Global Gelcoat Market Size, Share and Report Analysis By Raw Material (Polyester Resin, Vinyl Ester Resin, Epoxy Resin, Others), By Application (Spray-up, Brush And Roller), By End Use (Marine, Transportation, Construction, Wind And Energy, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 178712

- Number of Pages: 389

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

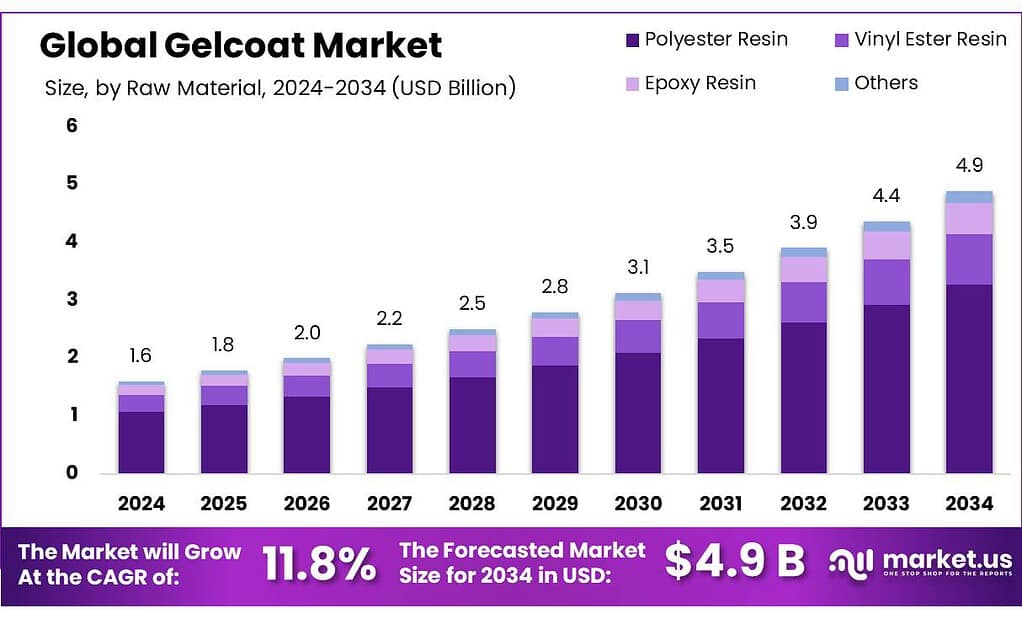

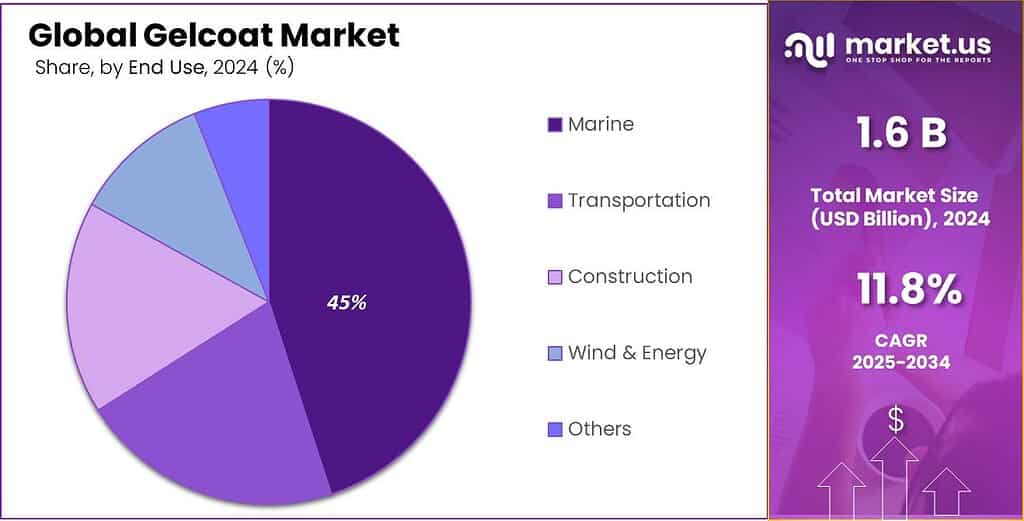

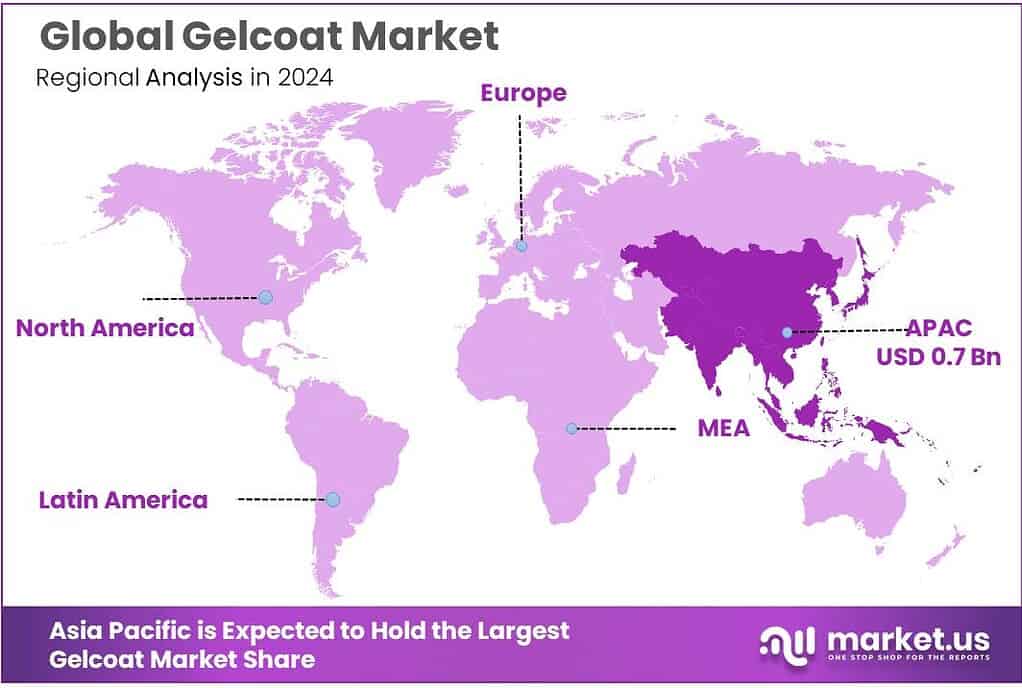

Global Gelcoat Market size is expected to be worth around USD 4.9 Billion by 2034, from USD 1.6 Billion in 2024, growing at a CAGR of 11.8% during the forecast period from 2025 to 2034. In 2024 Asia Pacific held a dominant market position, capturing more than a 48.6% share, holding USD 0.7 Billion in revenue.

Gelcoat is a specialized polymer coating applied as the outermost layer of fibre-reinforced plastic (FRP) parts, providing a smooth, glossy surface with strong resistance to UV radiation, water, chemicals and abrasion. In marine, construction, wind energy and hygienic panel applications, it effectively replaces paint: the gel layer is sprayed or brushed into the mould first and becomes the visible, protective skin of the composite structure.

Industrial demand for gelcoat tracks closely with the broader composites and infrastructure economy. In Europe, the construction of buildings sector alone generated about €177.9 billion of value added in 2022 and employed almost 3.5 million people, underlining the scale of façades, sanitary units and moulded components where gelcoat-finished FRP can compete with metals and concrete.

The EU construction sector as a whole still accounts for more than 5% of gross value added, confirming it as a durable demand base for high-performance coatings. Marine markets add another important pillar: the European boatbuilding sector alone comprises around 3,600 companies and more than 82,000 jobs, where FRP hulls commonly rely on gelcoat as their weather- and salt-water-resistant outer layer.

- According to the International Energy Agency, global annual renewable power capacity additions jumped by almost 50% in 2023 to nearly 510 gigawatts, the fastest growth rate in two decades, with China, Europe, the United States and Brazil all setting new records. Wind energy is a particularly important end use because gelcoats are specified for blade and nacelle housings; total installed wind capacity reached about 1,015 gigawatts in 2023, with 93% onshore and 7% offshore.

Global industry bodies report that new wind installations were roughly 116–117 gigawatts per year in 2023 and 2024, but still below the approximately 320 gigawatts per year required to achieve the United Nations’ renewable-tripling target, indicating significant headroom for further build-out and associated gelcoat demand.

Government initiatives and industrial policy further reinforce the market outlook. The International Renewable Energy Agency (IRENA) projects that, under a 1.5 °C pathway, average annual renewable power capacity additions need to reach about 1,066 GW per year between 2023 and 2050, a scenario that implies continued large-scale deployment of composite-intensive wind and solar hardware protected by gelcoat systems.

Government initiatives and public funding further reinforce these drivers. International Energy Agency (IEA) and the Global Wind Energy Council project that India alone has over 20 GW of wind turbine manufacturing capacity and targets 500 GW of non-fossil fuel power by 2030, including 100 GW from wind.

Key Takeaways

- Gelcoat Market size is expected to be worth around USD 4.9 Billion by 2034, from USD 1.6 Billion in 2024, growing at a CAGR of 11.8%.

- Polyester Resin held a dominant market position, capturing more than a 67.2% share.

- Spray-up held a dominant market position, capturing more than a 78.3% share.

- Marine held a dominant market position, capturing more than a 45.7% share.

- Asia Pacific region, holding a dominant 48.6% market share valued at around USD 0.7 billion.

By Raw Material Analysis

Polyester Resin leads the gelcoat space with a strong 67.2% share in 2024

In 2024, Polyester Resin held a dominant market position, capturing more than a 67.2% share, reflecting its long-standing role as the most widely used raw material in gelcoat production. Its dominance comes from a mix of practicality, affordability, and consistent performance across marine, construction, sanitary ware, and transportation products. Manufacturers continue to prefer polyester-based gelcoats because they cure quickly, offer good UV stability, and bond well with glass-reinforced composites, which keeps demand steady even when end-use markets face fluctuations. As industries seek reliable and cost-effective composite solutions, polyester resin remains the default choice in most mid-range and high-volume applications.

By Application Analysis

Spray-up dominates with a strong 78.3% share driven by fast and flexible application

In 2024, Spray-up held a dominant market position, capturing more than a 78.3% share, making it the most preferred method for applying gelcoat across marine, construction, sanitary ware, and transportation components. Its popularity comes from its simple process, quick application time, and ability to cover complex molds evenly. Fabricators rely on spray-up because it allows them to achieve a smooth, glossy, and durable finish without adding major labor or equipment costs. As demand for FRP products continued to rise in 2024—especially in water tanks, boat hulls, and architectural panels—manufacturers leaned toward spray-up as the most practical and time-saving application technique.

By End Use Analysis

Marine sector leads with 45.7% share as durability needs rise

In 2024, Marine held a dominant market position, capturing more than a 45.7% share, reflecting the long-standing dependence of boat builders and marine infrastructure developers on high-quality gelcoat finishes. The sector relies heavily on gelcoat because it provides a smooth, glossy, and highly weather-resistant surface capable of withstanding saltwater, UV exposure, and constant abrasion. Boat hulls, decks, jet skis, and repair applications all depend on gelcoat to maintain structural integrity and appearance. Throughout 2024, rising coastal tourism, increased small-craft manufacturing, and refurbishment of older vessels contributed to strong demand within the marine segment, keeping it the leading end-use category.

Key Market Segments

By Raw Material

- Polyester Resin

- Vinyl Ester Resin

- Epoxy Resin

- Others

By Application

- Spray-up

- Brush & Roller

By End Use

- Marine

- Transportation

- Construction

- Wind & Energy

- Others

Emerging Trends

Hygienic, easy-to-clean gelcoat surfaces are emerging as a quiet but important trend

One of the most interesting latest trends in the gelcoat space is its growing use as a hygienic, easy-to-clean surface in fish and food infrastructure, not just in boats. As countries invest in modern harbours, fish markets, cold rooms and processing halls, project designers are moving away from bare concrete and rust-prone steel toward fibre-reinforced plastic (FRP) panels, tanks and flooring finished with gelcoat. These surfaces are smoother, resist stains and moisture, and can handle frequent washing and disinfecting. For workers who stand all day in wet, slippery conditions, a tough gelcoat surface is not a luxury; it is simply something that makes the workday safer and easier to manage.

The food numbers behind this shift are huge. The Food and Agriculture Organization (FAO) reports that global fisheries and aquaculture production reached 223.2 million tonnes in 2022, a 4.4% increase compared with 2020, with 185.4 million tonnes of aquatic animals and 37.8 million tonnes of algae. When so much fish is moving through landing centres, auction halls and processing plants every day, surface quality really matters. Floors, walls and tanks that are rough or corroded are harder to clean and more likely to harbour bacteria and odour.

At the same time, the world is trying to cut food loss and waste, especially in fish. FAO estimates that around 35% of the global fisheries and aquaculture harvest is either lost or wasted every year. A good part of this loss happens because cold rooms fail, ice is not available, or handling areas are not clean enough. That is why governments and funding agencies are putting serious money into infrastructure. In India, the Pradhan Mantri Matsya Sampada Yojana (PMMSY) was launched in 2020 with an overall investment target of INR 20,050 crore up to 2024-25 to close gaps in cold chain, landing centres and market infrastructure.

Food-processing policy is moving in the same direction. India’s Pradhan Mantri Kisan Sampada Yojana (PMKSY), which supports food processing and value-addition, has received a total outlay of INR 6,520 crore for the 2021–2026 period, including an additional INR 1,920 crore recently approved to expand the scheme. New processing units created under such schemes often look for materials that are both food-safe and low-maintenance.

Drivers

Growing marine and aquaculture activity is driving gelcoat demand

One major driving factor for the gelcoat market is the rapid growth of marine and aquaculture activity as the world looks for more protein from the sea. Modern fishing vessels, workboats, aquaculture cages, storage tanks and processing equipment increasingly use fibre-reinforced plastics (FRP), and gelcoat is the outer skin that protects these structures from saltwater, sunlight and constant wear. As coastal economies scale up their fisheries and farmed fish production, they quietly pull more gelcoat into the value chain, even though buyers mainly see it as part of a boat hull, tank or panel rather than a separate product.

Global numbers from leading food bodies show how strong this pull has become. The Food and Agriculture Organization (FAO) reports that total fisheries and aquaculture production reached a record 223.2 million tonnes in 2022, up 4.4% compared with 2020. Within this, aquaculture alone produced 130.9 million tonnes, surpassing capture fisheries for the first time and accounting for just over half of aquatic animal output. Such growth means more fish farms, more service vessels, more landing centres and more cold-chain facilities, all of which favour corrosion-resistant composite structures finished with gelcoat rather than bare metal that rusts quickly in marine conditions.

Consumption trends tell a similar story. FAO data show that apparent per-capita consumption of aquatic foods has risen from about 9.1 kg per person in 1961 to around 20–20.7 kg in 2020–2022, more than doubling in sixty years as diets diversify and incomes rise. The OECD-FAO Agricultural Outlook projects that apparent food fish consumption will climb further to about 21.2 kg per capita by 2032, up from 20.4 kg in the 2020–2022 base period.

Governments are backing this expansion with targeted funding, which indirectly supports the gelcoat ecosystem. In India, the Fisheries and Aquaculture Infrastructure Development Fund (FIDF) was created with an outlay of ₹7,522.48 crore to support harbours, landing centres, cold stores, ice plants, fish transport, hatcheries and other facilities, and has been extended for three years from 2023-24 to 2025-26. In parallel, a new sub-scheme under the Pradhan Mantri Matsya Sampada Yojana (PMMSY) carries a targeted investment of ₹6,000 crore to strengthen value chains for fishers, vendors and small enterprises.

Restraints

Rising regulatory pressure on hazardous emissions is slowing gelcoat expansion

One major restraining factor for the gelcoat market is the growing regulatory pressure around hazardous emissions—especially volatile organic compounds (VOCs) and styrene—which are central concerns for many global food-sector bodies and environmental agencies. Gelcoat, especially polyester-based formulations, contains styrene, a compound now monitored closely due to its health and environmental implications. As rules tighten, many small and mid-size manufacturers face higher compliance costs, slower approvals, and pressure to shift to alternative chemistries that are more expensive and technically challenging.

The shift is driven in part by the global food sector’s push toward safer production and cleaner environments. The Food and Agriculture Organization (FAO) notes that the food and aquaculture value chain now involves 223.2 million tonnes of production in 2022, up 4.4% compared with 2020, which means more vessels, tanks, and processing structures are being built. But alongside this expansion, global food systems are also being pushed to operate under stricter environmental norms.

- This creates a complex situation. On one side, aquaculture is growing. On the other, regulations are tightening around materials used in these facilities—many of which rely heavily on gelcoat. The Organisation for Economic Co-operation and Development and FAO jointly state in their Agricultural Outlook that global fish consumption is expected to reach 21.2 kg per capita by 2032, up from 20.4 kg in 2020–2022.

Regulatory bodies worldwide are responding. In India, environmental compliance guidelines applied near coastal and freshwater food facilities fall under the Central Pollution Control Board, which has strengthened emissions norms for industries operating adjacent to aquaculture zones. Similarly, the World Bank has expanded its Blue Economy programmes, with over US$10.5 billion committed to sustainable oceans and fisheries projects as of FY24. These projects emphasize low-impact infrastructure and cleaner materials, putting indirect pressure on traditional gelcoat use in fishing vessels, cold storage units, and hatchery systems.

Opportunity

Expanding blue economy and food infrastructure is opening a fresh growth lane for gelcoat

One major growth opportunity for the gelcoat market comes from the quiet but powerful build-out of the “blue economy” and food-related marine infrastructure. Around the world, governments and development banks are investing heavily in ports, fishing harbours, aquaculture farms, cold-chain facilities and small workboats that support the fish on people’s plates. Most of these assets now use composite structures that need a tough, UV- and salt-resistant outer skin, and that is exactly where gelcoat fits in. Instead of being seen only as a finishing layer for boats, gelcoat is gradually becoming a standard surface in many parts of the food value chain that touch the sea.

The scale of seafood and farmed fish production explains why this opportunity is not a short-term trend. The Food and Agriculture Organization reports that global fisheries and aquaculture output reached 223.2 million tonnes in 2022, about 4.4% higher than in 2020, with 185.4 million tonnes coming from aquatic animals and 37.8 million tonnes from algae. That is a huge volume of food that depends on fishing vessels, farm cages, landing centres and processing halls.

Demand for aquatic food is set to keep rising. The joint Organisation for Economic Co-operation and Development–FAO Agricultural Outlook projects that apparent food fish consumption will reach about 21.2 kg per person by 2032, up from 20.4 kg per person in the 2020–2022 average. Public investment is turning this structural need into a pipeline of real projects.

India’s Fisheries and Aquaculture Infrastructure Development Fund (FIDF) has an approved size of ₹7,522.48 crore, with budgetary support of ₹939.48 crore, and has been formally extended for three years from 2023-24 to 2025-26. At the global level, the World Bank notes that its blue economy portfolio has risen to more than US$10.5 billion in active projects by FY24, covering sustainable fisheries, aquaculture and coastal infrastructure.

Regional Insights

Asia Pacific – the dominant gelcoat market with 48.6% share and USD 0.7 Bn value

The Asia Pacific region, holding a dominant 48.6% market share valued at around USD 0.7 billion, remains the strongest hub for gelcoat consumption due to its massive composite manufacturing base, booming marine activity, and expanding construction and transportation sectors. Countries such as China, India, Japan, and South Korea collectively drive the region’s dominance with their rapidly scaling industrial output and strong demand for fibre-reinforced plastic (FRP) products.

Supporting statistics highlight why Asia Pacific continues to lead the gelcoat market. The Food and Agriculture Organization (FAO) reports that Asia contributes nearly 70% of global aquaculture production, reaching over 130.9 million tonnes in 2022, demonstrating the region’s heavy reliance on FRP boats, storage systems, hatcheries, and tanks—equipment commonly finished with durable gelcoat surfaces.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

LyondellBasell operates in over 100 countries, with 55+ manufacturing sites and annual revenues of nearly USD 43.7 billion (2023). The company employs around 19,600 people and is one of the largest polyolefin and resin producers supporting gelcoat intermediates. Its R&D spending exceeds USD 350 million annually, enabling advanced composites and polymer technologies. The company’s production capacity of 40+ million tonnes per year in chemicals and polymers strengthens its supply contribution to gelcoat and composite-grade resin formulations.

Lanxess generates annual revenues of approximately EUR 6.7 billion (2023) and operates in 33 countries with 60+ production sites. The company employs nearly 12,900 people worldwide. Its high-performance additives and resin intermediates support gelcoat manufacturing, especially for corrosion-resistant composites. Lanxess allocates about EUR 250 million annually to innovation and sustainability programs. Its materials segment supplies chemical building blocks used in FRP and gelcoat systems, strengthening its role in automotive, marine, and construction composites markets.

Eastman Chemical Company reports revenues of USD 9.2 billion (2023) and employs around 14,500 people globally. Operating across 100+ countries, Eastman maintains 50+ manufacturing sites. Its polyester resins, solvents, and specialty additives are widely used in gelcoat and composite applications. Eastman invests over USD 250 million annually in R&D and sustainability projects. Its chemical intermediates contribute to marine, transportation, and architectural gelcoat formulations requiring improved weatherability, UV resistance, and long-term gloss retention.

Top Key Players Outlook

- LyondellBasell Industries Holdings B.V

- Interplastic Corporation

- Lanxess

- Eastman Chemical Company

- Polynt Reichold

- Owens Corning

- 3M

- Ashland Inc.

- Ineos

- Akzo Nobel N.V.

Recent Industry Developments

In 2024, LyondellBasell reported a net income of USD 1.4 billion and invested about USD 1.8 billion in business reinvestment, showing strong financial backing for its materials programmes.

In 2025, Eastman generated around USD 8.75 billion in sales revenue, slightly lower than the previous year but demonstrating resilience amid broad market pressures and continued demand for specialty products that support gelcoat formulations.

Report Scope

Report Features Description Market Value (2024) USD 1.6 Bn Forecast Revenue (2034) USD 4.9 Bn CAGR (2025-2034) 11.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Raw Material (Polyester Resin, Vinyl Ester Resin, Epoxy Resin, Others), By Application (Spray-up, Brush And Roller), By End Use (Marine, Transportation, Construction, Wind And Energy, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape LyondellBasell Industries Holdings B.V, Interplastic Corporation, Lanxess, Eastman Chemical Company, Polynt Reichold, Owens Corning, 3M, Ashland Inc., Ineos, Akzo Nobel N.V. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- LyondellBasell Industries Holdings B.V

- Interplastic Corporation

- Lanxess

- Eastman Chemical Company

- Polynt Reichold

- Owens Corning

- 3M

- Ashland Inc.

- Ineos

- Akzo Nobel N.V.

Our Clients

- 178712

- Feb 2026