Quick Navigation

Report Overview

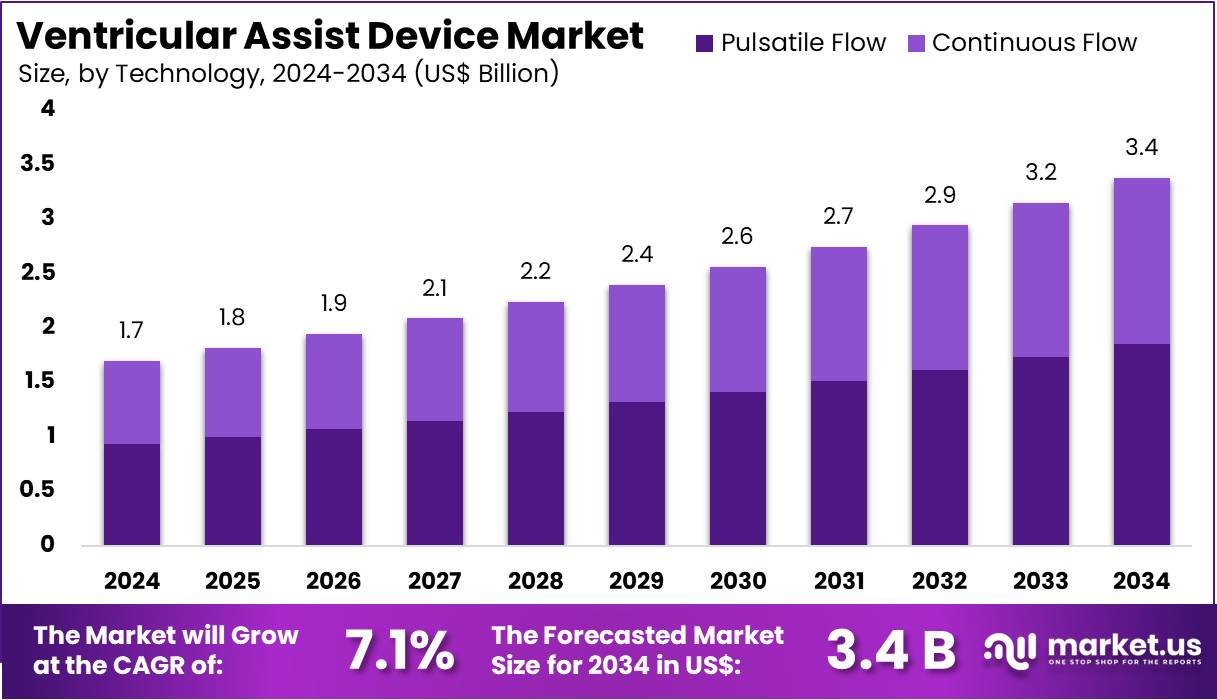

The Ventricular Assist Device Market size is expected to be worth around US$ 3.4 billion by 2034 from US$ 1.7 billion in 2024, growing at a CAGR of 7.1% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 44.2% share and holds US$ 0.8 Billion market value for the year.

Increasing prevalence of heart failure and advancements in cardiac care drive the growth of the ventricular assist device (VAD) market. As the global population ages and the incidence of heart disease rises, the demand for devices that aid in pumping blood and enhancing heart function continues to grow. VADs play a critical role in supporting patients with severe heart failure, providing a solution for those who are not candidates for a heart transplant.

Technological innovations in VADs, such as smaller, more durable devices with improved battery life and enhanced biocompatibility, create opportunities for broader adoption and increased patient comfort. According to the Journal of Cardiac Failure’s 2023 report, approximately 6.7 million adults in the US are currently living with heart failure, a number projected to rise to 8.5 million by 2030, highlighting the increasing burden of this condition. The rise in heart failure cases contributes to the growing demand for VADs, as they help prolong patients’ lives and improve their quality of life while awaiting a transplant.

Key Takeaways

- In 2023, the market for qeyword generated a revenue of US$ 1.7 billion, with a CAGR of 7.1%, and is expected to reach US$ 3.4 billion by the year 2033.

- The product type segment is divided into total artificial heart, right ventricular assist device, left ventricular assist device, and bi-ventricular assist device, with left ventricular assist device taking the lead in 2023 with a market share of 40%.

- Considering technology, the market is divided into pulsatile flow and continuous flow. Among these, pulsatile flow held a significant share of 55%.

- Furthermore, concerning the application segment, the market is segregated into destination therapy, bridge to transplant, and others. The destination therapy sector stands out as the dominant player, holding the largest revenue share of 50% in the qeyword market.

- The end-user segment is segregated into hospitals, specialty clinics, and others, with the hospitals segment leading the market, holding a revenue share of 60%.

- North America led the market by securing a market share of 44.2% in 2023.

Product Type Analysis

The left ventricular assist device segment led in 2023, claiming a market share of 40% owing to the increasing incidence of heart failure and the rising number of patients with left ventricular dysfunction. LVADs are anticipated to remain a critical treatment option for patients who are not candidates for a heart transplant or as a bridge to transplant.

The growing adoption of LVADs for managing chronic heart failure, along with advances in device design that offer greater efficiency, reliability, and patient comfort, is likely to drive the demand for these devices. Additionally, as healthcare systems focus on improving patient outcomes and reducing hospital readmissions, LVADs are projected to see increased use in both short-term and long-term heart failure management, contributing to the segment’s growth.

Technology Analysis

The pulsatile flow held a significant share of 55% as advancements in pulsatile flow technology offer improved hemodynamic performance and mimic the natural heartbeat. Pulsatile flow devices are expected to remain important in specific clinical scenarios, such as long-term heart failure treatment and as a bridge to heart transplants.

The physiological benefits of pulsatile flow, including better organ perfusion and reduced risk of thrombosis compared to continuous flow devices, are anticipated to drive the adoption of pulsatile flow devices. Although continuous flow devices have gained popularity due to their smaller size and energy efficiency, the continued demand for pulsatile flow technology in critical care is expected to fuel growth in this segment as patients and healthcare providers seek the most effective long-term heart support solutions.

Application Analysis

The destination therapy segment had a tremendous growth rate, with a revenue share of 50% as an increasing number of heart failure patients are ineligible for heart transplants. Destination therapy, which involves the use of ventricular assist devices as a long-term therapy rather than a bridge to transplant, is projected to gain traction as patients with end-stage heart failure seek alternatives to traditional heart transplantation. The growth of this segment is anticipated to be driven by advancements in LVAD technology, which have improved device longevity and patient outcomes.

As healthcare systems prioritize quality of life for heart failure patients, the demand for destination therapy options is likely to rise, particularly as the donor organ shortage continues to limit heart transplants. The growing focus on chronic heart failure management is expected to drive the expansion of the destination therapy segment.

End-user Analysis

The hospitals segment grew at a substantial rate, generating a revenue portion of 60% as hospitals remain the primary location for implanting and managing ventricular assist devices. The increasing prevalence of heart failure and the growing number of patients requiring advanced heart support devices, including LVADs, are expected to drive the demand for these devices in hospital settings.

Hospitals are likely to continue being the main providers of care for patients who require surgical implantation, monitoring, and long-term management of ventricular assist devices. Additionally, the increasing focus on improving patient outcomes and reducing hospital readmissions in heart failure management is expected to boost the adoption of these devices in hospitals. As hospitals continue to invest in advanced cardiac care technologies, the demand for ventricular assist devices in these settings is anticipated to continue growing.

Key Market Segments

By Product Type

- Total Artificial Heart

- Right Ventricular Assist Device

- Left Ventricular Assist Device

- Bi-Ventricular Assist Device

By Technology

- Pulsatile Flow

- Continuous Flow

By Application

- Destination Therapy

- Bridge to Transplant

- Others

By End-user

- Hospitals

- Specialty Clinics

- Others

Drivers

Increasing Incidence of Heart Failure is Driving the Market

The rising prevalence of heart failure significantly drives the ventricular assist device (VAD) market. Heart disease remains a leading cause of mortality globally, with the Centers for Disease Control and Prevention (CDC) reporting that approximately 6.2 million adults in the US have heart failure as of 2023. This high incidence underscores the critical need for advanced cardiac support solutions like VADs. VADs play a vital role in supporting heart function and blood flow in patients with weakened hearts, improving survival rates and quality of life.

As the number of heart failure cases continues to increase, the demand for VADs is expected to grow, further propelling market expansion. The adoption of VAD technology is also bolstered by the increasing awareness of heart failure and the growing acceptance of mechanical circulatory support. As healthcare systems continue to invest in innovative solutions, the market for VADs will likely continue to see growth, offering life-saving benefits to a broader patient base. This increasing demand for heart failure management is expected to sustain the market’s positive trajectory.

Restraints

Product Recalls and Safety Concerns are Restraining the Market

Despite their life-saving potential, the VAD market faces challenges related to product recalls and safety concerns. In recent years, several recalls have been issued for left ventricular assist devices (LVADs) due to mechanical failures and safety issues. These include recalls for products like the HeartWare VAD and HeartMate II, which were due to risks like driveline connector looseness and system controller failures. Such safety concerns can reduce patient and healthcare provider confidence, potentially limiting market growth.

The risks associated with device failure can also lead to longer recovery times and additional procedures for patients, further exacerbating the burden. These incidents can significantly affect consumer trust and restrict the widespread adoption of VADs. To overcome these challenges, there is a pressing need for more robust post-market surveillance, continuous monitoring of device safety, and improvements in VAD technology to enhance reliability. Addressing these issues effectively will be key to ensuring broader acceptance and accelerating market growth.

Opportunities

Technological Advancements in VAD Design are Creating Growth Opportunities

Advancements in VAD technology present significant growth opportunities in the market. The development of continuous-flow devices has enhanced efficiency, reduced size, and improved patient outcomes. These innovations not only make VADs more efficient but also improve patient mobility and comfort, as smaller and lighter devices are now available. Furthermore, improvements in battery life and wireless monitoring capabilities have made these devices more convenient and effective for long-term use.

The development of more durable VADs has expanded their applicability, providing heart failure patients with a long-term solution that improves their quality of life. The integration of advanced materials and biocompatible components has further enhanced the safety and performance of VADs. These technological innovations contribute to increasing the accessibility and acceptance of VADs by offering patients safer, more effective, and less invasive treatment options. As these devices continue to improve, they are expected to attract more patients and healthcare providers, fostering continued market growth.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the VAD market. Economic downturns can lead to reduced healthcare budgets, limiting access to advanced cardiac therapies like VADs. Financial constraints in healthcare systems slow down the adoption of new technologies, making it harder for healthcare providers to invest in cutting-edge treatments.

On the other hand, economic growth and rising disposable incomes lead to greater investments in healthcare, boosting the demand for advanced medical technologies like VADs. Geopolitical stability facilitates global trade and distribution, ensuring the availability of these devices across multiple regions. However, geopolitical tensions and trade barriers can disrupt supply chains, affecting the availability of critical components for VADs, thereby slowing market growth.

Additionally, varying regulatory standards across countries impact the approval and monitoring processes for VADs, which can create delays or complications in their market entry. Despite these challenges, technological advancements in VAD design and a growing global emphasis on improving heart failure management will continue to drive the market forward. With continued innovation and better access to healthcare, the market outlook remains positive, even in the face of macroeconomic and geopolitical uncertainties.

Latest Trends

Shift Towards Destination Therapy is a Recent Trend in the Market

A notable recent trend in the VAD market is the shift towards destination therapy, where VADs are used as a long-term solution for patients who are not candidates for heart transplantation. This approach expands the patient base for VADs beyond those awaiting transplants, creating new opportunities for growth in the market.

Destination therapy offers a viable solution for patients with advanced heart failure who are ineligible for a transplant due to factors such as age or comorbid conditions. The development of more reliable and durable VADs has made destination therapy a feasible option for many patients, improving survival rates and overall quality of life.

This trend reflects a broader shift towards personalized medicine, where treatment plans are customized to meet the specific needs and circumstances of individual patients. As more healthcare providers adopt destination therapy, the VAD market will likely continue to expand, offering life-saving alternatives for those who previously had limited treatment options. This growing shift towards long-term mechanical support is expected to play a crucial role in the future of the VAD market.

Regional Analysis

North America is leading the Ventricular Assist Device Market

North America dominated the market with the highest revenue share of 44.2% owing to several key factors. A major contributor was the increasing prevalence of cardiovascular diseases, leading to a higher demand for advanced cardiac support devices. Technological advancements also played a crucial role; the development of continuous-flow VADs improved patient outcomes and expanded the patient population eligible for these devices.

Moreover, the aging population in North America, with a higher incidence of heart failure, further fueled the demand for VADs. Healthcare policies and reimbursement frameworks in the region have increasingly supported the adoption of these life-saving devices, making them more accessible to patients in need.

Additionally, the presence of leading medical device manufacturers, such as Abbott Laboratories and Medtronic, has fostered innovation and competition, resulting in more advanced and cost-effective VAD options. These factors collectively contributed to the robust growth trajectory of the VAD market in North America throughout 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing burden of cardiovascular diseases, particularly in countries like China and India, which have large patient populations. China accounted for a significant portion of the global left ventricular assist device market revenue in 2024, with expectations of continued growth. The demand for advanced cardiac support devices is expected to rise with the aging population and the adoption of Western lifestyles.

Healthcare infrastructure improvements and increased healthcare spending are likely to facilitate the adoption of sophisticated VAD technologies. Government initiatives aimed at enhancing healthcare access and quality are projected to support market expansion. Collaborations between international medical device manufacturers and local healthcare providers are expected to introduce innovative VAD solutions tailored to the regional market. These factors are likely to contribute to the significant growth of the VAD market in the Asia-Pacific region during the forecast period.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the ventricular assist device (VAD) market focus on technological innovation, strategic collaborations, and expanding global reach to drive growth. They invest in research and development to improve device efficiency, durability, and patient outcomes, making these devices more accessible and effective for heart failure patients.

Companies also form partnerships with hospitals, research centers, and healthcare organizations to enhance product adoption and gather clinical data. Expanding into emerging markets with rising healthcare needs and increasing awareness of heart failure treatment further boosts market penetration. Regulatory approvals and continuous advancements in minimally invasive VADs help maintain competitiveness in the evolving market.

Medtronic, headquartered in Dublin, Ireland, is a global leader in medical devices, including those for cardiovascular care. The company’s HeartWare ventricular assist system (HVAD) is designed for patients with severe heart failure, offering an advanced solution to improve heart function. Medtronic focuses on expanding its VAD portfolio through innovation and strategic partnerships with healthcare providers and research institutions. Its global presence, combined with ongoing R&D efforts, positions the company as a dominant player in the heart failure treatment space.

Top Key Players in the Ventricular Assist Device Market

- Sun Medical Technology Research Corp

- ReliantHeart

- Medtronic

- Jarvik Heart

- Cardiac Assist

- Berlin Heart

- Abiomed

- Abbott

Recent Developments

- In August 2022, Abbott revealed that patients receiving its HeartMate 3 left ventricular assist device experienced improved survival rates, leading to an anticipated increase in the device’s adoption and use in clinical practice.

- In September 2021, Abbott collaborated with Cereno Scientific to integrate its advanced CardioMEMS technology in a Phase II clinical study of CS1, aimed at addressing pulmonary arterial hypertension and thrombotic conditions, marking a significant step in innovative cardiovascular treatment options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.7 billion |

| Forecast Revenue (2034) | US$ 3.4 billion |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Total Artificial Heart, Right Ventricular Assist Device, Left Ventricular Assist Device, and Bi-Ventricular Assist Device), By Technology (Pulsatile Flow and Continuous Flow), By Application (Destination Therapy, Bridge to Transplant, and Others), By End-user (Hospitals, Specialty Clinics, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Sun Medical Technology Research Corp, ReliantHeart, Medtronic, Jarvik Heart, Cardiac Assist, Berlin Heart, Abiomed, and Abbott. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |