Global Intrinsically Safe Equipment Market Size, Share, Growth Analysis Product (Sensors, Detectors, Switches, Transmitters, Isolators, LED Indicators, Others), Zone (Zone 0, Zone 1, Zone 2, Zone 20, Zone 21, Zone 22), Class (Class 1, Class 2, Class 3), End Use Industry (Oil and Gas, Mining, Power, Chemical and Petrochemical, Processing, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180591

- Number of Pages: 391

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

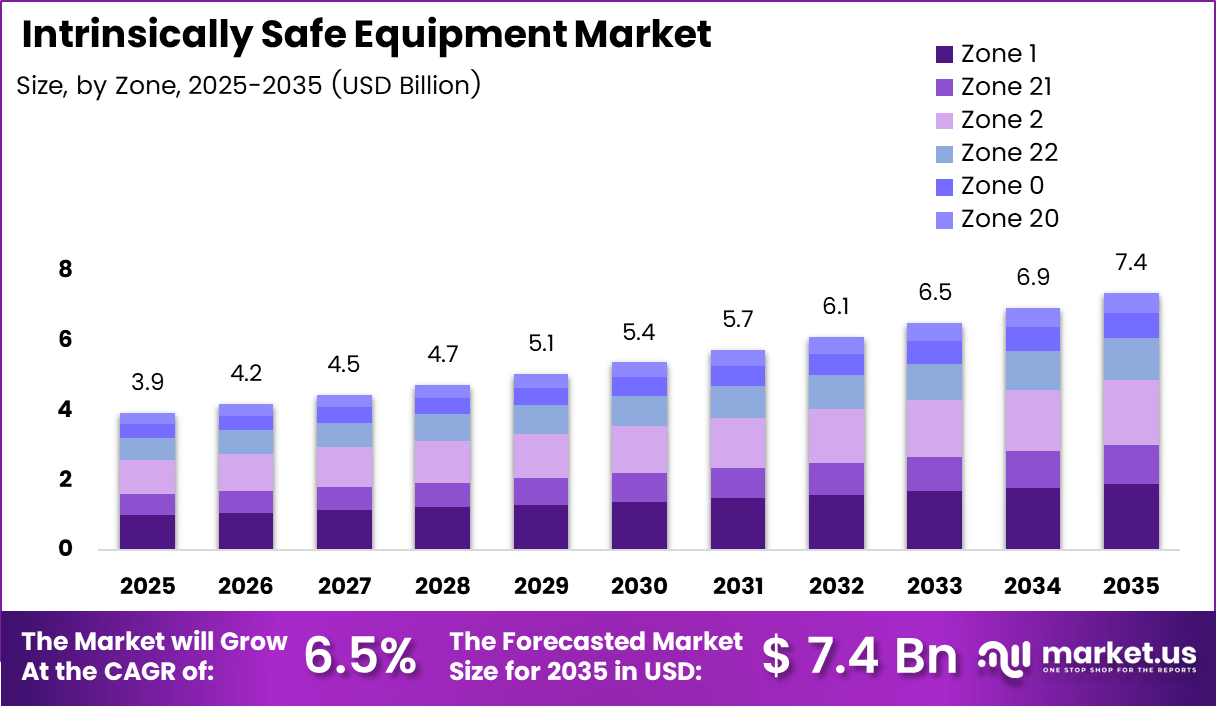

Global Intrinsically Safe Equipment Market size is expected to be worth around USD 7.4 Billion by 2035 from USD 3.9 Billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

The intrinsically safe equipment market encompasses devices and systems specifically engineered for use in hazardous environments where flammable gases, vapors, or combustible dust may be present. These products are designed to prevent ignition by limiting the energy available in electrical circuits. Moreover, they are essential across industries such as oil and gas, mining, chemicals, and power generation.

Expanding operations in oil and gas, mining, and chemical processing sectors across emerging economies are generating significant new demand. Governments in Asia Pacific, the Middle East, and Africa are investing heavily in energy infrastructure and industrial capacity. Consequently, the need for certified hazardous area equipment including sensors, transmitters, and communication devices is growing in tandem with broader industrial development activity.

The market is also benefiting from rapid technological advancement in industrial automation and the Industrial Internet of Things. Smart intrinsically safe sensors and connected monitoring systems are increasingly deployed to enhance operational efficiency and predictive maintenance in hazardous facilities. Moreover, the integration of cloud-enabled diagnostics is creating new value-added capabilities that are accelerating adoption across the global oil and gas and mining sectors.

Intrinsic safety is a low-energy protection technique where current, voltage, and power are reduced to levels too low to cause ignition. Generally, the maximum power level available in such systems is less than 1.3W. Additionally, electrical currents are engineered to remain below 29V DC and under 300 mA, ensuring they can never ignite a flammable environment under normal or fault conditions.

Intrinsically safe devices also operate within strict temperature thresholds, typically not exceeding 135°C. This ensures safe operation even in the most demanding industrial environments. Consequently, these temperature and energy limits make intrinsically safe equipment the preferred choice for hazard zone applications where conventional electrical devices pose unacceptable ignition risks.

Growing industrial safety regulations and mandatory compliance requirements are key forces driving market expansion. Regulatory frameworks such as ATEX in Europe and NEC in North America require certified intrinsically safe equipment in designated hazard zones. Therefore, industries operating in flammable or explosive environments must continually invest in certified devices to maintain legal compliance and protect worker safety.

Key Takeaways

- The global Intrinsically Safe Equipment Market is valued at USD 3.9 Billion in 2025 and is projected to reach USD 7.4 Billion by 2035, at a CAGR of 6.5%.

- By Product, Sensors dominate with a 22.3% market share in 2025.

- By Zone, Zone 1 leads the segment with a 25.9% share in 2025.

- By Class, Class 1 holds the largest share at 65.9% in 2025.

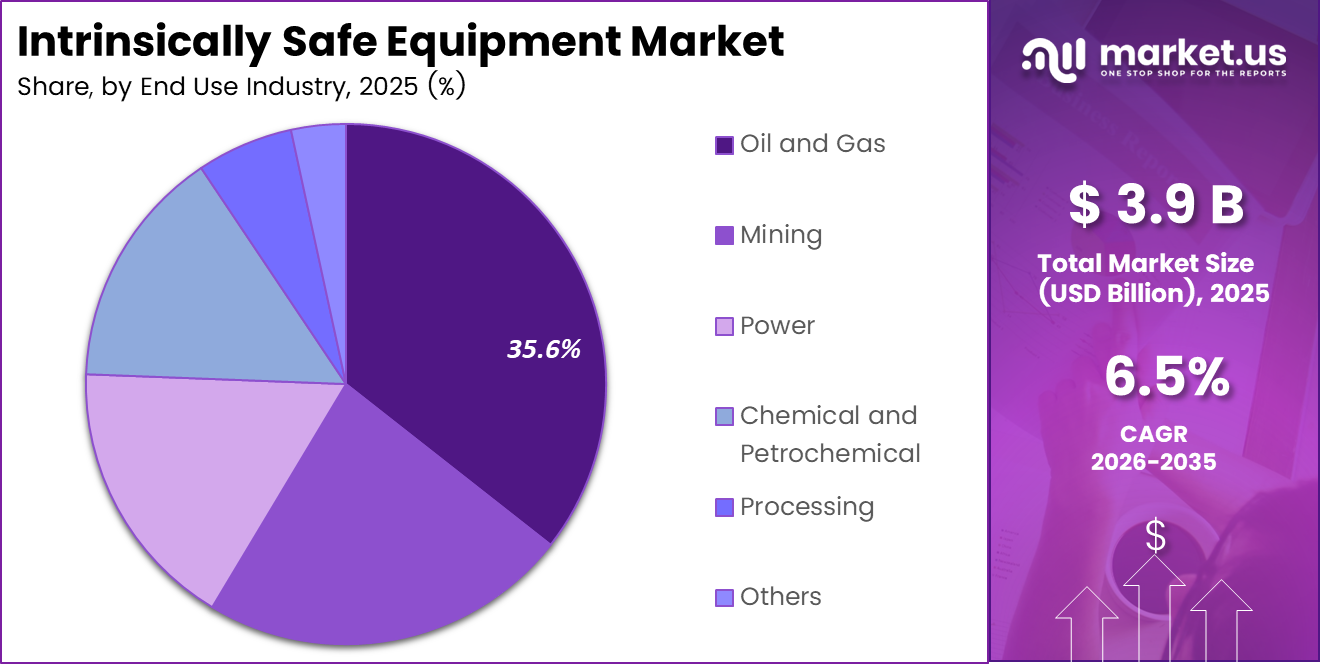

- By End Use Industry, Oil and Gas is the dominant sector with a 35.6% share in 2025.

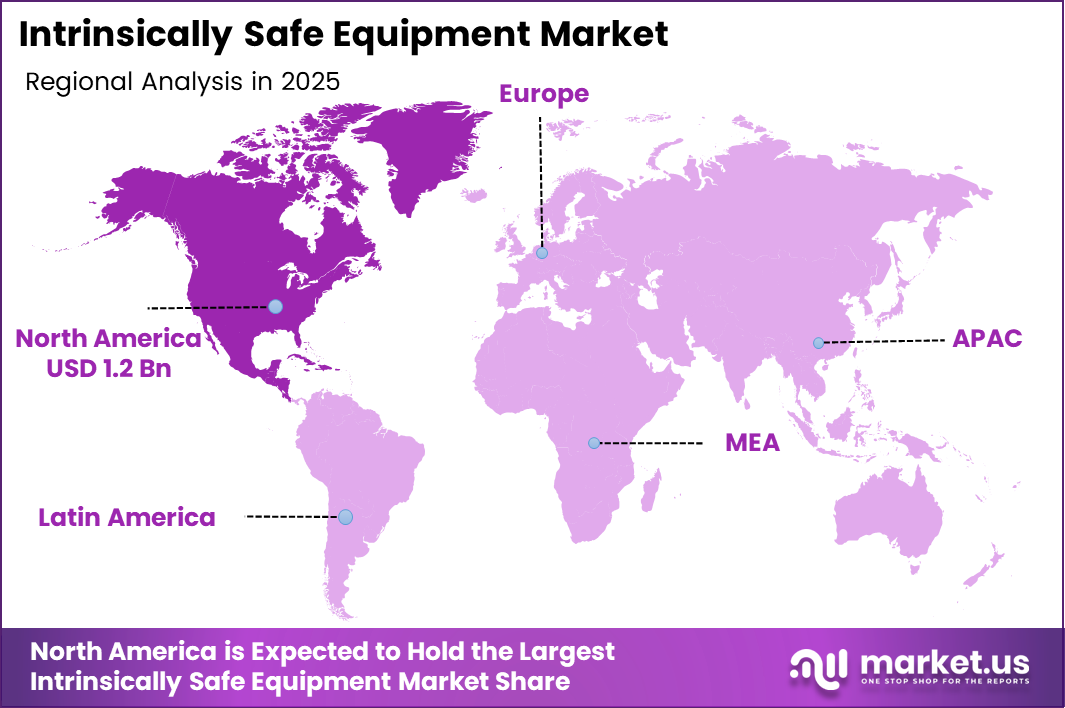

- North America dominates the regional landscape with a 32.1% share, valued at USD 1.2 Billion.

Product Analysis

Sensors dominate with 22.3% due to their critical role in continuous hazard monitoring and process control across oil and gas and mining facilities.

In 2025, Sensors held a dominant market position in the Product segment of the Intrinsically Safe Equipment Market, with a 22.3% share. These devices detect and measure physical parameters such as temperature, pressure, and gas concentration in hazardous areas. Moreover, their widespread deployment in continuous process monitoring applications makes them indispensable across oil and gas, chemical, and mining facilities.

Detectors are a critical product category used for identifying the presence of flammable gases, combustible dust, and toxic substances in hazardous environments. These devices provide early warning capabilities that protect both personnel and assets from explosion and fire risks. Additionally, tightening workplace safety regulations are driving consistent demand for certified gas and flame detectors across industrial facilities globally.

Switches are widely deployed in hazardous zone applications for control and automation functions. They are designed to operate safely in environments where standard electrical switching components would pose an ignition risk. Consequently, certified intrinsically safe switches are a standard specification in control panels and field instrumentation systems used across oil and gas and petrochemical facilities.

Transmitters convert process measurements into standardized signals for transmission to control systems in hazardous industrial environments. They are essential components in process automation and remote monitoring applications. Furthermore, the growing adoption of digital field instrumentation and smart transmitters is expanding the addressable market for intrinsically safe transmitter products across major industries.

Isolators

Isolators are widely used in hazardous area electrical systems to provide galvanic separation between safe and potentially explosive environments. They help protect control systems by preventing excess current or voltage from reaching sensitive equipment. The increasing adoption of automated industrial systems is driving higher demand for reliable isolator solutions.LED Indicators

LED indicators are essential components used for visual signaling and operational status monitoring in hazardous industrial environments. These devices provide clear and energy-efficient indication of system conditions, alarms, or equipment status. Their durability and low power consumption make them suitable for continuous operation in demanding hazardous locations.Others

Other supporting intrinsically safe components include switches, barriers, sensors, and communication modules used across various hazardous area installations. These products enhance system functionality and ensure safe equipment operation in explosive atmospheres. As industrial automation and monitoring systems become more interconnected, demand for such complementary safety components continues to increase.Zone Analysis

Zone 1 dominates with 25.9% due to its prevalence in oil and gas facilities where flammable atmospheres are intermittently present during normal operations.

In 2025, Zone 1 held a dominant market position in the Zone segment of the Intrinsically Safe Equipment Market, with a 25.9% share. Zone 1 refers to areas where a flammable atmosphere is likely to occur during normal operations. Moreover, the high concentration of Zone 1 classified areas in oil and gas refineries and chemical plants drives consistent demand for certified equipment in this category.

Zone 0 represents the most hazardous classification, covering areas where flammable gas or vapor is continuously present. Equipment certified for Zone 0 must meet the most stringent safety standards and engineering requirements. Consequently, the specialized nature of Zone 0 applications commands premium pricing and requires highly engineered intrinsically safe solutions from certified manufacturers.

Zone 20 refers to areas where combustible dust is present continuously or for long periods during normal operations. These environments are commonly found in industries such as grain processing, food production, and pharmaceutical manufacturing where fine dust particles accumulate. Due to the constant presence of explosive dust atmospheres, highly certified intrinsically safe equipment is essential to ensure operational safety and regulatory compliance.

Zone 21 includes areas where combustible dust is likely to occur occasionally during normal industrial activities. This classification is typical in facilities like coal processing plants, chemical factories, and powder-handling units. Increasing awareness of dust explosion hazards is encouraging industries to adopt reliable intrinsically safe equipment designed to operate safely in such intermittent dust environments.

Zone 2 represents locations where flammable gases or vapors are not normally present but may occur under abnormal conditions such as leaks or equipment failures. These environments are commonly found in oil and gas facilities, refineries, and chemical processing plants. Intrinsically safe equipment in these areas helps reduce ignition risks while supporting safe and efficient industrial operations.

Zone 22 applies to areas where combustible dust is not normally present but may appear for short periods due to accidental releases or process disturbances. Such environments exist in industries including food processing, pharmaceuticals, and metal manufacturing. The demand for cost-effective intrinsically safe equipment in Zone 22 is rising as companies focus on maintaining safety while optimizing operational efficiency.

Class Analysis

Class 1 dominates with 65.9% due to its application in environments containing flammable gases and vapors, which are the most common hazard type across major end-use industries.

In 2025, Class 1 held a dominant market position in the Class segment of the Intrinsically Safe Equipment Market, with a 65.9% share. Class 1 covers locations where flammable gases or vapors may be present in sufficient quantities to produce explosive mixtures. Moreover, its prevalence across oil and gas, chemical, and petrochemical facilities makes it the single largest demand driver in the Class segmentation.

Class 2 designates hazardous locations where combustible dust may be present in sufficient quantities to ignite. This classification is applicable in industries such as grain handling, coal processing, and pharmaceutical manufacturing. Consequently, tightening workplace safety regulations governing dust explosion risks are driving steady demand for Class 2 certified intrinsically safe equipment in these specialized sectors.

Class 3 covers locations where ignitable fibers or flyings are present but are not likely to be suspended in air in quantities sufficient to produce explosive mixtures. This classification applies primarily to textile manufacturing and woodworking facilities. Additionally, growing safety compliance requirements in these sectors are contributing to gradual expansion in the addressable market for Class 3 certified intrinsically safe products.

End Use Industry Analysis

Oil and Gas dominates with 35.6% due to extensive hazardous zone operations and strict mandatory compliance requirements for certified explosion-proof and intrinsically safe equipment.

In 2025, Oil and Gas held a dominant market position in the End Use Industry segment of the Intrinsically Safe Equipment Market, with a 35.6% share. This sector operates extensively in classified hazardous areas including upstream exploration, midstreA. Consequently, mining operators are major consumers of certified sensors, lighting, communication devices, and control systems that comply with hazardous area standards.

Power generation facilities often operate in environments where flammable gases, vapors, or combustible materials may be present. Intrinsically safe equipment helps prevent ignition risks while ensuring safe monitoring and control of critical power systems. Growing investments in thermal, nuclear, and renewable power infrastructure are supporting steady demand for certified safety equipment.

Chemical and petrochemical plants handle highly volatile substances that create potentially explosive atmospheres. Intrinsically safe devices are essential for maintaining safe communication, monitoring, and automation within hazardous processing areas. Strict regulatory standards and the expansion of chemical manufacturing capacity are further increasing the adoption of these safety solutions.

Industrial processing facilities such as food, pharmaceutical, and metal processing plants frequently generate combustible dust and hazardous vapors. Intrinsically safe equipment plays a crucial role in ensuring safe production and preventing explosion risks in these environments. Increasing automation and modernization of processing plants are contributing to the rising demand for certified safety technologies.

Other industries including mining, wastewater treatment, and transportation also require intrinsically safe equipment in hazardous operational environments. These sectors often deal with flammable gases, dust, or volatile chemicals during routine activities. As safety awareness and compliance requirements increase, adoption of intrinsically safe solutions across these additional sectors continues to expand.

Key Market Segments

By Product

- Sensors

- Detectors

- Switches

- Transmitters

- Isolators

- LED Indicators

- Others

By Zone

- Zone 0

- Zone 1

- Zone 2

- Zone 20

- Zone 21

- Zone 22

By Class

- Class 1

- Class 2

- Class 3

By End Use Industry

- Oil and Gas

- Mining

- Power

- Chemical and Petrochemical

- Processing

- Others

Drivers

Stringent Industrial Safety Regulations and Expanding Hazardous Area Operations Drive Intrinsically Safe Equipment Demand

Mandatory compliance with industrial safety standards such as ATEX, IECEx, and NEC is a primary driver of intrinsically safe equipment demand. Governments and regulatory bodies across major markets require certified equipment in all classified hazardous zones. Consequently, industries operating in explosive or flammable environments must continuously invest in compliant devices to avoid legal penalties and protect worker safety.

Rapid expansion of oil and gas production, mining operations, and chemical processing in emerging economies is generating significant new demand. Countries across Asia Pacific, the Middle East, and Africa are scaling up energy and industrial infrastructure investments. Therefore, the volume of hazardous area installations requiring certified intrinsically safe sensors, detectors, transmitters, and communication equipment is growing substantially in these high-growth regions.

Growing adoption of industrial automation and process control technologies in hazardous environments is a further key driver. Facilities are deploying increasingly sophisticated intrinsically safe instrumentation to improve process efficiency and operational reliability. Moreover, rising demand for real-time monitoring and predictive maintenance capabilities is expanding the specification of advanced certified sensors and smart transmitters across oil and gas and mining applications globally.

Restraints

High Certification Costs and Technical Complexity Limit Broader Adoption of Intrinsically Safe Equipment

The high cost of certifying intrinsically safe equipment to international standards such as ATEX and IECEx is a significant market restraint. Manufacturers must invest heavily in testing, documentation, and regulatory approval processes for each product and hazard zone classification. Consequently, certification costs increase product prices substantially, making advanced intrinsically safe solutions less accessible for budget-constrained operators in developing markets.

Technical complexity in designing and installing intrinsically safe systems presents a further barrier to adoption. The strict energy limitation requirements, which cap power at less than 1.3W and voltage below 29V DC, impose design constraints that limit device functionality. Therefore, engineers and system integrators require specialized training and expertise to design compliant intrinsically safe circuits and installations correctly.

Limited product interoperability between different certified equipment brands and standards can create compatibility challenges for end users. Facilities operating with mixed equipment inventories may face difficulties integrating certified devices from different manufacturers into unified control architectures. Moreover, the need to maintain strict separation between intrinsically safe and non-intrinsically safe circuits adds complexity and cost to installation and maintenance activities across hazardous area facilities.

Growth Factors

Industrial IoT Integration and Emerging Market Infrastructure Growth Accelerate Market Expansion

The integration of Industrial IoT capabilities into intrinsically safe equipment is a major growth driver. Cloud-enabled monitoring, wireless connectivity, and remote diagnostics are being incorporated into certified hazardous area devices. Moreover, these smart capabilities allow operators to achieve real-time visibility into field equipment performance, enabling predictive maintenance and reducing unplanned downtime across oil and gas and mining operations.

Growing investment in energy infrastructure across emerging economies is creating strong new demand for hazardous area equipment. Countries in Asia Pacific, the Middle East, and Africa are expanding oil, gas, and chemical processing capacity at a rapid pace. Consequently, demand for certified intrinsically safe instrumentation, communication devices, and control systems is growing consistently in tandem with new facility construction and expansion projects.

Rising focus on worker safety and the growing adoption of digital workplace safety management systems are supporting market growth. Industrial operators are investing in more comprehensive hazardous area monitoring capabilities to reduce accident risk and liability. Additionally, the development of lightweight and ruggedized intrinsically safe mobile devices and wearables is creating new application opportunities across a broader range of hazardous area industries and job functions.

Emerging Trends

Wireless Connectivity and Smart Diagnostics Reshape the Intrinsically Safe Equipment Market

The growing adoption of wireless intrinsically safe communication devices is transforming operations in hazardous industrial environments. Certified smartphones, tablets, and handheld computers now allow field workers to access real-time data and conduct inspections without leaving hazardous zones. Moreover, partnerships between safety equipment manufacturers and consumer technology companies are accelerating the development of next-generation intrinsically safe mobile solutions for industrial use.

Cloud-enabled monitoring and remote diagnostics capabilities are emerging as a significant value-added trend in intrinsically safe equipment. Manufacturers are increasingly embedding connectivity features that allow equipment health data to be transmitted to centralized monitoring platforms. Consequently, operators in oil and gas facilities can identify potential equipment failures early and schedule maintenance proactively, reducing operational risk and improving asset reliability.

The development of miniaturized and multi-function intrinsically safe sensors and transmitters is a notable trend reshaping product design. Advances in low-power electronics are enabling greater functionality within the strict energy limits required for intrinsic safety certification. Additionally, growing demand for integrated gas detection, temperature sensing, and communication capabilities in a single certified device is driving innovation across the intrinsically safe equipment product landscape.

Regional Analysis

North America Dominates the Intrinsically Safe Equipment Market with a Market Share of 32.1%, Valued at USD 1.2 Billion

North America holds the leading position in the global intrinsically safe equipment market, accounting for a share of 32.1% and valued at USD 1.2 Billion. The United States drives regional demand, supported by a large and mature oil and gas industry, extensive chemical processing infrastructure, and strict NEC and OSHA compliance requirements. Moreover, ongoing investment in energy infrastructure modernization and the expansion of LNG facilities is sustaining healthy demand for certified hazardous area equipment.

Europe Intrinsically Safe Equipment Market Trends

Europe is a key market driven by the ATEX directive and IECEx certification framework, which mandate certified equipment across all hazardous area industries. Germany, the UK, and the Netherlands are the leading markets, supported by active oil and gas, chemical, and pharmaceutical sectors. Furthermore, the region’s strong emphasis on worker safety compliance and the adoption of advanced industrial automation technologies continue to support premium equipment demand.

Asia Pacific Intrinsically Safe Equipment Market Trends

Asia Pacific is the fastest-growing regional market, driven by rapid expansion of oil and gas, mining, and chemical processing industries across China, India, and Southeast Asia. Growing government investment in energy infrastructure and increasing regulatory adoption of international hazardous area standards are expanding the certified equipment market. Consequently, the region represents the most significant long-term growth opportunity for intrinsically safe equipment manufacturers globally.

Middle East and Africa Intrinsically Safe Equipment Market Trends

The Middle East and Africa region presents strong growth potential, underpinned by large-scale oil and gas production operations across the GCC. Saudi Arabia, the UAE, and Qatar are major consumers of certified hazardous area instrumentation and communication equipment. Moreover, ongoing upstream and downstream energy investment programs across the region are driving sustained demand for intrinsically safe sensors, detectors, and process control devices.

Latin America Intrinsically Safe Equipment Market Trends

Latin America represents a growing market for intrinsically safe equipment, led by Brazil and Mexico, where oil and gas and mining sectors are active. Regional demand is supported by expanding energy production and increasing regulatory awareness of hazardous area safety requirements. However, economic volatility and infrastructure funding constraints can create uneven growth conditions across different countries within the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Pepperl+Fuchs Inc. is a globally recognized leader in hazardous area electrical equipment and intrinsic safety technology. The company offers one of the broadest portfolios of certified sensors, isolators, and field devices for explosive atmospheres. Moreover, its ongoing investment in digital connectivity and smart field device technologies positions it strongly to capture growing demand from industrial IoT-driven hazardous area applications worldwide.

Fluke Corporation is a leading manufacturer of electronic test and measurement tools, with a dedicated range of products certified for use in hazardous environments. The company’s intrinsically safe meters and diagnostic instruments are widely used by maintenance professionals in oil and gas, chemical, and utility sectors. Additionally, Fluke’s strong brand reputation and extensive global distribution network support its continued growth in certified hazardous area markets.

Emerson Electric Co. provides a comprehensive range of intrinsically safe process instrumentation and automation solutions for hazardous industrial environments. Its certified transmitters, sensors, and control systems are widely deployed across oil and gas, chemical, and power generation facilities globally. Consequently, Emerson’s deep application expertise and integrated automation portfolio make it a preferred supplier for large-scale hazardous area instrumentation projects in mature and emerging markets.

Siemens AG is a major global supplier of certified hazardous area automation and instrumentation products, serving industries including oil and gas, mining, and chemical processing. The company’s intrinsically safe product range includes sensors, switches, and process control devices designed for Zone and Class classified environments. Furthermore, Siemens leverages its global manufacturing scale and digital industry expertise to deliver integrated certified solutions for complex hazardous area applications.

Key Players

- Pepperl+Fuchs Inc.

- Fluke Corporation

- Emerson Electric Co.

- Siemens AG

- ABB

- Extronics

- Banner Engineering Corp.

- Bayco Products Inc.

- CorDEX Instruments

- Eaton Corporation PLC

- G.M. International s.r.l.

- Georgin

- Honeywell International Inc.

- OMEGA Engineering Inc.

- R. Stahl AG

- Rockwell Automation Inc.

- Schneider Electric SE

- Other Key Players

Recent Developments

- January 2025 – A leading intrinsically safe equipment manufacturer completed a strategic acquisition to strengthen its hazardous-area communication device portfolio, expanding its certified product offering for use in explosive atmospheres. The move is expected to enhance the company’s competitive position in the growing industrial communication segment of the hazardous area equipment market.

- May 2025 – Pepperl+Fuchs SE partnered with Samsung Electronics to develop intrinsically safe mobile devices designed for use in hazardous industrial environments, combining Samsung’s advanced smartphone technology with Pepperl+Fuchs’s certification expertise. The collaboration aims to deliver next-generation certified handheld solutions for field workers operating in oil and gas and chemical processing facilities.

- January 2026 – Manufacturers increased investment in cloud-enabled monitoring and remote diagnostics capabilities for intrinsically safe equipment deployed in oil and gas facilities, responding to growing operator demand for real-time asset health visibility. This trend is accelerating the integration of Industrial IoT features into certified hazardous area devices across the global market.

Report Scope

Report Features Description Market Value (2025) USD 3.9 Billion Forecast Revenue (2035) USD 7.4 Billion CAGR (2026-2035) 6.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Product (Sensors, Detectors, Switches, Transmitters, Isolators, LED Indicators, Others), Zone (Zone 0, Zone 1, Zone 2, Zone 20, Zone 21, Zone 22), Class (Class 1, Class 2, Class 3), End Use Industry (Oil and Gas, Mining, Power, Chemical and Petrochemical, Processing, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Pepperl+Fuchs Inc., Fluke Corporation, Emerson Electric Co., Siemens AG, ABB, Extronics, Banner Engineering Corp., Bayco Products Inc., CorDEX Instruments, Eaton Corporation PLC, G.M. International s.r.l., Georgin, Honeywell International Inc., OMEGA Engineering Inc., R. Stahl AG, Rockwell Automation Inc., Schneider Electric SE, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Intrinsically Safe Equipment MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Intrinsically Safe Equipment MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Pepperl+Fuchs Inc.

- Fluke Corporation

- Emerson Electric Co.

- Siemens AG

- ABB

- Extronics

- Banner Engineering Corp.

- Bayco Products Inc.

- CorDEX Instruments

- Eaton Corporation PLC

- G.M. International s.r.l.

- Georgin

- Honeywell International Inc.

- OMEGA Engineering Inc.

- R. Stahl AG

- Rockwell Automation Inc.

- Schneider Electric SE

- Other Key Players

Our Clients

- 180591

- Mar 2026