Global Fans And Blowers Market Size, Share Analysis Report By Technology (Centrifugal, Axial), By Deployment (Power Generation, Oil and Gas, Construction, Iron and Steel, Chemicals, Mining, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 184161

- Number of Pages: 202

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

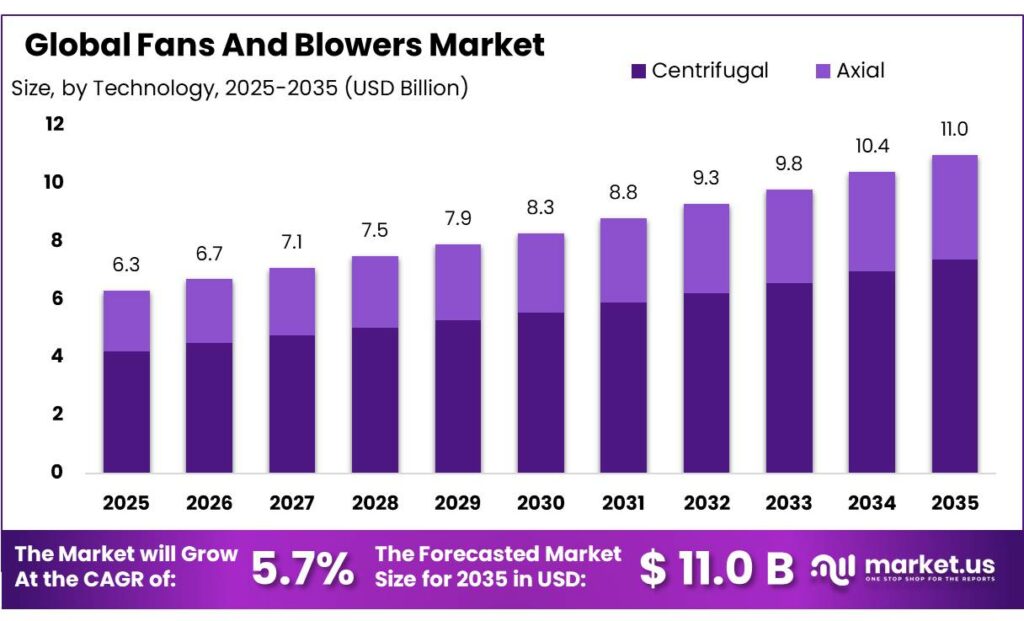

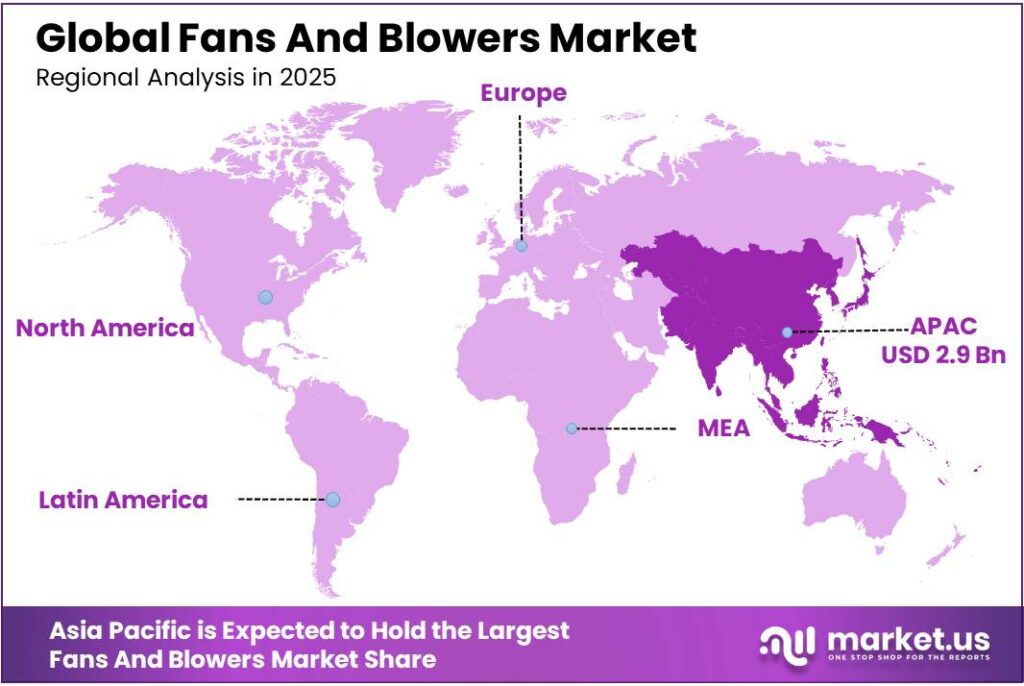

The Global Fans And Blowers Market size is expected to be worth around USD 11.0 Billion by 2035, from USD 6.3 Billion in 2025, growing at a CAGR of 5.7% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 47.5% share, holding USD 2.9 Billion revenue.

The fans and blowers industry remains a foundational part of industrial air movement, ventilation, combustion support, cooling, drying, pneumatic conveying, wastewater aeration, and food processing operations. Its strategic importance is rising because air-handling equipment now sits at the intersection of productivity, energy efficiency, emissions control, and process reliability.

In Europe alone, the European Commission states that nearly 4 billion fans are in use, and the regulated industrial-fan segment represents only about 5% of installed units yet accounts for 80% of total fan electricity consumption. The Commission also notes that about 214 million regulated industrial fans were operating in the EU27 in 2020, underscoring how a relatively narrow installed base drives a disproportionately large energy burden and therefore remains a prime target for efficiency upgrades.

From an industrial scenario standpoint, demand is being reinforced by sectors that require continuous air control and contamination-safe processing. The U.S. Department of Agriculture reports that agriculture, food, and related industries contributed about $1.537 trillion to U.S. GDP in 2023, equal to 5.5% of the economy, while U.S. food and beverage manufacturing employed 1.7 million people in 2021. This matters for fans and blowers because food factories, ingredient handling systems, ovens, drying lines, refrigeration rooms, and hygienic compressed-air systems all depend on stable airflow and pressure performance.

Demand visibility is especially strong in food-linked industries, where airflow reliability, hygiene, drying, cooling, dust control, and bulk discharge are operational priorities. FoodDrinkEurope reports that the EU food and drink industry employs 4.7 million people, generates €1.2 trillion in turnover, and creates €250 billion in value added, making it the EU’s largest manufacturing industry.

In the United States, USDA reports that consumers spent $2.58 trillion on food in 2024, including $2.17 trillion on domestically produced food, while the U.S. food and beverage manufacturing sector employed 1.7 million people. This industrial scale supports recurring need for sanitary ventilation, combustion air, odor handling, drying lines, and pneumatic conveying equipment across processing and logistics environments.

Government and regulatory signals continue to influence investment decisions. In January 2025, the U.S. DOE withdrew its proposed conservation standards for fans and blowers, creating a more cautious compliance environment in the short term, but the policy attention itself keeps efficiency measurement and specification discipline high in procurement. Employment for U.S. food processing equipment workers is projected to grow 5% from 2024 to 2034, with about 37,500 openings per year, indicating continued facility activity and equipment demand.

Key Takeaways

- Fans And Blowers Market size is expected to be worth around USD 11.0 Billion by 2035, from USD 6.3 Billion in 2025, growing at a CAGR of 5.7%.

- Centrifugal held a dominant market position, capturing more than a 67.3% share.

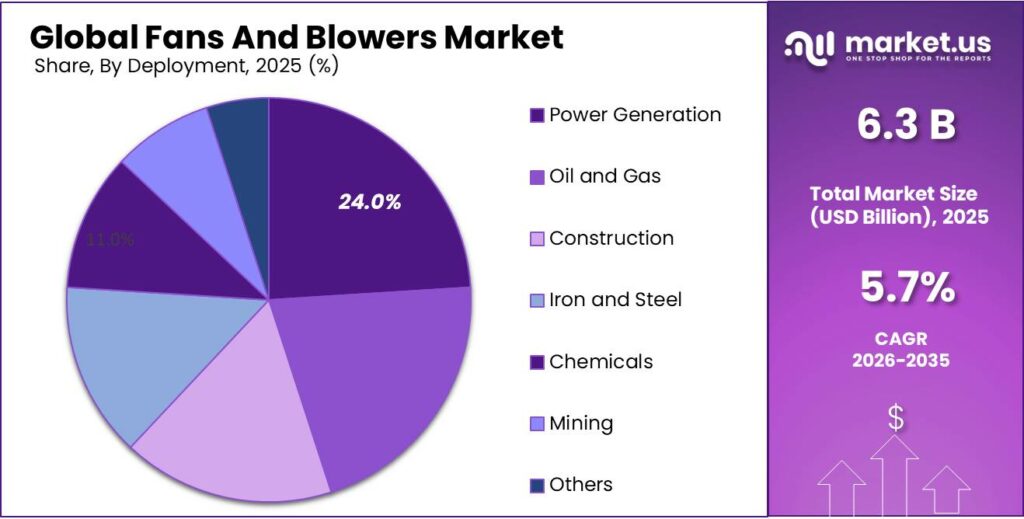

- Power Generation held a dominant market position, capturing more than a 24.8% share.

- Asia Pacific held the dominant position in the global fans and blowers market, accounting for 47.5% share and reaching nearly USD 2.9 Bn.

By Technology Analysis

Centrifugal technology dominates with 67.3% thanks to strong airflow performance and wide industrial use

In 2025, Centrifugal held a dominant market position, capturing more than a 67.3% share. This strong position was mainly supported by its reliable performance in applications that need high-pressure airflow, stable air movement, and better efficiency in controlled environments. Centrifugal fans and blowers are widely preferred across industrial ventilation, HVAC systems, manufacturing plants, dust collection units, and process cooling because they can move air effectively even in systems with resistance from ducts, filters, or bends.

By Deployment Analysis

Power generation leads deployment demand with 24.8% driven by continuous airflow needs in energy plants

In 2025, Power Generation held a dominant market position, capturing more than a 24.8% share. This leadership was largely supported by the critical role fans and blowers play in maintaining efficient operations across thermal, hydro, and renewable power facilities. These systems are extensively used for boiler air supply, flue gas handling, cooling processes, ventilation, and emission control, making them essential to uninterrupted plant performance. The steady expansion of electricity demand, along with ongoing upgrades in aging power infrastructure, continued to support strong deployment across this segment.

Key Market Segments

By Technology

- Centrifugal

- Axial

By Deployment

- Power Generation

- Oil and Gas

- Construction

- Iron and Steel

- Chemicals

- Mining

- Others

Emerging Trends

Smart cold-chain ventilation and energy-efficient airflow systems are the latest trend shaping fans and blowers demand

One of the most important latest trends in the fans and blowers market is the shift toward smart, energy-efficient ventilation systems in food cold chains. Food companies are now moving beyond basic airflow equipment and adopting blower systems integrated with IoT sensors, temperature monitoring, variable speed drives, and predictive maintenance controls. This trend is strongly linked to the growing need to reduce food loss.

- According to FAO’s 2026 update, 526 million tonnes of food, nearly 12% of global food output, is lost due to insufficient refrigeration infrastructure.

Sustainable cooling and solar-powered storage projects are creating the next technology wave

A second major trend is the rise of sustainable cooling infrastructure powered by renewable energy and low-emission refrigeration systems. Governments and global food agencies are increasingly focusing on green cold chains to reduce emissions from food logistics. FAO’s sustainable cooling work highlights that refrigeration-related food systems are becoming a major policy focus, especially in regions facing high post-harvest losses.

A strong recent example comes from food cold-chain expansion projects where energy-efficient cold stores and smart ventilation systems are being linked with solar-assisted refrigeration designs, especially in rural agriculture zones and export clusters. These projects require blowers for condenser airflow, moisture removal, ventilation balancing, and thermal circulation.

Drivers

Expansion of cold chain and food processing infrastructure is a major demand driver for fans and blowers

One major driving factor for the fans and blowers market is the rapid growth of food cold chain and processing infrastructure. Food plants, cold storages, ripening chambers, dairy units, frozen food warehouses, and grain preservation centers all depend heavily on continuous airflow for cooling, drying, moisture control, and ventilation. This is where industrial fans and blowers become essential.

A strong example comes from India’s Ministry of Food Processing Industries, which reported that 395 integrated cold chain projects had been approved by June 2025, with 291 already operational. These projects together created 25.52 lakh metric tonnes of preservation capacity, showing the scale of temperature-controlled infrastructure being added.

Government-backed food security and storage programs are increasing equipment installations

Another strong growth driver is the rise in government-supported food security and storage programs. Public investments in food warehouses, rural silos, pack houses, and refrigerated logistics directly create demand for industrial ventilation systems. FAO’s latest data shows that 31.2% of the world’s food systems value remains linked to core agrifood activities, reflecting the massive size of the infrastructure ecosystem that depends on controlled air circulation.

Governments are also actively funding this expansion. In 2025, India approved an additional ₹1,920 crore under its food processing infrastructure push, taking the total PMKSY allocation to ₹6,520 crore, with a dedicated ₹1,000 crore support for new food irradiation and cold chain facilities. Such projects require reliable blowers for air handling, exhaust, drying, odor control, and temperature balancing.

Restraints

High energy use and rising food storage costs are limiting faster fan and blower adoption

One major restraining factor for the fans and blowers market is the high operating cost linked to continuous energy consumption, especially in food storage and processing environments. In cold rooms, grain silos, dairy plants, and frozen food warehouses, fans and blowers often run 24/7 to maintain airflow, remove moisture, and prevent spoilage.

This creates a major electricity burden for facility operators. The challenge becomes more serious because FAO reports that around 13% of food is lost globally between harvest and retail, much of it during handling, storage, and transport stages where airflow systems are critical.

Poor storage infrastructure and food spoilage losses reduce new equipment investment

Another major restraint comes from weak storage infrastructure in food supply chains, especially in emerging agricultural economies. When warehouses, mandis, and rural cold rooms lack proper insulation, sealed ducts, or moisture control systems, even high-quality fans and blowers cannot deliver full efficiency.

FAO-linked data also shows that more than 700 publications and 29,000+ food loss data points have been recorded globally, highlighting how storage-stage inefficiencies remain a widespread challenge. A practical example often cited in grain handling is that about 10% of food grains can be spoiled in the post-harvest stage, with nearly 6% linked to poor storage conditions.

Opportunity

Expansion of food cold chain networks is creating strong growth opportunities for fans and blowers

One of the biggest growth opportunities for the fans and blowers market is the rapid expansion of food cold chain and preservation infrastructure, especially across developing economies. Every new cold storage, reefer transport hub, food irradiation unit, ripening chamber, and integrated warehouse needs reliable air circulation, condenser cooling, exhaust, and humidity control systems.

This directly opens long-term demand for industrial fans and blowers. A strong example comes from India’s Ministry of Food Processing Industries, which reported that 395 integrated cold chain projects had been approved by June 2025, with 291 already operational. These facilities have already created 25.52 lakh metric tonnes of preservation capacity and 114.66 lakh metric tonnes of processing capacity annually.

Government-backed food processing schemes are opening new installation demand

A second major opportunity is coming from government-led infrastructure funding and subsidy programs, which are accelerating food warehouse and processing expansion. Under India’s PMKSY and related cold chain initiatives, the government approved an additional ₹1,000 crore outlay in 2025 for 50 new food irradiation units, further strengthening temperature-controlled supply systems.

Alongside this, the Agriculture Infrastructure Fund continues to support post-harvest infrastructure with a ₹1 lakh crore financing facility running through FY 2025–26, aimed at storage, silos, warehouses, and community farming assets.

Regional Insights

Asia Pacific dominates the fans and blowers market with 47.5% share, reaching USD 2.9 Bn on the back of industrial expansion

Asia Pacific held the dominant position in the global fans and blowers market, accounting for 47.5% share and reaching nearly USD 2.9 Bn. The region’s leadership is strongly supported by rapid industrialization, large-scale infrastructure projects, and the continuous rise in manufacturing output across China, India, Japan, South Korea, and Southeast Asia. Strong growth in industries such as power generation, chemicals, food processing, mining, cement, and HVAC installation continues to create sustained demand for industrial ventilation and air-handling systems.

The region also benefits from rising commercial and residential construction activity, where fans and blowers are increasingly used in HVAC systems, smoke extraction, and cooling applications. Recent industry trends also show Asia Pacific as the fastest-growing regional market with nearly 7% CAGR through the forecast period, reflecting strong long-term replacement and new installation demand.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Flakt Woods Group SA remains one of the most established names in the fans and blowers market, supported by its strong global HVAC and air-technology network. The company operates across 20+ countries, supported by 13 production sites, 9 centers of excellence, and presence in 65+ countries worldwide, which gives it strong penetration in industrial ventilation and critical air solutions. Its estimated annual revenue stands close to USD 864.5 Mn, supported by 2,000–5,000 employees globally. Its strength continues to come from energy-efficient ventilation systems and large commercial infrastructure projects.

Greenheck Fan Corp. is a major numerical contributor to the global market, with a particularly strong footprint in commercial ventilation and industrial air movement solutions. The company is supported by manufacturing and distribution operations across multiple North American facilities, with products sold in 70+ countries. Greenheck’s broad line includes centrifugal fans, axial fans, make-up air systems, and air control equipment, making it highly diversified. Its strong replacement demand from commercial buildings, hospitals, data centers, and industrial plants continues to support high shipment volumes and stable annual revenue contribution in the market.

Howden Group Ltd holds a strong engineering-led position in industrial blowers, compressors, and air-gas handling systems. The company generates an estimated USD 203.6 Mn annual revenue with approximately 1,039 employees, while revenue per employee stands near USD 196,000, highlighting strong operational productivity. Its blowers are widely used in mining, power generation, cement, and oil & gas applications where high-pressure air handling is essential. The company’s numerical strength is further supported by its expanding installed industrial base and long-term service contracts, which continue to reinforce its market position globally.

Top Key Players Outlook

- Acme Engineering & Manufacturing Corp.

- Airmaster Fan Company Inc.

- Continental Blower LLC

- CG Power and Industrial Solutions Limited

- DongKun Industrial Co. Ltd.

- Flakt Woods Group SA

- Gardner Denver Inc.

- Greenheck Fan Corp.

- Howden Group Ltd

- Loren Cook Company

- Pollrich GmbH

Recent Industry Developments

Greenheck Fan Corp. strength comes from its deep manufacturing scale and product breadth, with operations supported by multiple U.S. production campuses, 70+ years of market presence since 1947, and an estimated 2,337 employees in 2025, up 2.6% from 2024.

Report Scope

Report Features Description Market Value (2025) USD 6.3 Bn Forecast Revenue (2035) USD 11.0 Bn CAGR (2026-2035) 5.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Centrifugal, Axial), By Deployment (Power Generation, Oil and Gas, Construction, Iron and Steel, Chemicals, Mining, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Acme Engineering & Manufacturing Corp., Airmaster Fan Company Inc., Continental Blower LLC, CG Power and Industrial Solutions Limited, DongKun Industrial Co. Ltd., Flakt Woods Group SA, Gardner Denver Inc., Greenheck Fan Corp., Howden Group Ltd, Loren Cook Company, Pollrich GmbH Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Acme Engineering & Manufacturing Corp.

- Airmaster Fan Company Inc.

- Continental Blower LLC

- CG Power and Industrial Solutions Limited

- DongKun Industrial Co. Ltd.

- Flakt Woods Group SA

- Gardner Denver Inc.

- Greenheck Fan Corp.

- Howden Group Ltd

- Loren Cook Company

- Pollrich GmbH

Our Clients

- 184161

- April 2026