Quick Navigation

Report Overview

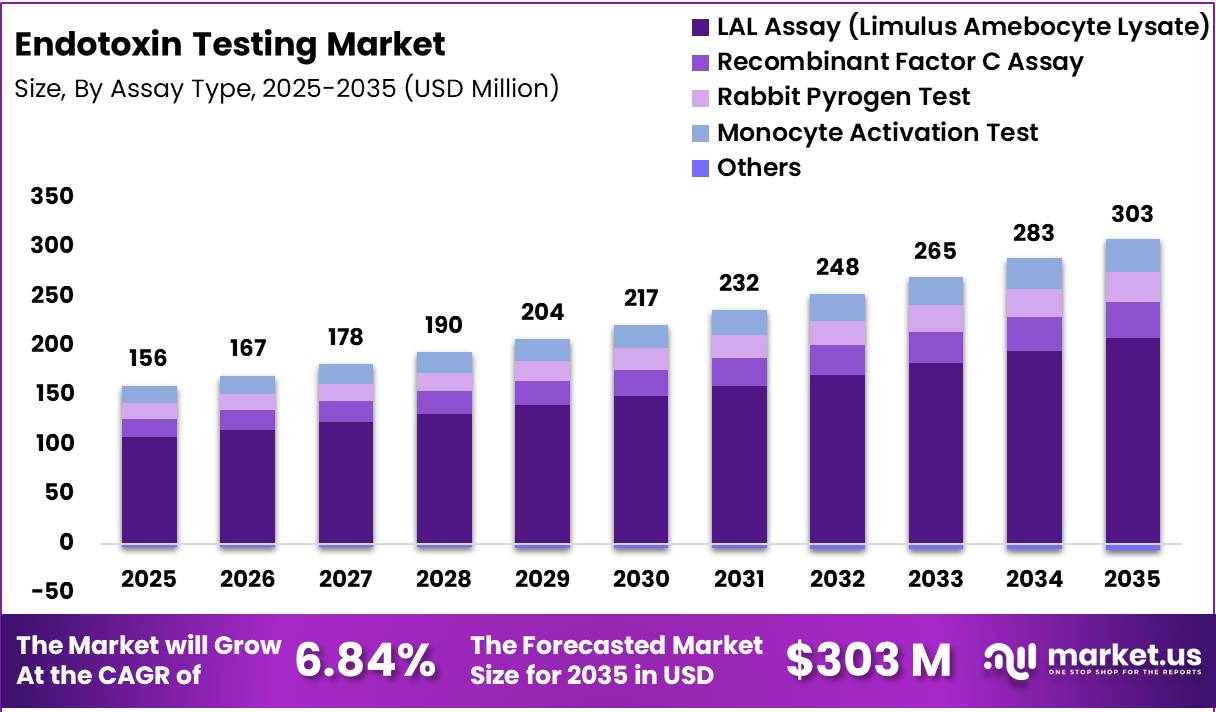

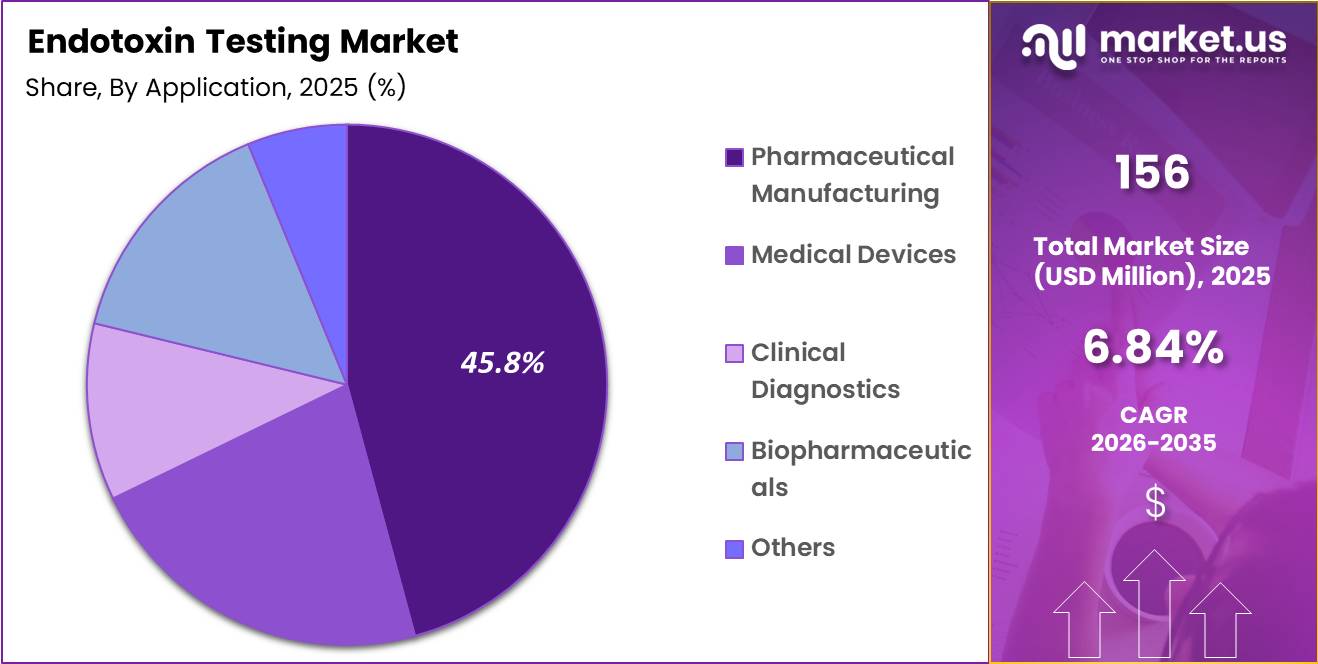

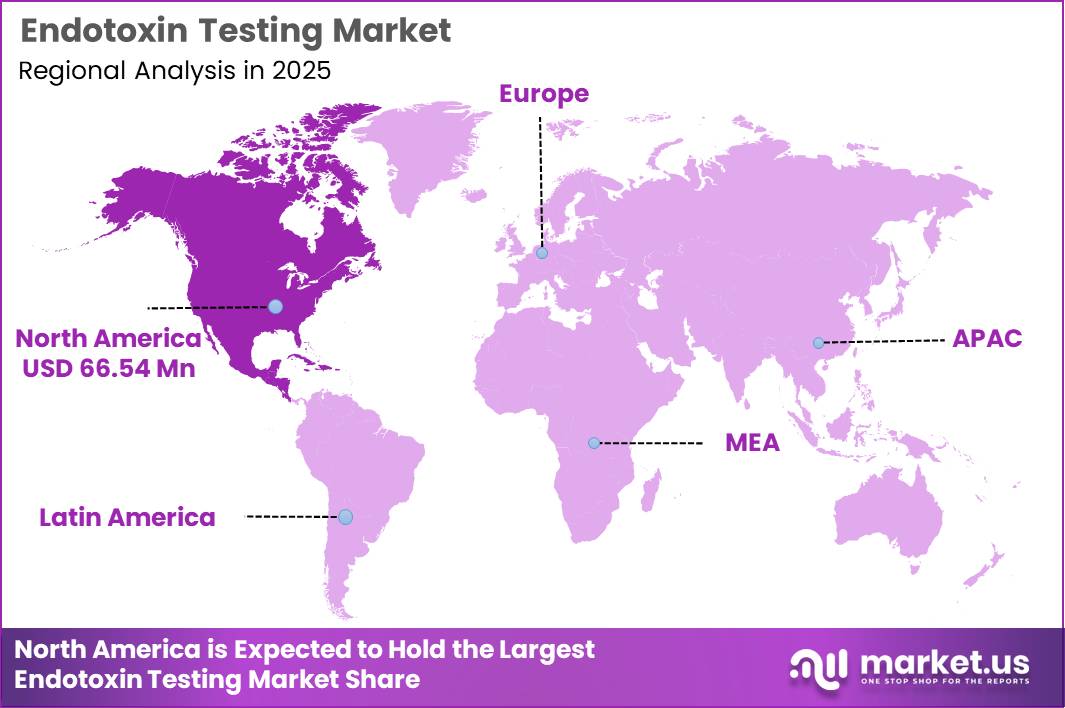

Global Endotoxin Testing Market size is expected to be worth around US$ 303 Million by 2035 from US$ 156 Million in 2025, growing at a CAGR of 6.84% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.60% share with a revenue of US$ 66.54 Million.

Endotoxin testing is a critical quality control process used to detect bacterial endotoxins released by gram-negative organisms. These endotoxins, commonly present in non-sterile environments such as water, air, soil, and through human contact, pose significant risks in healthcare and pharmaceutical applications.

Testing is conducted across multiple stages of product development and manufacturing, including raw material assessment, bulk lot release, and final product validation. It is widely applied across industries such as pharmaceuticals, biopharmaceuticals, medical devices, and research.

The foundation of endotoxin testing can be traced to the 1950s, when the clotting properties of horseshoe crab blood cells were discovered to react with endotoxins. This led to the development of the Limulus Amebocyte Lysate (LAL) test, which was later standardized through regulatory guidelines, enhancing product safety and compliance.

Market growth is being driven by the increasing incidence of healthcare-associated infections (HAIs), which remain a major global concern. These infections, often linked to contaminated medical equipment and inadequate infection control practices, increase the risk of severe complications such as sepsis and inflammation. Endotoxin testing plays a vital role in mitigating these risks by ensuring the safety of injectable drugs and medical devices.

Technological advancements are further strengthening the market. Innovations such as integrated absorbance microplate readers are improving testing accuracy, operational efficiency, and regulatory compliance.

Additionally, strategic acquisitions are expanding testing capabilities and laboratory networks, enabling service providers to meet rising demand. Overall, the endotoxin testing market is expected to experience steady growth, supported by regulatory emphasis on patient safety and ongoing technological progress.

Key Takeaways

- Market Size: Global Endotoxin Testing Market size is expected to be worth around US$ 303 Million by 2035 from US$ 156 Million in 2025, growing at a CAGR of 6.84% during the forecast period from 2026 to 2035.

- Market Share: In 2025, North America led the market, achieving over 42.60% share with a revenue of US$ 66.54 Million.

- Product Analysis: endotoxin testing market is segmented into consumables, instruments, and services. Consumables are projected to dominate the market, accounting for approximately 52.8% of total revenue in 2025.

- Assay Type Analysis: The LAL assay is expected to hold the largest market share of 68.9% in 2025

- Application Analysis: Pharmaceutical manufacturing is anticipated to dominate the segment, capturing approximately 45.8% of the market share in 2025

- End User Analysis: North America led the market, achieving over 42.60% share with a revenue of US$ 66.54 Million.

Product Analysis

The endotoxin testing market is segmented into consumables, instruments, and services. Consumables are projected to dominate the market, accounting for approximately 52.8% of total revenue in 2025. This dominance is attributed to the recurring demand for reagents, assay kits, cartridges, and testing accessories that are essential for routine endotoxin detection processes.

The high frequency of testing in pharmaceutical and biopharmaceutical manufacturing environments has significantly contributed to sustained consumables demand. Additionally, stringent regulatory requirements regarding product safety and sterility have reinforced continuous procurement cycles.

Instruments represent a critical segment, encompassing endotoxin detection systems, readers, and automated platforms. Although capital-intensive, the adoption of technologically advanced instruments has increased due to the need for improved accuracy, sensitivity, and workflow efficiency. Automation trends are further supporting segment growth.

The services segment is expected to witness steady expansion, driven by the growing outsourcing of endotoxin testing to specialized laboratories. This trend is particularly evident among small and mid-sized manufacturers seeking cost optimization and regulatory compliance support. Overall, a balanced growth trajectory is anticipated across all product segments, with consumables maintaining a leading position.

Assay Type Analysis

Based on assay type, the endotoxin testing market is categorized into Limulus Amebocyte Lysate (LAL) assay, Recombinant Factor C (rFC) assay, Rabbit Pyrogen Test, Monocyte Activation Test (MAT), and others.

The LAL assay is expected to hold the largest market share of 68.9% in 2025, driven by its widespread regulatory acceptance, high sensitivity, and established reliability in detecting bacterial endotoxins. Its extensive use across pharmaceutical and medical device industries has solidified its dominant position.

The Recombinant Factor C assay is gaining traction as a sustainable and animal-free alternative to LAL. Increasing regulatory support and advancements in biotechnology are accelerating its adoption, particularly among environmentally conscious organizations.

The Rabbit Pyrogen Test, although historically significant, is witnessing declining usage due to ethical concerns, higher costs, and the availability of in vitro alternatives. Similarly, the Monocyte Activation Test is emerging as a comprehensive solution for detecting both endotoxin and non-endotoxin pyrogens, especially in complex biological products.

Other assay types contribute marginally but offer niche applications. Overall, technological innovation and regulatory evolution are expected to gradually shift market dynamics, although LAL assays will remain dominant in the near term.

Application Analysis

The endotoxin testing market, by application, includes pharmaceutical manufacturing, medical devices, clinical diagnostics, biopharmaceuticals, and others. Pharmaceutical manufacturing is anticipated to dominate the segment, capturing approximately 45.8% of the market share in 2025. This leadership is driven by stringent regulatory frameworks requiring endotoxin testing at multiple stages of drug production, including raw materials, in-process samples, and finished products.

The medical devices segment holds a significant share, supported by increasing production of implantable and injectable devices that necessitate rigorous endotoxin control to ensure patient safety. Regulatory compliance requirements across global markets are reinforcing consistent testing practices in this segment.

Biopharmaceuticals represent a rapidly growing application area due to the expansion of biologics, vaccines, and biosimilars. The complexity of these products necessitates highly sensitive endotoxin detection methods, thereby driving demand.

Clinical diagnostics also contribute to market growth, particularly in laboratory testing and quality assurance procedures. Other applications, including academic research and environmental testing, hold smaller shares but provide incremental growth opportunities. Overall, increased healthcare demand and regulatory oversight continue to support application-based market expansion.

End User Analysis

Based on end users, the endotoxin testing market is segmented into pharmaceutical and biotechnology companies, medical device companies, contract research organizations (CROs), hospitals and diagnostic laboratories, and academic and research institutes.

Pharmaceutical and biotechnology companies are expected to dominate the market, accounting for 48.3% of total share in 2025. This dominance is attributed to large-scale production activities, strict quality control requirements, and continuous investments in drug development and manufacturing processes.

Medical device companies represent a significant segment, driven by regulatory mandates for endotoxin testing in device production, particularly for sterile and implantable products. Increasing innovation in medical technology is further contributing to segment growth.

Contract research organizations are witnessing rising demand due to the growing trend of outsourcing testing services. These organizations provide specialized expertise, cost efficiency, and regulatory compliance support, making them attractive partners for manufacturers.

Hospitals and diagnostic laboratories contribute to steady demand, particularly for clinical validation and safety testing. Academic and research institutes play a smaller yet important role in advancing endotoxin detection technologies. Overall, strong regulatory frameworks and increasing outsourcing trends are shaping end-user dynamics in the market.

Key Market Segments

By Product

- Instruments

- Consumables

- Services

By Assay Type

- LAL Assay (Limulus Amebocyte Lysate)

- Recombinant Factor C Assay

- Rabbit Pyrogen Test

- Monocyte Activation Test

- Others

By Application

- Pharmaceutical Manufacturing

- Medical Devices

- Clinical Diagnostics

- Biopharmaceuticals

- Others

By End User

- Pharmaceutical and Biotechnology Companies

- Medical Device Companies

- Contract Research Organizations

- Hospitals and Diagnostic Laboratories

- Academic and Research Institutes

Driving Factors

The growth of the endotoxin testing market is strongly driven by stringent regulatory requirements imposed by global health authorities such as the U.S. Food and Drug Administration and pharmacopeial standards. Endotoxins, primarily lipopolysaccharides from Gram-negative bacteria, are highly pyrogenic and can induce severe immune responses even at low concentrations.

Regulatory frameworks mandate strict endotoxin limits for parenteral drugs and medical devices. For instance, the FDA specifies an endotoxin threshold of 5.0 endotoxin units (EU)/kg body weight for most injectable drugs, while more sensitive applications such as intrathecal injections are limited to 0.2 EU/kg.

Additionally, numerical limits such as 0.5 EU/mL for certain sterile products highlight the need for accurate and sensitive testing methodologies. These regulatory thresholds have significantly increased the adoption of validated methods like Limulus Amebocyte Lysate (LAL) assays across pharmaceutical manufacturing.

The expansion of biologics and injectable drug pipelines further reinforces this demand, as these products require stringent endotoxin monitoring throughout production. Consequently, regulatory compliance has become a primary growth catalyst for endotoxin testing technologies globally.

Trending Factors

A key trend observed in the endotoxin testing market is the transition toward advanced and alternative testing technologies that enhance sensitivity, reproducibility, and ethical compliance. Traditional LAL-based methods—such as gel-clot, chromogenic, and turbidimetric assays—remain widely used and are recognized by the U.S. Food and Drug Administration for product release testing. However, there is increasing interest in recombinant factor C (rFC)-based assays and automated endotoxin detection systems.

This shift is supported by the need for standardized and quantitative outputs. Industry observations indicate variability in definitions such as “low endotoxin,” which may range from <0.5 EU/mL to <5 EU/mL, reflecting inconsistency in conventional testing interpretations. Consequently, automated and digital platforms are being adopted to improve data accuracy and comparability.

Furthermore, regulatory guidance increasingly emphasizes validation, inter-laboratory reproducibility, and precision testing, including multi-site evaluations for assay performance. These developments indicate a gradual but clear shift toward technologically advanced, standardized, and animal-free endotoxin testing approaches.

Restraining Factors

Despite strong regulatory support, the endotoxin testing market faces several operational and technical restraints. One major limitation is the complexity and variability associated with test performance and interpretation.

According to guidance from the U.S. Food and Drug Administration, endotoxin assays must meet strict validation criteria, including precision, reproducibility, and interference testing across multiple conditions. These requirements increase both time and cost burdens for manufacturers.

Additionally, the LAL assay, the most widely used method, has inherent limitations. Variability can occur due to product interference, dilution factors, and sensitivity thresholds. For example, excessive dilution beyond the maximum valid dilution (MVD) may lead to false-negative results, masking harmful endotoxin levels.

Another constraint is the lack of universally standardized definitions for endotoxin levels in non-compendial products, where terms such as “endotoxin-free” are inconsistently applied. This lack of harmonization can reduce comparability across laboratories and regions. Collectively, these technical and regulatory complexities act as barriers to streamlined adoption and scalability of endotoxin testing solutions.

Opportunity

Significant opportunities are emerging in the endotoxin testing market due to the expansion of biologics, personalized medicine, and advanced therapeutics. Regulatory agencies such as the U.S. Food and Drug Administration continue to issue updated guidance for investigational drugs, particularly in high-risk areas such as oncology, where combination therapies require careful endotoxin limit evaluation.

The increasing complexity of drug formulations has heightened the need for customized endotoxin limit calculations, typically based on the formula K/M, where K represents 5 EU/kg and M corresponds to maximum dose exposure. This creates demand for advanced analytical tools capable of handling diverse dosage forms and delivery routes.

Moreover, the growing adoption of single-use systems, cell and gene therapies, and sterile medical devices is expected to expand testing requirements. Emerging markets are also strengthening regulatory frameworks, leading to higher compliance rates and testing volumes.

In parallel, the development of non-animal-based assays and automated platforms presents a strong innovation opportunity, addressing both ethical concerns and operational efficiency. These factors collectively position endotoxin testing as a critical and expanding segment within pharmaceutical quality control.

Regional Analysis

North America

North America represents the leading regional segment in the endotoxin testing market, contributing nearly 42.60% of global revenue. This position is supported by a mature pharmaceutical and biotechnology ecosystem, alongside rigorous regulatory oversight from authorities such as the U.S. Food and Drug Administration.

Advanced healthcare infrastructure, substantial investment in drug discovery, and strong demand for biologics and medical devices continue to drive market expansion. Ongoing investments by key industry participants in research, development, and advanced testing methodologies further reinforce the region’s dominant standing.

Europe

Europe accounts for approximately 30% of the global endotoxin testing market. Market growth is underpinned by stringent regulatory frameworks and increasing demand for high-quality pharmaceutical products and biologics. Regulatory guidance from the European Medicines Agency ensures strict compliance with endotoxin testing standards.

Major contributors include Germany, France, and United Kingdom, where investments in biopharmaceutical innovation remain strong. Additionally, the adoption of recombinant alternatives, such as Factor C-based assays, is increasing as part of efforts to minimize animal-derived testing.

Asia-Pacific

The Asia-Pacific region holds an estimated 20% share of the global market and is projected to register the highest growth rate. Expansion is driven by the rapid development of pharmaceutical and biotechnology sectors, rising healthcare expenditure, and increasing emphasis on regulatory compliance and product safety.

Key markets such as China, Japan, and India are witnessing significant growth due to increased biologics manufacturing, clinical research activities, and the expansion of contract research organizations. Demand for cost-efficient and high-throughput endotoxin testing solutions is expected to accelerate across the region.

Latin America

Latin America contributes approximately 5% to the global endotoxin testing market. Growth is primarily supported by the expansion of pharmaceutical manufacturing capabilities and improvements in healthcare infrastructure. Key markets such as Brazil and Mexico are benefiting from rising healthcare investments and evolving regulatory frameworks focused on enhancing product safety and quality standards.

Middle East & Africa

The Middle East & Africa region accounts for nearly 2% of the global market. Market development is driven by ongoing healthcare sector advancements, increasing pharmaceutical production, and initiatives aimed at strengthening regulatory compliance.

However, limited availability of advanced testing technologies and a shortage of skilled professionals remain key constraints, potentially moderating the pace of market growth in the region.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The report provides a comprehensive assessment of key organizations operating in the global endotoxin testing market, supported by a comparative evaluation based on product portfolios, business overviews, geographic footprint, strategic initiatives, segment-wise market share, and SWOT analysis. Detailed insights into company performance and positioning enable a clear understanding of the competitive landscape.

Additionally, the report delivers an in-depth review of recent industry developments, including product innovations, technological advancements, joint ventures, partnerships, mergers and acquisitions, and strategic alliances. These developments are analyzed to identify emerging trends and strategic directions adopted by leading market participants.

Such structured analysis facilitates an accurate evaluation of competitive intensity and market dynamics. It also enables stakeholders to assess growth strategies, identify potential opportunities, and understand how companies are strengthening their market presence in response to evolving regulatory requirements and increasing demand for advanced endotoxin testing solutions.

Market Key Players

- Lonza Group AG

- Charles River Laboratories International, Inc.

- bioMérieux SA

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Associates of Cape Cod, Inc.

- Wako Chemicals USA, Inc.

- GenScript Biotech Corporation

- Hyglos GmbH

- Pacific BioLabs

- Eli Lilly and Company

- Sanofi S.A.

- Pfizer Inc.

- Novartis AG

- GlaxoSmithKline plc

- Others

Recent Developments

- October 2025 – Lonza Group AG expands rapid microbiology capabilities through acquisition. A strategic acquisition of Redberry SAS was completed to strengthen rapid microbiology and endotoxin testing solutions. The integration of Red One™ technology is expected to enhance automation and reduce testing turnaround time, supporting biopharmaceutical manufacturers in accelerating batch release cycles. This move reflects increasing industry focus on rapid endotoxin detection platforms.

- May 2025 – bioMérieux SA benefits from regulatory shift toward non-animal testing. The implementation of USP Chapter <86> marked a significant regulatory transition, endorsing recombinant and non-animal-derived endotoxin testing methods. This development is expected to accelerate adoption of sustainable testing solutions and reduce reliance on traditional Limulus Amebocyte Lysate (LAL) assays.

- April 2026 – Strong market growth outlook reinforces investment momentum. The broader pharmaceutical microbiology QC testing market was valued at USD 4.07 billion in 2025 and is projected to reach USD 4.6 billion in 2026, reflecting growing demand for endotoxin and sterility testing solutions. This growth trajectory is encouraging leading players such as Pfizer Inc. and Novartis AG to increase internal QC investments.

- 2026 – Market expansion driven by biologics and regulatory pressure. The endotoxin testing market is estimated at USD 2.44 billion in 2026, with continued expansion supported by rising biologics production and stricter compliance requirements. Companies including Sanofi S.A. and GlaxoSmithKline plc are increasing adoption of advanced endotoxin testing platforms to ensure product safety.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 156 Million |

| Forecast Revenue (2035) | US$ 303 Million |

| CAGR (2026-2035) | 6.84% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Instruments, Consumables, Services) By Assay Type (LAL Assay (Limulus Amebocyte Lysate), Recombinant Factor C Assay, Rabbit Pyrogen Test, Monocyte Activation Test, Others) By Application (Pharmaceutical Manufacturing, Medical Devices, Clinical Diagnostics, Biopharmaceuticals, Others) By End User (Pharmaceutical and Biotechnology Companies, Medical Device Companies, Contract Research Organizations, Hospitals and Diagnostic Laboratories, Academic and Research Institutes) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Lonza Group AG, Charles River Laboratories International, Inc., bioMérieux SA, Thermo Fisher Scientific Inc., Merck KGaA, Associates of Cape Cod, Inc., Wako Chemicals USA, Inc., GenScript Biotech Corporation, Hyglos GmbH, Pacific BioLabs, Eli Lilly and Company, Sanofi S.A., Pfizer Inc., Novartis AG, GlaxoSmithKline plc, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |