Global Passenger Car Motor Oil Market Size, Share, And Enhanced Productivity By Grade (Mineral, Synthetic, Semi-Synthetic), By Engine Type (Gasoline, Diesel, Hybrid (Gasoline+Electric)), By Viscosity (Low Viscosity Grades (0W-16, 0W-20, 5W-20), Medium Viscosity Grades (5W-30, 10W-30), High Viscosity Grades (10W-40, 15W-40, 20W-50)), By Application (Passenger Cars, SUVs, Light Trucks), By Distribution Channel (Retail, OEM, Service Centre, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179526

- Number of Pages: 273

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

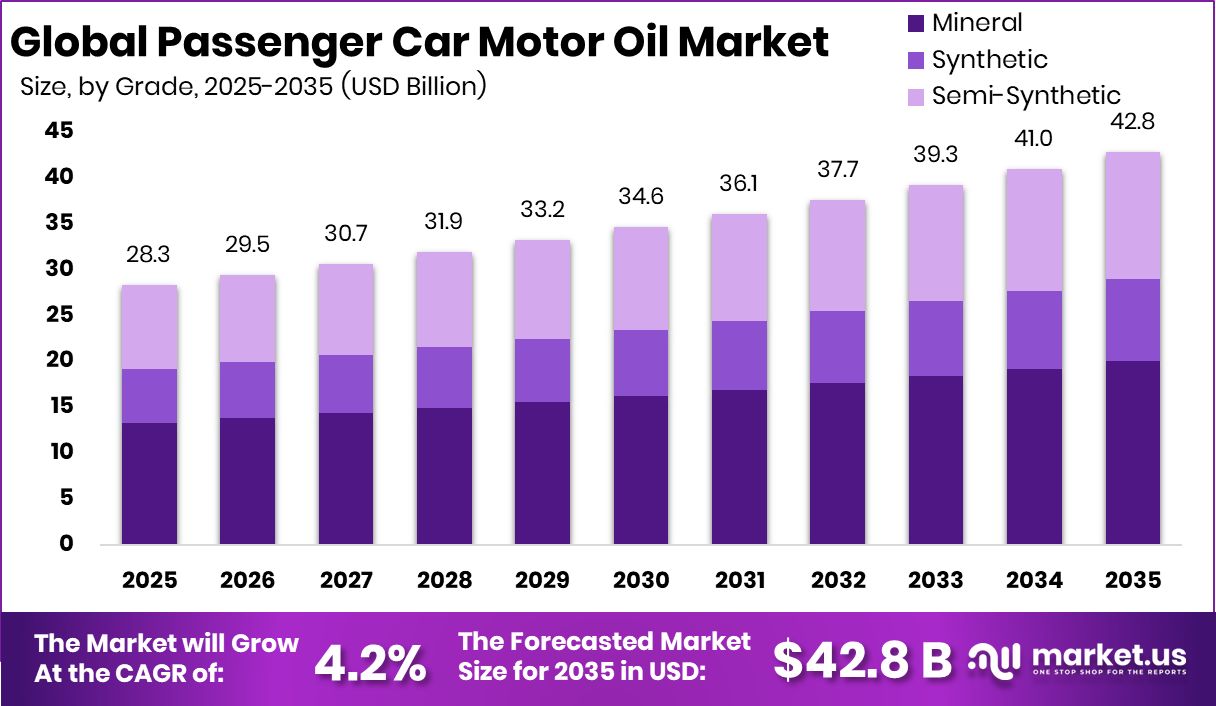

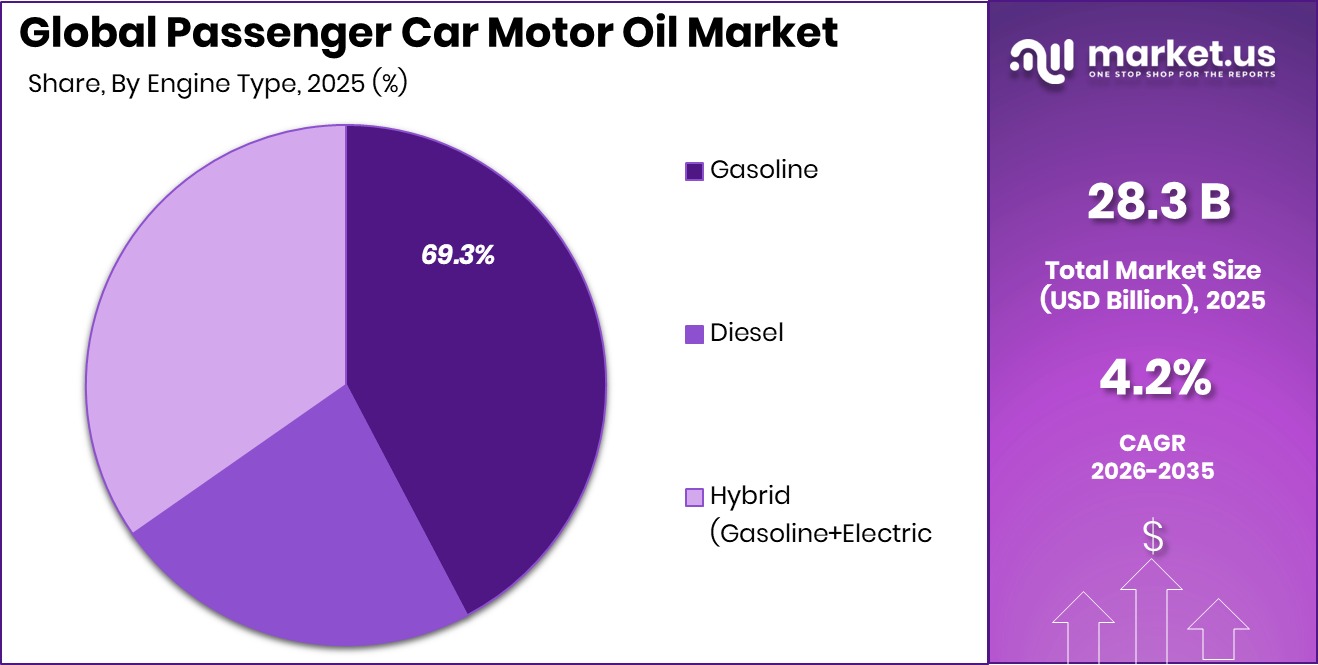

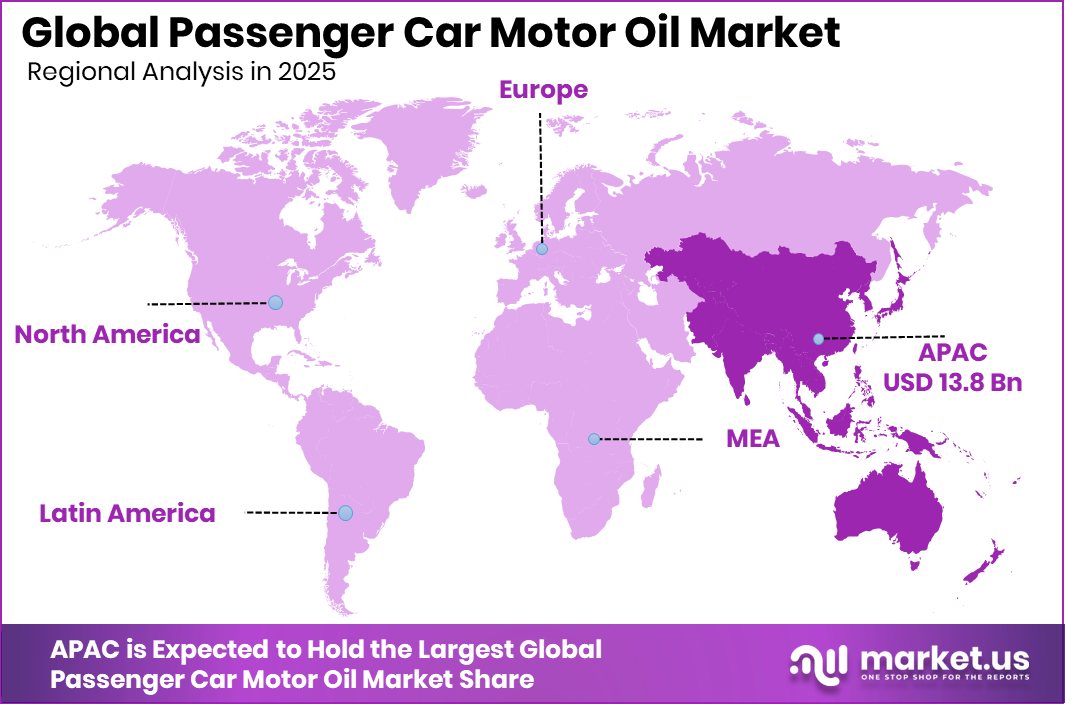

The Global Passenger Car Motor Oil Market is expected to be worth around USD 42.8 billion by 2035, up from USD 28.3 billion in 2025, and is projected to grow at a CAGR of 4.2% from 2026 to 2035. The Asia Pacific region dominates with 48.9% market share, touching USD 13.8 Bn.

The Passenger Car Motor Oil Market covers a wide mix of formulations such as mineral, synthetic, and semi-synthetic oils, serving different engine types, including gasoline, diesel, and hybrid systems. These oils are essential for reducing friction, controlling heat, and keeping engines clean, especially across varied viscosity grades ranging from low to high. The market is shaped by applications across passenger cars, SUVs, and light trucks, delivered mainly through retail, OEM channels, and service centres.

Passenger Car Motor Oil refers to lubricants specifically designed to protect vehicle engines from wear, sludge, and overheating. It supports smooth running and helps maintain fuel economy. The Passenger Car Motor Oil Market represents the global industry involved in producing, distributing, and selling these oils for everyday vehicles used by personal and commercial drivers.

Growth in this market is supported by rising mobility needs and the shift toward cleaner engines. Increasing attention to alternative fuels also influences lubrication trends, highlighted by recent commitments such as the EU awarding over €600 million to alternative fuel projects, and airlines joining a $150 million sustainable aviation fuel fund. These transitions push demand for advanced oils suitable for evolving engine technologies.

At the same time, global financing trends shape long-term opportunities. Reports show $869 billion in fossil-fuel finance in 2024, with the world’s largest banks pledging the same amount to fossil-fuel firms, while major banks supplied $43 billion over ten years to large fuel producers. Even the UK development body still holds $700 million in overseas fossil-fuel assets. These figures reflect how shifting financial flows and energy transitions will influence lubricant needs in the coming years.

Key Takeaways

- The Global Passenger Car Motor Oil Market is expected to be worth around USD 42.8 billion by 2035, up from USD 28.3 billion in 2025, and is projected to grow at a CAGR of 4.2% from 2026 to 2035.

- The Passenger Car Motor Oil Market shows strong demand, with mineral grades holding 46.8% share.

- Gasoline engines dominate the Passenger Car Motor Oil Market, accounting for nearly 69.3% usage worldwide.

- Medium viscosity grades like 5W-30 lead the Passenger Car Motor Oil Market with 48.6% share.

- Passenger cars significantly influence the Passenger Car Motor Oil Market, contributing a major 63.1% portion.

- Retail channels continue driving the Passenger Car Motor Oil Market forward, securing around 44.5% distribution.

- In the Asia Pacific, the market commands a 48.9% share valued at USD 13.8 Bn.

By Grade Analysis

Passenger Car Motor Oil Market shows mineral grade dominating with a strong 46.8% share.

In 2025, the Passenger Car Motor Oil Market continues to be shaped strongly by mineral-based formulations, which hold a dominant 46.8% share. This segment remains influential because many vehicle owners still prefer affordable and widely compatible motor oils, especially in markets where older car fleets are common. Mineral oils provide sufficient lubrication for everyday driving conditions, making them a dependable option for cost-sensitive consumers.

While synthetic and semi-synthetic options are rising, mineral oils still anchor the market due to stable demand from developing economies. Workshops and small service centers also rely heavily on these oils because of their predictable pricing and broad OEM acceptance. Overall, the mineral grade segment remains a foundational market pillar in 2025.

By Engine Type Analysis

Passenger Car Motor Oil Market remains gasoline-engine dominated, holding a significant 69.3% share.

In 2025, gasoline engines continue to dominate the Passenger Car Motor Oil Market, capturing a strong 69.3% share. This leadership is driven by the sheer number of gasoline-powered cars across global roads, particularly in urban areas where compact and mid-size vehicles remain the preferred mobility option. The rising adoption of turbocharged gasoline engines also increases the need for oils designed to handle higher temperatures and friction levels.

Consumers prioritize smoother performance and fuel economy, both of which rely heavily on reliable engine lubrication. As gasoline vehicles maintain their widespread presence in both mature and emerging automotive markets, demand for compatible motor oils stays consistently high, making the gasoline segment the most influential contributor in 2025.

By Viscosity Analysis

Passenger Car Motor Oil Market sees medium viscosity oils leading with a 48.6% share.

In 2025, medium viscosity grades such as 5W-30 and 10W-30 hold a significant 48.6% share of the Passenger Car Motor Oil Market, reflecting strong preference across mainstream vehicle types. These grades strike a dependable balance between engine protection, cold-start performance, and fuel efficiency, making them suitable for various climates and driving patterns.

Automakers commonly recommend medium-viscosity oils for modern passenger cars due to their proven ability to reduce wear and support longer drain intervals. Their versatility ensures ongoing demand from both personal vehicle owners and service stations. With engine technologies continually evolving toward better thermal stability, these viscosity grades remain the key choice for drivers seeking practical and reliable engine lubrication in 2025.

By Application Analysis

The passenger car motor oil market is dominated by passenger cars, controlling a 63.1% share.

In 2025, passenger cars continue to dominate the overall motor oil landscape with a commanding 63.1% market share. The global expansion of personal vehicle ownership, particularly in Asia, Europe, and North America, ensures steady consumption of engine oils tailored to daily commuting and long-distance travel. Drivers increasingly prioritize smoother engine performance and extended service life, which keeps demand robust for high-quality motor oils.

As urbanization accelerates and household incomes rise in developing regions, more families opt for private cars, further reinforcing the segment’s strength. Routine servicing, manufacturer recommendations, and higher annual mileage all contribute to sustained motor oil usage. With passenger cars remaining the backbone of road mobility, this segment retains its central role in 2025.

By Distribution Channel Analysis

Passenger Car Motor Oil Market records retail distribution dominance with a notable 44.5% share.

In 2025, the retail channel secures a substantial 44.5% share of the Passenger Car Motor Oil Market, driven by rising consumer preference for convenient purchasing options. Car owners frequently buy oils directly from automotive shops, supermarkets, and independent retailers as part of their routine maintenance habits. Many consumers trust retail outlets for authentic products and accessible price comparisons.

The availability of multiple brands and packaging sizes makes retail stores a reliable choice for do-it-yourself customers who prefer home oil changes. Additionally, expanding retail networks in suburban and rural areas supports steady product movement. With retail continuing to offer convenience, visibility, and availability, it remains a major distribution pathway for passenger car motor oils in 2025.

Key Market Segments

By Grade

- Mineral

- Synthetic

- Semi-Synthetic

By Engine Type

- Gasoline

- Diesel

- Hybrid (Gasoline+Electric)

By Viscosity

- Low Viscosity Grades (0W-16, 0W-20, 5W-20)

- Medium Viscosity Grades (5W-30, 10W-30)

- High Viscosity Grades (10W-40, 15W-40, 20W-50)

By Application

- Passenger Cars

- SUVs

- Light Trucks

By Distribution Channel

- Retail

- OEM

- Service Centre

- Others

Driving Factors

Growing vehicle ownership increases oil demand

Growing vehicle ownership continues to push the Passenger Car Motor Oil Market forward as more households rely on personal transportation for everyday mobility. Regular maintenance, higher annual mileage, and a steady increase in road-active vehicles naturally raise the demand for engine oils across retail and service channels. This rising flow of consumers aligns with broader investment activities shaping fuel-dependent industries.

A notable example is Blackharbor BD announcing a $500 million funding capacity for gas, diesel, oil sectors, and luxury home builders, showing how financial support for fuel-heavy sectors indirectly reinforces lubricant needs. As personal mobility expands, these combined factors keep engine oil consumption steady and widely distributed across global markets.

Restraining Factors

Longer oil-change intervals reduce usage

Longer oil-change intervals continue to influence the Passenger Car Motor Oil Market by reducing the frequency at which drivers require lubrication services. Modern engines and improved oil formulations allow vehicles to run more miles before servicing, lowering overall consumption. This restraint becomes more pronounced as cleaner engines and improved monitoring systems extend replacement cycles.

Added to this is the ongoing shift toward electric mobility. A major influence comes from VW’s $2 billion penalty for the diesel scam, which led to Electrify America building a nationwide electric charging network to boost the EV market, accelerating the adoption of vehicles that require far less motor oil. Together, these elements slow traditional lubricant demand.

Growth Opportunity

Rising hybrid vehicles create formulation needs

Rising hybrid vehicle adoption presents a clear opportunity for the Passenger Car Motor Oil Market, as hybrid engines still rely on specialized lubricants capable of handling frequent stop-start cycles and varying thermal loads. These engines require tailored formulations to maintain cleanliness and fuel economy, opening space for advanced oil development. Growth is further shaped by global investment patterns that support conventional engines in mixed-fleet regions.

A key example is Ukraine receiving funding for 40 Wabtec diesel locomotives, signaling ongoing reliance on fuel-based transport systems. Such developments maintain long-term relevance for engine oils, especially in regions where hybrid adoption grows alongside continued use of internal combustion systems.

Latest Trends

Shift toward low-viscosity performance oils

The market is witnessing a clear shift toward low-viscosity performance oils as automakers and consumers look for improved fuel economy, smoother cold starts, and reduced friction. These lighter formulations help engines operate more efficiently while meeting modern emission norms. The trend is influenced by decisions within the automotive sector regarding future powertrain direction.

A notable occurrence includes a major car brand axing £222 million in electric vehicle funding in favor of a £659 million petrol and diesel boost, signaling a renewed emphasis on traditional engines. This pivot reinforces demand for modern low-viscosity oils, ensuring they remain central to evolving engine designs and service requirements.

Regional Analysis

Asia Pacific holds 48.9% of the Passenger Car Motor Oil Market, reaching USD 13.8 Bn.

In the Passenger Car Motor Oil Market, Asia Pacific remains the dominant regional cluster, accounting for 48.9% of total demand and reaching a valuation of USD 13.8 billion. This leadership is supported by a large passenger car population, rising maintenance activity, and consistent vehicle usage across emerging economies within the region.

In contrast, North America reflects stable consumption patterns driven by regular servicing habits and a mature automotive landscape. Europe shows steady demand supported by stringent vehicle care practices and a strong aftermarket structure.

Meanwhile, the Middle East & Africa exhibit moderate growth, influenced by expanding vehicle ownership in urban centers. Latin America continues to rely on the aftermarket segment, with rising passenger car usage contributing to consistent oil replacement cycles. Across all regions, Asia Pacific leads decisively, shaping the overall market direction through its substantial share and economic scale.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, ExxonMobil continues to shape the global Passenger Car Motor Oil Market through its long-standing expertise in engine lubrication technologies and its strong product positioning across major automotive channels. The company’s focus on developing motor oils that support engine cleanliness and long-drain performance keeps it well aligned with evolving customer expectations. Its established retail presence and trusted product portfolio help maintain relevance as drivers increasingly prioritize consistent vehicle maintenance and dependable engine protection.

Shell plc remains a central force in the market, leveraging its broad global network and brand recognition to strengthen its position among passenger car owners. The company’s emphasis on engine oils engineered for smooth performance and heat stability allows it to meet diverse climate and driving conditions. Shell’s established lubricant distribution channels, service center partnerships, and consumer-focused product communication contribute to sustained acceptance across various markets, especially where routine servicing is a priority for car owners.

BP plc continues to maintain its foothold in 2025 by offering passenger car motor oils designed to support engine reliability in both older and newer vehicle models. The company’s ability to balance performance formulation with broad market accessibility keeps its products visible across service workshops and retail outlets. BP’s ongoing commitment to strengthening its lubricant portfolio ensures steady participation in a market driven by regular oil change cycles and consumer trust in well-established automotive brands.

Top Key Players in the Market

- ExxonMobil

- Shell plc

- BP plc

- Chevron Corporation

- TotalEnergies

- Sinopec

- PetroChina

- Valvoline Inc.

- FUCHS

- Petronas Lubricants International

Recent Developments

- In September 2025, ExxonMobil started up new lubricant and fuel production units at its Singapore complex, boosting its ability to make high-value base stocks used in engine oils, including those for passenger cars. The facility increases Group II base stock capacity, which is a key raw material for motor oils, improving supply chain strength and meeting customer needs.

- In April 2024, Shell introduced new performance motor oil products under its Shell Helix Ultra range, designed to help car engines deliver better power and fuel efficiency. These updated oils meet higher specifications and offer improved protection for modern gasoline engines. This launch aimed to give drivers more reliable lubrication and stronger engine performance across different regions.

Report Scope

Report Features Description Market Value (2025) USD 28.3 Billion Forecast Revenue (2035) USD 42.8 Billion CAGR (2026-2035) 42.8 Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Grade (Mineral, Synthetic, Semi-Synthetic), By Engine Type (Gasoline, Diesel, Hybrid (Gasoline+Electric)), By Viscosity (Low Viscosity Grades (0W-16, 0W-20, 5W-20), Medium Viscosity Grades (5W-30, 10W-30), High Viscosity Grades (10W-40, 15W-40, 20W-50)), By Application (Passenger Cars, SUVs, Light Trucks), By Distribution Channel (Retail, OEM, Service Centre, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ExxonMobil, Shell plc, BP plc , Chevron Corporation, TotalEnergies, Sinopec, PetroChina, Valvoline Inc., FUCHS, Petronas Lubricants International Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Passenger Car Motor Oil MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Passenger Car Motor Oil MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ExxonMobil

- Shell plc

- BP plc

- Chevron Corporation

- TotalEnergies

- Sinopec

- PetroChina

- Valvoline Inc.

- FUCHS

- Petronas Lubricants International

Our Clients

- 179526

- February 2026