Global Poultry Processing Equipment Market Size, Share, And Industry Analysis Report By Poultry Type (Chicken, Turkey, Duck), By Equipment Type (Killing and Defeathering, Evisceration, Cut-Up, Deboning and Skinning, Marinating and Tumbling), By Product Type (Fresh Processed, Raw Cooked, Pre-Cooked, Raw Fermented Sausages, Cured, Dried), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181912

- Number of Pages: 262

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

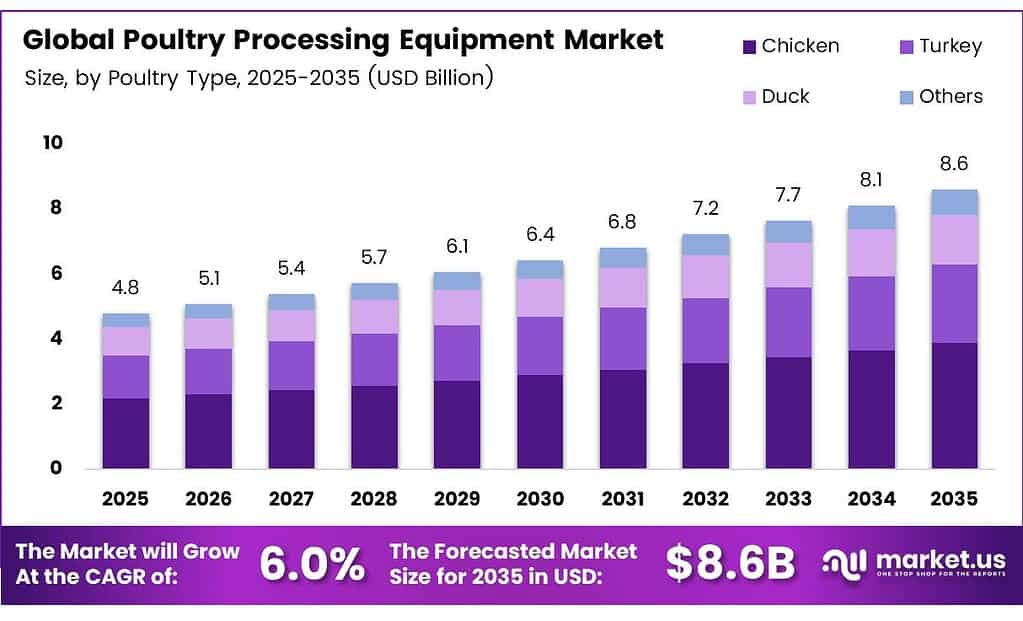

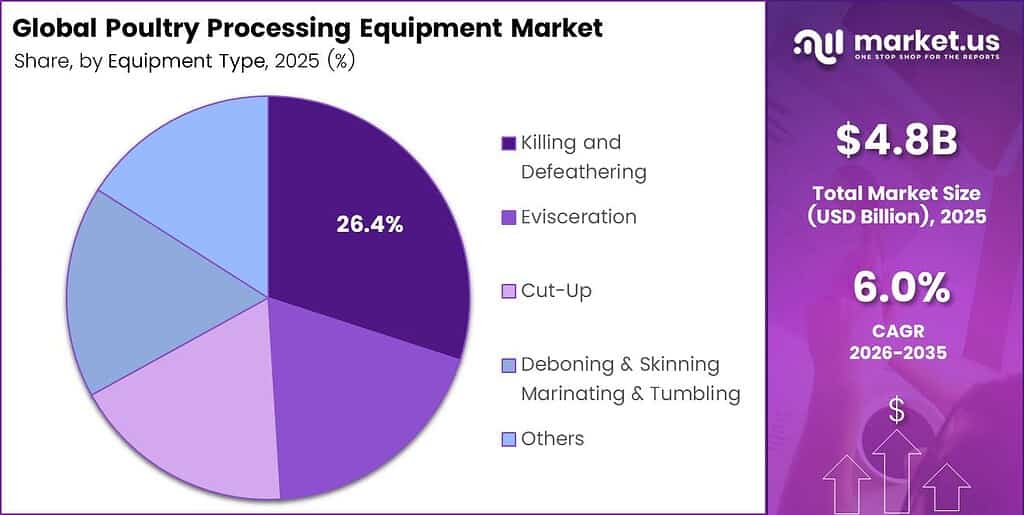

The Global Poultry Processing Equipment Market size is expected to be worth around USD 8.6 billion by 2035 from USD 4.8 billion in 2025, growing at a CAGR of 6.0% during the forecast period 2026 to 2035.

Poultry processing equipment refers to the range of industrial machinery used across slaughterhouses and processing plants. These systems handle killing, defeathering, evisceration, cut-up, deboning, and further processing of poultry. Processors use these machines to meet food safety standards while maintaining high throughput volumes.

The market supports the global poultry supply chain from farm to shelf. Chicken, turkey, and duck processors rely on these systems to scale operations efficiently. Modern equipment integrates automation, hygiene monitoring, and real-time yield management across large-scale facilities worldwide.

China exported $278 million of machinery for the preparation of meat and poultry in 2024, with primary destinations including the United States at $49.5 million, Russia at $16.9 million, and Indonesia at $13.1 million. This signals strong global demand for cost-competitive processing equipment from emerging manufacturing hubs.

The Netherlands exported $93.8 million of machinery parts of machinery for the poultry industry, ranking as the world’s largest exporter in this category. This highlights Europe’s continued dominance in precision processing technology exports. Marel hf. reported revenue of €1.643 billion in 2024, reflecting the scale of global demand for integrated poultry processing systems.

Food safety regulations continue to push equipment upgrades across the industry. USDA and FDA compliance requirements mandate sanitation, traceability, and hygiene controls in processing environments. Consequently, processors invest in advanced equipment that meets evolving federal and international food safety standards throughout the supply chain.

Key Takeaways

- The Global Poultry Processing Equipment Market is valued at USD 4.8 billion in 2025 and projected to reach USD 8.6 billion by 2035, growing at a CAGR of 6.0%.

- Chicken dominates with a 76.3% market share in 2025.

- Killing and Defeathering leads with a 26.4% share.

- Fresh Processed holds the largest share at 29.8%.

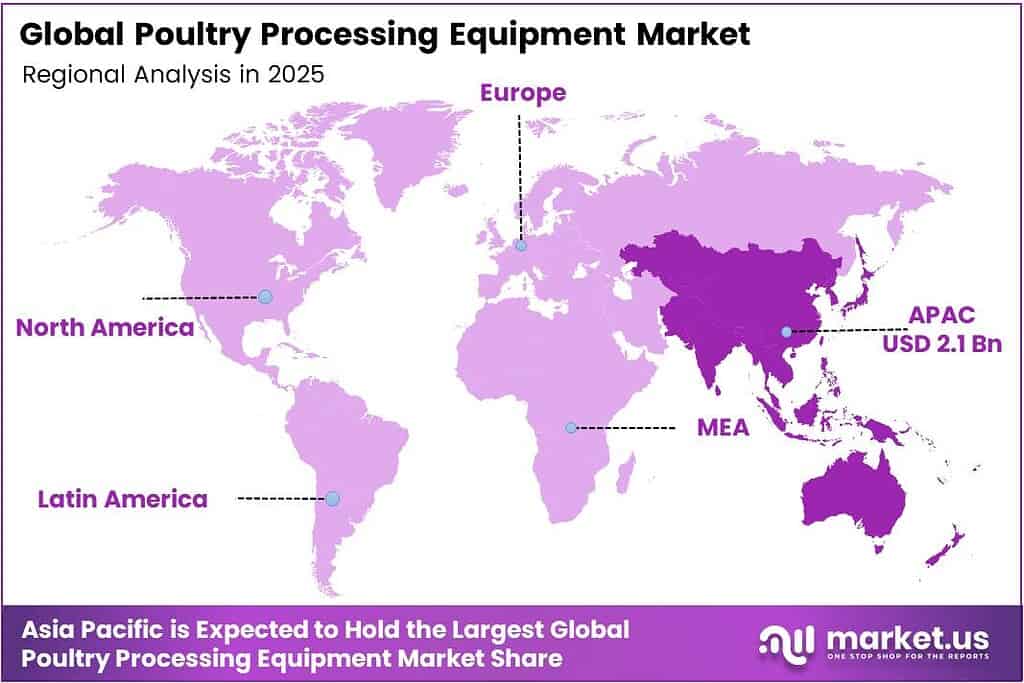

- Asia Pacific dominates the regional landscape with a 43.1% share, valued at USD 2.1 billion.

By Poultry Type Analysis

Chicken dominates with 76.3% due to its high global consumption volume and widespread industrial processing demand.

In 2025, Chicken held a dominant market position in the By Poultry Type segment of the Poultry Processing Equipment Market, with a 76.3% share. Chicken remains the most consumed poultry globally. Processors invest heavily in automated chicken processing lines to manage scale, improve yield, and reduce labor dependency across large-volume facilities.

Turkey processing represents a significant secondary segment driven by seasonal and year-round demand. North American and European processors adopt specialized turkey processing equipment to handle larger bird sizes. Moreover, growing exports from the United States and Brazil expand turkey processing capacity requirements in established and emerging markets.

Duck processing equipment sees rising adoption, particularly across the Asia Pacific markets. China and Vietnam lead duck consumption globally, driving demand for specialized defeathering and cut-up machinery. Consequently, regional processors are upgrading duck processing lines to meet export quality standards and growing domestic protein consumption trends.

By Equipment Type Analysis

Killing and Defeathering dominates with 26.4% due to its critical role as the first and highest-throughput stage in the processing chain.

In 2025, Killing and Defeathering held a dominant market position in the By Equipment Type segment of the Poultry Processing Equipment Market, with a 26.4% share. This equipment stage handles the highest bird volumes per hour. Processors prioritize investment in high-speed killing and defeathering systems to maintain throughput and minimize line downtime.

Evisceration equipment follows as a critical hygiene-focused stage in processing lines. Modern evisceration systems integrate automated inspection and contamination controls compliant with USDA and EU food safety standards. Therefore, processors consistently upgrade evisceration technology to meet regulatory expectations and reduce the risk of product recalls.

Cut-Up equipment enables portioning into standard retail and foodservice formats such as breasts, thighs, and wings. Automated cut-up systems improve yield accuracy and reduce manual trimming waste. Additionally, growing consumer demand for pre-cut and value-added poultry portions continues to drive investment in advanced cut-up machinery across processing facilities.

By Product Type Analysis

Fresh Processed dominates with 29.8% due to strong consumer preference for minimally processed, refrigerated poultry products.

In 2025, Fresh Processed held a dominant market position in the By Product Type segment of the Poultry Processing Equipment Market, with a 29.8% share. Retail and foodservice channels drive strong demand for fresh, chilled poultry. Processors invest in high-speed chilling and packaging systems to maintain freshness standards for domestic and export distribution.

Raw Cooked products include nuggets, patties, and formed poultry items processed with heat before packaging. Processors serving quick-service restaurant supply chains prioritize raw-cooked processing equipment for consistent quality and throughput. Moreover, growing global demand for convenient protein formats continues to support this segment’s expansion across processing facilities.

Pre-Cooked poultry products cater to ready-to-eat and meal kit markets experiencing rapid growth globally. Processing equipment for pre-cooked lines integrates cooking, chilling, and modified atmosphere packaging technologies. Consequently, manufacturers serving retail and e-commerce grocery channels are upgrading pre-cooked processing capacity to meet rising consumer convenience expectations.

Key Market Segments

By Poultry Type

- Chicken

- Turkey

- Duck

- Others

By Equipment Type

- Killing and Defeathering

- Evisceration

- Cut-Up

- Deboning and Skinning

- Marinating and Tumbling

- Others

By Product Type

- Fresh Processed

- Raw Cooked

- Pre-Cooked

- Raw Fermented Sausages

- Cured

- Dried

- Others

Emerging Trends

AI-Driven Monitoring Transforms Plant Operations

Real-time AI performance monitoring tools are reshaping poultry processing plant operations globally. Processors now deploy intelligent sensor networks that track throughput, yield loss, and equipment health in real time. China’s exports of meat and poultry preparation machinery reached $24.1 million in March 2025, a 17.7% year-over-year increase, signaling rising global adoption of new processing technologies.

Air-Chilled Processing and Advanced Robotics Gain Ground

Innovative air-chilled processing lines are gaining momentum for superior sanitation and resource efficiency across modern facilities. Processors adopt these systems to meet retail buyer requirements for chemical-free chilling and extended shelf life. Moreover, advanced robotics workshops now emphasize animal care protocols and operational safety, reflecting a broader industry shift toward precision automation that aligns welfare, safety, and efficiency objectives within integrated processing environments.

Drivers

Labor Shortages and AI Adoption Accelerate Equipment Investment

Persistent labor shortages in poultry processing plants are accelerating the adoption of AI and robotics solutions across the industry. Processors facing chronic workforce gaps invest in automated systems that reduce dependence on manual labor. The United States imported $103 million of machinery parts of machinery for the poultry industry in 2022, making it the world’s largest importer, reflecting strong domestic demand for processing automation solutions.

USDA Grants and Food Safety Standards Drive Modernization

Federal USDA Meat and Poultry Processing Expansion Grants are enabling capacity modernization and supply chain resilience for processors across the United States. Furthermore, growing demand for further-processed and specialized poultry products is driving significant equipment specialization investments. Heightened focus on food safety and sanitation protocols, highlighted at industry events like IPPE 2026, is also fueling advanced hygiene technology upgrades across processing plants globally.

Restraints

Regulatory Delays Create Investment Uncertainty for Processors

Ongoing regulatory delays in poultry grower payment systems and capital improvement rules are creating investment uncertainty across the industry. Processors hesitate to commit large capital expenditures when compliance timelines remain unclear. Marel hf. reported operating cash flow of €79.3 million for the first nine months of 2024, indicating that even leading manufacturers face reinvestment pressure during periods of market uncertainty.

Capital Costs and Supply Constraints Slow Large-Scale Upgrades

Escalating capital costs combined with breeder supply constraints are slowing large-scale equipment modernization projects across the poultry sector. High upfront investment requirements place pressure on mid-size processors with limited access to financing. Moreover, supply chain disruptions in specialty components and breeder stock availability create compounding delays that further extend the timeline for major processing facility upgrade programs.

Growth Factors

Intelligent Automation and USDA Research Funding Expand Access

Integration of scalable intelligent automation systems for small and mid-size processors is gaining momentum through USDA-funded research initiatives. Marel hf. recorded quarterly orders of €402.5 million in Q3 2024, indicating continued global capital expenditure by poultry processors on automation equipment. Consequently, the market is benefiting from both public funding support and strong private sector demand for next-generation processing systems.

Sustainable Chilling Technologies and Workforce Programs Drive Expansion

Development and adoption of sustainable non-CO2 inline chilling technologies are improving efficiency and shelf life across modern poultry facilities. Collaborative workforce development programs linking safety training with next-generation processing equipment are also creating a skilled talent pipeline. Additionally, John Bean Technologies (JBT Marel) reported fourth-quarter 2024 orders of $523 million and a backlog of $721 million, indicating a strong demand pipeline for poultry and protein processing equipment globally.

Regional Analysis

Asia Pacific Dominates the Poultry Processing Equipment Market with a Market Share of 43.1%, Valued at USD 2.1 Billion

Asia Pacific leads the global poultry processing equipment market with a 43.1% share, valued at USD 2.1 billion in 2025. China, India, and Southeast Asian nations drive demand through expanding poultry production volumes and rising protein consumption. Moreover, government initiatives supporting the modernization of food processing infrastructure across the region continue to fuel sustained equipment investment and capacity expansion.

North America represents a mature and technology-intensive poultry processing equipment market. The United States leads regional demand, supported by large-scale chicken and turkey processing operations and significant USDA grant-driven modernization activity. Additionally, stringent food safety regulations continue to push processors toward advanced automation, hygiene systems, and high-throughput processing lines across the region.

Europe maintains a strong position in both poultry processing equipment manufacturing and consumption. Germany, the Netherlands, and Denmark serve as leading exporters of precision processing technology and components globally. Furthermore, EU food safety directives and sustainability mandates continue to drive demand for compliant, energy-efficient processing equipment across the region’s established poultry industry.

The Middle East and Africa region shows growing investment in domestic poultry processing capacity driven by food security priorities. GCC countries are expanding integrated poultry processing facilities to reduce dependence on imported protein products. Consequently, equipment demand across this region is rising as governments prioritize local production infrastructure and cold chain development to support growing urban food demand.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Marel hf. stands as one of the most diversified and globally recognized poultry processing equipment manufacturers in the market. The company delivers integrated processing systems spanning slaughter, evisceration, cut-up, deboning, and further processing. Marel operates across more than 30 countries and serves processors of all sizes. Its strong order book and global service network reinforce its leadership position in the industry.

John Bean Technologies Corporation, now operating as JBT Marel following its merger with Marel, represents a combined powerhouse in food and protein processing equipment. The company delivers solutions across portioning, cooking, freezing, and inspection for poultry and other protein processors. Its broad product portfolio and global customer base position it as a full-line equipment partner for large-scale poultry processing operations worldwide.

GEA Group AG provides advanced poultry processing and food technology solutions designed for efficiency, hygiene, and sustainability compliance. The company’s systems address thermal processing, chilling, portioning, and packaging across the poultry supply chain. GEA’s engineering expertise and commitment to sustainable processing technologies make it a preferred partner for processors pursuing operational modernization and regulatory compliance across European and global markets.

Meyn Food Processing Technology B.V. specializes in complete poultry processing lines with a strong emphasis on automation, animal welfare, and yield optimization. The company delivers systems from live bird handling through final product packaging. Meyn’s focus on precision cutting and intelligent line management helps processors improve throughput efficiency, reduce product giveaway, and maintain consistent product quality across high-volume industrial processing environments.

Top Key Players in the Market

- Marel hf

- John Bean Technologies Corporation

- GEA Group AG

- Meyn Food Processing Technology B.V.

- Baader Group

- Perdue Farms Inc

- Sanderson Farms Inc

- Bachoco

- Koch Foods

- Tyson Foods Inc

- Charoen Pokphand Group

Recent Developments

- In February 2026, GEA launched the CookStar First, a compact twin-zone spiral oven for small- to mid-sized producers. It supports coated poultry, steam-cooked products, and further-processed items, emphasizing “home-cooked” quality, energy efficiency, and versatility alongside plant-based applications.

- In October 2025, Meyn manufacturing, innovation, and experience campus in Westminster, South Carolina. This expands local production, engineering, training, and service for America’s poultry processors, including full processing lines for hands-on optimization. A related South Carolina state announcement referenced an expansion creating jobs, aligning with the same Oconee County/Westminster footprint.

Report Scope

Report Features Description Market Value (2025) USD 4.8 Billion Forecast Revenue (2035) USD 8.6 Billion CAGR (2026-2035) 6.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Poultry Type (Chicken, Turkey, Duck, Others), By Equipment Type (Killing and Defeathering, Evisceration, Cut-Up, Deboning and Skinning, Marinating and Tumbling, Others), By Product Type (Fresh Processed, Raw Cooked, Pre-Cooked, Raw Fermented Sausages, Cured, Dried, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Marel hf, John Bean Technologies Corporation, GEA Group AG, Meyn Food Processing Technology B.V., Baader Group, Perdue Farms Inc, Sanderson Farms Inc, Bachoco, Koch Foods, Tyson Foods Inc, Charoen Pokphand Group Customization Scope Customization for segments and region/country levels will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Poultry Processing Equipment MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Poultry Processing Equipment MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Marel hf

- John Bean Technologies Corporation

- GEA Group AG

- Meyn Food Processing Technology B.V.

- Baader Group

- Perdue Farms Inc

- Sanderson Farms Inc

- Bachoco

- Koch Foods

- Tyson Foods Inc

- Charoen Pokphand Group

Our Clients

- 181912

- March 2026