Global Transmission Fluids Market Size, Share, And Enhanced Productivity By Base Oil (Mineral Oil, Semi-synthetic, Synthetic), By Viscosity (Low Viscosity, High Viscosity), By Transmission Type (Automatic, Manual, Continuously Variable, Dual Clutch, Electric), By Vehicle (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Off Road Vehicles), By Sales Channel (Factory Fill, Service Fill(Authorized Service Outlets, Independent Garages)), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180093

- Number of Pages: 398

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

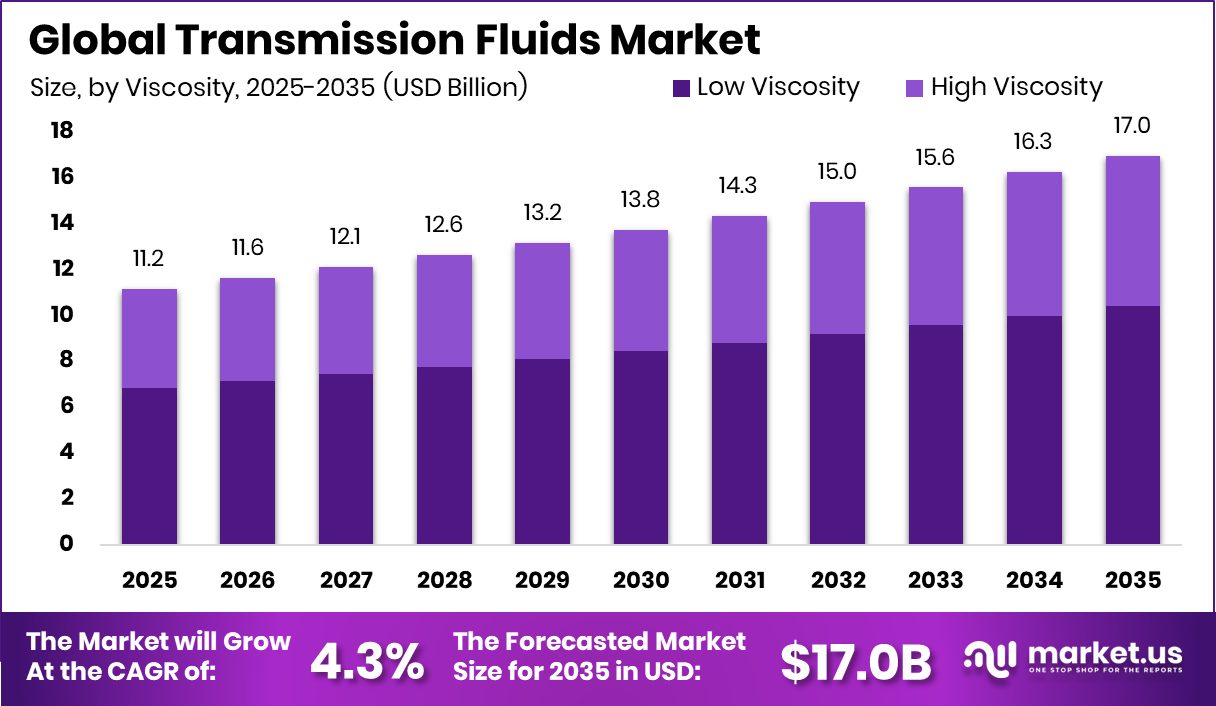

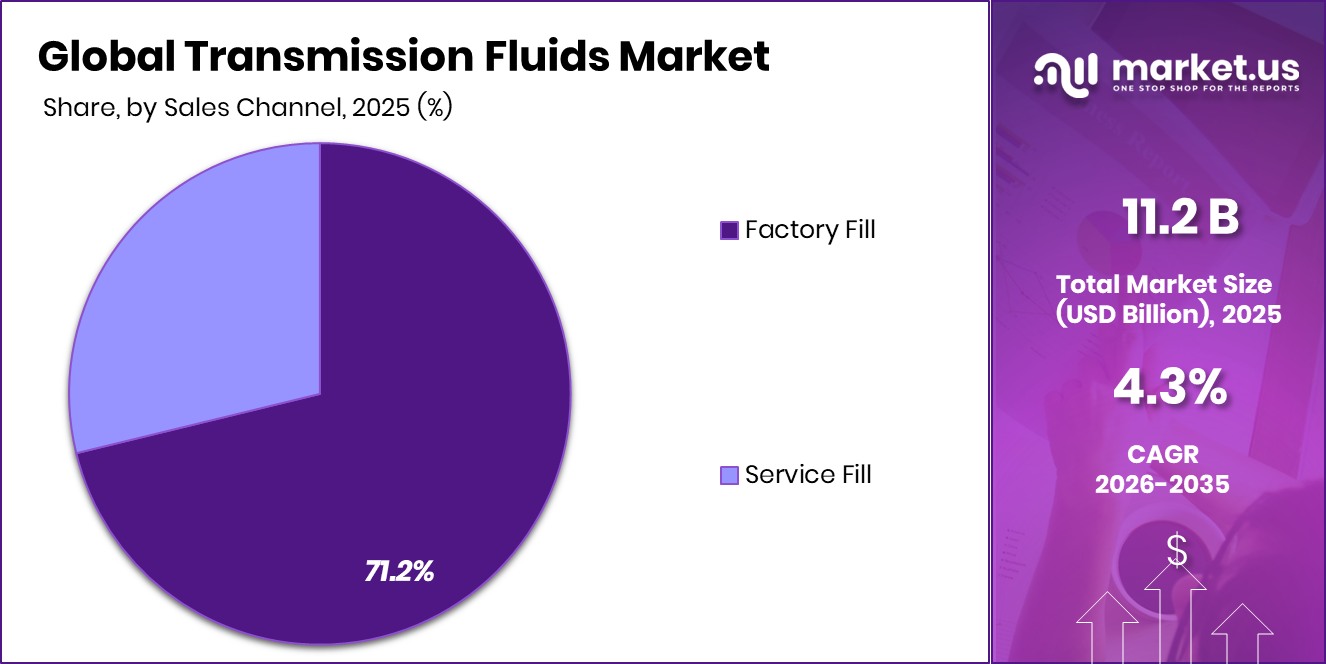

The Global Transmission Fluids Market is expected to be worth around USD 17.0 billion by 2035, up from USD 11.2 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035. Growing vehicle servicing demand supports the Asia Pacific Transmission Fluids Market at 43.8%, USD 4.9 Bn.

Transmission fluids are specialized lubricating liquids used inside vehicle transmission systems to ensure smooth gear shifting, reduce friction, and protect internal components from heat and wear. These fluids play an important role in maintaining transmission efficiency and durability in both automatic and manual vehicles. They also support cooling, hydraulic pressure control, and corrosion protection within the transmission assembly. Because modern vehicles use different transmission technologies such as automatic, dual-clutch, and continuously variable systems, transmission fluids are developed with different base oils, including mineral, semi-synthetic, and synthetic formulations.

The Transmission Fluids Market represents the global demand and supply of these specialized lubricants used in passenger cars, commercial vehicles, and off-road machinery. The market includes products designed for several transmission systems such as automatic, manual, continuously variable, dual clutch, and electric transmissions. Fluids are supplied through factory fill during vehicle manufacturing and through service fill during vehicle maintenance. As vehicles operate over long periods, transmission fluids require periodic replacement to maintain system performance, making maintenance services an important part of this market.

One of the major growth drivers is the ongoing development of automotive technology and related infrastructure investments. Governments and institutions are increasing funding for research, engineering, and infrastructure development. For instance, McGill researchers received $9.7 million in CFI funding, while Fluid Wire Robotics secured a €2.5 million EIC Accelerator grant to advance robotics technology. Large-scale infrastructure financing, including over Shs 5 trillion in loan proposals for road, power, and agricultural development, also contributes to increased vehicle movement and machinery use.

Strong demand for transmission fluids is closely linked to the expanding global vehicle fleet and routine automotive servicing. Passenger vehicles, commercial fleets, and off-road equipment require regular maintenance to ensure reliable transmission performance. Community and industrial initiatives also influence industrial growth. For example, BASF donated $39,000 to United Way, highlighting industry involvement in broader development activities that support local economies and mobility needs.

Looking ahead, several opportunities are emerging for transmission fluid development, particularly as modern vehicles adopt advanced transmission systems and electrified drivetrains. Investments in power infrastructure and energy networks continue to influence transportation and automotive activity. However, policy changes can also affect infrastructure expansion, as seen when a $1 billion investment in the Georgia power grid faced delays following a funding freeze. Such developments shape the broader environment in which vehicle usage and maintenance needs evolve.

Key Takeaways

- The Global Transmission Fluids Market is expected to be worth around USD 17.0 billion by 2035, up from USD 11.2 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035.

- In the Transmission Fluids Market, Mineral Oil dominated base oil segment with 47.3% share due to cost efficiency.

- In the Transmission Fluids Market, Low Viscosity fluids led viscosity segment with 61.4% share improving fuel efficiency.

- In the Transmission Fluids Market, the automatic transmission type held a 48.1% share as the adoption of automatic vehicles continues rising.

- In the Transmission Fluids Market, Passenger Cars dominated the vehicle segment with 59.7% share due to growing car ownership.

- In the Transmission Fluids Market, Service Fill sales channel captured 71.2% share, supported by frequent vehicle maintenance demand.

- Strong automotive production helps Asia Pacific secure a 43.8% share, totaling USD 4.9 Bn.

By Base Oil AnalysisThe

Transmission Fluids Market sees Mineral Oil dominating the base oil segment with 47.3% share.

In 2025, Mineral Oil held a dominant position in the Transmission Fluids Market, accounting for nearly 47.3% of the total share. Mineral-based transmission fluids continue to remain widely used across automotive applications due to their reliable lubrication properties and relatively lower production cost. Many vehicle owners and service providers still prefer mineral oil fluids for conventional vehicles because they provide stable performance under moderate operating conditions.

In developing automotive markets, where cost sensitivity plays a major role, mineral oil-based transmission fluids remain a practical choice for passenger cars and light commercial vehicles. Their compatibility with older transmission systems also supports ongoing demand. Automotive workshops and fleet operators often select mineral-based formulations for routine servicing, which keeps this segment active in both OEM recommendations and aftermarket maintenance activities across global transportation networks.

By Viscosity Analysis

Transmission Fluids Market shows Low Viscosity fluids leading demand with 61.4% share.

In 2025, Low Viscosity transmission fluids dominated the Transmission Fluids Market with a share of about 61.4%. Modern vehicle transmissions are designed to operate with fluids that flow easily and reduce internal friction, making low-viscosity formulations highly preferred. Automakers increasingly recommend these fluids because they help improve fuel efficiency and enable smoother gear shifting.

As vehicles adopt more advanced transmission technologies, such as continuously variable and multi-speed automatic systems, low-viscosity fluids help maintain stable performance under different driving conditions. Their ability to support quicker lubrication during cold starts also improves transmission durability over time. Automotive manufacturers and service providers have gradually shifted toward these lighter formulations as they align with global efforts to improve vehicle efficiency and reduce mechanical wear in high-performance transmission systems.

By Transmission Type Analysis

Transmission Fluids Market highlights the Automatic transmission segment holding a strong 48.1% share globally.

In 2025, Automatic transmission systems accounted for a leading 48.1% share of the Transmission Fluids Market. The growing adoption of automatic vehicles across many countries has significantly influenced demand for specialized transmission fluids. Drivers increasingly prefer automatic transmissions for the convenience they provide in urban traffic and long-distance travel. These systems require dedicated automatic transmission fluids that support smooth gear engagement, thermal stability, and proper hydraulic operation.

As passenger mobility expands and traffic congestion rises in urban regions, the popularity of automatic vehicles continues to increase. Automakers are also introducing advanced automatic and dual-clutch transmission systems, which further supportthe consumption of high-quality transmission fluids. Service centers and vehicle manufacturers t, therefore, maintain a strong demand for automatic transmission fluid products designed specifically for these complex transmission mechanisms.

By Vehicle Analysis

Transmission Fluids Market indicates Passenger Cars dominating the vehicle segment with 59.7% share.

In 2025, Passenger Cars represented the largest vehicle segment in the Transmission Fluids Market, holding approximately 59.7% share. The dominance of passenger cars reflects their large global vehicle population and the consistent need for periodic maintenance. Transmission fluids play an important role in ensuring smooth gear operation, protecting internal transmission components, and maintaining efficient vehicle performance. As personal mobility remains essential for daily commuting, passenger cars require regular servicing, which directly drives fluid replacement demand.

Many vehicle owners follow scheduled maintenance guidelines recommended by manufacturers, leading to steady consumption of transmission fluids in this segment. Additionally, the steady introduction of automatic and hybrid passenger vehicles has increased the technical requirements for transmission fluids, encouraging automotive service networks to adopt specialized products tailored to passenger vehicle transmission systems.

By Sales Channel Analysis

Transmission Fluids Market records Service Fill channel leading distribution with 71.2% share.

In 2025, Service Fill remained the dominant sales channel in the Transmission Fluids Market, capturing about 71.2% share. Most transmission fluids are consumed during vehicle servicing rather than during initial vehicle manufacturing. Over time, transmission fluids degrade due to heat, friction, and contamination, making periodic replacement necessary for maintaining transmission performance. Service stations, automotive workshops, and authorized dealerships therefore represent the primary distribution points for these fluids.

As the global vehicle fleet continues to expand, routine maintenance activities generate consistent demand for replacement transmission fluids. Vehicle owners typically rely on service professionals to replace these fluids during scheduled maintenance intervals. This ongoing aftermarket demand ensures that the service fill segment remains the most significant contributor to transmission fluid sales across both developed and emerging automotive markets.

Key Market Segments

By Base Oil

- Mineral Oil

- Semi-synthetic

- Synthetic

By Viscosity

- Low Viscosity

- High Viscosity

By Transmission Type

- Automatic

- Manual

- Continuously Variable

- Dual Clutch

- Electric

By Vehicle

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Off-Road Vehicles

By Sales Channel

- Factory Fill

- Service Fill

- Authorized Service Outlets

- Independent Garages

Driving Factors

The growing global vehicle fleet increases demand

The Transmission Fluids Market continues to benefit from the steady growth in the global vehicle fleet, particularly as passenger cars and commercial vehicles remain essential for daily transportation and logistics activities. As more vehicles operate across urban and highway networks, the need for reliable transmission lubrication increases, ensuring smooth gear performance and system durability. Vehicle owners and fleet operators regularly replace transmission fluids during scheduled maintenance to maintain efficiency and prevent mechanical wear.

Technological innovation in automotive mobility also supports industry momentum. For example, a driverless solar car startup recently secured $2 million in funding from the Australian Renewable Energy Agency (ARENA), highlighting the continued investment in advanced vehicle technologies that will influence future drivetrain systems and lubricant requirements.

Restraining Factors

Rising electric vehicles reduce fluid demand.

One of the challenges affecting the Transmission Fluids Market is the rapid rise of electric vehicles, which use simpler drivetrain systems compared with conventional internal combustion vehicles. Many fully electric vehicles do not require traditional transmission fluids used in multi-gear systems, which gradually reduces long-term demand for certain fluid categories.

As governments and automotive manufacturers accelerate electrification strategies, lubricant consumption patterns are expected to shift. Policy support for energy-efficient transportation is also influencing this transition. For instance, the U.S. Department of Energy announced a $137 million investment aimed at improving commercial and passenger vehicle efficiency, encouraging technologies that reduce energy consumption and support cleaner mobility solutions.

Growth Opportunity

Expanding electric drivetrain fluids technology development

Although electrification presents challenges for conventional transmission fluids, it also opens new opportunities for advanced lubricant technologies designed for electric drivetrains. Modern electric vehicles require specialized fluids for cooling electric motors, reducing friction in e-axles, and maintaining efficiency in high-speed components. This evolving technical requirement is encouraging lubricant developers to create innovative fluid formulations suited for electrified mobility.

Investment activity in autonomous and electric transportation technologies further highlights this opportunity. For example, Alphabet’s self-driving division Waymo secured $5.6 billion in funding to expand autonomous mobility services in the United States, while FIAT introduced a £3,000 electric vehicle incentive in Britain to support EV adoption, reflecting the growing importance of next-generation vehicle technologies.

Latest Trends

Shift toward low viscosity transmission fluid.s

A notable trend in the Transmission Fluids Market is the shift toward low-viscosity formulations that improve fuel efficiency and support smoother transmission performance. Modern vehicles are increasingly designed with advanced transmission systems that require lighter fluids to reduce friction and enhance operational efficiency. Automotive developments across global transportation sectors continue to influence lubricant innovation.

For instance, Uzbekistan recently announced plans to renew its rail fleet with 200 passenger cars, reflecting broader transportation upgrades. In addition, competitive pricing strategies are shaping the electric vehicle landscape, as Fiat reduced EV prices by up to £4,040 following the end of the E-Grant program, further accelerating the transition toward modern vehicle technologies that influence lubricant demand trends.

Regional Analysis

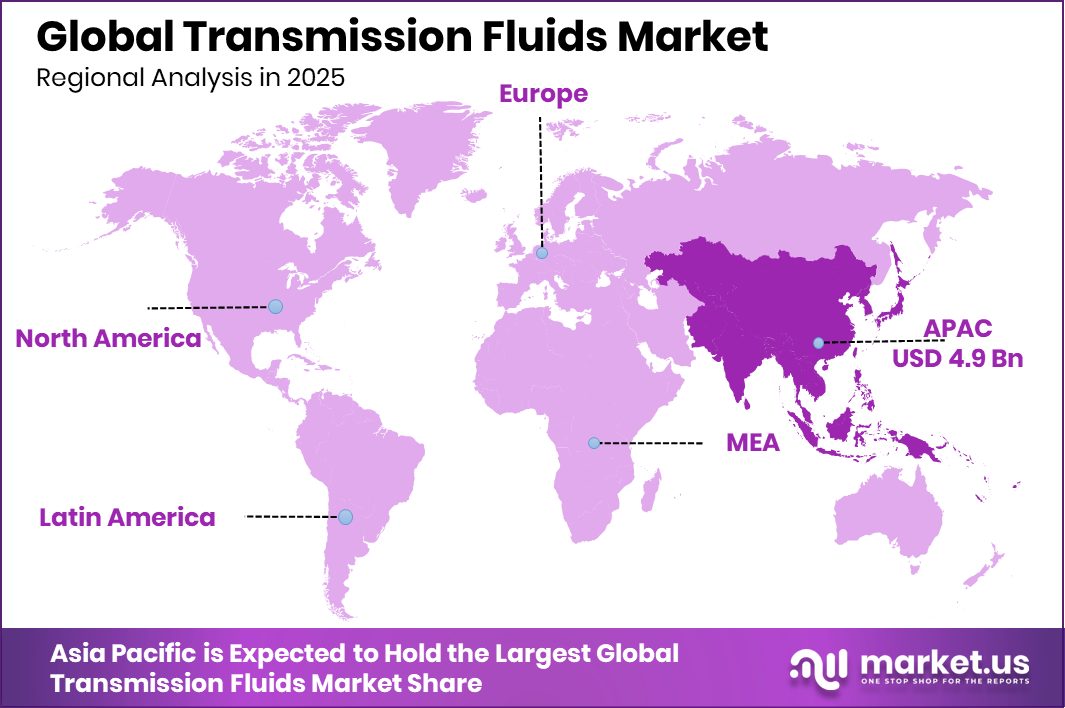

Asia Pacific dominates the Transmission Fluids Market with 43.8% share, reaching a USD 4.9 Bn value.

The Transmission Fluids Market shows varied growth patterns across major regions, including North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, largely influenced by vehicle ownership, automotive production, and maintenance activities.

Asia Pacific remains the dominating region, accounting for 43.8% of the global market with a value of USD 4.9 Bn. The region’s strong position is supported by its large automotive manufacturing base and expanding passenger vehicle fleet, which continuously drives demand for transmission fluid replacement and servicing. Countries acrossthe Asia Pacific have witnessed steady vehicle usage, creating consistent requirements for transmission maintenance in both automatic and manual systems.

In North America, the market is supported by a mature automotive sector and a high number of vehicles requiring routine servicing. Europe also represents a stable market where advanced vehicle technologies and regular maintenance practices sustain demand for high-performance transmission fluids.

Meanwhile, the Middle East & Africa market continues to grow gradually due to increasing vehicle ownership and expanding automotive service infrastructure. Latin America shows moderate demand driven by rising passenger car usage and the need for regular transmission servicing. Overall, regional demand patterns are closely tied to vehicle population and ongoing maintenance cycles within automotive markets.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, ExxonMobil Corporation continues to play a significant role in the global Transmission Fluids Market through its wide portfolio of automotive lubricants and advanced fluid technologies. The company has built a strong reputation for delivering transmission fluids that support smooth gear operation and long-term transmission protection across different vehicle categories. With its global production facilities and extensive distribution network, ExxonMobil maintains strong relationships with automotive manufacturers, service workshops, and lubricant distributors. Its continued focus on product innovation and performance testing allows the company to provide transmission fluids that meet modern vehicle requirements, including improved thermal stability and wear protection.

Royal Dutch Shell Plc remains another important participant in the transmission fluids industry, supported by its well-known lubricant brands and large international presence. The company focuses on developing transmission fluids designed to enhance efficiency and durability in both passenger and commercial vehicles. Shell’s global supply chain and long-standing partnerships with automotive companies allow it to serve multiple regional markets effectively. The company also emphasizes technological development in lubricant formulations, helping vehicle transmissions perform reliably under different driving and operating conditions.

BP Plc, through its Castrol brand, continues to strengthen its position in the transmission fluids space by offering specialized formulations for modern automotive systems. Castrol products are widely used in service networks and automotive maintenance facilities worldwide. The brand’s strong recognition among vehicle owners and mechanics supports steady demand for its transmission fluids, particularly for automatic and high-performance transmissions.

Top Key Players in the Market

- ExxonMobil Corporation

- Royal Dutch Shell Pic

- BP PIc (via Castrol)

- Chevron Corporation

- TotalEnergies SE

- Valvoline Inc.

- Fuchs Petrolub SE

- Phillips 66 Lubricants

- Idemitsu Kosan Co., Ltd.

- Petro-Canada Lubricants Inc.

Recent Developments

- In February 2025, TotalEnergies SE introduced a new fully synthetic transmission fluid called Fluidsyn ATF/CVT through its lubricants division. The company, which produces energy products, fuels, and automotive lubricants, developed this fluid to support both automatic transmission (ATF) and continuously variable transmission (CVT) systems used in modern vehicles. The product helps improve fuel efficiency, protect transmission components, and simplify workshop inventory because a single lubricant can cover a wide range of vehicles.

- In June 2024, Chevron Corporation, which develops fuels, lubricants, and automotive fluids, expanded its lubricant portfolio with Havoline Full Synthetic Multi-Vehicle ATF designed for modern automatic transmissions. The fluid helps improve gear shifting performance and protects transmission components under high temperatures and heavy driving conditions. It is formulated to work with many modern automatic transmission systems used in passenger vehicles.

Report Scope

Report Features Description Market Value (2025) USD 11.2 Billion Forecast Revenue (2035) USD 17.0 Billion CAGR (2026-2035) 4.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Base Oil (Mineral Oil, Semi-synthetic, Synthetic), By Viscosity (Low Viscosity, High Viscosity), By Transmission Type (Automatic, Manual, Continuously Variable, Dual Clutch, Electric), By Vehicle (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Off Road Vehicles), By Sales Channel (Factory Fill, Service Fill(Authorized Service Outlets, Independent Garages)) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ExxonMobil Corporation, Royal Dutch Shell Pic, BP PIc (via Castrol), Chevron Corporation, TotalEnergies SE, Valvoline Inc., Fuchs Petrolub SE, Phillips 66 Lubricants, Idemitsu Kosan Co., Ltd., Petro-Canada Lubricants Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Transmission Fluids MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Transmission Fluids MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ExxonMobil Corporation

- Royal Dutch Shell Pic

- BP PIc (via Castrol)

- Chevron Corporation

- TotalEnergies SE

- Valvoline Inc.

- Fuchs Petrolub SE

- Phillips 66 Lubricants

- Idemitsu Kosan Co., Ltd.

- Petro-Canada Lubricants Inc.

Our Clients

- 180093

- March 2026