Global Gear Lubricants Market Size, Share, And Enhanced Productivity By Type (Mineral Gear Lubricants, Synthetic Gear Lubricants, Semi-Synthetic Gear Lubricants), By Packaging Type (Drums, Pails, Cartons, Totes, Bulk), By Viscosity Grade (SAE 75W, SAE 80W, SAE 90, SAE 140, SAE 250), By Application (Automotive, Marine, Construction, Mining), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180195

- Number of Pages: 303

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

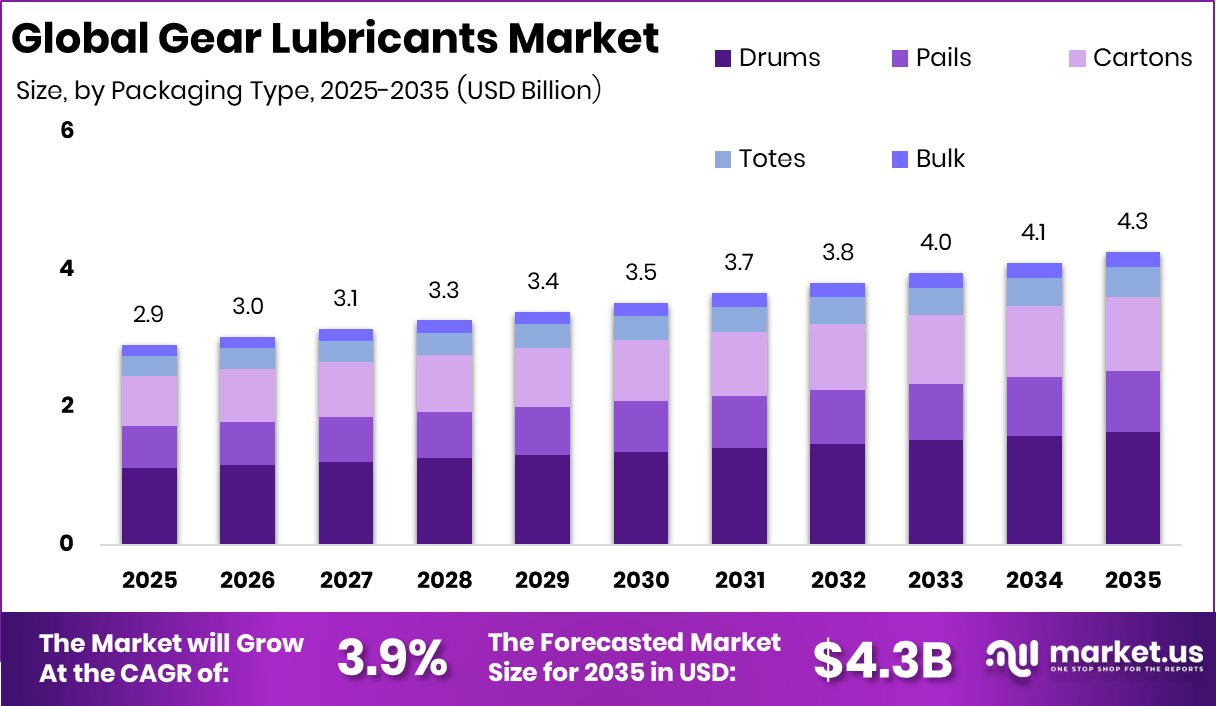

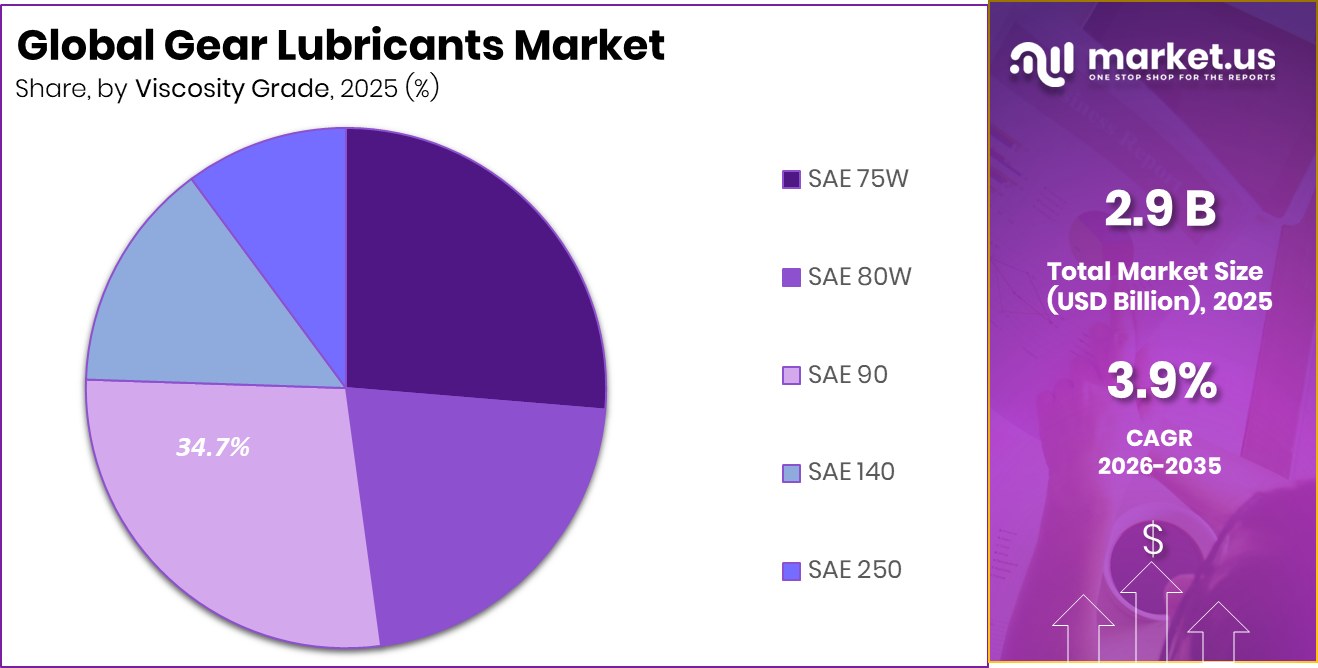

The Global Gear Lubricants Market is expected to be worth around USD 4.3 billion by 2035, up from USD 2.9 billion in 2025, and is projected to grow at a CAGR of 3.9% from 2026 to 2035. Strong automotive demand drives the North America Gear Lubricants Market, accounting for 46.3%, valued at USD 1.3 Bn.

Gear lubricants are specialized oils used to reduce friction and wear between moving gear components inside machines and vehicles. These lubricants form a protective film between gear surfaces, allowing smooth power transmission while preventing overheating and mechanical damage. Gear lubricants are widely used in automotive transmissions, industrial gearboxes, construction equipment, mining machinery, and marine propulsion systems, where heavy loads and high pressure are common.

The gear lubricants market refers to the global trade and consumption of these specialized oils used across transportation and industrial sectors. The market includes different product types such as mineral gear lubricants, synthetic gear lubricants, and semi-synthetic gear lubricants. Gear oils are supplied in several packaging formats, including drums, pails, cartons, totes, and bulk containers. They are also classified by viscosity grades such as SAE 75W, SAE 80W, SAE 90, SAE 140, and SAE 250, depending on operating conditions.

Market growth is supported by rising industrial equipment usage and expanding transportation infrastructure worldwide. Heavy machinery used in mining, construction, and manufacturing depends heavily on gear lubrication to maintain reliable performance. Increasing investment activity also reflects broader industrial expansion, highlighted by developments such as an innovative Houston-area hardtech startup closing a $5M seed round and the Texas Space Commission distributing $5.8 million to Houston companies for technology advancement.

Demand for gear lubricants continues to rise with growing vehicle fleets and industrial maintenance needs. Logistics operations, marine transport, and construction activities require consistent lubrication to ensure equipment durability. Economic and institutional spending, including reports such as LSSTF spending N1.77b on security within a year and record donations from major oil interests during Trump’s campaign, also reflect wider energy and infrastructure activities that indirectly support lubricant demand.

Future opportunities for the gear lubricants market lie in improving equipment efficiency and extending maintenance cycles. Industries are increasingly focused on reliable machinery performance, which creates steady demand for advanced lubrication solutions across automotive, mining, marine, and construction applications. As industrial development continues across multiple regions, the need for durable gear lubrication products is expected to remain strong.

Key Takeaways

- The Global Gear Lubricants Market is expected to be worth around USD 4.3 billion by 2035, up from USD 2.9 billion in 2025, and is projected to grow at a CAGR of 3.9% from 2026 to 2035.

- In the Gear Lubricants Market, mineral gear lubricants hold 49.6% share and are widely used across industrial and automotive machinery applications.

- In the Gear Lubricants Market, drum packaging accounts for 38.5% share, supporting bulk storage and transportation needs globally.

- In the Gear Lubricants Market, SAE 90 viscosity grade dominates with 34.7%, preferred for heavy-duty gearbox lubrication.

- In the Gear Lubricants Market, automotive applications represent a 43.9% share, driven by rising vehicle production and maintenance demand.

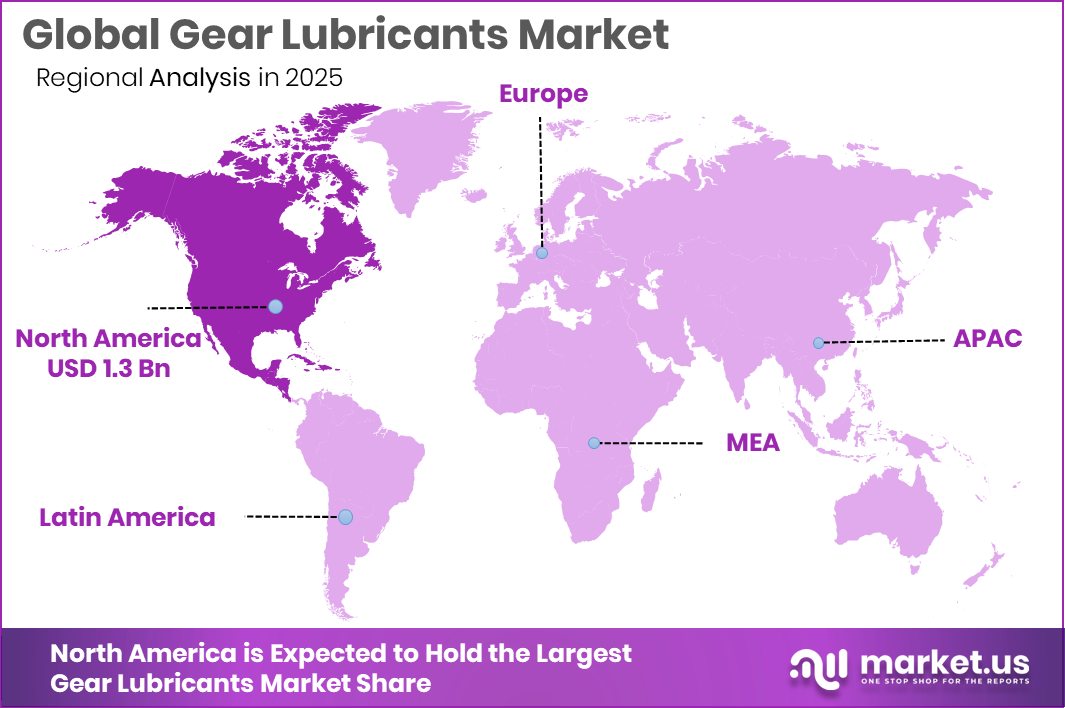

- The Gear Lubricants Market in North America recorded a 46.3% share, totaling USD 1.3 Bn value.

By Type Analysis

Mineral gear lubricants dominate the gear lubricants market with 49.6% global share.

In 2025, mineral gear lubricants held around 49.6% share of the global Gear Lubricants Market, reflecting their wide use across automotive and industrial applications. These lubricants remain popular because they provide reliable protection for gears operating under moderate loads and temperatures. Many vehicle manufacturers and fleet operators continue to rely on mineral-based formulations due to their cost efficiency and established performance in conventional gear systems.

In developing economies, where older vehicles and industrial equipment are common, mineral lubricants remain the preferred option. Market analysts also observe steady demand from manufacturing plants, mining equipment, and agricultural machinery that require dependable lubrication. As transportation activity and industrial output continue to expand globally, mineral gear lubricants are expected to maintain a strong presence within the overall gear lubricants market.

By Packaging Type Analysis

The drums packaging segment leads the gear lubricants market with 38.5% market share globally.

In 2025, drums accounted for about 38.5% of the Gear Lubricants Market by packaging type, making them the most widely used packaging format across industries. Drums are commonly preferred by automotive workshops, manufacturing units, mining companies, and heavy equipment operators that require large volumes of lubricants for routine operations. A typical drum packaging ensures convenient storage, easier transportation, and reduced packaging waste compared with smaller containers.

Bulk purchasing through drums also helps industrial buyers manage costs more effectively, especially for facilities that use lubricants continuously in gearboxes, transmissions, and industrial machinery. In regions with strong industrial and automotive service sectors, drums remain the standard supply format for lubricant distributors. As industrial maintenance activities increase worldwide, drum packaging is expected to continue playing a central role in the gear lubricants supply chain.

By Viscosity Grade Analysis

SAE 90 viscosity grade accounts for 34.7% Gear Lubricants Market demand.

In 2025, SAE 90 viscosity grade represented nearly 34.7% of the Gear Lubricants Market, largely due to its suitability for heavy-duty gear systems and traditional automotive transmissions. SAE 90 gear oil provides a thicker lubrication film, which helps protect gears operating under high-pressure and load conditions. It is widely used in manual transmissions, differentials, and commercial vehicle gearboxes where strong wear protection is required.

Many trucking fleets and off-road vehicle operators still rely on SAE 90 oils because they deliver stable performance even in demanding working environments. Industrial machinery with slower-moving gears also benefits from this viscosity grade, as it reduces friction and prolongs equipment life. As commercial transportation and heavy equipment usage continue to grow globally, SAE 90 gear lubricants are expected to remain an important segment of the market.

By Application Analysis

Automotive application dominates the Gear Lubricants Market, holding 43.9% share globally.

In 2025, the automotive sector accounted for about 43.9% of the Gear Lubricants Market by application, supported by the continuous expansion of passenger vehicles, commercial fleets, and off-road transportation. Gear lubricants are essential for maintaining smooth gear movement and reducing friction in transmissions, differentials, and axles. The rising number of vehicles on roads, especially in emerging economies, has increased the demand for regular maintenance and replacement of gear oils.

Automotive workshops, fleet operators, and service centers play a key role in sustaining lubricant consumption through routine servicing cycles. Additionally, growing logistics activities and long-distance transportation have increased the operating hours of trucks and commercial vehicles, further supporting lubricant demand. As global mobility and freight movement continue to rise, the automotive segment is expected to remain the dominant consumer of gear lubricants.

Key Market Segments

By Type

- Mineral Gear Lubricants

- Synthetic Gear Lubricants

- Semi-Synthetic Gear Lubricants

By Packaging Type

- Drums

- Pails

- Cartons

- Totes

- Bulk

By Viscosity Grade

- SAE 75W

- SAE 80W

- SAE 90

- SAE 140

- SAE 250

By Application

- Automotive

- Marine

- Construction

- Mining

Driving Factors

Rising automotive production increases gear lubricant demand

Rising automotive production increases gear lubricant demand. The global expansion of passenger vehicles, commercial fleets, and heavy transportation equipment continues to drive the need for reliable gear lubrication systems. Gear lubricants play a crucial role in protecting transmissions, axles, and differentials from wear, heat, and friction during continuous operation. As vehicle ownership grows across both developed and emerging economies, regular maintenance and servicing cycles are increasing lubricant consumption.

Automotive manufacturing facilities, logistics fleets, and service centers collectively contribute to stable demand for gear oils used in vehicle gear systems. At the same time, broader technology investment activity reflects the pace of industrial progress, illustrated by Hong Kong’s AI firm viAct raising $7.3M in Series A funding to expand across the MENA region and Europe, highlighting the growing connection between industrial technology development and equipment performance requirements.

Restraining Factors

Volatile crude oil prices affect lubricant costs

Volatile crude oil prices affect lubricant costs. Gear lubricants are commonly produced using base oils derived from petroleum, making their pricing sensitive to fluctuations in crude oil markets. When oil prices change significantly, lubricant manufacturers often face rising production costs and supply uncertainties. These fluctuations can influence pricing strategies and purchasing decisions among distributors, industrial users, and automotive service providers.

In some cases, sudden cost increases may delay procurement or encourage industries to optimize lubricant usage intervals. Market conditions in the energy and technology sectors often highlight similar financial volatility. For example, Hyperbots, a finance-focused agentic AI platform, recently secured $6.5 million in Series A funding, demonstrating how companies continue investing in financial efficiency tools as industries seek better ways to manage operational costs and supply chain fluctuations.

Growth Opportunity

Growing electric vehicles require specialized gear lubricants

Growing electric vehicles require specialized gear lubricants. As electric mobility expands globally, new drivetrain technologies are creating demand for lubricants designed specifically for electric gear systems. Electric vehicles use reduction gears and specialized transmission components that operate under unique thermal and mechanical conditions. This shift encourages lubricant manufacturers to develop products that support efficiency, durability, and quiet operation within electric drivetrains.

The gradual transition toward electrified transportation, therefore, creates opportunities for new gear oil formulations tailored for modern vehicle architectures. Alongside these developments, strong investment flows into transportation technology companies signal wider innovation momentum. For instance, Motive recently raised $150 million in funding, reflecting continued financial support for advanced fleet management and transportation technology platforms that contribute to the modernization of global vehicle operations.

Latest Trends

Rising adoption of synthetic gear lubricants

Rising adoption of synthetic gear lubricants. Industries are increasingly shifting toward synthetic formulations because they provide improved thermal stability, better wear protection, and longer service intervals compared with traditional mineral oils. Synthetic gear lubricants are particularly useful in high-load gear systems, commercial vehicles, and industrial equipment operating under demanding conditions. Their ability to maintain performance in extreme temperatures also supports equipment reliability across transportation, mining, and construction sectors.

As companies aim to reduce maintenance downtime and extend equipment lifespan, synthetic lubricant adoption continues to grow steadily across multiple industries. At the same time, investment momentum within transportation technology remains strong. Motive raised another $150 million in funding led by Kleiner ahead of a potential IPO, reflecting increasing confidence in technologies that support fleet efficiency, operational monitoring, and equipment performance improvements.

Regional Analysis

North America dominates Gear Lubricants Market with 46.3% share, reaching a USD 1.3 Bn value.

The Gear Lubricants Market shows varied growth patterns across major regions, including North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, reflecting differences in industrial activity, vehicle production, and maintenance demand. North America emerged as the dominating region, accounting for 46.3% of the global market share with a valuation of around USD 1.3 Bn. The strong presence of automotive manufacturing, large commercial vehicle fleets, and established industrial maintenance practices continues to support steady lubricant consumption across the United States and Canada.

Europe represents another important regional market, supported by its mature automotive sector and strong industrial machinery base, where gear lubricants are widely used in manufacturing equipment and transportation systems. Asia Pacific is witnessing steady demand driven by expanding vehicle ownership and growing industrial operations across developing economies.

Meanwhile, the Middle East & Africa region is gradually increasing its consumption of gear lubricants due to rising transportation activities and industrial infrastructure development. Latin America also contributes to the market through growing automotive servicing demand and expanding logistics operations, supporting consistent lubricant usage across the region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, ExxonMobil continues to hold a strong position in the global Gear Lubricants Market through its wide lubricant portfolio and global distribution network. The company supplies gear oils for automotive, industrial, and heavy-duty equipment applications under its well-known lubricant brands. ExxonMobil focuses on delivering products designed for high load performance, wear protection, and longer oil drain intervals, which are important for commercial vehicles and industrial machinery. The company’s extensive refining capacity and supply infrastructure allow it to serve large automotive manufacturers, industrial operators, and fleet maintenance providers across multiple regions. Its technical service teams also work closely with equipment manufacturers to ensure compatibility between gear lubricants and modern gearbox technologies.

Shell remains another major participant in the Gear Lubricants Market, supported by its global lubricants business and strong presence in automotive and industrial sectors. The company offers a wide range of gear oils developed for passenger vehicles, heavy-duty trucks, and industrial gear systems. Shell’s lubricant operations benefit from a broad manufacturing network and long-standing relationships with vehicle manufacturers and industrial equipment companies. The company also invests in lubricant technology development, focusing on improving efficiency, reducing equipment wear, and supporting longer service intervals.

Chevron also plays an important role in the Gear Lubricants Market, particularly in automotive and industrial lubrication solutions. The company supplies gear oils designed for durability, thermal stability, and equipment protection across demanding operating environments. Chevron’s lubricant products are widely used in commercial fleets, construction machinery, and industrial gear systems where reliability is critical. Its global supply network and technical support capabilities allow the company to maintain strong relationships with distributors, service providers, and industrial customers worldwide.

Top Key Players in the Market

- ExxonMobil

- Shell

- Chevron

- TotalEnergies

- BP

- Fuchs Petrolub AG

- Castrol

- Valvoline

- Kluber Lubrication

Recent Developments

- In October 2025, Shell plc launched Shell Spirax S4 GX 75W-90, a synthetic gear oil developed for passenger cars and light commercial vehicles. The product improves gearbox protection and smoother shifting, strengthening Shell’s lubricant portfolio for automotive gear systems.

- In April 2024, ExxonMobil introduced Mobilube GX 80W-90, a new gear oil designed for heavy-duty commercial vehicles. The lubricant improves wear protection and supports longer oil-drain intervals, helping fleet operators reduce maintenance needs and improve gearbox reliability in demanding transport operations.

Report Scope

Report Features Description Market Value (2025) USD 2.9 Billion Forecast Revenue (2035) USD 4.3 Billion CAGR (2026-2035) 3.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Mineral Gear Lubricants, Synthetic Gear Lubricants, Semi-Synthetic Gear Lubricants), By Packaging Type (Drums, Pails, Cartons, Totes, Bulk), By Viscosity Grade (SAE 75W, SAE 80W, SAE 90, SAE 140, SAE 250), By Application (Automotive, Marine, Construction, Mining) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ExxonMobil, Shell, Chevron, TotalEnergies, BP, Fuchs Petrolub AG, Castrol, Valvoline, Kluber Lubrication Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ExxonMobil

- Shell

- Chevron

- TotalEnergies

- BP

- Fuchs Petrolub AG

- Castrol

- Valvoline

- Kluber Lubrication

Our Clients

- 180195

- March 2026