Global Specialty Oilfield Chemicals Market Size, Share, And Industry Analysis Report By Product (Inhibitors, Friction Reducers, Surfactants, Biocides, Demulsifiers, Others), By Application (Production, Drilling Fluids, Oil Recovery, Cementing, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179259

- Number of Pages: 351

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

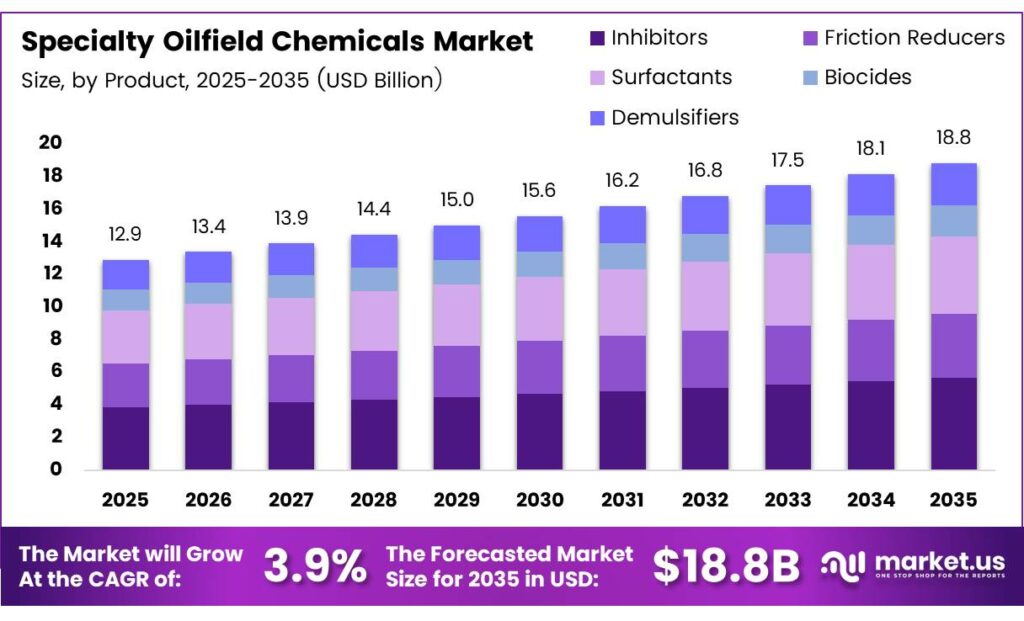

The Global Specialty Oilfield Chemicals Market size is expected to be worth around USD 18.8 billion by 2035 from USD 12.9 billion in 2025, growing at a CAGR of 3.9% during the forecast period 2026 to 2035.

Specialty oilfield chemicals serve a critical role in upstream and midstream oil and gas operations. These chemicals support drilling, production, stimulation, and pipeline integrity activities. They include inhibitors, surfactants, biocides, demulsifiers, and friction reducers that operators apply to improve efficiency and asset performance.

The market grows as global energy demand pushes operators to extract more from existing and new reservoirs. Upstream companies invest in chemical solutions to extend field life, reduce operational downtime, and improve recovery rates. Moreover, expanding shale and unconventional plays worldwide continue to fuel steady demand for high-performance oilfield chemical formulations.

- ChampionX recorded $3.63 billion in total revenue in 2024, reinforcing its strong position as a leading supplier of production-focused oilfield chemical technologies. With $2.29 billion generated by its Chemical Technologies segment, production chemicals made up nearly two-thirds of its oilfield-related revenue, highlighting both the company’s commercial scale and the central role these solutions play within major operators’ operations.

Enhanced oil recovery programs and horizontal drilling expansion reinforce market growth globally. Operators in mature basins adopt chemical injection systems to sustain production levels. Additionally, new field developments in deepwater and offshore environments require advanced chemical additives, creating fresh demand across multiple product categories and application segments.

Key Takeaways

- The Global Specialty Oilfield Chemicals Market is valued at USD 12.9 billion in 2025 and is projected to reach USD 18.8 billion by 2035, at a CAGR of 3.9% during the forecast period 2026 to 2035.

- Inhibitors dominate the market with a 34.6% share in 2025.

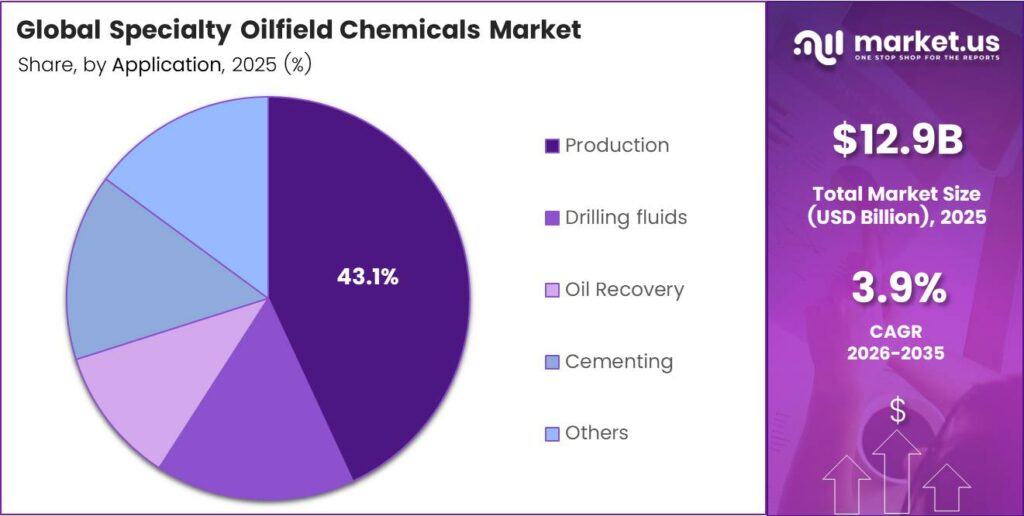

- Production holds the largest share at 43.1% among all application segments.

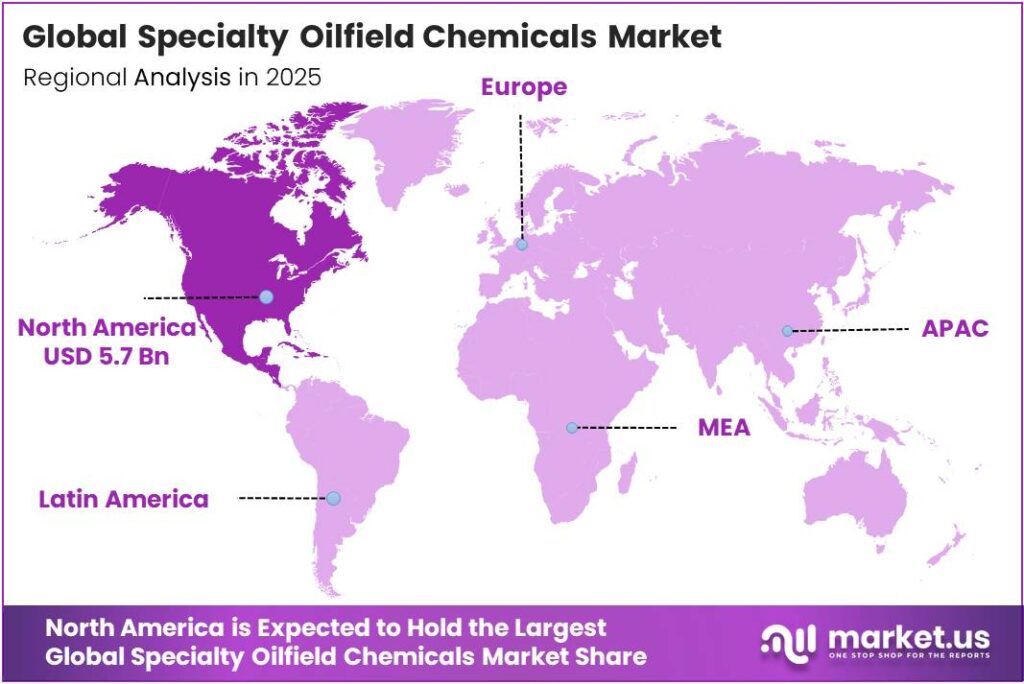

- North America leads all regions with a market share of 44.3%, valued at USD 5.7 billion in 2025.

By Product Analysis

Inhibitors dominate with 34.6% due to widespread use in corrosion and scale prevention across oilfield operations.

In 2025, Inhibitors held a dominant market position in the By Product segment of the Specialty Oilfield Chemicals Market, with a 34.6% share. Corrosion and scale inhibitors protect pipelines, wellbores, and surface equipment from chemical degradation. Moreover, operators consistently prioritize these chemicals to reduce maintenance costs and extend asset life across production environments.

Friction Reducers represent a fast-growing product category in the specialty oilfield chemicals space. Horizontal drilling and multi-stage hydraulic fracturing operations rely heavily on friction-reducing agents to improve pump efficiency and wellbore performance. Consequently, the surge in unconventional shale development globally has expanded friction reducer consumption significantly over recent years.

Surfactants serve critical roles in drilling, stimulation, and enhanced recovery operations by reducing interfacial tension between oil, water, and rock surfaces. These chemicals improve fluid performance and increase hydrocarbon mobility in reservoir formations. Additionally, surfactant demand grows as operators apply enhanced oil recovery techniques in both conventional and unconventional plays.

Biocides protect oilfield systems from microbial growth that causes corrosion, souring, and production losses. Water injection and produced water management activities drive consistent biocide demand across upstream operations. Furthermore, tightening environmental standards push manufacturers to develop more targeted and biodegradable biocide formulations for oilfield use.

Demulsifiers separate water and solids from crude oil during production and processing stages. These chemicals improve crude oil quality and support more efficient separation at surface facilities. Additionally, rising water-cut in maturing fields increases demulsifier application frequency, supporting steady volume demand across major production regions worldwide.

The Others category includes specialty products such as scale dissolvers, clay stabilizers, foaming agents, and flow improvers. These niche chemicals address specific reservoir and operational challenges. However, their combined contribution supports overall market breadth and allows chemical suppliers to offer complete oilfield chemical solution packages to operators across diverse field conditions.

By Application Analysis

Production dominates with 43.1% due to the continuous chemical treatment needs of active producing wells and surface facilities.

In 2025, Production held a dominant market position in the By Application segment of the Specialty Oilfield Chemicals Market, with a 43.1% share. Production operations require continuous chemical injection to prevent corrosion, scale, emulsions, and microbial activity in wellbores and flowlines. Moreover, mature fields with declining reservoir pressure demand greater chemical treatment intensity to sustain output rates.

Drilling Fluids represent one of the most technically demanding application areas within specialty oilfield chemicals. Operators use drilling fluid chemicals to cool drill bits, control formation pressure, and stabilize wellbore walls during drilling operations. Additionally, the shift toward deeper and more complex wells increases drilling fluid complexity, driving demand for advanced chemical additives and fluid-system packages.

Oil Recovery chemicals support enhanced recovery programs that extract additional hydrocarbons from partially depleted reservoirs. Surfactants, polymers, and alkali chemicals improve sweep efficiency and reduce residual oil saturation in reservoir rock. Consequently, as operators target higher recovery factors from existing fields, oil recovery chemical applications gain growing importance within the broader market portfolio.

Cementing chemicals provide wellbore integrity and zonal isolation during well construction and completion activities. Additives such as accelerators, retarders, and fluid-loss control agents ensure cement slurry performance under extreme downhole temperatures and pressures. Furthermore, rising deepwater and unconventional well activity sustains strong cementing chemical demand across international and North American drilling markets.

Key Market Segments

By Product

- Inhibitors

- Friction Reducers

- Surfactants

- Biocides

- Demulsifiers

- Others

By Application

- Production

- Drilling Fluids

- Oil Recovery

- Cementing

- Others

Emerging Trends

Digital Innovation and Sustainability Goals Reshape the Specialty Oilfield Chemicals Landscape

Oilfield operators integrate artificial intelligence and digital monitoring platforms into chemical management workflows. These systems optimize chemical injection rates in real time, reducing waste and improving treatment efficiency. Moreover, predictive analytics tools help operators anticipate production chemistry challenges before they escalate into costly well interventions or equipment failures.

- Demand for eco-friendly and biodegradable oilfield chemical formulations grows steadily as sustainability mandates tighten across the industry. Operators and regulators increasingly require low-toxicity alternatives to conventional chemical products used in drilling and production. Kemira’s Americas region generated €1,113 million of 2024 revenue, reflecting scale in specialty chemistry markets that increasingly favor sustainable product platforms.

Deepwater and offshore drilling projects generate expanding demand for advanced specialty chemical additives. These environments impose extreme pressure, temperature, and flow assurance challenges that require highly engineered chemical solutions. Clariant reported full-year 2024 sales of CHF 4.152 billion, illustrating the commercial scale that leading specialty chemical suppliers command as offshore project activity intensifies globally.

Drivers

Rising Upstream Activity and Advanced Drilling Technologies Drive Specialty Oilfield Chemicals Demand

Global crude oil production growth and active upstream exploration programs fuel consistent demand for specialty oilfield chemicals. National oil companies and independent operators expand drilling programs to meet rising energy consumption worldwide. Halliburton reported total revenue of $22.9 billion for full-year 2024, confirming the substantial commercial scale of oilfield services that directly consume and deploy specialty chemical products.

- Enhanced oil recovery programs expand into complex and low-permeability reservoir formations, driving demand for specialized chemical systems. Polymer flooding, surfactant injection, and alkaline treatments require high-performance formulations tailored to specific reservoir conditions. ChampionX Production Chemical Technologies’ revenue from Latin America totalled $307.6 million in 2024, underlining the region’s growing role as a production chemistry demand center for demulsifiers and scale inhibitors.

Horizontal drilling and multi-stage hydraulic fracturing technologies require large volumes of friction reducers, scale inhibitors, and breaker chemicals. Operators apply these specialty products to improve wellbore performance and maximize production from unconventional shale formations. Consequently, the continued expansion of shale drilling in the United States, Argentina, and other basins reinforces sustained demand growth across multiple oilfield chemical product categories.

Restraints

Crude Oil Price Volatility and Environmental Compliance Costs Constrain Market Expansion

Crude oil price volatility directly impacts upstream exploration and production budgets, reducing operator spending on specialty chemicals during market downturns. When oil prices fall sharply, operators cut chemical injection volumes and defer treatment programs to preserve cash flow. Consequently, specialty oilfield chemical suppliers face revenue pressure and demand uncertainty during periods of sustained commodity price weakness.

Stringent environmental regulations impose significant compliance costs on chemical manufacturers and oilfield operators. Regulatory bodies in North America, Europe, and the Asia Pacific tighten restrictions on chemical discharge, toxicity limits, and environmental impact assessments for oilfield chemical use. Moreover, developing compliant product formulations requires substantial research and testing investment, which increases operating costs for both producers and end users in regulated markets.

Smaller oilfield operators often struggle to absorb the full cost of advanced specialty chemical programs, particularly in low-margin environments. Limited technical expertise and procurement capacity also restrict the adoption of premium chemical solutions among independent producers. However, the growth of managed chemical service models and performance-based contracting helps reduce the financial barriers that restrain adoption across smaller upstream operators worldwide.

Growth Factors

Emerging Region Investments and Next-Generation Chemical Technologies Accelerate Market Expansion

Rising oilfield exploration investments in Africa, the Middle East, and Southeast Asia create new demand for specialty chemical solutions. ChampionX Production Chemical Technologies’ revenue from United States customers reached $1.02 billion in 2024, representing approximately 45% of this segment’s global sales and indicating the concentrated growth potential that also exists in emerging international markets.

- Nanotechnology-enhanced oilfield chemical formulations deliver superior performance in demanding reservoir and wellbore environments. Nano-scale additives improve thermal stability, reduce chemical consumption volumes, and increase treatment effectiveness compared to conventional alternatives. SNF Group generated EBITDA exceeding €800 million in 2025, underlining the profitability that advanced polyacrylamide and specialty polymer chemistries deliver across enhanced oil recovery and water treatment programs.

Redevelopment of aging and mature oil reservoirs worldwide opens significant demand for specialty production and recovery chemicals. Operators apply chemical workover programs, scale treatments, and flow improvers to revive declining production from established fields. Additionally, growing ESG compliance requirements drive the development of bio-based and low-toxicity specialty oilfield chemicals, creating a new product growth frontier that combines commercial and sustainability objectives for leading chemical manufacturers.

Regional Analysis

North America Dominates the Specialty Oilfield Chemicals Market with a Market Share of 44.3%, Valued at USD 5.7 Billion

North America leads the global specialty oilfield chemicals market, capturing a dominant share of 44.3% and a market value of USD 5.7 billion in 2025. The United States drives this leadership through its extensive shale and unconventional drilling programs that consume large volumes of friction reducers, inhibitors, and stimulation chemicals. Moreover, active well-completion activity across the Permian Basin, Eagle Ford, and Bakken formations sustains consistent chemical demand throughout the region.

Europe represents a mature but stable market for specialty oilfield chemicals, supported by North Sea production operations and enhanced recovery programs in aging fields. Kemira’s total, confirming EMEA’s importance as a base for specialty chemistry supply to oilfield and adjacent industries. Additionally, regulatory pressure drives European operators to prioritize low-toxicity and biodegradable chemical alternatives.

Asia Pacific shows strong growth momentum in specialty oilfield chemicals, led by expanding upstream activity in China, India, Malaysia, and Australia. National oil companies in the region invest in new field development and enhanced oil recovery programs that drive chemical consumption. Furthermore, growing deepwater exploration in Southeast Asia increases demand for advanced drilling fluid additives and production chemistry solutions across this dynamic region.

Latin America offers significant growth opportunities for specialty oilfield chemicals, supported by active deepwater projects in Brazil and shale development programs in Argentina. The region’s resource base and operator investment commitments drive sustained chemical consumption across production, drilling, and enhanced recovery applications. However, fiscal and regulatory uncertainties in certain markets continue to moderate the pace of upstream spending and related chemical demand growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Nouryon operates as a global specialty chemicals leader with a strong portfolio of products serving oilfield drilling, production, and stimulation applications. The company focuses on developing high-performance surfactants, corrosion inhibitors, and fluid treatment solutions for upstream operators. Nouryon’s research capabilities and global manufacturing footprint enable it to deliver tailored chemical formulations that address complex oilfield challenges across multiple geographies and well types.

BASF SE holds a prominent position in the specialty oilfield chemicals market through its extensive range of oilfield additives, including scale inhibitors, biocides, and demulsifiers. The company applies its deep chemistry expertise to develop innovative solutions for production optimization and flow assurance in challenging reservoir environments. BASF’s global supply chain and technical service capabilities support operators in designing and implementing effective chemical treatment programs across diverse upstream operations worldwide.

Baker Hughes serves the specialty oilfield chemicals market through its well-integrated portfolio of production chemicals, stimulation fluid additives, and drilling chemical solutions. The company combines chemical formulation expertise with digital monitoring and data analytics capabilities to deliver optimized chemical programs for operators. Baker Hughes targets production efficiency and environmental compliance as central themes in its oilfield chemicals strategy, addressing growing operator demand for sustainable and performance-driven chemical treatment solutions globally.

Halliburton deploys specialty oilfield chemicals across its comprehensive completion, production, and drilling service offerings. The company’s chemical product range spans friction reducers, cementing additives, and production treatment chemicals used in wells across North America and international markets. Halliburton’s scale and integration across oilfield services allow it to position specialty chemicals as a critical enabler of broader well performance outcomes, reinforcing its competitive depth in the global oilfield chemicals marketplace.

Top Key Players in the Market

- Nouryon

- BASF SE

- SMC Global

- Baker Hughes

- Halliburton

- The Lubrizol Corporation

- Aquapharm Chemical Pvt. Ltd.

- Clariant

- Solvay S.A.

- Thermax Chemical Division

Recent Developments

- In 2025, Nouryon opened its Innovation Center for oilfield applications in Houston, Texas (the first dedicated facility of its kind in the city). The center focuses on R&D for sustainable drilling and completion, production, and stimulation processes. It includes state-of-the-art testing capabilities in demulsification, corrosion and scale inhibition, and stimulation chemistries.

- In 2025, BASF announced a capacity expansion for its Basoflux range of paraffin inhibitors at the Tarragona, Spain site. The investment adds assets for greater efficiency and flexibility, including more sustainable aqueous-based dispersion paraffin inhibitors and solvent-based products.

Report Scope

Report Features Description Market Value (2025) USD 12.9 Billion Forecast Revenue (2035) USD 18.8 Billion CAGR (2026-2035) 3.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Inhibitors, Friction Reducers, Surfactants, Biocides, Demulsifiers, Others), By Application (Production, Drilling Fluids, Oil Recovery, Cementing, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Nouryon, BASF SE, SMC Global, Baker Hughes, Halliburton, The Lubrizol Corporation, Aquapharm Chemical Pvt. Ltd., Clariant, Solvay S.A., Thermax Chemical Division Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Specialty Oilfield Chemicals MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Specialty Oilfield Chemicals MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Nouryon

- BASF SE

- SMC Global

- Baker Hughes

- Halliburton

- The Lubrizol Corporation

- Aquapharm Chemical Pvt. Ltd.

- Clariant

- Solvay S.A.

- Thermax Chemical Division

Our Clients

- 179259

- February 2026