Quick Navigation

Report Overview

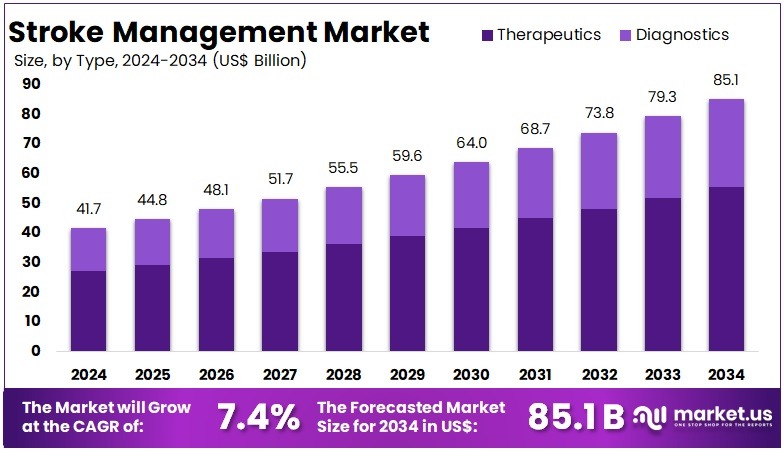

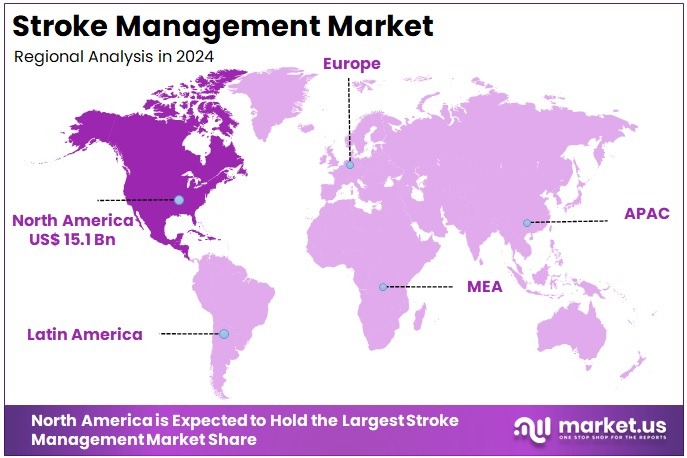

The Global Stroke Management Market size is expected to be worth around US$ 85.1 Billion by 2034, from US$ 41.7 Billion in 2024, growing at a CAGR of 7.4% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 36.4% share and holds US$ 15.1 Billion market value for the year.

Stroke management is evolving rapidly due to technological innovations, growing public awareness, and targeted government interventions. Advanced diagnostic tools such as high-resolution brain imaging and artificial intelligence (AI)-powered systems are transforming stroke detection and treatment. For instance, telemedicine enables faster diagnosis in remote areas, allowing patients to receive timely care. These tools not only improve patient outcomes but also reduce long-term disability and mortality related to stroke.

According to the World Stroke Organization’s Global Stroke Fact Sheet 2025, stroke remains the second leading cause of death globally, causing approximately 7 million deaths each year. It also accounts for more than 160 million disability-adjusted life years (DALYs) annually. Between 1990 and 2021, stroke cases rose by 70%, with ischemic strokes comprising about 65% of all incidents. The rise is linked to factors such as urbanization, lifestyle changes, and an aging global population.

A study published in PubMed Central highlights that 75% of strokes occur in individuals aged 65 or older, underscoring the increasing need for geriatric stroke care. In the United States alone, approximately 795,000 people experience a stroke annually, with 610,000 being first-time cases. Notably, ischemic strokes represent 87% of all stroke incidents. According to Lippincott Journals, India faces over 1.6 million stroke cases each year, with significant regional differences in mortality rates—some regions report death rates three times higher than the national average.

Governments and organizations such as the World Health Organization (WHO) are actively promoting stroke awareness and prevention. For example, WHO’s Essential Medicines List ensures that life-saving drugs are accessible globally. Public campaigns teaching symptom recognition methods, like the FAST method, and improvements in emergency response systems have led to better early intervention. These initiatives play a vital role in reducing the impact of stroke on global health.

Preventive healthcare is also gaining momentum as a strategy to reduce stroke incidence. Programs focused on healthy diets, increased physical activity, and smoking cessation target modifiable risk factors like hypertension, high cholesterol, and obesity. These lifestyle changes, when implemented through national health programs, serve as cost-effective ways to lower the burden of stroke across populations.

Despite these advancements, major challenges persist. High treatment costs and limited access to advanced diagnostics hinder stroke care in low-income regions. Additionally, 87% of stroke-related deaths and 89% of DALYs occur in low- and middle-income countries. A global study estimates the economic cost of stroke at over USD 890 billion annually, nearly 0.66% of the global GDP. This figure is expected to double by 2050. Growth factors such as VEGF and BDNF have shown potential in promoting neuroregeneration. For instance, elevated levels of VEGF and G-CSF in the first week after stroke are associated with better recovery outcomes and reduced brain lesion volumes.

Key Takeaways

- The Global Stroke Management Market is projected to reach US$ 85.1 Billion by 2034, growing at a CAGR of 7.4% from 2025.

- In 2024, the market stood at US$ 41.7 Billion, marking the base year for the forecast period of 2025 to 2034.

- Therapeutics accounted for over 65.4% of the stroke management market in 2024, indicating strong demand for pharmacological interventions in stroke care.

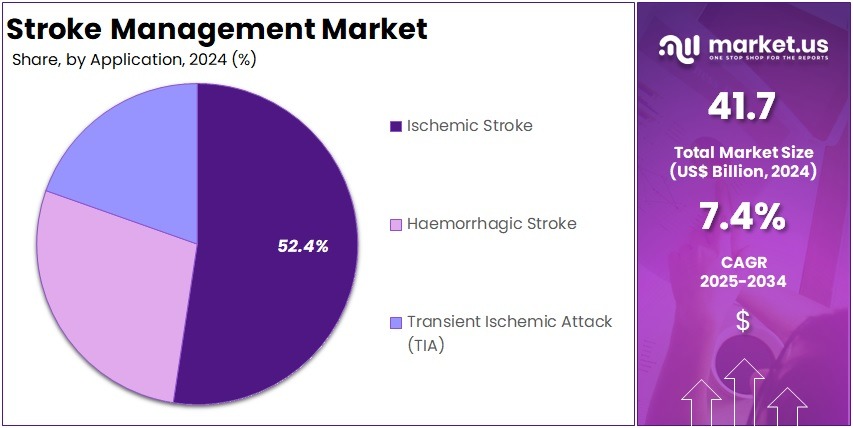

- Ischemic stroke dominated the application segment with a 52.4% share in 2024, driven by its higher global prevalence compared to other stroke types.

- Hospitals were the leading end users in 2024, representing 41.3% of the market share, due to comprehensive stroke care infrastructure and specialist availability.

- North America held the largest regional share at 36.4% in 2024, with a market value of US$ 15.1 Billion, supported by advanced healthcare systems.

Type Analysis

In 2024, Therapeutics held a dominant market position in the Type Segment of Stroke Management, capturing more than a 65.4% share. This leadership was mainly due to the increasing need for effective stroke treatment. Experts observed a rise in ischemic stroke cases, which led to a greater demand for therapeutic drugs. Among these, Tissue Plasminogen Activator (tPA) was identified as a vital solution due to its ability to dissolve clots quickly. It became a standard in emergency stroke care.

Medical professionals also highlighted the growing use of Anticoagulants and Antiplatelets. These drugs played a crucial role in preventing recurrent strokes. In addition, Antihypertensive medications were often prescribed to manage blood pressure, which is a major stroke risk factor. Healthcare providers focused more on treatments that could lower long-term complications. The wide availability of stroke medications and improved awareness supported this trend. As a result, therapeutics remained a preferred option in clinical settings.

Meanwhile, the Diagnostics segment showed steady growth, supported by advancements in imaging technology. Tools such as CT scans, MRI, carotid ultrasound, and echocardiography were regularly used for accurate stroke detection. CT and MRI scans were especially favored due to their speed and clarity in visualizing brain damage. Despite this progress, diagnostic tools served mostly as support for therapeutic planning. Analysts noted that while diagnostics are vital, the market continues to lean heavily toward therapeutic interventions.

Application Analysis

In 2024, Ischemic Stroke held a dominant market position in the Application Segment of Stroke Management, capturing more than a 52.4% share. This dominance has been linked to its high occurrence rate worldwide. It is widely known that ischemic strokes are the most common type, often caused by blood clots. Improved access to treatments and timely interventions has supported this segment’s growth. The use of clot-dissolving drugs and mechanical thrombectomy procedures continues to rise in clinical practice.

Experts observed that growing awareness programs and early diagnosis methods are further strengthening the ischemic stroke segment. Increasing demand for brain imaging and diagnostic tools has improved patient outcomes. The adoption of minimally invasive treatments has reduced recovery time and hospital stays. These trends are likely to continue as healthcare systems focus on rapid stroke response. A larger elderly population and rising chronic diseases also support long-term market demand in this segment.

The Haemorrhagic Stroke and Transient Ischemic Attack (TIA) segments held smaller shares in 2024. However, both are expected to show steady growth. Haemorrhagic strokes, though less common, are more severe and linked to hypertension. Advancements in neurosurgery and critical care tools are aiding this segment’s progress. TIA cases, often seen as warning signs, are gaining attention due to their risk of future strokes. Preventive strategies, such as blood thinners and lifestyle changes, are boosting demand in this area. These segments are set to expand with rising awareness and screening initiatives.

End User Analysis

In 2024, Hospitals held a dominant market position in the End User Segment of Stroke Management, capturing more than a 41.3% share. According to industry trends, hospitals were the primary treatment centers for acute stroke cases. Their dominance was driven by the availability of skilled professionals, advanced imaging tools, and emergency care services. Hospitals also offer specialized stroke units, which are essential for managing ischemic and haemorrhagic strokes. These factors supported their strong presence in the stroke management ecosystem.

Ambulatory Surgical Centers (ASCs) occupied a moderate share in the end user segment. These facilities provide cost-effective and efficient care, especially for less severe neurological issues. However, their role in stroke management remains limited due to the need for continuous monitoring and advanced neurology services. Diagnostic Centers also held a smaller portion of the market. Their contribution is significant in the early detection of stroke symptoms, particularly in cases of Transient Ischemic Attacks (TIAs).

Rehabilitation Centers played an essential role in the recovery phase after stroke treatment. These centers focus on improving motor skills, speech, and daily functions. As awareness of stroke rehabilitation continues to grow, demand for these services is expected to rise. Although they do not handle emergency care, they support long-term patient outcomes. This trend reflects a shift toward comprehensive care beyond initial treatment. Growth in this segment will likely continue as healthcare systems prioritize quality of life and functional recovery in stroke survivors.

Key Market Segments

By Type

- Diagnostics

- Computed Tomography Scan (CT Scan)

- Magnetic Resonance Imaging (MRI)

- Carotid Ultrasound

- Cerebral Angiography

- Electrocardiography

- Echocardiography

- Others

- Therapeutics

- Tissue Plasminogen Activator

- Anticoagulant

- Antiplatelet

- Antihypertensive

By Application

- Ischemic Stroke

- Haemorrhagic Stroke

- Transient Ischemic Attack (TIA)

By End User

- Hospitals

- Ambulatory Surgical Centers

- Diagnostic Centers

- Others

Drivers

Increasing Prevalence of Hypertension and Coronary Heart Disease

The rising number of people with hypertension is a key factor driving the stroke management market. Hypertension is a major risk factor for both ischemic and hemorrhagic strokes. It weakens blood vessels, increasing the chance of rupture or blockage. As more people are diagnosed with high blood pressure, the need for stroke-related healthcare rises. This trend is particularly strong in aging populations. The increase in hypertension cases leads to higher stroke rates, creating greater demand for effective stroke care and prevention methods.

Coronary heart disease (CHD) is also a significant contributor to stroke risk. CHD reduces blood flow to the brain by narrowing or blocking arteries. This condition increases the chances of ischemic stroke. The global rise in CHD cases is directly linked to poor diet, lack of exercise, and other lifestyle factors. As CHD becomes more common, stroke incidents are expected to grow. This drives the need for advanced stroke management solutions to improve patient care and reduce the burden on healthcare systems.

The combined increase in hypertension and CHD has led to a growing patient base at risk of stroke. This has made stroke prevention and treatment a top priority in the healthcare sector. Hospitals and clinics are adopting better technologies and therapies to meet this rising demand. Pharmaceutical and medical device companies are also investing more in stroke-related innovations. As a result, the stroke management market is expanding steadily. The need for faster diagnosis and improved care is shaping future growth in this area.

Restraints

Limited Access to Advanced Stroke Care in Developing Regions

Access to advanced stroke care remains limited in many developing regions. Despite medical advancements, healthcare disparities continue to affect outcomes. Specialized stroke care facilities are often lacking in rural and underdeveloped areas. The absence of such infrastructure prevents timely and effective treatment. Without access to diagnostic tools and emergency care, stroke patients face delays in intervention. This results in poor health outcomes. Timely treatment is critical in reducing brain damage. Limited access increases the risk of death and long-term disabilities in stroke patients.

A major barrier to stroke management is the shortage of trained healthcare professionals. Many developing countries lack neurologists and emergency care specialists. This shortage affects the ability to diagnose and treat strokes quickly. Nurses and general practitioners may not have proper training in stroke care. As a result, symptoms are often missed or misdiagnosed. Early identification is essential to improve survival rates. Without skilled staff, life-saving treatments like thrombolysis are delayed. This leads to greater damage and longer recovery times for patients.

The consequences of limited stroke care access are severe. Mortality rates are significantly higher in developing regions. Survivors often suffer from long-term disabilities. These outcomes place a burden on families and healthcare systems. Economic constraints further limit investment in stroke care facilities. Additionally, public awareness about stroke symptoms is low. This causes delays in seeking help. Improving stroke care requires better infrastructure, training, and education. With targeted efforts, outcomes can improve over time. Reducing these disparities is key to global health equity.

Opportunities

Integration of Artificial Intelligence and Telemedicine

The integration of artificial intelligence (AI) and telemedicine is transforming stroke management. AI tools can analyze medical images and detect strokes with high accuracy. These systems reduce the time needed for diagnosis, enabling faster treatment decisions. Telemedicine platforms further enhance this by allowing remote consultations between patients and specialists. This is especially useful in areas with limited access to healthcare facilities. Together, these technologies ensure that stroke patients receive timely care. As a result, patient outcomes can be significantly improved.

AI-powered diagnostic systems help healthcare professionals identify stroke symptoms early. Machine learning models can evaluate CT or MRI scans in real time. This leads to quicker decisions and reduces the risk of complications. When combined with telemedicine, patients can receive expert consultations without traveling. This improves accessibility, especially in rural and underserved areas. Stroke treatment becomes more effective with faster diagnosis and immediate care. Therefore, AI and telemedicine work together to streamline clinical workflows and reduce delays in treatment.

Telemedicine also plays a key role in continuous stroke care and rehabilitation. Patients can stay in touch with doctors for follow-up visits and therapy sessions from their homes. AI-driven platforms can track patient progress and alert clinicians to any issues. This ensures continuous monitoring and reduces hospital readmissions. Moreover, it supports personalized treatment plans and enhances recovery. These benefits highlight a strong growth opportunity in the stroke management market. The demand for digital health tools is expected to rise steadily in coming years.

Trends

Advancements in Neuroprotective Therapies and Personalized Medicine

A key trend in stroke management is the rise of neuroprotective therapies. These therapies are designed to protect brain tissue during and after a stroke. Researchers are working to develop drugs that can limit damage to the brain in the early stages. The goal is to prevent further loss of brain function and improve outcomes. New drug candidates are being tested in clinical trials. These advancements show promise in reducing stroke-related disabilities and increasing survival rates. The focus remains on early intervention and rapid treatment.

Another major advancement is the growing use of personalized medicine in stroke care. Personalized medicine uses patient-specific data such as genetics, age, and health history. This approach helps doctors choose treatments that suit each individual. It can also reduce the risk of side effects and improve treatment success. With advances in diagnostic tools, patient profiling has become faster and more accurate. As a result, care plans can be more targeted. This shift supports better patient outcomes and more efficient use of healthcare resources.

The integration of neuroprotective therapies with personalized medicine marks a new era in stroke management. These strategies aim to improve recovery and reduce long-term effects. Personalized neuroprotective interventions are being explored to maximize benefits. The combination allows for more precise and effective care. As these technologies continue to evolve, hospitals are adopting them into clinical practice. The future of stroke care is moving towards tailored and protective treatments. This trend is expected to transform recovery timelines and lower the burden of stroke on society.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 36.4% share and holding a market value of US$ 15.1 Billion for the year. The region’s strong position is linked to a high rate of stroke cases and increasing awareness of early treatment. As reported by independent sources, stroke continues to be a major health concern across the United States and Canada. This has created rising demand for fast diagnosis, effective therapies, and comprehensive care options.

Healthcare infrastructure across North America is well-developed, contributing to market growth. A wide network of hospitals and stroke centers offers access to advanced medical equipment and trained professionals. These facilities support both emergency treatment and long-term rehabilitation. Experts suggest that continued investment in health systems has improved stroke outcomes in the region. In addition, strong public health policies and awareness campaigns have encouraged early screening and faster access to care.

North America is also benefiting from the growing use of digital health tools. Telemedicine and remote monitoring have helped expand stroke services, especially in underserved areas. Analysts note that elderly populations in the region are growing, which increases the demand for stroke-related care. Furthermore, strong government support for research and reimbursement continues to drive innovation. These combined factors reinforce the region’s leadership in the global stroke management market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The stroke management market is shaped by key players who provide innovative products and technologies. GE Healthcare is a leading name with its advanced diagnostic imaging solutions, such as CT and MRI machines, which are crucial for early stroke detection. The company focuses on AI-driven imaging solutions to enhance diagnostic accuracy. Boston Scientific specializes in thrombectomy devices, including the Solitaire™ Flow Restoration Device, which is vital for treating ischemic strokes by removing blood clots. This device is widely adopted globally, positioning Boston Scientific as a market leader.

Medtronic is another significant player, offering a comprehensive range of stroke management devices. Their thrombectomy systems, like the Solitaire™ and Penumbra™ devices, are designed to restore blood flow rapidly in acute ischemic stroke patients. Medtronic also focuses on neurovascular interventions and embolization devices. Johnson & Johnson, through its DePuy Synthes subsidiary, plays a major role with thrombectomy devices and stents. Additionally, the company’s acquisition of Codman & Shurtleff has expanded its product portfolio, solidifying its place in stroke treatment and rehabilitation.

Bayer AG is a key player in stroke prevention, primarily through its pharmaceutical offerings. Its anticoagulant, Xarelto®, is widely prescribed for preventing ischemic strokes in patients with atrial fibrillation. Bayer is actively involved in clinical research to explore new therapeutic options for stroke management. Other important companies include Siemens Healthineers, Stryker Corporation, Abbott Laboratories, and Penumbra Inc. These firms contribute to the market with cutting-edge devices and therapies aimed at improving stroke intervention and recovery, ensuring continued growth in the sector.

Market Key Players

- GE Healthcare

- Boston Scientific Corporation

- Medtronic

- Johnson & Johnson

- Bayer AG

- F. Hoffmann-La Roche Ltd

- Boehringer Ingelheim International GmbH

- Sanofi

- Medtronic

- Teva Pharmaceuticals USA, Inc.

- Pfizer Inc.

Recent Developments

- In January 2024: GE HealthCare announced an agreement to acquire MIM Software, a global provider of advanced medical imaging solutions. This acquisition aims to enhance GE HealthCare’s capabilities in precision care across various disease states, including oncology, neurology, and cardiology. By integrating MIM Software’s AI-driven imaging analytics with GE HealthCare’s medical technology, the company plans to streamline workflows, improve diagnostics, and enable personalized care. The deal is expected to accelerate advancements in Theranostics, beta amyloid imaging for Alzheimer’s diagnosis, and myocardial perfusion for coronary artery disease detection.

- In November 2024: At the American Heart Association (AHA) 2024 conference, Boston Scientific presented three-year data on its Watchman FLX device, which is used to seal the heart’s left atrial appendage in patients with atrial fibrillation to prevent strokes. The OPTION trial demonstrated that the Watchman FLX device had lower rates of major bleeding compared to oral anticoagulants while providing similar protection against strokes. These results suggest potential for expanding the device’s indications and positioning it as a frontline therapy for stroke prevention in patients undergoing cardiac ablation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 41.7 Billion |

| Forecast Revenue (2034) | US$ 85.1 Billion |

| CAGR (2025-2034) | 7.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type [Diagnostics (Computed Tomography Scan (CT Scan), Magnetic Resonance Imaging (MRI), Carotid Ultrasound, Cerebral Angiography, Electrocardiography, Echocardiography, Others), Therapeutics (Tissue Plasminogen Activator, Anticoagulant, Antiplatelet, Antihypertensive)], By Application (Ischemic Stroke, Haemorrhagic Stroke, Transient Ischemic Attack (TIA)), By End User (Hospitals, Ambulatory Surgical Centers, Diagnostic Centers, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | GE Healthcare, Boston Scientific Corporation, Medtronic, Johnson & Johnson, Bayer AG, F. Hoffmann-La Roche Ltd, Boehringer Ingelheim International GmbH, Sanofi, Medtronic, Teva Pharmaceuticals USA, Inc., Pfizer Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |