Global Pumps Market Size, Share and Report Analysis By Type (Centrifugal Pumps and Positive Displacement Pumps), By Sales Channel (Aftermarket and New Sales), By End-Use (Industrial, Agriculture, and Residential And Commercial), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 180179

- Number of Pages: 377

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

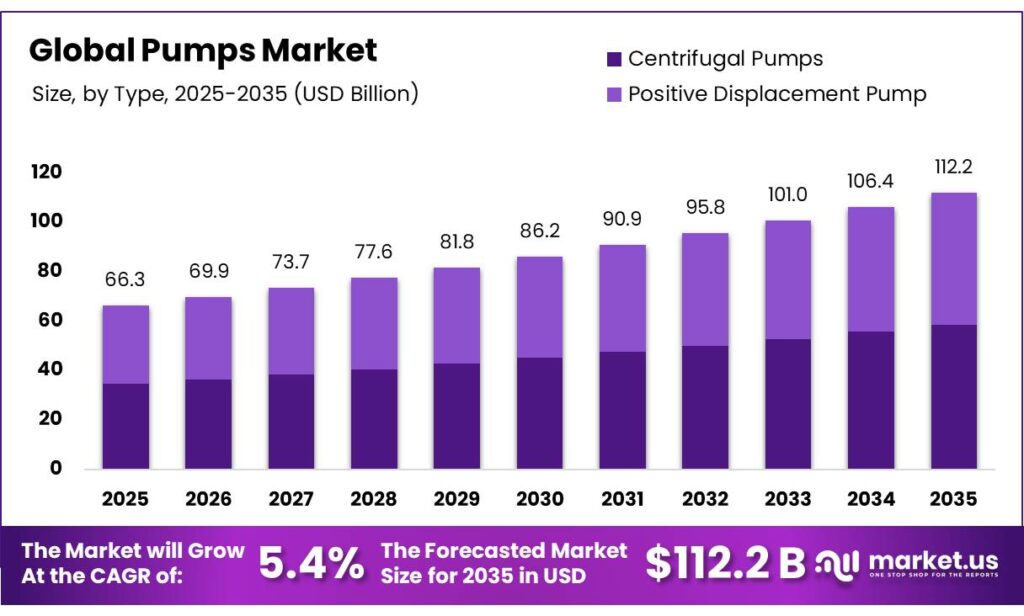

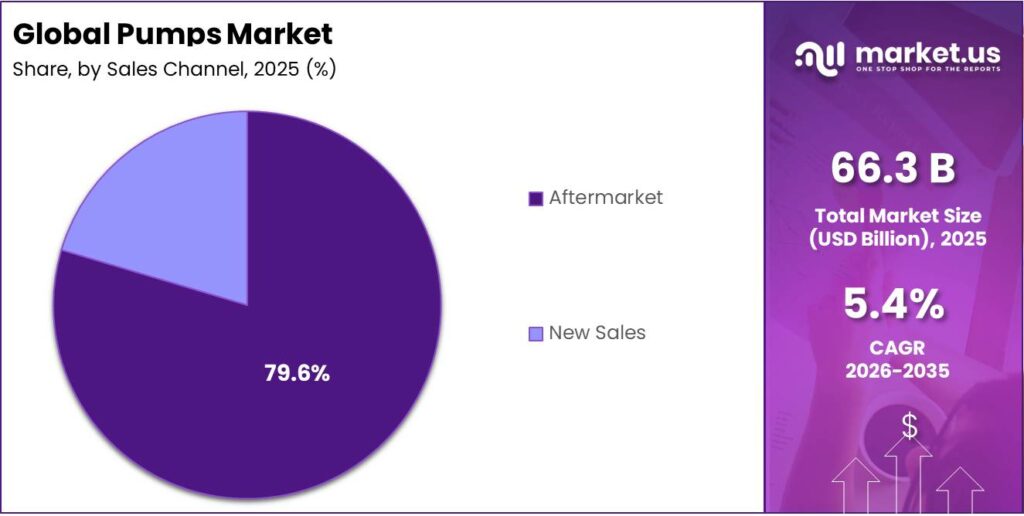

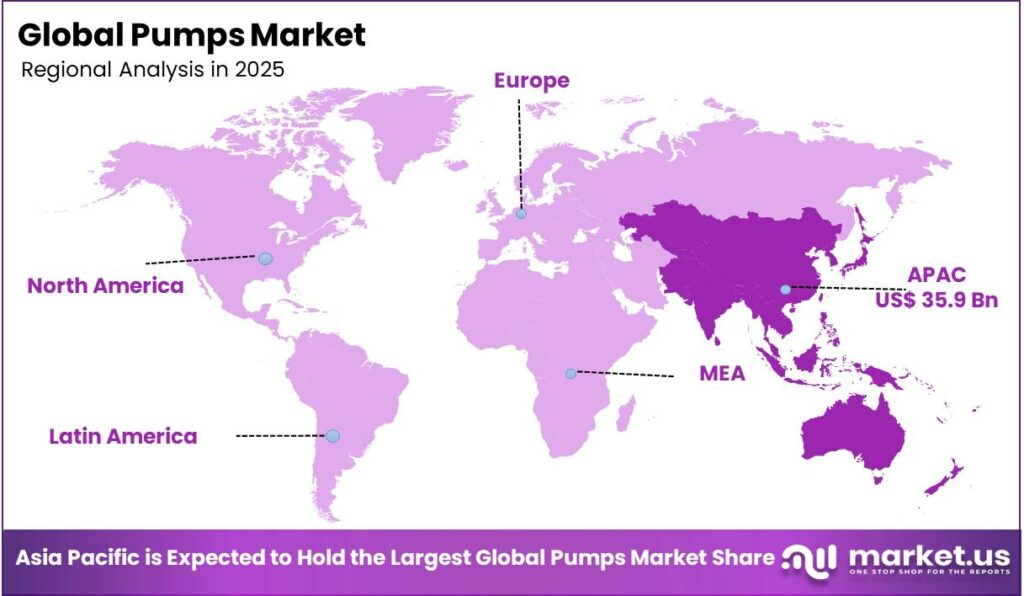

The Global Pumps Market is expected to be worth around USD 112.2 Billion by 2035, up from USD 66.3 Billion in 2025, at a CAGR of 5.4% from 2026 to 2035. The Asia Pacific segment maintained 54.1%, supporting a Alcohol-Based Disinfectants value of USD 35.9 Bn.

A pump is a machine that moves fluids (liquids or gases) or slurries by mechanical action, usually by converting electrical or mechanical energy into hydraulic energy. They work by creating a pressure difference (or vacuum) that sucks the fluid in and forces it out to a higher-pressure area. The market is primarily driven by the needs of industrial sectors, urbanization, and infrastructure development. The shift towards IoT-enabled pumps for remote monitoring and predictive maintenance further exemplifies ongoing technological advancements in the market.

Centrifugal pumps dominate the market due to their efficiency in handling large volumes of fluids with lower maintenance costs, making them ideal for applications such as water supply, wastewater treatment, and industrial processing. The Asia Pacific region holds the largest share, driven by rapid industrialization and urban expansion, with increasing demand for pumps in water management, energy production, and agriculture.

However, geopolitical tensions pose challenges by disrupting supply chains and increasing raw material costs, especially in regions dependent on international trade. Additionally, regulatory compliance drives innovation in pump technologies, with energy efficiency becoming a focal point. Despite the prominence of pumps in industries, the market sees substantial aftermarket activity, as pumps require frequent replacement and maintenance in established systems.

Key Takeaways:

- The global pumps market was valued at USD 66.3 billion in 2025.

- The global pumps market is projected to grow at a CAGR of 5.4% and is estimated to reach USD 112.2 billion by 2035.

- On the basis of type, centrifugal pumps dominated the market, constituting 52.3% of the total market share.

- Based on the sales channel, aftermarket sales led the pumps market, comprising 79.6% of the total market.

- Among the end-uses of the pumps, the industrial sector is the most considerable end-use of the product, accounting for around 82.9% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the pumps market, accounting for 54.1% of the total global consumption.

Type Analysis

Centrifugal Pumps are a Prominent Segment in the Market.

The market is segmented based on the type of pumps into centrifugal and positive displacement pumps. The centrifugal pumps led the market, comprising 52.3% of the market share, primarily due to their simplicity, versatility, and efficiency in handling large volumes of liquids. They operate by converting rotational energy from a motor into kinetic energy, which is ideal for low-viscosity fluids such as water, chemicals, and oil. Their design is less complex, making them easier and cheaper to maintain and operate compared to positive displacement pumps.

Additionally, centrifugal pumps can handle a wide range of flow rates and pressures, making them suitable for diverse applications, from water supply systems to industrial processes. In addition, their ability to operate with variable flow conditions and low pulsation makes them more efficient in large-scale systems, contributing to their widespread adoption.

Sales Channel Analysis

Aftermarket Sales Dominated the Pumps Market.

On the basis of sales channels, the pumps market is segmented into aftermarket and new sales. The aftermarket sales dominated the pumps market, comprising 79.6% of the market share, due to the critical role they play in maintenance and replacement within existing infrastructure. Many industrial systems, water treatment plants, and irrigation systems have long lifecycles, requiring pumps to be replaced or repaired as they wear out over time.

Additionally, pumps in established systems often need to be upgraded or replaced to meet new regulatory standards, improve energy efficiency, or adapt to changing operational needs. The aftermarket further sees a demand for customized solutions, such as pump modifications or specialized parts, to ensure compatibility with specific applications. Moreover, industries prefer to buy pumps as replacements when the need arises, rather than investing in entirely new systems, thus driving sustained aftermarket demand.

End-Uses Analysis

Pumps Are Mostly Utilized in Industrial Sectors.

Among the end-uses of the pumps, 82.9% of the total global consumption of pumps is in the industrial sector, outperforming agriculture, and residential & commercial sectors, due to the high demand for fluid handling in complex and large-scale processes. Industries such as manufacturing, chemicals, oil and gas, and power generation require pumps to move fluids for critical operations such as cooling, heating, chemical processing, and wastewater management. These sectors need pumps capable of handling large volumes, high pressures, and various fluid types, which makes industrial applications the primary focus.

Additionally, the industrial sector often operates under more rigorous standards, driving the adoption of specialized pumps for efficiency, durability, and compliance. While agriculture and residential sectors do require pumps, their usage is generally less complex and demands lower capacities compared to industrial processes, thus making the industrial sector the dominant consumer.

Key Market Segments:

By Type

- Centrifugal Pumps

- Overhung Impeller

- Between Bearing

- Vertically Suspended

- Positive Displacement Pump

- Rotary Pump

- Vane

- Gear

- Lobe

- Others

- Reciprocating Pump

- Piston

- Diaphragm

- Rotary Pump

By Sales Channel

- Aftermarket

- New Sales

By End-Use

- Industrial

- Oil & Gas

- Water & Wastewater

- Mining

- Chemical and Petrochemical

- Food and Beverage

- Power Generation

- Pharmaceuticals

- Others

- Agriculture

- Residential & Commercial

Drivers

Rapid Urbanization and Industrial Development Drive the Pumps Market.

Rapid urbanization and industrial development are significant drivers of the pumps market. According to the United Nations, over 68% of the global population is projected to reside in urban areas by 2050. This shift necessitates enhanced infrastructure, including water supply, wastewater treatment, and irrigation systems, primary sectors where pumps are integral.

For instance, in India, the Ministry of Housing and Urban Affairs reports that urban water supply and sewerage infrastructure are a key focus, with significant investments in pumping stations and treatment facilities as part of urbanization efforts.

Apart from this, growing sectors such as chemical processing, power generation, and mining require a wide range of pump technologies. The energy production, particularly in oil and gas, relies heavily on specialized pumps for fluid transfer in refining processes. Similarly, in the European Union, the industrial strategy emphasizes sustainable manufacturing, which includes upgrading industrial facilities with advanced pumping systems for efficiency and environmental compliance.

Government-led initiatives and sectoral investments continue to expand pump applications, reinforcing the market’s expansion within urban and industrial contexts. The adoption of pumps is directly linked to policy priorities, such as water resource management and industrial sustainability.

Restraints

Regulatory Compliance and Standards Pose Challenges to the Pumps Market.

Regulatory compliance and adherence to standards present significant challenges for the pumps market, particularly in industries such as water treatment, oil and gas, and chemicals. In the European Union, the European Union’s Ecodesign Directive mandates stringent energy efficiency requirements for pumps, which manufacturers must meet in order to comply with environmental and operational standards. As per the European Commission, these regulations enforce the use of energy-efficient pumps, driving innovation but increasing the complexity and cost of design and manufacturing.

In the United States, the Environmental Protection Agency (EPA) enforces regulations on water quality standards, impacting pump design and performance in wastewater treatment and potable water systems. The Clean Water State Revolving Fund (CWSRF), managed by the EPA, provides financial assistance to municipalities to upgrade aging water infrastructure, often requiring the installation of pumps that meet new regulatory standards for energy consumption and environmental impact.

Additionally, the International Organization for Standardization (ISO) provides guidelines, such as ISO 9906, for testing pump performance and efficiency, which manufacturers must comply with to ensure global market access. These standards, while promoting safety and sustainability, increase the regulatory burden on pump manufacturers, leading to higher operational costs and the need for continuous adaptation to evolving standards.

Opportunity

Application in Agricultural Activities Creates Opportunities in the Pumps Market.

The application of pumps in agricultural activities presents significant opportunities in the pumps market, driven by the growing need for efficient irrigation, water management, and crop protection. According to the Food and Agriculture Organization (FAO), agriculture accounts for approximately 70% of global freshwater withdrawals, emphasizing the critical role of pumps in irrigation systems.

Governments worldwide are investing in modern irrigation infrastructure to enhance agricultural productivity and conserve water. For instance, the Indian government’s Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) aims to improve irrigation efficiency, including the promotion of pumps for micro-irrigation systems, benefiting small-scale farmers.

Additionally, the advancements in precision agriculture are increasing the demand for pumps in fertigation and irrigation systems, where precise water and nutrient delivery are essential for optimizing crop yields. As climate change exacerbates water scarcity, governments and agricultural stakeholders are increasingly focused on sustainable water usage.

For instance, the European Commission’s Water Framework Directive supports water-efficient farming practices, encouraging the use of pumps for irrigation in regions facing water stress. These developments create a growing demand for high-efficiency pump systems in agricultural applications.

Trends

Shift from Traditional Mechanical Pumps to Connected Equipment.

The shift from traditional mechanical pumps to connected, IoT-enabled equipment represents a key trend in the pumps market, driven by advancements in automation, data analytics, and predictive maintenance. According to the U.S. Department of Energy’s Industrial Energy Efficiency report, the integration of connected equipment in industrial processes, including pump systems, allows for real-time monitoring of performance, leading to improved energy efficiency and reduced operational costs.

For instance, the U.S. Municipality has highlighted the use of smart water pumps in municipal water systems to optimize energy usage and reduce non-revenue water losses. These systems, equipped with sensors and communication capabilities, enable operators to remotely monitor pump health and detect potential failures before they occur, reducing downtime and maintenance costs.

In Europe, the European Union’s Ecodesign Directive encourages the adoption of energy-efficient technologies, including connected pumps, in industrial and domestic applications. The European Commission’s Digital Single Market initiative further supports this trend by promoting digital innovations in industries that rely on pumping equipment, making connected pumps a priority in modern infrastructure projects.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Severe Disruptions of the Supply Chains of Pumps.

The geopolitical tensions, including trade disputes and regional conflicts, are influencing the global pumps market, primarily through disruptions in supply chains, increased raw material costs, and altered trade flows. For instance, the ongoing trade tensions between the United States and China have led to tariffs on pump components, impacting manufacturers’ costs and delivery timelines. The U.S. has imposed tariffs on Chinese-made goods, including certain pump components, which has resulted in a shift in procurement strategies and a reassessment of manufacturing footprints.

In Europe, the European Commission has raised concerns about the impact of the Russia-Ukraine conflict on energy supplies, which affects industries reliant on pumps for fluid transport and processing. The disruptions in energy imports, particularly natural gas, have led to reduced industrial output in some regions, impacting pump demand.

Furthermore, in the Middle East, geopolitical instability has affected infrastructure development projects, such as desalination plants and water management systems. Conflicts in regions such as Yemen and Syria have slowed construction, limiting growth in pump demand within those sectors. These geopolitical factors contribute to uncertainty in the market, prompting companies to diversify sourcing and adapt to changing global conditions.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Pumps Market.

In 2025, the Asia Pacific dominated the global pumps market, holding about 54.1% of the total global consumption, driven by rapid industrialization, urbanization, and infrastructure development. According to the UN-Habitat, APAC’s urban population is projected to increase to over a billion people by 2030, highlighting the demand for water, wastewater, and irrigation systems, all of which heavily rely on pumps. In countries such as India and China, government initiatives such as the Smart Cities Mission in India and the 13th Five-Year Plan in China focus on improving water management and wastewater treatment infrastructure, directly driving pump demand.

The region’s growing industrial base further intensifies the need for pumps. The sectors such as chemical manufacturing, power generation, and mining in APAC increasingly rely on pumps for fluid handling and circulation. Additionally, there is increased use of pumps for flood prevention and water supply systems in Japan due to the region’s vulnerability to natural disasters. This expansion in both industrial and infrastructural applications reinforces APAC’s position as the largest market for pumps.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of pumps focus on product innovation, especially in developing energy-efficient and high-performance pumps to meet evolving industry standards, such as those outlined in environmental regulations. Companies invest in R&D to create smarter, IoT-enabled pumps with remote monitoring capabilities for predictive maintenance and operational optimization.

Another strategy is expanding after-sales services, including installation, maintenance, and technical support, to ensure long-term customer relationships and enhance brand loyalty. Furthermore, manufacturers focus on regional diversification, establishing localized production facilities or partnerships in emerging markets, such as the Asia-Pacific, to capitalize on the growing infrastructure and industrial demand.

Key Developments

- In May 2025, Grundfos, a global leader in advanced water technology and pump solutions, revealed the expansion of its facilities in Brookshire, Texas, representing a substantial enlargement of the existing facility.

- In December 2025, Ebara Corporation announced the launch of its dry vacuum pump, MODEL EV-H, and plasma abatement system, MODEL ELF, which were set to commence mass production at the beginning of 2026.

The Major Players in The Industry

- Grundfos Holding A/S

- Xylem

- KSB

- Ebara Corporation

- Flowserve Corporation

- Sulzer Ltd.

- SLB

- Dover Corporation

- Weatherford International plc

- Wilo SE

- Baker Hughes

- Alfa Laval

- ITT Inc.

- Pentair plc

- Danfoss

- Other Key Players

Report Scope

Report Features Description Market Value (2025) USD 66.3 Bn Forecast Revenue (2035) USD 112.2 Bn CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Centrifugal Pumps and Positive Displacement Pumps), By Sales Channel (Aftermarket and New Sales), By End-Use (Industrial, Agriculture, and Residential & Commercial) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Grundfos Holding A/S, Xylem, KSB, Ebara Corporation, Flowserve Corporation, Sulzer Ltd., SLB, Dover Corporation, Weatherford International plc, Wilo SE, Baker Hughes, Alfa Laval, ITT Inc., Pentair plc, Danfoss, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Grundfos Holding A/S

- Xylem

- KSB

- Ebara Corporation

- Flowserve Corporation

- Sulzer Ltd.

- SLB

- Dover Corporation

- Weatherford International plc

- Wilo SE

- Baker Hughes

- Alfa Laval

- ITT Inc.

- Pentair plc

- Danfoss

- Other Key Players

Our Clients

- 180179

- Mar 2026