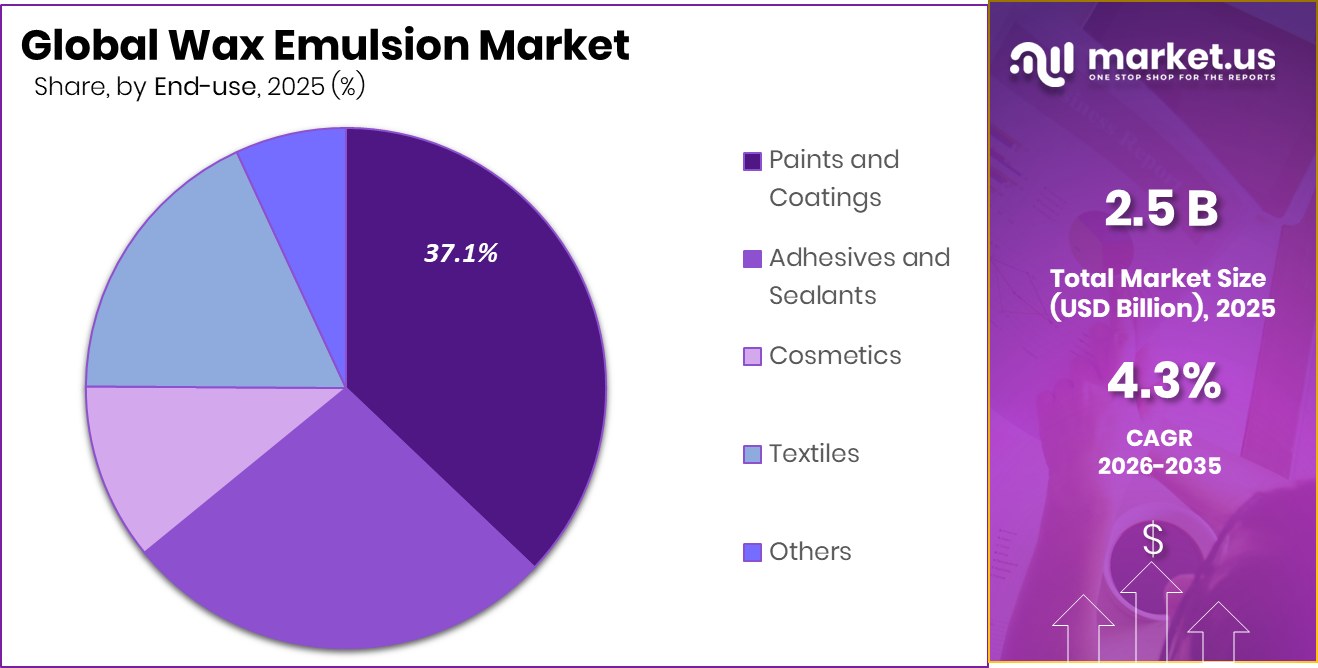

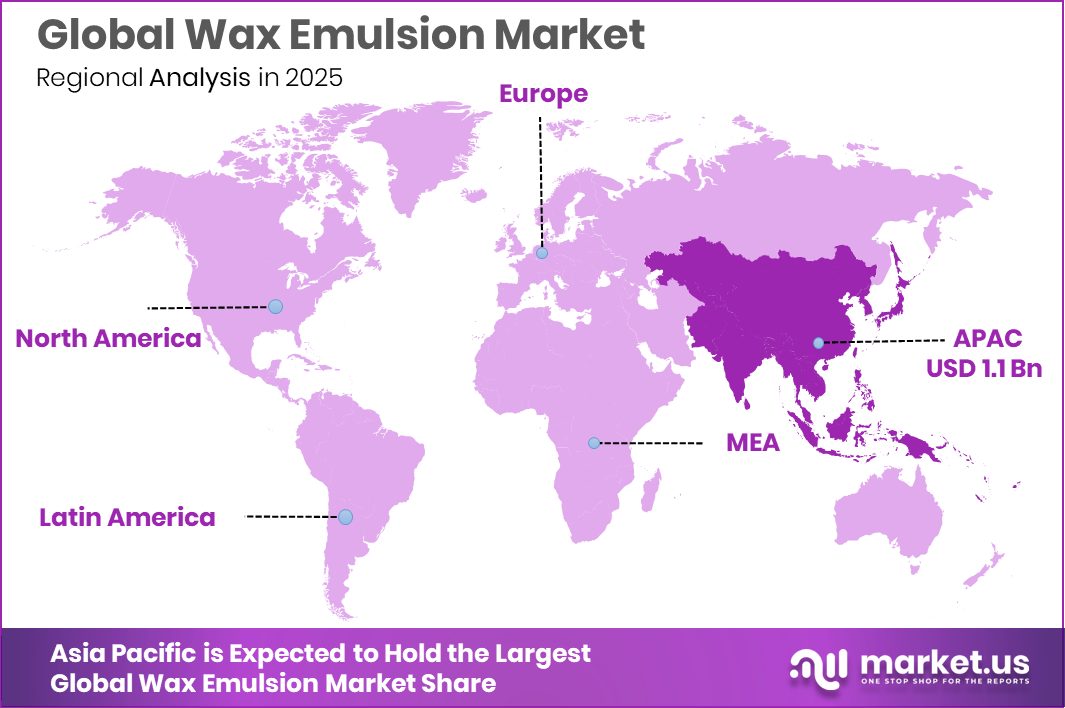

The Global Wax Emulsion Market is expected to be worth around USD 3.7 billion by 2035, up from USD 2.5 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035. Strong industrial growth pushed the Asia Pacific Wax Emulsion Market to 44.8% and USD 1.1 Bn.

The global Wax Emulsion Market is shaped by two key material categories—synthetic and natural—along with a broad product mix that includes paraffin, carnauba, polyethylene, polypropylene, and specialty blends. End-use demand is anchored in paints and coatings, adhesives and sealants, cosmetics, textiles, and several industrial processes. Wax emulsions are stable dispersions formed by breaking wax into fine particles within water, creating a smooth, versatile material used to improve surface protection, slip, gloss control, and moisture resistance. The Wax Emulsion Market represents the commercial ecosystem around production, supply, and application of these emulsions across multiple manufacturing sectors.

Growth in this market is supported by rising adoption of water-based systems, the need for improved surface performance, and the continued shift away from solvent-heavy formulations. Industry-wide developments—such as Ecoat securing €21 million to reinvent the future of paint—indicate strong momentum for advanced coatings that increasingly rely on high-quality wax emulsions.

Demand also benefits from ongoing consolidation and restructuring in the coatings value chain, highlighted by Nippon Paint Holdings entering a $2.3 billion deal for AOC and major portfolio adjustments such as BASF initiating a €6 billion coatings business sale, later reported at valuations around $6.8 billion, and considering a possible €7 billion divestment to Carlyle due to energy-related pressures.

Additional opportunities arise from strengthened distribution and raw-material networks, reflected in Univar Solutions being acquired by Apollo Funds for $8.1 billion, signalling deeper investment flows into chemical supply platforms that support wax emulsion ingredients and applications.

Key Takeaways

- The Global Wax Emulsion Market is expected to be worth around USD 3.7 billion by 2035, up from USD 2.5 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035.

- Synthetic wax emulsions dominate the Wax Emulsion Market, capturing 68.4% due to reliable performance.

- Paraffin wax emulsions hold 37.2%, driving the Wax Emulsion Market through cost-effective formulation benefits.

- Paints and coatings segment leads the Wax Emulsion Market with 37.1% driven by surface protection needs.

- The Wax Emulsion Market in the Asia Pacific reached USD 1.1 Bn with 44.8%.

By Material Analysis

Growing industrial applications further strengthen synthetic materials’ 68.4% share in the expanding Wax Emulsion Market.

In 2025, the Wax Emulsion Market continues to witness strong dominance of synthetic materials, holding nearly 68.4% of the total share due to their consistent performance, stability, and compatibility across diverse industrial applications. Manufacturers prefer synthetic wax emulsions for their enhanced water resistance, abrasion protection, and smooth film-forming ability, which strengthens their adoption in coatings, adhesives, textiles, and packaging sectors.

Growing emphasis on high-quality surface finishing in the construction and automotive industries further accelerates demand. At the same time, rising innovations in high-performance emulsion formulations are supporting expansion in both developed and emerging markets. Synthetic wax emulsions remain the most reliable option for industrial-scale use, driven by cost efficiency, technical benefits, and continuous product improvement.

By Product Analysis

With 37.2% share, paraffin remains essential in the Wax Emulsion Market across multiple applications.

In 2025, paraffin-based wax emulsions secure a significant position in the Wax Emulsion Market, accounting for around 37.2% of the product segment. Their wide availability, cost-friendly production, and versatile functional properties make them a preferred choice in paper, packaging, cosmetics, leather finishing, and industrial coatings. The ability of paraffin emulsions to enhance barrier properties, reduce moisture absorption, and improve surface functionality contributes to their consistent adoption across manufacturing environments.

Growing demand for better printability and water repellency in packaging materials further strengthens their use. Additionally, industries focused on improving material durability and processing efficiency continue to lean toward paraffin emulsions, reinforcing their role as a staple product type within the global wax emulsion landscape.

By End Use Analysis

The Wax Emulsion Market expands as paints and coatings utilize 37.1% for enhanced performance.

In 2025, the paints and coatings sector remains the leading end-use segment in the Wax Emulsion Market, representing nearly 37.1% of total consumption. Increasing demand for scratch resistance, anti-blocking performance, improved texture, and enhanced surface protection drives extensive adoption in architectural, industrial, automotive, and wood coatings. The shift toward water-based and eco-friendly formulations further boosts the relevance of wax emulsions as manufacturers seek safer, low-VOC additives.

Rising construction activities, interior refurbishment trends, and infrastructure spending across Asia-Pacific and North America also support market expansion. Wax emulsions continue to deliver critical functional advantages such as gloss control, slip enhancement, and long-term coating durability, making them essential across modern coating formulations.

Key Market Segments

By Material

- Synthetic

- Natural

By Product

- Paraffin

- Carnauba

- Polyethylene

- Polypropylene

- Others

By End Use

- Paints and Coatings

- Adhesives and Sealants

- Cosmetics

- Textiles

- Others

Driving Factors

Rising demand for advanced water-based coatings

The Wax Emulsion Market continues to grow as industries shift toward cleaner, water-based coating systems, with demand rising in paints, textiles, paper finishing, and packaging. The move toward safer formulations encourages manufacturers to adopt wax emulsions for better surface performance, moisture resistance, and improved durability.

Market momentum is further supported by technological progress across the materials ecosystem, reflected in funding milestones such as Citrine Informatics raising $16M in a Series C round, highlighting broader innovation in material science and formulation development. As sustainability expectations strengthen, users across construction, automotive, and consumer goods increasingly rely on wax emulsions to elevate performance while meeting regulatory pressure to reduce solvent-based coatings.

Restraining Factors

High production costs limit market expansion

Despite healthy demand, the Wax Emulsion Market faces cost-related challenges that slow broader adoption. Price volatility in raw materials, energy inputs, and specialized emulsifiers results in higher production costs, making it difficult for smaller manufacturers to keep pace with large-scale industrial demands. These cost pressures often impact the profitability of end-use sectors such as textiles, adhesives, and industrial coatings.

A related industry event that reflects ongoing cost and technology pressures is Tissium securing €50M to expand its nerve and hernia repair technologies, showing how capital continues flowing toward high-performance material innovation. Similar investment surges raise expectations for advanced chemistry, making price competitiveness a critical restraint within wax emulsions.

Growth Opportunity

Expanding applications in sustainable coating technologies

Opportunities continue to expand as manufacturers look for sustainable coating technologies that balance performance and environmental responsibility. Wax emulsions offer strong potential in low-VOC formulations, premium surface finishes, and next-generation industrial coatings designed for packaging, automotive parts, and engineered materials. The growing push for circular material systems strengthens the need for improved wax-based dispersions.

Industry momentum is also influenced by breakthroughs in the material science ecosystem, demonstrated by Albert Invent raising $7.5M in seed funding to advance software for material innovation. These developments indicate wider opportunities for companies looking to refine formulation performance, reduce environmental impact, and create value-added coating solutions.

Latest Trends

Shift toward bio-based wax emulsion formulations

Recent trends show a strong shift toward bio-based wax emulsion formulations, driven by environmental expectations and the need to replace petroleum-heavy inputs. Industries are exploring natural wax sources and hybrid blends that deliver slip, abrasion protection, and moisture resistance while reducing environmental footprint. This shift is reinforced by advancements in biomaterial research, including funding events such as Cohera Medical securing $26.3M in a Series D round to expand its in-body adhesive innovations.

Though not directly related to coatings, such funding demonstrates rising global interest in bio-engineered material systems. Together, these trends push the Wax Emulsion Market toward cleaner chemistries, innovative formulation pathways, and long-term sustainability.

Regional Analysis

Asia Pacific held 44.8% share, driving the Wax Emulsion Market to USD 1.1 Bn.

In the Wax Emulsion Market, regional performance shows clear variation across key global zones, with Asia Pacific emerging as the dominant region, accounting for 44.8% of total market share and generating approximately USD 1.1 billion in value. This strong lead is supported by rising industrial output, expanding construction activity, and the rapid growth of coatings, textiles, and packaging sectors across major economies.

In contrast, North America maintains steady demand driven by mature coatings and paper industries, while Europe reflects consistent consumption supported by established manufacturing hubs and regulatory shifts toward water-based formulations. Latin America continues to show gradual adoption as industrial activities expand across developing markets.

Meanwhile, the Middle East & Africa region benefits from rising infrastructure development and increasing use of protective coatings. Although all regions contribute meaningfully, the Asia Pacific clearly sets the pace with its higher production capacities, strong manufacturing base, and large-scale industrial consumption, reinforcing its leadership position within the overall market structure.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, BASF SE continues to strengthen its position in the global Wax Emulsion Market through its broad chemical expertise and advanced formulation capabilities. The company’s portfolio aligns with growing demand for high-performance emulsions used in coatings, adhesives, and packaging, supported by consistent innovation in water-based and environmentally conscious solutions. BASF’s strong global manufacturing footprint enables reliable supply, while its focus on application-specific performance gives it an edge in markets requiring superior film formation, abrasion resistance, and sustainability-driven upgrades.

Nippon Seiro Co. maintains a strategic role in the market, leveraging its long-standing specialization in wax-based products and consistent quality standards. The company benefits from stable demand across Asia, supported by its ability to supply paraffin and microcrystalline wax emulsions tailored for paper, packaging, and surface-treatment industries. Its technology-driven approach and commitment to controlled production processes ensure compatibility with customer specifications, reinforcing its relevance as industries shift toward precise formulation requirements and high-purity wax applications.

Altana AG demonstrates strong growth potential through its focus on specialty additives and performance-enhancing wax emulsions. The company’s expertise in coatings, inks, and plastics supports expanding adoption across high-value industrial segments. Its emphasis on surface modification, abrasion improvement, and slip enhancement positions Altana as a preferred supplier for manufacturers seeking advanced functional benefits. With a reputation for technical excellence and consistent product development, Altana remains a key player shaping innovation trends in the 2025 global wax emulsion landscape.

Top Key Players in the Market

- BASF SE

- Nippon Seiro Co.

- Altana AG

- Sasol Limited

- Exxon Mobil Corporation

- Hexion

- The Lubrizol Corporation

- Danquinsa GmbH

- RAZON CONSTRUCTION CHEMICALS

- Khavaran Paraffin

Recent Developments

- In March 2025, BASF introduced Joncryl® Wax 30, a new polyethylene wax emulsion designed for use in food packaging inks and overprint varnishes (OPVs). This product improves rub resistance, gloss, and clarity for packaging applications and replaces an earlier equivalent, helping customers meet durability and performance needs in packaging films and paperboard coatings.

- In October 2024, Nippon Seiro was featured in an international business overview for its leadership and innovative work in the wax industry. The company’s emphasis on diverse, eco-friendly products and long-term strategy was highlighted in this coverage.

Report Scope

Report Features Description Market Value (2025) USD 2.5 Billion Forecast Revenue (2035) USD 3.7 Billion CAGR (2026-2035) 4.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Synthetic, Natural), By Product (Paraffin, Carnauba, Polyethylene, Polypropylene, Others), By End Use (Paints and Coatings, Adhesives and Sealants, Cosmetics, Textiles, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, Nippon Seiro Co., Altana AG, Sasol Limited, Exxon Mobil Corporation, Hexion, The Lubrizol Corporation, Danquinsa GmbH, RAZON CONSTRUCTION CHEMICALS, Khavaran Paraffin Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BASF SE

- Nippon Seiro Co.

- Altana AG

- Sasol Limited

- Exxon Mobil Corporation

- Hexion

- The Lubrizol Corporation

- Danquinsa GmbH

- RAZON CONSTRUCTION CHEMICALS

- Khavaran Paraffin

Our Clients

- 179596

- February 2026